Meta places a massive 6-gigawatt order, nuclear power stocks surge strongly!

2026 Outlook | Musk, Huang Renxun Issue Collective Warning! Power Shortages Spark New Investment Opportunities; Here's a List of Power 'Goldmines' to Watch

Fellow investors, as we face a brand-new 2026, instead of anxiously chasing trends, it's better to calmly understand the direction. Stay tuned.@Niuniu Classroomto unlock your investment roadmap in real time. In the new year, let’s stay calm and patient, proceed steadily for long-term success, and slowly grow our wealth together.

Electricity is increasingly becoming the Sword of Damocles that constrains AI development.

Tech giants like Musk, Huang Renxun, and OpenAI CEO Sam Altman have all expressed concerns about power shortages.

More notably, former US President Trump pointed out that he would use an 'energy emergency status' to approve the expedited construction of AI power plants. Microsoft CEO Nadella admitted that the company faces an unprecedented dilemma: 'We have piles of GPUs, but due to power shortages and lack of space, they can only remain idle.'

In addition,Overnight, the US government announced it will allocate $Centrus Energy (LEU.US)$and another two nuclear fuel manufacturers $900 million each,totaling approximately $2.7 billion. This move aims to restart domestic nuclear fuel production and gradually reduce dependence on Russian enriched uranium.

In fact, in this era where technology competes for the future, the key constraint on AI development has shifted from 'computing power shortage' to 'electricity shortage.'

Looking ahead to 2026, where will the capital flow indicators point? After an in-depth analysis, Chip、Optical communications、StorageNext, we will focus on a key component of the AI landscape and exclusively reveal to fellow investors: why is the power sector so important? Which companies are worth watching?

Why is the power sector so important?

Why is there a power shortage caused by North American AIDC? In short,The explosive growth of AI data centers has created new electricity demands, which have led to a power gap due to the slow growth of U.S. power sources and an aging power grid that cannot meet these demands.

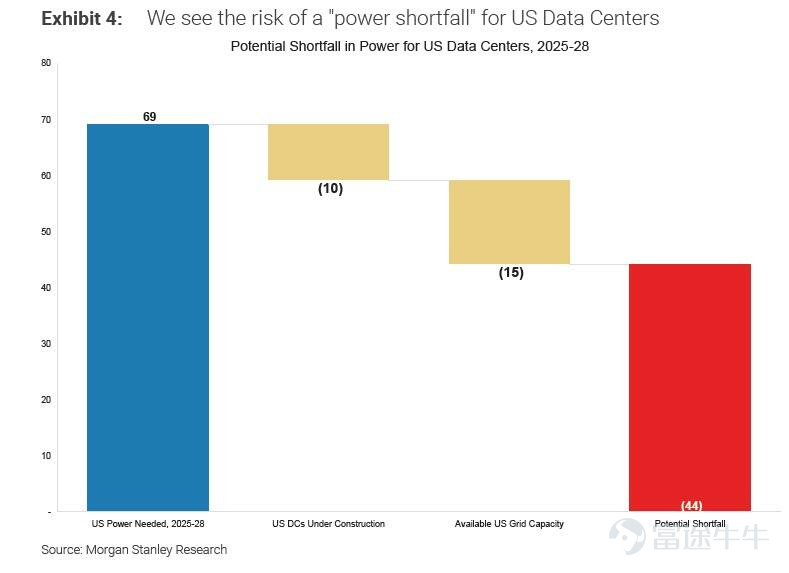

According to a Morgan Stanley research report, by 2028, the total electricity demand for U.S. data centers is expected to reach approximately 69 gigawatts (GW). Of this, about 10 GW will come from data centers under construction, and another 15 GW can be connected via the existing power grid, but there will still be a power gap of approximately 44 GW.

