有沒有一種戰法可以穿越牛熊市?

Mabwell Biotech finally passes Hong Kong listing hearing after three attempts: Accumulated losses of 5.7 billion yuan, chairman penalized for short-term trading

Mabwell (Shanghai) Biotechnology Co., Ltd. (hereinafter referred to as Mabwell Biotech), established in 2017, has consistently positioned itself as a leader in innovative drug development since its listing on the Shanghai Stock Exchange STAR Market in January 2022.

The company first submitted its listing application to the Hong Kong Stock Exchange on January 6, 2025. However, the review process was delayed due to an investigation by the CSRC into allegations of short-term trading involving Chairman Liu Datao, causing the initial application to expire on July 6, 2025.

Subsequently, the company refiled its H-share listing application on August 29, 2025, and received the overseas issuance approval notice from the China Securities Regulatory Commission on November 21 of the same year, clearing a key regulatory hurdle. By the end of March 2026, Mabwell Biotech (688062.SH) submitted its third listing application and disclosed its post-hearing prospectus, eventually passing the Hong Kong Stock Exchange's listing hearing in early April 2026, entering the final stage of issuance and listing.

This Hong Kong stock listing plans to issue no more than 62.6646 million overseas-listed ordinary shares. The proceeds will mainly be used for the clinical development of its core product 9MW2821, advancing the oncology and age-related disease pipeline, as well as commercialization efforts. Upon successful listing, Maiwei Biotech will become another innovative biopharmaceutical company with dual 'A+H' listings, further expanding its international financing channels and accelerating R&D and globalization.

Changjiang Securities’ research report highlights that driven by the wave of Chinese innovative drug companies and upstream enterprises going public on the Hong Kong stock market, Hong Kong's role as a key window for Chinese pharmaceutical assets to connect with global capital is expected to strengthen further, bringing more international attention and fair valuation opportunities to high-quality innovative drug companies.

Revenue heavily reliant on out-licensing, ongoing losses remain under pressure

In terms of financial data, Maiwei Biotech’s revenue in 2024 and 2025 was 200 million yuan and 659 million yuan respectively, with a significant year-on-year increase of 229.8% in 2025.

However, this growth primarily relied on out-licensing revenue rather than core drug sales. In 2024 and 2025, the company's drug sales revenue was 145 million yuan and 250 million yuan, accounting for 72.4% and 38.0% of total revenue, respectively; out-licensing revenue was 55.03 million yuan and 409 million yuan, accounting for 27.6% and 62.0% of total revenue, respectively.

Notably, most of the out-licensing revenue in 2025 came from upfront payments or milestone payments made by Qilu Pharmaceutical and Disc, which are non-recurring in nature. This indicates significant uncertainty in the sustainability of the company’s revenue. GF Securities pointed out that out-licensing can improve cash flow in the short term, supporting continued investment in R&D, while in the medium to long term, domestic companies can also learn R&D experience from collaborations, enhancing their clinical operational capabilities. Therefore, out-licensing will remain the preferred strategy for innovative drug companies expanding overseas.

From the product mix perspective, Mailisu® (a biosimilar of denosumab) is the primary revenue source, with sales of 124 million yuan and 203 million yuan in 2024 and 2025 respectively, accounting for over 80% of drug sales revenue. Other marketed products include Maiweijian® (a biosimilar of denosumab for treating giant cell tumor of bone), Mailisheng® (a G-CSF drug for treating febrile neutropenia), and Junmaitong® (a biosimilar of adalimumab), but their sales scale remains relatively small.

