有沒有一種戰法可以穿越牛熊市?

Re-examining Xiao Noodles’ 'trademark controversy'—accusations of corporate bullying: stock price plunges nearly 40%, what lies ahead for its 0.5% market share?

On December 5, 2025, Guangzhou Xiao Noodles Catering Co., Ltd. (hereinafter referred to as Xiao Noodles, HKEX: 2408) officially listed on the Main Board of the Hong Kong Stock Exchange, debuting with fanfare as the 'first Chinese noodle restaurant stock.' At the time, the entire foodservice industry was abuzz with speculation about whether this dark horse in the Chinese noodle segment would accelerate the sector’s capitalization. Its first annual report post-listing appeared impressive—store count continued to grow, and its financial condition improved significantly thanks to IPO proceeds. On the surface, the company seemed firmly on track for rapid scale-driven growth. Yet beneath this veneer of success, structural weaknesses—including low profitability, a capital-intensive model, and persistently high costs—had already planted the seeds of trouble.

In June 2026, a trademark enforcement campaign targeting small family-run shops in county-level towns ignited a public outcry, causing brand sentiment to plummet sharply. Compounded by a sustained post-IPO stock price decline and a wave of prepaid membership refunds, the newly listed restaurant chain found itself caught in a perfect storm spanning operations, public opinion, and capital markets.

Settlement fees of seven to eight thousand yuan versus bowls of noodles priced at just seven to eight yuan

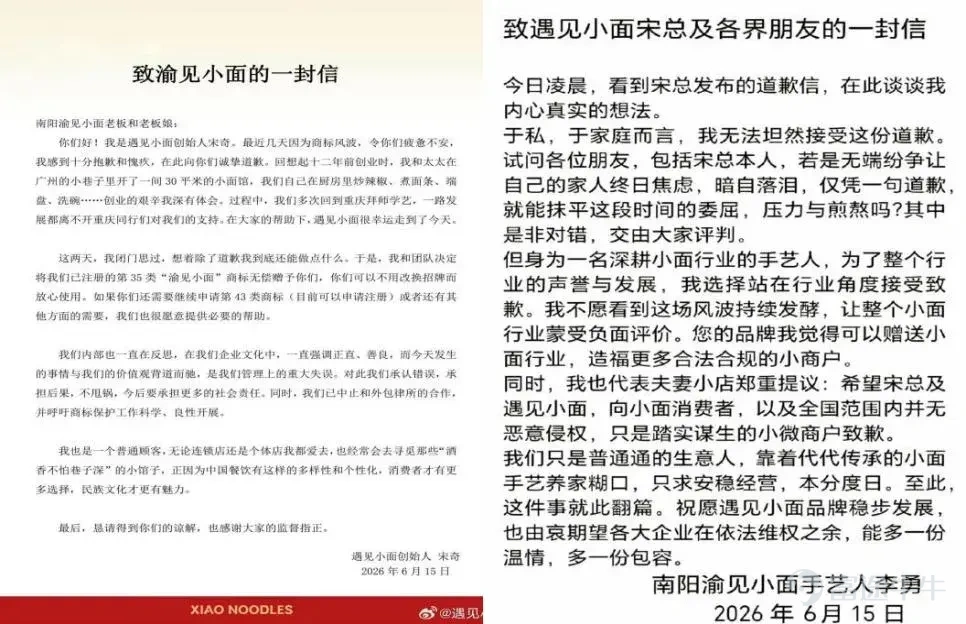

On June 12, 2026, a trademark lawsuit suddenly went viral on social media. Xiao Noodles sued a husband-and-wife-owned noodle shop in Nanyang, Henan Province—named 'Yu Jian Xiao Mian'—demanding several thousand yuan in compensation. Many netizens lamented that small-town businesses already operate on razor-thin margins, and it felt heartless for a large brand to aggressively pursue legal action over a phonetically similar name. Public sentiment quickly turned, with many consumers openly criticizing the brand for lacking magnanimity. As tensions escalated, numerous prepaid cardholders rushed to request refunds, while others complained that the platform’s advertised 'refund anytime' policy was effectively non-functional, fueling mounting dissatisfaction.