![Fellow investors, as we face a brand-new 2026, instead of anxiously chasing trends, it's better to calmly understand the direction. Stay tuned.[Share Link: @Niuniu Classroom]to unlock your investment roadmap in real time. In the new year, let’s stay calm and patient, proceed steadily for long-term success, and slowly grow our wealth together. Electricity is increasingly becoming the Sword of Damocles that constrains AI development. Tech giants like Musk, Huang Renxun, and OpenAI CEO Sam Altman have all expressed concerns about power shortages. More notably, former US President Trump pointed out that he would use an 'energy emergency status' to approve the expedited construction of AI power plants. Microsoft CEO Nadella admitted that the company faces an unprecedented dilemma: 'We have piles of GPUs, but due to power shortages and lack of space, they can only remain idle.' In addition,Overnight, the US government announced it will allocate $Centrus Energy (LEU.US)$and another two nuclear fuel manufacturers $900 million each,totaling approximately $2.7 billion. This move aims to restart domestic nuclear fuel production and gradually reduce dependence on Russian enriched uranium. In fact, in this era where technology competes for the future, the key constraint on AI development has shifted from 'computing power shortage' to 'electricity shortage.' Looking ahead to 2026, where will the capital flow indicators point? After an in-depth analysis, [Share Link: Chip]、[Share Link: Optical communications]、[Share Link: Storage]Next, we will focus on a key part of the AI landscape, exclusively for fellow investors...](https://nnqimage.futunn.com/sns_client_feed/900080/20260106/web-1767688012656-IAWdRRXOSJ.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

According to a recent report by SemiAnalysis,The power grid is old and overburdened; processes like queuing, approvals, and capacity expansions can't keep up with the pace of the computing arms race.Data shows that large data centers generate approximately $12 million in annual revenue per megawatt of IT load. This means that if AI projects are halted due to power shortages, the hidden opportunity cost could reach tens of billions of dollars. Faced with power grid connection queues lasting several years, traditional waiting has become economically unacceptable, forcing tech giants to seek fast-deployment alternative power supply solutions as a "lifeline" to maintain growth.

Against the backdrop of an unreliable power grid, 'Bring Your Own Generation' (BYOG) has become an inevitable choice for AI giants. Companies like OpenAI and xAI have abandoned waiting for continuous power grid expansion and have started building their own gas turbine power plants.The xAI Memphis cluster completed the deployment of 100,000 GPU computational power in just four months, driven primarily by the rapid implementation capability of gas turbines.

According to the latest information, xAI has purchased an additional five 380-megawatt natural gas turbines from Doosan Energy of South Korea. The first two units are expected to be delivered by the end of 2026. This will provide power support for over 600,000 GB200NVL72 equivalent-scale clusters (or more than 350,000 VR200NVL144 equivalent-scale clusters).

Source: X

Previously, Google acquired Intersect Power for $4.75 billion in cash plus assumed debt. Intersect is a company specializing in data center and energy infrastructure solutions, offering the fastest, cheapest, cleanest, and most reliable energy solutions by colocating industrial demands with dedicated natural gas and renewable energy power generation facilities.

Alphabet CEO Sundar Pichai stated in the announcement: "Intersect will help us expand our computing power and energy capacity, allowing us to build new power generation facilities more flexibly and efficiently as new data center loads grow, while reimagining energy solutions to drive U.S. innovation capabilities and global leadership."

Which companies are worth watching?

Overall, the supply-demand gap for electricity in the U.S. may continue to widen. To address the electricity shortage in the U.S., related industrial chains will face new opportunities:

Gas turbineshave emerged as the preferred choice for tech companies' 'self-generated power.' GE Vernova and Siemens Energy’s order schedules are already booked until 2028, reflecting high earnings visibility and pricing power that form the strongest investment rationale currently. Meanwhile,fuel cellsare capturing the high ground of rapid deployment markets thanks to their 'plug-and-play' agility; whereasEnergy storagethey have become the key balancing factor between supply and demand.

Take a long-term view,Nuclear powerwith its ultra-long service life and low marginal cost, remains the optimal solution for a long-term energy foundation; and as AI reshapes infrastructure,power grid equipmentupgrades are equally critical.