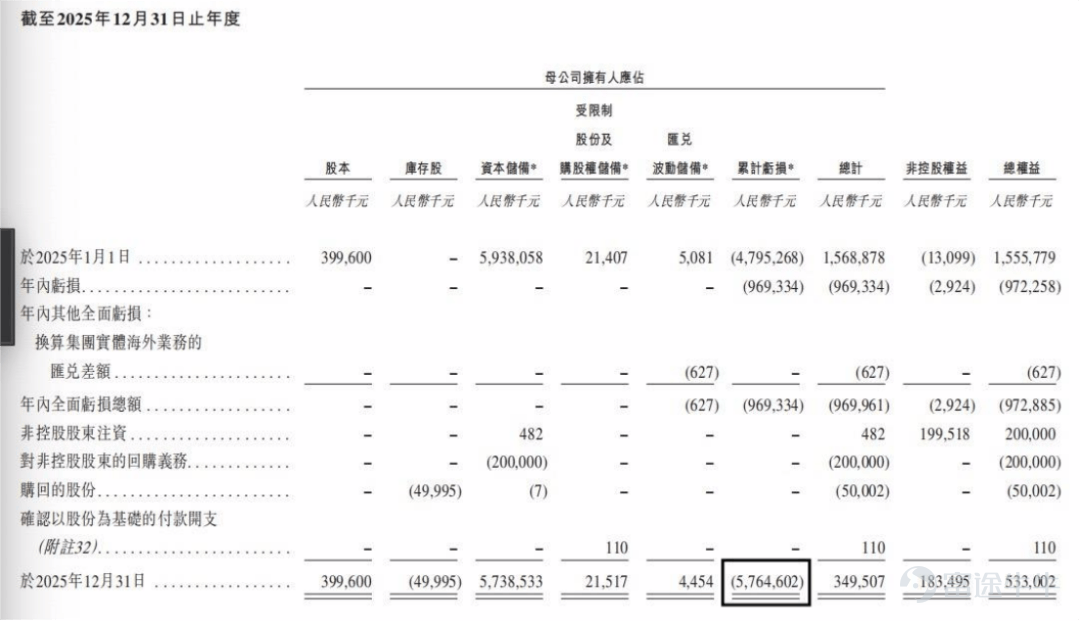

In terms of profitability, the company remains in a continuous loss-making state. In 2024 and 2025, the company's annual losses were 1.047 billion yuan and 972 million yuan, with per-share losses of 2.61 yuan and 2.43 yuan respectively. Although losses narrowed in 2025, accumulated losses continue to grow. As of December 31, 2025, the company's accumulated losses amounted to 5.765 billion yuan.

The company stated that the losses were mainly attributed to R&D expenses, general and administrative expenses, and sales and distribution expenses, with R&D costs being the largest expenditure item, accounting for over 80% of operating expenses.

Renowned financial and auditing expert Liu Zhigeng believes that while Maiwei Biotech's revenue in 2025 surged by 229.8% year-on-year to 659 million yuan, the growth was largely driven by one-off out-licensing revenue (accounting for 62.0%, approximately 409 million yuan). Core drug sales revenue increased to 250 million yuan, but its growth rate (72.71%) lagged far behind total revenue, with its share dropping to 38.0%, indicating a shift from sales-driven to licensing-driven revenue, reflecting insufficient organic growth momentum. Meanwhile, the company remains deeply in the red (net loss of 972 million yuan). Despite a gross margin of 90.27%, the company's R&D spending accounted for 148.3% of revenue, making this 'cash-burning' model unsustainable and profitability highly unstable. This 'high growth' is essentially structural and temporary external funding rather than mature commercial capability, with future sustainability hinging on the ability to secure major licensing deals, drive core product volume growth, and enhance R&D conversion efficiency.

Orient Securities has lowered its revenue and gross margin forecasts for the company in 27 years. The brokerage predicts the net profit attributable to shareholders will be -716 million yuan, -495 million yuan, and 92 million yuan for the years 2026 to 2028 respectively. Using the discounted cash flow valuation method, it estimates a reasonable market value of 17.907 billion yuan for the company, corresponding to a target price of 44.81 yuan. It maintains a 'Buy' rating.

Moreover, the net cash flow from operating activities during the performance record period was negative, at -956 million yuan and -290 million yuan for 2024 and 2025 respectively. The company admits that it has incurred significant operating losses since its establishment and expects this loss-making status to persist in the near term.

