Fiber optic shortage triggers upstream supply crisis! Will fiber optic stocks keep soaring?

AI 'compute power inflation' has fully erupted! Prices are rising across the board from storage, CPUs to cloud services, with these four sectors raking in massive profits!

Since the beginning of this year, benefiting from the explosive growth of global AI infrastructure and computing power demands, the technology sector's prosperity has continued to rise. Leading US tech giants have strongly pushed the S&P 500 Index to a new historical high.

Beneath the surface of index prosperity, we must recognize the fundamental shift in market trading logic. Currently, the most crucial narrative within the AI investment community has transitioned from early concept hypeto a more predictable 'compute power inflation' rationale.This is not traditional monetary inflation but rather refers to the increased pricing power and value reassessment caused by the scarcity of core hardware resources amid the AI arms race.

Recent developments indicate that price hikes driven by robust AI demand continue to spread—Overseas markets are experiencing another wave of memory price increases, with reports stating that Samsung Electronics and SK Hynix will significantly raise the prices of LPDDRmemoryused in iPhones, driven by AI Agent demand.CPUMoreover, upstream compute power inflation is trickling down to midstreamcloud computingsectors, with Amazon and Google recently announcing theirCloud servicesPrice hikes.

This article will provide a detailed analysis for fellow investors, exploring the key dynamics and investment opportunities in the 'computing power inflation' supply chain.

What are some recent highlights worth watching in the AI sector?

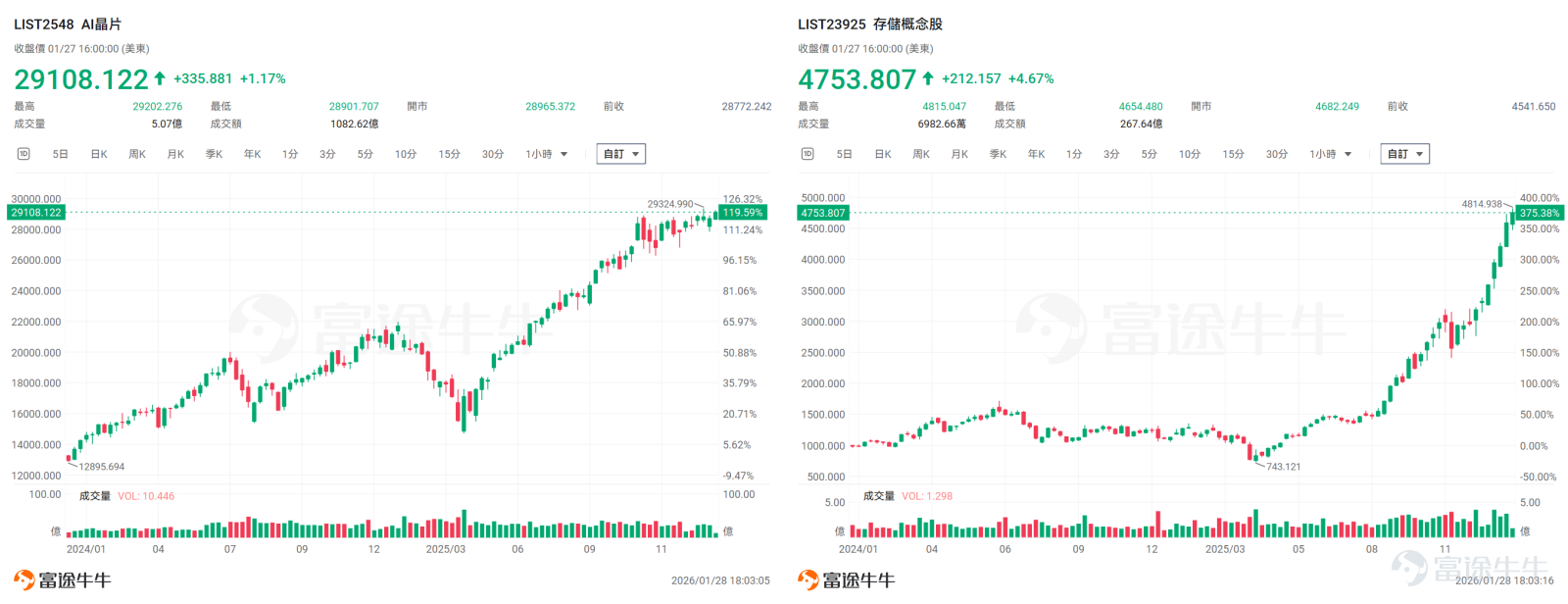

Firstly, driven by the surge in demand from the AI boom, the storage industry is undoubtedly leading price increases,Since the beginning of the year, DDR5 spot prices have risen significantly, while DDR4 spot prices started to increase in September 2024 and continue to trend upwards.

Goldman Sachs expects that this indicates strong upward momentum in DRAM contract prices recently, as DDR5/DDR4 spot prices have already generated substantial premiums compared to contract prices.

The latest channel survey from Goldman Sachs shows that, compared to December contract prices, DDR5/DDR4 spot prices are at a premium of 76%/172%, respectively, driving recent contract price increases and optimism across the industry.

