Oil prices breaking above $100 fuel expectations of rate hikes! Will the Fed act next week?

Tengsi | Japan hikes rates, and Waller scraps forward guidance?! Is the era of yen carry trades coming to an end?

"Japan has raised interest rates."This was the market’s loudest interpretation in March 2024 when the Bank of Japan ended negative interest rates—marking the moment when Japan, the world’s last economy maintaining negative rates, raised interest rates for the first time in seventeen years, lifting its policy rate from minus 0.1% to a range between 0% and 0.1%.

Though seemingly just a modest 0.1% hike, it represented a giant leap in Japan’s monetary policy:

—Both negative interest rates and yield curve control were scrapped on the same day, officially consigning an era of aggressive monetary policy to history.

But what was truly puzzling was the market reaction at the time in 2024: instead of surging after the rate hike, the yen actually fell further against the dollar, breaching the key 150 level once again—an outcome as baffling as if a teacher announced a holiday tomorrow and all the students burst into tears.

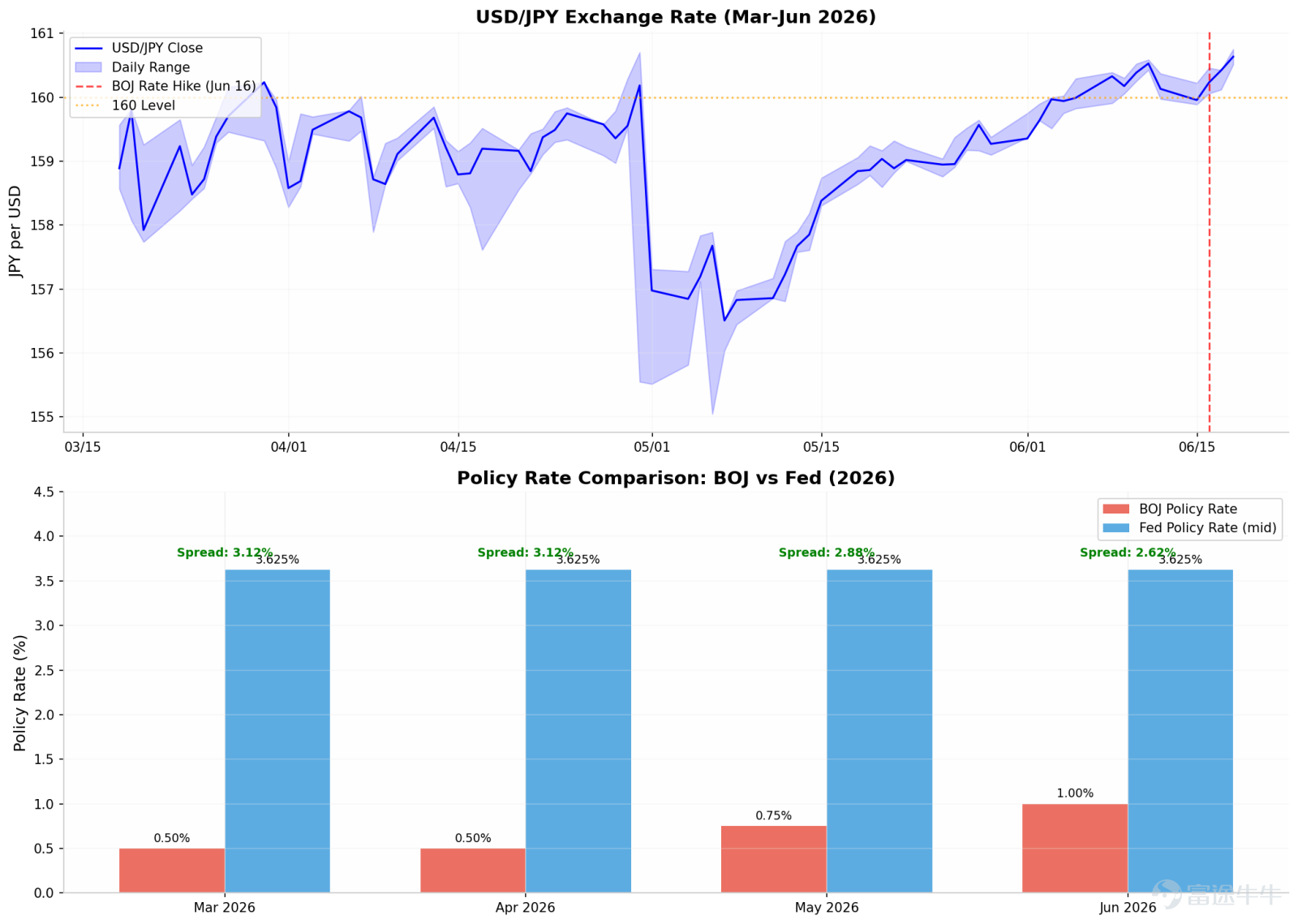

Two years on, by June 2026, the Bank of Japan has already raised rates to 1.0%, the highest level since 1995, yet the yen remains stuck trading between 159 and 160.

CFTC net short positions in the yen exceed 115,000 contracts,reaching the highest level since November 2017。

BCA Researchhas dubbed the yen carry trade"a ticking time bomb"— This is no longera question of 'whether it can still be done'but rather a sign that an era is coming to an end.

Before reading: This article referencesBeware of the impact if the Bank of Japan raises rates to 1%@富途馮文慧 Annaand offers further reflections on it.

The Bank of Japan's rate hike path over the past two years

The Bank of Japan ended negative interest rates and scrapped Yield Curve Control (YCC) in March 2024, raising rates for the first time to a range of 0%–0.1%. It hiked again in July 2024 to 0.25%.

In January 2025, it raised rates to 0.5%, the largest increase since 2007, and further increased them to 0.75% in December 2025—the highest level in thirty years.

In June 2026, the BOJ approved another 25-basis-point hike to 1.0% by a 7-to-1 vote, marking the highest policy rate since 1995. With five rate hikes over two years, the pace has clearly accelerated. The forward guidance stated:“We will continue to raise rates as appropriate based on developments in the economy, prices, and financial conditions.” “Financial conditions will remain accommodative and continue to support economic activity.”。