In terms of stock price performance, the company’s A-shares have experienced significant fluctuations since their listing on the STAR Market in January 2022. Initially, the stock price surged to over 30 yuan per share but then declined with volatility. In March 2024, the company’s stock was included in the FTSE Global Equity Index, but this did not significantly boost market performance. By the end of 2025, the company's stock price had dropped sharply from its initial high after listing, with market capitalization falling by more than 60%.

Continuous increase in R&D expenses, innovative drugs rely on external collaborations

As an innovative pharmaceutical enterprise, Maiwei Biotech has continued to invest heavily in R&D. For 2024 and 2025, the company’s R&D costs were 783 million yuan and 977 million yuan respectively, marking a year-on-year increase of 24.8%.

Among these, the R&D costs for the core product 9MW2821 were 216 million yuan and 299 million yuan respectively, accounting for 27.6% and 30.6% of R&D expenses, and 18.1% and 20.2% of total operating expenditures. Investments in other products under development, including ADC products like 7MW3711 and 7MW4911 as well as non-ADC products such as 9MW1911 and 9MW3811, also continue to increase.

In terms of the composition of R&D costs, clinical research and technical service fees are the largest expenditure items, amounting to 342 million yuan and 485 million yuan for 2024 and 2025 respectively, accounting for 43.7% and 49.6% of R&D costs. Next are employee salaries and benefits, which were 198 million yuan and 214 million yuan, representing 25.2% and 21.9% of R&D costs respectively.

Furthermore, depreciation and amortization expenses were 97.98 million yuan and 138 million yuan respectively, showing a clear upward trend. Laboratory material costs were 79.87 million yuan and 88.18 million yuan, while other R&D costs were 47.51 million yuan and 52.5 million yuan respectively. R&D costs have continued to rise.

As of the latest practicable date, the company’s R&D team comprises 380 employees, with over 60% holding advanced degrees (more than 12% with doctorates and over 47% with master's degrees). The core R&D personnel consist of seven members covering fields such as chemistry, biology, pharmacology, and medicine, each with over 15 years of average experience in the pharmaceutical industry. In 2024 and 2025, the company collaborated with over 180 and over 200 principal investigators respectively to conduct clinical trials for candidate products. The company has obtained 140 patents globally and filed 276 patent applications, including 25 patents and 17 patent applications related to its core products.

In developing innovative drugs, Maiwei Biotech is highly reliant on external collaborations. The company has signed licensing agreements with multiple domestic and international pharmaceutical enterprises, granting partners the rights to develop and commercialize certain products.

In January 2023, the company entered into an exclusive license agreement with Disc (a clinical-stage pharmaceutical company listed on Nasdaq) for 9MW3011. Under the agreement, the company is entitled to receive up to $412.5 million in upfront payments, milestone payments, and royalties.

In June 2025, the company entered into an exclusive license agreement with Calico (a subsidiary of Alphabet Inc.) for 9MW3811, entitling it to receive more than $600 million in upfront payments, milestone payments, and royalties.

In October 2025, the company entered into an exclusive license agreement with Qilu Pharmaceutical for MaiLiSheng®, securing an aggregate maximum of 500 million yuan in upfront payments and sales milestone payments, as well as double-digit royalties on MaiLiSheng® net sales.

This 'self-developed + external licensing' model, while bringing cash flow to the company in the short term, also means that the company is ceding part of its future earnings to partners. Additionally, several of the company's drug candidates are still in the clinical development stage, with a long way to go before commercialization. The core product 9MW2821 is expected to submit its NDA (New Drug Application) to the National Medical Products Administration no earlier than 2027.

The company admitted that the development of innovative drugs is time-consuming and costly, with uncertain outcomes, and the company may not successfully develop and market its core products. Clinical development is a time-intensive and costly process, and early research and trial results may not predict future trial outcomes.

Rising debt-to-asset ratio; chairman penalized for short-term trading

In terms of financial status, Maiwei Biotech's debt-to-asset ratio has been on the rise. As of December 31, 2024, the company’s total assets amounted to 7.275 billion yuan, with total liabilities at 2.720 billion yuan, resulting in a debt-to-asset ratio of approximately 37.4%. By December 31, 2025, the company’s total assets reached 9.736 billion yuan, while total liabilities rose to 3.952 billion yuan, pushing the debt-to-asset ratio to 40.6%.