We have also compiled a list of companies involved in upstream and midstream power sectors as well as related infrastructure for fellow investors' reference:

![Fellow investors, as we face a brand-new 2026, instead of anxiously chasing trends, it's better to calmly understand the direction. Stay tuned.[Share Link: @Niuniu Classroom]to unlock your investment roadmap in real time. In the new year, let’s stay calm and patient, proceed steadily for long-term success, and slowly grow our wealth together. Electricity is increasingly becoming the Sword of Damocles that constrains AI development. Tech giants like Musk, Huang Renxun, and OpenAI CEO Sam Altman have all expressed concerns about power shortages. More notably, former US President Trump pointed out that he would use an 'energy emergency status' to approve the expedited construction of AI power plants. Microsoft CEO Nadella admitted that the company faces an unprecedented dilemma: 'We have piles of GPUs, but due to power shortages and lack of space, they can only remain idle.' In addition,Overnight, the US government announced it will allocate $Centrus Energy (LEU.US)$and another two nuclear fuel manufacturers $900 million each,totaling approximately $2.7 billion. This move aims to restart domestic nuclear fuel production and gradually reduce dependence on Russian enriched uranium. In fact, in this era where technology competes for the future, the key constraint on AI development has shifted from 'computing power shortage' to 'electricity shortage.' Looking ahead to 2026, where will the capital flow indicators point? After an in-depth analysis, [Share Link: Chip]、[Share Link: Optical communications]、[Share Link: Storage]Next, we will focus on a key part of the AI landscape, exclusively for fellow investors...](https://nnqimage.futunn.com/sns_client_feed/900080/20260106/web-1767688015185-CgQn9HdB0k.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

1. Upstream: Core technologies, equipment manufacturing, and fuel

Nuclear technology and fuel – providing nuclear reactor technology and uranium fuel supply

Nuclear technology and fuel – providing nuclear reactor technology and uranium fuel supplyThis is currently the most heated sector in the market. In particular, SMR (Small Modular Reactor) technology is regarded as a dedicated power source for future data centers. Specifically:

$NuScale Power (SMR.US)$ is the first publicly listed SMR nuclear power company, with its core product being the SMR power module;

$Oklo Inc (OKLO.US)$ focuses on developing small modular reactors (SMRs), a company invested in by 'ChatGPT's father,' Altman;

$NANO Nuclear Energy (NNE.US)$ specializes in developing small modular reactors, covering four key areas of SMR-related content, including manufacturing, fuel, transportation, and other aspects, aiming to create a diversified vertically integrated industrial chain;

$BWX Technologies (BWXT.US)$ focuses on nuclear reactor component manufacturing and nuclear technology. The biggest difference between BWXT and SMR/OKLO is that BWXT serves as a large-scale equipment supplier and technical service provider, primarily offering nuclear reactor components, nuclear fuel, and defense-related nuclear technologies for both government and commercial sectors. Its clients include the U.S. government (such as providing nuclear reactors for naval submarines).

Uranium mining includes $Cameco (CCJ.US)$ 、 $Uranium Energy (UEC.US)$ 、 $Energy Fuels (UUUU.US)$ 、 $Centrus Energy (LEU.US)$ among others.

Gas turbines — Natural gas remains an indispensable transitional and peak-shaving energy source before the full adoption of nuclear power.Amid the construction boom of data centers driven by advancements in artificial intelligence, American AI giants have not only signed substantial agreements for nuclear power procurement but have also hastily revived a technology largely abandoned by the mainstream power industry: gas turbines.

YesterdayThe Underrated AI Winner! GEV's Surge in Orders Doubles Stock Price — Here’s a List of Infrastructure ‘Golden Opportunities’ to Keep HandyA previous article also mentionedGas turbines are currently the most technically mature and mainstream choice.

Currently, the world’s three largest gas turbine suppliers $GE Vernova (GEV.US)$ 、 $SIEMENS AG (SIEGY.US)$ 、 $Mitsubishi Heavy Industries (7011.JP)$ account for nearly 90% of the global gas turbine market share. Additionally, Caterpillar is one of the world’s leading manufacturers of gas engines and industrial gas turbines. In early November, Caterpillar announced plans to more than double its gas turbine production capacity to meet surging demand for natural gas power plants.