More notably, Samsung Electronics and SK Hynix have recently succeeded in nearly doubling the prices of low-power DRAM supplied to Apple compared to the previous quarter,Marking that even one of the world's largest smartphone manufacturers has had to accept significant price hikes amid tight memory supply.Analysts believe that,This price adjustment breaks Apple's long-standing practice of leveraging its market position to secure low-cost memory, highlighting the severity of the current imbalance between supply and demand in the memory market.

Additionally, within the storage industry, $Seagate Technology (STX.US)$ 、 $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$ companies have successively released better-than-expected earnings results:

Seagate stated that its production capacity for 2026 has already been fully allocated and it has begun discussing 2027 order arrangements with customers. The CEO frankly stated that the current focus of customers has shifted from price to whether they can secure stable supply.

SK Hynix announced its strongest quarterly performance ever, with Q4 operating profit more than doubling year-over-year. The company emphasized that as the artificial intelligence market shifts from training to inference, and with growing demand for distributed architectures, the role of memory will become increasingly critical.Therefore, not only will the demand for high-performance memory such as HBM continue to grow, but the overall demand for memory products, including server DRAM and NAND, will also increase.

Secondly, CPUs have recently entered a phase of price hikes.KeyBanc data shows that due to large-scale cloud service providers 'sweeping up inventory,' Intel and AMD’s server CPU production capacity for all of 2026 has been almost entirely booked. To address extreme supply-demand imbalances and ensure stable future supply,both companies plan to raise server CPU prices by 10-15%.

Guolian Minsheng pointed out that the key focus of computing industry development in the AI era lies in innovations in computing architecture, while the importance of general-purpose computing such as CPUs is expected to further increase. With new computing scenarios emerging, demands for speed and precision are rising, making innovation in computing architecture a focal point for industry growth.As the infrastructure in the computing domain, the importance of CPUs is expected to become even more prominent.

Thirdly, cloud services have also broken the industry's 20-year convention of only decreasing prices, with Amazon AWS and Google Cloud recently announcing price hikes one after another.

$Alphabet-C (GOOG.US)$ Cloud providers announced price increases, effective May 1, 2026, for Google Cloud, CDN Interconnect, Peering, and AI and computing infrastructure services.

$Amazon (AMZN.US)$ AWS recently increased the price of its EC2 machine learning capacity blocks (Capacity Blocks for ML) by approximately 15%, with the hourly cost of the p5e.48xlarge instance rising from $34.61 to $39.80.

Guolian Minsheng Securities summarized in today’s research report thatThe AI supply chain has initiated inflationary transmission, from storage to CPUs, with cloud computing potentially being the next direction for inflation.Continuous growth in AI demand has led to a sequential trend of price increases across different segments of the AI supply chain, starting with storage in the first half of 2025, followed by CPUs in January 2026, and recently cloud computing providers, represented by AWS, also initiating price hikes.

The institution further analyzed that once cloud service providers successfully raise prices on a service without triggering significant customer churn, second and third rounds of price increases will become easier. North American large-scale cloud providers continue to maintain rapid development in their cloud businesses, with strong demand-side momentum also serving as an important basis for price increases.With the growth in AI demand, overall requirements such as AI inference have increased, further driving continuous revenue growth for cloud providers’ cloud businesses.

Finally, optical fiber has seen a very noticeable price increase recently.According to market reports, the latest price of G.652.D has risen to 44 yuan/core km, with an increase of over 80% year-to-date,Optical fiber is expected to become another AI hard currency following storage and CPU.

In addition to the above-mentioned price hike logic, there has been continuous news in the AI market recently, including $NVIDIA (NVDA.US)$ Investment $CoreWeave (CRWV.US)$ 、 $Meta Platforms (META.US)$ Partnering $Corning (GLW.US)$ as well as e-commerce and Clawdbot gaining global popularity.

– NVIDIA announced a $2 billion investment in CoreWeave,to accelerate this data center company’s progress in adding more than 5GW of AI computing power by 2030.This investment will have a significant impact on the cloud market, highlighting the investment boom in the AI infrastructure sector, further elevating the importance of cloud vendors.

– Meta has reached a long-term supply agreement worth up to $6 billion with Corning,to acquire fiber optic cables needed for its data centers. Additionally, it will purchase electricity from Vistra's existing nuclear power plants and support the construction of small modular reactors planned by Oklo and TerraPower LLC within the next decade.

– The explosive popularity of Clawdbot has excited the AI community, being hailed as the 'ChatGPT moment' of 2026.Clawdbot is an open-source AI agent framework, essentially functioning as a 'hands-and-feet-equipped Claude' capable of running on local devices like a Mac mini.

Guolian Securities believes that Clawdbot’s rise represents not only a victory for software but also signals clear opportunities in the edge AI industry chain: the necessity of personal computers acting as 'AI gateways.' This benefits endpoint chip suppliers with strong NPU computing power. As Agent task complexity increases, higher demands will be placed on local CPUs’ multitasking scheduling capabilities.