Seeing public sentiment spiral out of control, the brand quickly stepped in to mitigate the damage. On June 13, Xiao Noodles officially announced it was dropping its lawsuit and initiating a comprehensive internal review. Just two days later, founder Song Qi issued a public apology, acknowledging this as a serious management failure that contradicted the company’s core values. The brand also decided to transfer the disputed trademark to the husband-and-wife shop free of charge and terminated its relationship with the external law firm involved.

On June 15, the owner of 'Yu Jian Xiao Mian' published an open letter addressed to Song Qi and the broader community on social media, effectively bringing the incident to a close.

Regarding this trademark dispute, the Chongqing Xiao Mian Association released a special statement emphasizing that geographically descriptive public terms should serve the entire industry’s development; supporting enterprises’ lawful and compliant trademark enforcement actions; calling for clearer legal boundaries in such cases; and endorsing the withdrawal of the lawsuit to foster a collaborative and symbiotic industry ecosystem.

Meanwhile, Zhu Dangpeng, a food industry analyst in China, stated,Looking back at this controversy, the founder’s prompt public apology and subsequent remedial measures were commendable. However, the negative impact has already taken hold, and the damage to the brand cannot be underestimated.

On the capital markets front, Xiao Noodles’ stock performance this year has been notably weak.From mid-February to now—just about four months—the company’s share price has declined by more than 37%, reflecting subdued investor confidence and sentiment. Even though the company continued share buybacks in May, this appears insufficient to reverse the trend.

Growth driven primarily by store expansion lacks solid profitability fundamentals.

From a financial perspective, Xiao Noodles’ growth has been largely driven by scale expansion, while profit quality has weakened. In 2025, the company reported revenue of RMB 1.622 billion, up 40.50% from RMB 1.154 billion in 2024. This revenue growth was chiefly fueled by new store openings. By the end of 2025, the company operated 503 stores, a net addition of 143 compared to 360 stores at the end of 2024, directly boosting overall revenue.

Profitability showed even stronger momentum: attributable net profit reached RMB 106 million in 2025, up 74.80% from RMB 60.7 million in 2024, significantly outpacing revenue growth. Nevertheless, this high growth rate has not altered the company’s inherently low-margin nature—its net profit margin in 2025 stood at just 6.54%, consistent with the typically thin margins seen across the Chinese noodle restaurant segment.

Excluding one-time expenses such as listing fees and foreign exchange losses, adjusted net profit for 2025 was RMB 135 million, up from RMB 63.888 million in 2024—an increase of 111.90%. The adjusted net profit margin rose to 8.30%, an improvement of 2.80 percentage points year-over-year, indicating a modest recovery in profitability.

The IPO fundraising has tangibly reshaped the company’s asset structure. Total assets reached RMB 2.083 billion at the end of 2025, up 79.41% from RMB 1.161 billion in 2024, with nearly all of the新增 assets attributable to proceeds from the listing. Liabilities also increased, with total liabilities rising 20.90% year-over-year to RMB 1.261 billion at year-end from RMB 1.043 billion, significantly slower than the pace of asset growth.

The most notable change is the debt-to-asset ratio, which dropped sharply from 89.90% in 2024 to 60.50%, substantially easing short-term debt repayment pressure. Shareholders’ equity also strengthened considerably, reaching RMB 822 million at the end of 2025 compared to just RMB 118 million the previous year, reflecting a much healthier capital structure.

However, one lingering concern remains: rigid lease-related liabilities from store operations are still substantial. Lease liabilities stood at RMB 942 million at year-end, up from RMB 735 million in 2024. With over a thousand stores, rental payments represent a fixed annual cash outflow that will continue to consume cash flow over the long term.