Market focus has shifted from“whether to hike rates”Shift in directionto “the strength of the wording”—analysts broadly believe that a one-off rate hike alone is unlikely to reverse yen depreciation; clearer signals of sustained tightening are needed to mark the start of an ongoing hiking cycle,Bank of Americawith forecasts pointing to a terminal rate of1.5%. Meanwhile,“timely rate hikes”is an open-ended phrasing that neither commits to another hike in September nor rules it out.

Ministry of Finance Intervention: Tools and 'Half-Life'

The psychological defense line for the Japanese Ministry of Finance is JPY 160 per USD; breaching this level triggers intervention. From April to May 2024, approximately JPY 9.8 trillion pulled the yen back from 160 to around 155, and from June to July, roughly JPY 5.5 trillion pushed the yen up from 161.96 to above 148.5.

Intervention between April 28 and May 27, 2026, reached JPY 11.73 trillion (approximately USD 73.5 billion), setting a new record for the largest single-month intervention ever, aimed at reversing the yen’s slide from a low of 160.72.

Intervention funds were primarily raised by selling U.S. Treasury securities; Japan holds approximately USD 1.17 trillion in U.S. Treasuries, accounting for over 90% of its foreign exchange reserves—creating a“reflexivity paradox”: large-scale intervention itself depresses U.S. Treasury prices and pushes up yields, thereby widening the interest rate differential between the U.S. and Japan.

The Finance Ministry’s verbal warnings follow a clear escalation ladder: from monitoring exchange rates, to taking action if necessary, to decisive responses, to“bold action”(bold action), and then to round-the-clock surveillance.

The current Minister of Finance,Satsuki Katayama,has used increasingly forceful language since assuming office in February 2026, stating on March 27:"Ultimately, decisive action is required—including bold measures.",Jun MuraIssued by the Vice Minister of Finance on April 30"Final warning"。

Historically, interventions have a"half-life"of approximately 2 to 4 weeks—providing a short-term boost of about ¥5, but USD/JPY often retests the pre-intervention highs afterward, making it difficult to reverse the interest rate differential-driven depreciation trend. Under IMF rules, up to three separate interventions within six months are still considered"a free-floating exchange rate regime", which sets the operational ceiling for Japanese authorities.