SOFC (Fuel Cell) — The New Favorite in AI Power SupplyThe lag in traditional power grids has also opened up a vast market space for 'behind-the-meter' (BTM) power solutions. Among these,fuel cell technology, with its unique advantages, is expected to capture 25% to 50% of the BTM solutions market, equivalent to 8-20 GW of installed capacity.

Fuel cells, particularly solid oxide fuel cells (SOFC), offer structural advantages over traditional gas turbines in terms of delivery time, noise, emissions, and flexibility.

And the company that represents enterprises here is none other than —— $Bloom Energy (BE.US)$ ,By deploying fuel cells on-site at data centers, companies can secure a stable and reliable power supply without waiting for grid upgrades or the construction of new transmission lines. This model not only enables rapid deployment but also provides data center operators with greater energy autonomy and cost control.

$Plug Power (PLUG.US)$ It is a leading enterprise in the global hydrogen fuel cell industry, one of the largest fuel cell integrators worldwide, and one of the highest-valued fuel cell companies globally, known as the first American hydrogen energy stock.

Since its founding in 1997, the company initially focused on stationary fuel cells, later becoming a leader in the fuel cell forklift segment, and in recent years has expanded its industrial chain through external collaborations to include hydrogen supply networks, raw materials, and hydrogen-related sectors,gradually forming a complete full-industry-chain layout.

Additionally, $FuelCell Energy (FCEL.US)$ It is a long-established clean energy technology company,specializing in proprietary molten carbonate fuel cell technology,primarily providing fixed base-load power generation solutions to utility and large industrial customers. Unlike Plug Power, FCEL’s systems excel in efficient 'combined heat and power' using natural gas or biogas, with a unique advantage of integrating carbon capture directly into the power generation process. The company is now actively leveraging its high-temperature technology strengths to enter the hydrogen production and industrial decarbonization markets.

Renewable Energy – A Short-Term Solution to Ease the Power CrisisIn the short term, solar energy and energy storage are solutions to address the power crisis. According to data from the U.S. Energy Information Administration (EIA), the U.S. power grid added 48.6 gigawatts (GW) of new installed capacity, of which approximately 80% was contributed by solar and energy storage. Specifically, this includes 30 GW of utility-scale solar and 10.3 GW of energy storage.

Key areas of focus include: $First Solar (FSLR.US)$ 、 $NextDecade (NEXT.US)$ 、 $Enphase Energy (ENPH.US)$ , and Brookfield, among others. However, attention must also be paid to issues such as poor power supply stability within this industry.

Backup power solution providers$Cummins (CMI.US)$ As the century-old leader in global power systems and the market dominator in data center backup power, it has become the "last line of defense" for tech giants like Microsoft and Amazon against power outages with its highly reliable diesel and natural gas generator sets; meanwhile, the company is aggressively transforming through its Accelera brand, heavily investing in electrolysis-based hydrogen production and fuel cell technologies, aiming to capture both the traditional stable power supply market and the future green energy sector.

$Power Solutions International (PSIX.US)$ This firm specializes in niche engine solutions powered by "alternative fuels," with a core advantage in manufacturing high-specification, low-emission engines compatible with natural gas, propane, and biogas, specifically designed to meet stringent environmental standards; supported by its major shareholder, Weichai Power, it provides data centers and industrial customers pursuing decarbonization with a practical transitional solution that is cleaner than traditional diesel, more mature than hydrogen, and cost-effective.

II. Midstream: Power Generation and Operations

The reason why power generation and operations have become key areas of focus in the current market can be summarized in one sentence: "Scarcity drives value." In the era of AI proliferation, stable and clean electricity has become the scarcest "fuel for computing power."

