【2026展望】提前部署!分享你睇好嘅投資機會

2026年展望|中美競逐新戰場!機器人行業或迎「商業化大考」,大摩點名了哪些核心公司?

2025年,人形機器人正式開啟從「秀場」走向「工廠」的量產元年。隨著宇樹、 $特斯拉 (TSLA.US)$ 、FigureAI等國內外頂尖玩家實現商用交付,行業基本面已發生質變:人形機器人不再只是展會上的科技圖騰,而是轉化為真實的生產力。這一躍遷,宣告了規模化應用時代的全面到來。

值得關注的是,機器人行業已經成為美國與全球其他大經濟體競爭的下一個主要戰場。此前,美國商務部長盧特尼克頻繁會見機器人產業的CEO,在「全力支持」(all in)該產業加快發展,也稱特朗普政府正考慮明年發布一項關於機器人的行政命令。

此外,作為全球產業進程的節拍器,特斯拉第三代人形機器人(Gen3)的量產路徑已愈發清晰。2025年12月初,Optimus團隊公布了最新視頻,展示機器人在復雜地面上穩健跑步的能力,與早期步履蹣跚的形象形成代際對比,證明其在 「小腦」層面(負責運動控制)的實質性跨越。

與此同時,中國方面,宇樹科技、樂居智慧、智元機器人等人形機器人頭部整機廠密集啟動IPO、併購上市等資本化動作,產業開始邁入「產業化+資本化」雙輪驅動的爆發前夜。

展望2026年,業內普遍視為機器人企業的商業化「大考年」,資本市場不在滿足於精彩的技術演示及宏大的敘事,而是要求清晰的盈利路徑和可持續性的商業模式,或許自我造血能力不足的企業將會面臨一定的風險。

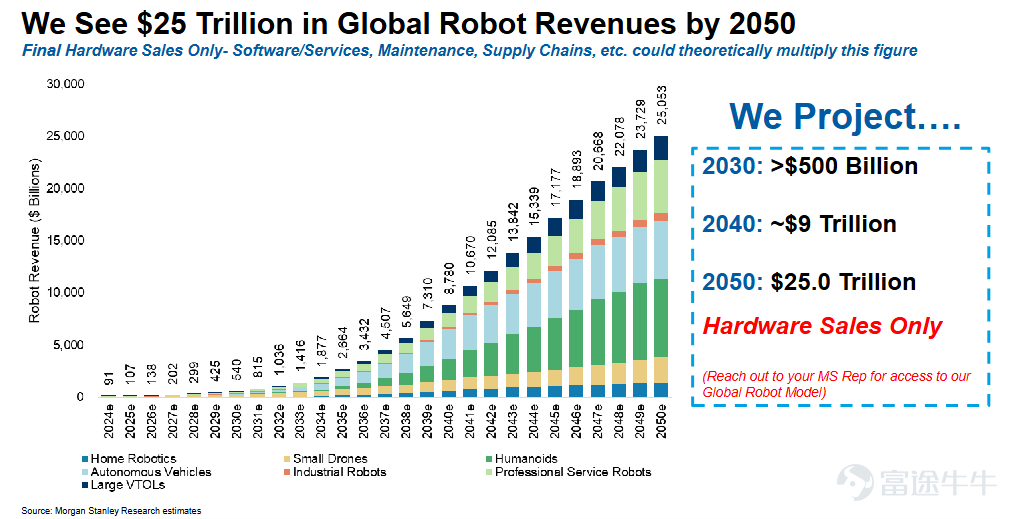

摩根士丹利全球具身AI團隊在最新發布的《機器人年鑑》中預測,基準情形下,全球機器人硬件銷售額將從2025年的約1000億美元激增至2030年的5000億美元,2040年達到9萬億美元,並在2050年攀升至25萬億美元。此預測僅涵蓋硬件銷售,若加上軟件服務、維護及供應鏈相關收入,市場規模可能會倍增。

來源:摩根士丹利

大摩透過其全球機器人模型預測,到2050年全球將銷售14億台機器人,運作中的機器人總數將達到65億台。機器人形態將高度多樣化,包括工業機器人、服務機器人、無人機、自動駕駛車輛、類人機器人、家用機器人等,涵蓋從製造業到醫療、農業、交通、國防、太空探索等各類應用場景。

根據大摩測算,2030年全球將售出約9000萬台機器人,2040年這數字將增加至6億台。其中,小型無人機和家用機器人在近期最具市場潛力,而人形機器人預計在2029-2030年開始規模化部署。

2026年,機器人行業有哪些值得關注?