Why did USD/JPY still break above 160 after the rate hike?

Kazuhiko Ueda’s strategy isto let the market guess for itself, which is precisely the same approach used over the past two yearsof 'raising rates yet seeing the yen weaken'—using minimal policy moves to preserve maximum optionality.

* First, markets price in the path of interest rate differentials, not single policy actions

The core driver of USD/JPY isthe market’s expectation for the path of the U.S.-Japan interest rate differential over the next 12 to 18 monthsDuring the Bank of Japan’s rate hike in March 2024, it simultaneously committed to continuing bond purchases and refrained from providing forward guidance on further tightening—effectively signaling to markets not to expect a series of rate hikes. As a result, the period during which the U.S.-Japan rate differential remained elevated was extended, causing USD/JPY to rise rather than fall.

!["Japan has hiked interest rates."This was the market's most resonant interpretation in March 2024, when the Bank of Japan ended negative interest rates—marking the moment when Japan, the world’s last economy maintaining negative rates, raised its policy rate for the first time in seventeen years, moving it from minus 0.1% to a range between 0% and 0.1%. Although it appears to be only a modest 0.1% hike, it represents a major step forward in Japanese monetary policy: —Negative interest rates and yield curve control were both scrapped on the same day, officially consigning the era of aggressive monetary easing to history. But the truly puzzling part was the market reaction at the time in 2024: instead of surging, the yen actually weakened further against the dollar, breaking below the key level of 150—akin to students bursting into tears when their teacher announces a holiday tomorrow. Two years later, by June 2026, the Bank of Japan had already raised rates to 1.0%, the highest level since 1995, yet the yen remains stuck trading between 159 and 160. CFTC net short positions in yen exceed 115,000 contracts,reaching the highest level since November 2017。 BCA Researchrefers to the yen carry trade as"Time bomb"— This is no longer a question of"whether it can still be done"but rather an issue of an era coming to an end. Reader advisory: This article references[Share Link: Beware of the impact if the Bank of Japan raises rates to 1%]@富途馮文慧 Annaand offers further reflections on it. The Bank of Japan's rate hike path over the past two years Since 2024, the Bank of Japan...](https://nnqimage.futunn.com/sns_client_feed/12486530/20260618/web-1781772573337-zYnqMwjqnI.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

*Second, the 'sincerity' of forward guidance is more valuable than the interest rate itself

The market compares what the central bank did (a 25 bp rate hike) with what it said (maintaining accommodative policy and continuing bond purchases). When verbal cues are more dovish than actual actions, market pricing follows the rhetoric—which explains why the yen briefly declined after both the March 2024 and June 2026 rate hikes, as Ueda’s wording always retained a dovish tone.‘patience’二字。

*Third, positioning crowding determines the intensity of reverse volatility

115,000 short contracts represent a ‘Sword of Damocles’ hanging over the yen—the largest short position in five years—meaning any unexpected hawkish signal could trigger a stampede of short-covering. However, until such a hawkish signal emerges, shorts are instead accelerating their positions during‘the final window’This is precisely the phenomenon we are witnessing right now.

It’s worth noting that the recent surge in oil prices has not caused significant inflation in Japan. Japan’s core CPI from January to April this year remains around 1.4%, well below the BOJ’s 2% target.

Betting on yen depreciation based on the linear assumption that surging oil prices → higher import prices for chemical products → soaring CPI is not a flawless trading logic.

The Mathematical Reality of Yen Carry Trades

The nominal yield spread appears attractive: if you buy $GaoTeng WeValue USD Money Market Fund (HK0000584752.MF)$ , the yield over the past year has been about 3.7%. Subtracting the TONA benchmark rate of 0.727%, this leaves a spread of roughly 2.7%. The breakeven exchange rate is USD/JPY 156.40, and the current rate of 160.63 provides a cushion of approximately 2.6%.