Previously, this sector was considered a slow-growth "defensive asset" (collecting electricity fees and paying dividends), but now it exhibits growth logic akin to tech stocks. In other words, midstream power generators have transformed from "utilities selling electricity" into "growth companies providing critical infrastructure for AI." Specific companies to watch include:

Independent power producersVertically integrated utilitiesDistributed Energy Services3. Supporting Infrastructure: Grid and Energy Storage

This industry serves as the "regulator and transmitter" — ensuring stable power transmission and addressing the volatility issues associated with renewable energy.

Electrical Equipment and Power Grids$Eaton (ETN.US)$ Eaton is the "power lifeline" and "final safeguard" for AI data centers; in an era where AI chips are causing explosive growth in energy consumption and power density, it provides comprehensive electrical management solutions from grid connection to rack outlets (e.g., high-voltage distribution equipment and UPS uninterruptible power systems). In simple terms, no matter which tech giant wins the AI race, they will all rely on Eaton’s equipment to ensure their expensive GPU computing power is not disrupted by power outages or overloads, making it a highly reliable "pick-and-shovel" winner in AI physical infrastructure.

Energy Storage — Providing battery technology, energy storage system integration, and long-duration energy storage solutions$Tesla (TSLA.US)$ : Not only a leader in electric vehicles,Tesla’s Megapack has become the "industry standard" and "capacity champion" for solving the intermittency challenges of green energy in AI data centers;For tech giants requiring 24/7 stable operations, Tesla provides the fastest-delivered and most integrated large-scale energy storage batteries currently available in the market, serving as critical infrastructure that converts solar energy into stable nighttime computing power fuel for AI.

$Fluence Energy (FLNC.US)$ : A leading energy storage integrator jointly created by Siemens and AES,In the AI era, Fluence plays a role akin to the "intelligent brain of the power grid"; it not only sells battery hardware but excels in utilizing AI-driven software systems for precise power dispatch, providing complex energy management services to hyperscale data centers. It is the preferred partner for tech giants seeking integrated hardware and software solutions while building green data centers.

$QuantumScape (QS.US)$ : Although its main focus currently lies in electric vehicles, QuantumScape’s solid-state batteries, which boast extremely high energy density and are "non-flammable,"are considered a potential upgrade option for future AI infrastructure;for data centers, where fire risk is a major concern and space is at a premium, if their technology achieves mass production, it will provide safer backup power in a smaller form factor, completely eliminating the fire hazards associated with traditional lithium-ion batteries.

$Eos Energy (EOSE.US)$ :offering unique zinc-based battery technology, positioning itself in AI data centers as delivering "ultimate safety" and "lithium alternatives."; since zinc batteries are entirely non-flammable and do not require expensive air conditioning cooling systems, they have become an attractive non-lithium differentiated choice for giants like Microsoft seeking safer alternatives to lithium-ion batteries, especially for backup power needs in the 3-12 hour range.

$ESS Tech (GWH.US)$ :specializing in all-iron flow batteries (Iron Flow), it represents the final piece of the puzzle for AI data centers aiming to achieve "100% round-the-clock green power";while traditional lithium-ion batteries can economically support discharges of up to four hours, ESS's technology is designed for long-duration energy storage (LDES) exceeding 12 hours, specifically addressing the prolonged power gap during the night after sunset, ensuring that AI servers can utilize inexpensive renewable energy stored during the day even at night.

$Microvast (MVST.US)$ : although initially focused on commercial heavy-duty truck batteries, it positions itself in the AI energy sector as a provider of high-performance industrial-grade battery components; its battery technology is characterized by high-rate charge-discharge capabilities and ultra-long cycle life, making it particularly suitable for data center energy storage systems that need to handle sudden load fluctuations (e.g., AI training peaks), offering high-power-density cell solutions for specific high-end industrial energy storage demands.

Summary

When power becomes a bottleneck, 'speed' and 'stability' become the most valuable commodities.This means the focus of investment logic must shift: it’s no longer just about who is in the race, but who can actually deliver the product. Equipment manufacturers with rapid capacity expansion and strong delivery capabilities are the true 'picks-and-shovels stocks' in this round of infrastructure growth.

Fellow investors may also refer to previous articles in the 2026 outlook series.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (7)

to post a comment

225

664