隨著產業步入量產前夕,各環節價值與投資節奏正在重新評估。當前,價值創造高度集中于上游核心零部件,尤其是構成執行系統的旋轉關節、線性關節(總成),其價值量占比可高達近70%。

具體而言,電機、減速器、絲杠的精密制造與集成是降本增效的關鍵,相關企業正經歷從樣品送樣(A/B樣)到獲取小批量訂單(RFQ)的關鍵驗證期,這是當下最具確定性的投資主線。

同時,靈巧手、六維力傳感器、3D視覺傳感器等關乎機器人精細操作與環境感知的環節,作為技術制高點和下一代硬件創新方向,亦持續受到市場追捧。

大摩報告特別指出,在具身智能競賽中,數據收集與製造能力密不可分。要製造出優秀的機器人,必須先製造大量「不完美」的機器人進行資料收集和模型訓練。原型機相對容易,但規模化生產才是真正的挑戰。大摩給出了機器人時代值得關注的100家公司,牛牛篩選出港美股相關概念股,供牛友們參考:

![牛友們,2025即將翻篇,面對全新的2026,與其焦慮地追逐風口,不如靜下心來看懂風向。追蹤 [鏈接: @牛牛課堂],第一時間解鎖你的投資地圖。新的一年,咱們不急不躁,行穩致遠,一起慢慢變富。 2025年,人形機器人正式開啟從「秀場」走向「工廠」的量產元年。隨著宇樹、 $特斯拉 (TSLA.US)$ 、FigureAI等國內外頂尖玩家實現商用交付,行業基本面已發生質變:人形機器人不再只是展會上的科技圖騰,而是轉化為真實的生產力。這一躍遷,宣告了規模化應用時代的全面到來。 值得關注的是,機器人行業已經成為美國與全球其他大經濟體競爭的下一個主要戰場。此前,美國商務部長盧特尼克頻繁會見機器人產業的CEO,在「全力支持」(all in)該產業加快發展,也稱特朗普政府正考慮明年發布一項關於機器人的行政命令。 此外,作為全球產業進程的節拍器,特斯拉第三代人形機器人(Gen3)的量產路徑已愈發清晰。2025年12月初,Optimus團隊公布了最新視頻,展示機器人在復雜地面上穩健跑步的能力,與早期步履蹣跚的形象形成代際對比,證明...](https://nnqimage.futunn.com/sns_client_feed/900080/20251231/web-1767174084457-rBKRJYKzOY.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

大腦 (Brain) - 軟件與核心運算:

晶片設計及製造包括 $Arm Holdings (ARM.US)$ 、 $新思科技 (SNPS.US)$ 、 $鏗騰電子 (CDNS.US)$ 、 $台積電 (TSM.US)$ 、 $英特爾 (INTC.US)$ 。

身體 (Body) - 硬體與驅動組件:

致動器與零件包括:軸承 $RBC軸承 (RBC.US)$ 、 $鐵姆肯 (TKR.US)$ 、 $Regal Rexnord (RRX.US)$ 、減速器/齒輪 $鐵姆肯 (TKR.US)$ 、 $Regal Rexnord (RRX.US)$ 、 整合式致動器 $Moog-A (MOG.A.US)$ 、 $Regal Rexnord (RRX.US)$ 、 $三花智控 (02050.HK)$ 、馬達 $Sensata Technologies (ST.US)$ 、 $Regal Rexnord (RRX.US)$ 、 $瑞薩電子(ADR) (RNECY.US)$ 、編碼器 $Novanta (NOVT.US)$ 、 $Sensata Technologies (ST.US)$ 、稀土/磁材 $MP Materials (MP.US)$ 、 $金力永磁 (06680.HK)$ ;

感測器包括:雷達與激光雷達 $曼格納國際 (MGA.US)$ 、 $英特爾 (INTC.US)$ 、 $Aptiv PLC (APTV.US)$、 $Teledyne Technologies (TDY.US)$;磁性感應器 $Allegro Microsystems (ALGM.US)$; 力矩感應器 $Novanta (NOVT.US)$ 、 $Sensata Technologies (ST.US)$ 、 $泰科電子 (TEL.US)$ ;視覺感應器 $Teledyne Technologies (TDY.US)$ 、 $英特爾 (INTC.US)$ 、 $安森美半導體 (ON.US)$ 、 $泰科電子 (TEL.US)$ 、 $索尼 (SONY.US)$ 、 $速騰聚創 (02498.HK)$ ;