Nominal yield spread (not actual carry trade economics)

However, this“2.7% spread”is significantly overstated—TONA is an overnight unsecured interbank rate reflecting nearly risk-free rates in the Japanese money market, excluding credit and term premiums.

In reality, institutional funding costs could amount to TONA (0.727%) plus a term premium of 0.3%–0.5%, prime broker spreads of 0.5%–1.5%, FX conversion costs of 0.05%–0.1%, and currency hedging costs of 1.0%–2.0%, totaling 2.6%–4.8%.

If you choose not to hedge currency risk, you’re exposed to tail risk from JPY appreciation; if you do hedge, hedging costs substantially erode the spread, leaving a net return of only 0.5%–1.2%—far below the nominal 2.7%. A 3%–5% JPY appreciation (i.e., USD/JPY falling to around 155) would completely wipe out the annual spread.

A consensus in FX trading is:When sizing positions, price for exit risk—not for carry收益.

What impact will Waller's 'missing signal' at the June Fed meeting have on USD/JPY yield spread pricing?

On June 18, the Federal Reserve decided unanimously (12–0) to keep the federal funds rate unchanged at 3.5%–3.75%, but the real shock from this meeting lay not in the rate decision itself, but in the statements made by newly appointed Chair Waller.

Waller himself did not submit a dot plot forecast and described the dot plot as merely"a scenario judgment with an eraser"rather than a commitment to a future policy path;

Among the remaining 18 FOMC participants, half—nine members—expect at least one rate hike this year: three anticipate a 25 bp hike, five foresee a 50 bp increase, and one projects a 75 bp hike; eight expect rates to remain unchanged, and one forecasts a 25 bp cut. The median projected terminal rate for this year stands at 3.8%, 40 bp higher than the March projection, indicating a more hawkish stance than markets anticipated;

The FOMC statement was significantly shortened and explicitly dropped forward guidance. Waller stated that market participants should shift their approach from"relying on the Fed to provide a clear path"Shift in directionto "pricing based on incoming economic data", though he simultaneously criticized economic data for its lagging nature.

The SEP simultaneously revised inflation upward and growth downward: PCE was sharply revised up from 2.7% to 3.6%, core PCE from 2.7% to 3.3%, and GDP down from 2.4% to 2.2%.

This is a classicstagflation signal, with upward revisions to inflation pushing U.S. Treasury yields higher and widening yield spreads, weighing on the yen, while downward revisions to growth heighten recession expectations and boost safe-haven demand, supporting the yen.

CITIC Securitiesjudges that as the U.S. and Iran move closer to a memorandum of understanding and geopolitical energy shocks ease marginally, May is likely to mark the peak of this cycle in U.S. CPI year-over-year growth. Additionally, with Waller facing political pressure from the White House and inclined not to support rate hikes this year, the FOMC’s“even split”stance will ultimately converge toward the Chair’s position,maintaining the view that rates will remain unchanged this year.。

Waller is essentially deferring"Policy Path Anchor"Taking it out of the market's hands will inevitably increase short-term volatility, but from a medium- to long-term perspective, this instead makes U.S.-Japan yield spread pricing increasingly dependent on the BOJ side, with the yen’s direction becoming more and more determined byKazuo Uedawhat he says and does.

Future Scenario Analysis

* Base Case: Orderly Deleveraging

The BOJ gradually hikes rates while the Fed maintains policy moderately; the yen appreciates slowly, existing positions are unwound gradually without severe stampedes—leading to localized volatility but no systemic crisis.

The key condition isthat the BOJ communicates each rate hike well in advance, as in August 2024"Black Monday"Different—the last time was when the market faced"zero-probability expectation"a sudden rate hike, whereas current markets have already fully priced in rate hike expectations, making a repeat of such a sharp shock unlikely.