Regarding the current ratio, the company's 2024 figure was 1.11, which dropped to 0.90 in 2025. Net current assets shifted from 164 million yuan at the end of 2024 to a net current liability of -220 million yuan by the end of 2025. As of February 28, 2026, net current liabilities further expanded to -380 million yuan.

Yu Fenghui, a senior researcher at the Pangoal Institution, stated that regarding Maiwei Biotech's debt situation, data shows its debt-to-asset ratio increased from 37.4% in 2024 to 40.6% in 2025. Simultaneously, the current ratio fell from 1.11 to 0.90, and net current assets turned negative, expanding to a net current liability of -380 million yuan by early 2026. These indicators reflect significant short-term pressure on debt repayment and liquidity risks for the company. The rise in the debt-to-asset ratio and decline in the current ratio suggest the company relies on debt financing to support operations and expansion, which, to some extent, increases financial costs and risks. Therefore, Maiwei Biotech needs to optimize its capital structure, enhance fund utilization efficiency, and improve cash flow conditions to alleviate the financial burden caused by liabilities and bolster financial stability.

The company admitted that this was primarily due to an increase in contract liabilities (related to upfront payments received from Calico and Kalexo) and higher interest-bearing bank borrowings to support operations.

In terms of debt, as of December 31, 2024, and December 31, 2025, the company's interest-bearing bank borrowings amounted to 2.042 billion yuan and 2.276 billion yuan, respectively, of which the current portions were 1.035 billion yuan and 1.328 billion yuan, respectively. In 2025, the company issued new corporate bonds worth 396 million yuan. As of December 31, 2025, the actual interest rates on the company's bank borrowings ranged from 1.95% to 4.50%. As of February 28, 2026, the company had committed but undrawn credit facilities totaling 1.4 billion yuan. The continuous expansion of the debt scale has put pressure on the company’s financial costs. In 2024 and 2025, the company's financial expenses were 112 million yuan and 111 million yuan, respectively.

More concerning is that the company’s chairman and general manager, Liu Datao, has been penalized by the China Securities Regulatory Commission (CSRC) for suspected short-term trading. According to the prospectus, on July 30, 2025, the Shanghai Regulatory Bureau of the CSRC issued an Administrative Penalty Decision to Liu Datao (chairman, executive director, and general manager of the company), determining that he engaged in short-term trading. Between January 18, 2022, and July 18, 2022, Liu used another person’s securities account to cumulatively purchase 976,567 shares of the company at a total transaction value of 19.2977 million yuan, and sold 634,265 shares at a total transaction value of 13.8836 million yuan. This behavior constituted short-term trading under Chinese securities law. The Shanghai CSRC issued a warning to Liu Datao and imposed a fine of 600,000 yuan.

The prospectus also disclosed that Liu Datao has returned 2.1845 million yuan in short-term trading profits to the company under Article 44 of the Chinese Securities Law, and fully paid the fine on August 7, 2025. The company's directors believe that this incident and the Administrative Penalty Decision do not affect Dr. Liu’s integrity or his eligibility to serve as a director, and will not have any material adverse impact on the company’s operations, financial performance, or business sustainability.

On the commercialization front, as of December 31, 2025, the company has established a distribution network covering more than 327 cities and regions across the country, comprising over 8,000 hospitals and institutions. The distribution network consists of 127 distributors. In 2024 and 2025, revenue generated from sales to distributors was 130 million yuan and 247 million yuan, respectively.

However, all distributors are independent third parties over whom the company has limited control, and the company cannot guarantee that the distributors will always distribute products effectively. Additionally, the company's commercialized products face the risk of being included in centralized procurement programs, which could adversely affect the pricing and profit margins of the company’s products. (Produced by Harbor Finance)

"Harbor Business Observation" Xu Huijing

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1