Moreover, Agents need to store large volumes of Markdown logs and context (RAG). The demand for SSD/NAND will grow alongside the expansion of 'local memory' data; simultaneously, to accelerate local gateway retrieval from vector databases, the adoption rate of high-performance memory (such as HBM or large-capacity high-speed memory) will further increase.

Clawdbot’s architecture, which involves 'frequent cloud requests and local execution,' places extremely high demands on low-latency connections.Optical modules and high-speed connectors that enable efficient connectivity between cloud computing centers and local endpoints remain foundational.

In the age of AI, which companies are worth watching?

From the above, it can be seen that in the AI era,computing power, transport power, storage power, and electrical power intertwine to form a network,supporting the accelerated operation of the entire ecosystem.

computing power determines the upper limit, storage and transport determine efficiency, and electricity determines survival. In the grand narrative of large AI models, the extreme thirst for data driven by computing power must be supported by robust storage capacity and delivered via high-speed transport. These three elements form the 'iron triangle' of AI performance.Electricity, meanwhile, is the physical foundation supporting all of this.At the same time, technological progress is reshaping the energy landscape, enabling a two-way empowerment between power supply and computing efficiency.

The fellow investor has compiled a list of 50 key companies across these four major fields in the AI era for investors' reference:

⚡Computing Power: The 'Brain Engine' of AI

Core Carrier:Responsible for data processing, model training, and inference. Includes companies involved in chip design, manufacturing (contract manufacturing), server assembly, and cloud computing giants providing computational capabilities.

Strategic Value: Computing power is the driving force behind AI, directly determining the efficiency of model training, the speed of inference, and the upper limits of intelligence. It is the core productivity that transforms data into intelligence.

Core Companies:

Chip Design/Equipment:$NVIDIA (NVDA.US)$ 、 $Broadcom (AVGO.US)$ 、 $Advanced Micro Devices (AMD.US)$ 、 $ASML Holding (ASML.US)$ 、 $Arm Holdings (ARM.US)$ ;

Electronics Manufacturing Services:$Celestica (CLS.US)$ 、 $Flex Ltd (FLEX.US)$ 、 $Fabrinet (FN.US)$ 、 $Sanmina (SANM.US)$ ;

Hyperscale Cloud:$Alphabet-A (GOOGL.US)$ 、 $Microsoft (MSFT.US)$ 、 $Amazon (AMZN.US)$ 、 $Oracle (ORCL.US)$ ;

High-Performance Computing:$IREN Ltd (IREN.US)$ 、 $TeraWulf (WULF.US)$ 、 $Cipher Digital (CIFR.US)$ 、 $Hut 8 (HUT.US)$ 。

🚀Transport Capacity: The 'Data Arteries' of AI

Core Carrier: Optical modules, fiber optic cables, high-speed communication equipment.

Strategic Value: Transport capacity determines the bandwidth and latency of data throughput. In cluster computing, transport capacity is the key to connecting isolated computing resources and achieving efficient parallel computation, directly impacting the response speed and system stability of AI implementation.

Core Companies:

Optics/Optical Modules:$Lumentum (LITE.US)$ 、 $Applied Optoelectronics (AAOI.US)$ 、 $Astera Labs (ALAB.US)$ 、 $Coherent (COHR.US)$ 、 $Semtech (SMTC.US)$ ;

Networking Equipment:$Credo Technology (CRDO.US)$ 、 $Arista Networks (ANET.US)$ 、 $Amphenol (APH.US)$ 、 $Ciena (CIEN.US)$ 。

💾 Storage Capability: The 'Resource Pool' of AI

Core Carrier: HBM (High Bandwidth Memory), DRAM, NAND Flash.

Strategic Value: Storage capability is not only the destination for data but also the 'supply station' for computing power. High-performance storage can break through the 'memory wall,' ensuring that massive amounts of data can be accessed by computing resources in real time, which is a prerequisite for maximizing computational performance.

🔋 Electricity: The "Energy Pillar" of AI

Core Carrier: Power distribution equipment, smart grids, nuclear power, etc.

Strategic Value: AI is an "electricity-guzzling behemoth." Electricity not only determines the operating costs of AI data centers but also their sustainability and expansion limits. Stable and affordable electricity is the fundamental guarantee for the long-term development of the AI industry.

Core Companies:

Batteries/energy storage: $Eos Energy (EOSE.US)$ 、 $Solid Power (SLDP.US)$ 、 $Fluence Energy (FLNC.US)$ ;

Energy infrastructure: $Vistra Energy (VST.US)$ 、 $Constellation Energy (CEG.US)$ 、 $Centrus Energy (LEU.US)$ 、 $Oklo Inc (OKLO.US)$ 、 $Bloom Energy (BE.US)$ 、 $Talen Energy (TLN.US)$ 、 $GE Vernova (GEV.US)$ 。

Summary

In the second half of AI development, the focus is on 'hardware' capabilities. Against this backdrop, investors should not limit their attention to models alone but instead concentrate on the physical infrastructure supporting this vast ecosystem. Computing power determines the upper limit of intelligence, transport capacity ensures the efficiency of clusters, storage capacity breaks through data bottlenecks, and electrical power holds the key to the industry’s lifeline.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

152

382