機身/有線控制/散熱包括 $曼格納國際 (MGA.US)$ 、 $安費諾 (APH.US)$ 、 $泰科電子 (TEL.US)$ 、 $Aptiv PLC (APTV.US)$ 、 $三花智控 (02050.HK)$ ;

整合商- 終端製造商:

更值得關注的是,摩根士丹利重磅發布的「Humanoid Tech 25」名單,該行在報告中建議投資者,把目光投向機器內部,鎖定提供「大腦」(AI)、「眼睛」(感測器)和「身體」(執行器)的供應商,而不是機器人品牌本身。這一變化本身就釋放出一個重要信號:產業關注重心,正在從整機展示轉向底層能力。

![牛友們,2025即將翻篇,面對全新的2026,與其焦慮地追逐風口,不如靜下心來看懂風向。追蹤 [鏈接: @牛牛課堂],第一時間解鎖你的投資地圖。新的一年,咱們不急不躁,行穩致遠,一起慢慢變富。 2025年,人形機器人正式開啟從「秀場」走向「工廠」的量產元年。隨著宇樹、 $特斯拉 (TSLA.US)$ 、FigureAI等國內外頂尖玩家實現商用交付,行業基本面已發生質變:人形機器人不再只是展會上的科技圖騰,而是轉化為真實的生產力。這一躍遷,宣告了規模化應用時代的全面到來。 值得關注的是,機器人行業已經成為美國與全球其他大經濟體競爭的下一個主要戰場。此前,美國商務部長盧特尼克頻繁會見機器人產業的CEO,在「全力支持」(all in)該產業加快發展,也稱特朗普政府正考慮明年發布一項關於機器人的行政命令。 此外,作為全球產業進程的節拍器,特斯拉第三代人形機器人(Gen3)的量產路徑已愈發清晰。2025年12月初,Optimus團隊公布了最新視頻,展示機器人在復雜地面上穩健跑步的能力,與早期步履蹣跚的形象形成代際對比,證明...](https://nnqimage.futunn.com/sns_client_feed/900080/20251231/web-1767173690980-n2v44cmrIj.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

摩根士丹利認定為類人機器人時代支柱的關鍵公司:

展望後市,還有什麼值得期待?

2026年機器人將進入從1-10成長階段,野村證券指出,全球人形及四足機器人市場仍處萌芽階段,行業頭部玩家格局清晰:人形機器人領域以特斯拉和Figure AI為主,四足機器人領域則以波士頓動力領跑。

根據野村從供應鏈企業取得的資訊測算,Tesla Optimus或將於2026年3月後啟動產能爬坡,2026年預計交付6萬-8萬台Optimus,到2026年下半年週產能可望達到1000-2000台。

在2026年,中國人形及四足機器人產業的量產進度將趕上特斯拉。野村認為,這主要得益於中國多數企業的產品設計策略——為實現更快量產及更低成本,主動捨棄了高擬人化性能,如採用輪式底盤、非靈巧手方案等。

根據野村測算,2026年優必選、宇樹科技、靈動科技、智元機器人、傅立葉智能、深之藍這六家企業將引領產業產能釋放,基準情境下合計出貨量可達11萬-20萬台(含四足機器人)。

來源;野村

不過,野村認為,2026年人形機器人市場的結構性成長仍受限制,量產節奏的時間節點、頭部企業(如特斯拉第三代Optimus)的最終產品設計、供應鏈份額分配均存變數,短期內難以對產業鏈企業業績形成實質貢獻。

因此,對於特斯拉產業鏈標的,野村更青睞核心非機器人業務具備強勁且明確成長動能的企業,其人形機器人業務應被視為高彈性長期期權,2027-2028年才有望兌現業績,而非2026年的盈利驅動項。

對於中國機器人產業鏈,野村看好兩類企業:一是具備真實技術護城河的企業,二是在關鍵子系統領域佔據主導地位的企業——這類企業將在2026年國內機器人市場迎來20萬台以上出貨浪潮時,獲取超額收益,且隨著當前主流機型(人形、輪式底盤、非靈巧方案)啟動量。

整體而言,野村對核心業務成長紮實且細分領域具備競爭優勢的企業持選擇性樂觀態度。

牛友們還可關注往期2026年展望系列文章:

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論(5)

發表評論

206

387