*Stress scenario: Accelerated reversal

Trigger conditions includethe Bank of Japan (BOJ) hiking rates by more than expected—e.g., a single 50-basis-point move,the Federal Reserve being forced to cut rates rapidly due to an economic recession, geopolitical shocks triggering a global risk-off episode, Japanese authorities intervening massively again in FX markets, forcing concentrated unwinding of yen shorts and creating a self-reinforcing appreciation spiral; emerging market assets and high-valuation tech stocks come under pressure amid tightening global liquidity—similar to October 1998, when USD/JPY plunged from 134 to 120 in a single day.

*Tail-risk scenario: Yield differential disappears entirely

The BOJ’s terminal rate rises to 1.5%–2.0%, while the Fed cuts rates to 2.5%–3.0%, completely eroding the basis for traditional yen carry trades and reshaping global capital flows, with the yen shifting fromfunding currencyis shifting intoan "investment currency"; however, if Japan's 10-year government bond yield rises to 2.5%, the government's interest expenditure in fiscal year 2028 would double compared to fiscal year 2024. This implies that the Bank of Japan’s (BOJ) room for rate hikes is constrained by fiscal considerations, making it unlikely that the interest rate differential will be fully eliminated—though a significant narrowing is highly probable.

In conclusion

Over the past 20 years, the yen has served globally as a"source of free funding"a role now being systematically ended by the Bank of Japan’s policy normalization. The BOJ’s upcoming policy decision could prove more decisive than geopolitical events at any moment.

History shows that every seemingly minor interest rate adjustment by the Bank of Japan can trigger global equity market turbulence; furthermore, the 115,000 short positions could be unwound at any time due to narrowing U.S.–Japan interest rate differentials, potentially causing global capital repatriation and stock market volatility.

Investors should strengthen risk management, control leverage levels, avoid complacency amid market euphoria, and closely monitor three key indicators: $USD/JPY (USDJPY.FX)$ USD/JPY movement (the 160 support level), changes in U.S.–Japan government bond yield spreads, and guidance on the future rate hike path in the Bank of Japan’s post-meeting statement.

!["Japan has hiked interest rates."This was the market's most resonant interpretation in March 2024, when the Bank of Japan ended negative interest rates—marking the moment when Japan, the world’s last economy maintaining negative rates, raised its policy rate for the first time in seventeen years, moving it from minus 0.1% to a range between 0% and 0.1%. Although it appears to be only a modest 0.1% hike, it represents a major step forward in Japanese monetary policy: —Negative interest rates and yield curve control were both scrapped on the same day, officially consigning the era of aggressive monetary easing to history. But the truly puzzling part was the market reaction at the time in 2024: instead of surging, the yen actually weakened further against the dollar, breaking below the key level of 150—akin to students bursting into tears when their teacher announces a holiday tomorrow. Two years later, by June 2026, the Bank of Japan had already raised rates to 1.0%, the highest level since 1995, yet the yen remains stuck trading between 159 and 160. CFTC net short positions in yen exceed 115,000 contracts,reaching the highest level since November 2017。 BCA Researchrefers to the yen carry trade as"Time bomb"— This is no longer a question of"whether it can still be done"but rather an issue of an era coming to an end. Reader advisory: This article references[Share Link: Beware of the impact if the Bank of Japan raises rates to 1%]@富途馮文慧 Annaand offers further reflections on it. The Bank of Japan's rate hike path over the past two years Since 2024, the Bank of Japan...](https://nnqimage.futunn.com/sns_client_feed/12486530/20260618/web-1781772591049-H95MCvrgB8.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

$U.S. 1-Year Treasury Bills Yield (US12M.BD)$$U.S. 5-Year Treasury Notes Yield (US5Y.BD)$ $U.S. 10-Year Treasury Notes Yield (US10Y.BD)$ $U.S. 30-Year Treasury Bonds Yield (US30Y.BD)$ $USD (USDindex.FX)$ $Japan 1-Year Treasury Notes Yield (JP12M.BD)$$Japan 5-Year Treasury Notes Yield (JP5Y.BD)$ $Japan 10-Year Treasury Notes Yield (JP10Y.BD)$ $Japan 30-Year Treasury Notes Yield (JP30Y.BD)$ $Nikkei 225 (.N225.JP)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

9

2