Cash flow performance stands out as one of the few bright spots in the financial report. Net cash flow from operating activities totaled RMB 448 million in 2025, up 42.68% from RMB 314 million in 2024, demonstrating stable cash-generating capability from existing stores. However, the company continues to invest heavily, with net cash outflow from investing activities amounting to RMB 53.804 million, primarily spent on new store fit-outs, equipment purchases, and digital upgrades—reflecting a now-routine pattern of heavy asset investment.

Financing cash flows show clear阶段性 characteristics: the company raised RMB 242 million through its IPO last year, compared to a net outflow of RMB 155 million in 2024, which was mainly used for debt repayment and dividends. In terms of cash reserves, the company redeemed all its wealth management products last year, bringing cash and cash equivalents to RMB 677 million—a very comfortable short-term liquidity position. However, most of this cash is already earmarked, with the bulk allocated for further store expansion, leaving limited room for flexible deployment.

The strategy of scaling up through rapid store expansion has brought Xiao Noodles’ underlying operational issues to the surface. Persistent price competition, asset-heavy operations dragging down efficiency, and uneven store distribution are now intertwined, collectively constraining the brand’s further growth.

Xiao Noodles vividly exemplifies the three unavoidable cost pressures in the restaurant industry: raw materials, labor, and rent. In 2025, raw material and consumables expenses totaled RMB 526 million, up 32.80% year-over-year and accounting for 32.40% of revenue—a slight decline from 34.30% last year, thanks to economies of scale from centralized procurement. Employee-related costs reached RMB 356 million, up 34.30% year-over-year, representing 21.90% of revenue; more stores naturally require more staff, making labor costs difficult to reduce. Rent expenses amounted to RMB 275 million, up 30.70% year-over-year and accounting for 17.00% of revenue—the brand has managed to keep this ratio in check by deliberately selecting non-core commercial locations.

Together, these three cost categories accounted for 71.30% of total revenue, meaning more than 70% of income was consumed by costs. Combined with a one-time listing expense of RMB 27.996 million, profit margins have been squeezed to almost nothing.

Looking at actual store operations, among the 503 stores, 411 are company-operated and only 92 are franchised, giving a direct-operated store ratio of 81.71%—a classic asset-heavy model. Total GMV in 2025 reached RMB 1.812 billion, up 34.38% year-over-year, though this growth rate lagged behind revenue growth. In an effort to attract more customers, the brand proactively lowered prices: average ticket size at company-operated stores fell from RMB 32.10 to RMB 29.90, while franchised stores saw a drop from RMB 31.80 to RMB 28.80.

The price cuts have indeed delivered results: average daily orders per company-operated store rose from 386 to 406, and franchised stores saw an increase from 390 to 412 orders. However, the cost is evident—same-store sales grew by just 1.00% last year, following a 4.20% decline the previous year. While foot traffic increased, average ticket size dropped, effectively canceling each other out and capping per-store profitability.

The sustained low-price strategy has created a vicious cycle. To retain customers amid fierce competition, the brand keeps cutting prices. Although order volume has improved, average ticket size continues to fall. The gains from higher foot traffic fail to offset losses from lower prices, leaving same-store sales growth negligible. Moreover, the long-term focus on affordability has locked in a specific customer base; any attempt to raise prices now to boost margins risks significant customer attrition, leaving the brand stuck between a rock and a hard place.

With store locations heavily concentrated in core cities, where does the goal of capturing 0.5% market share stand?

Xiao Noodles’ high reliance on company-operated stores further drags down operational efficiency. The headquarters handles everything—from site selection and store fit-outs to staffing—for these outlets, resulting in high upfront investment and an average payback period of about 13 months per new store. In contrast, franchised stores are few in number and expanding slowly, failing to leverage a light-asset model to share costs, which keeps management and financial pressure on headquarters persistently high.

The weakness in store distribution is also glaring. Of its 411 company-operated stores, 356 are located in Tier-1 and emerging Tier-1 cities, while only 39 are in Tier-2 and lower-tier cities. This concentration in high-tier urban markets—now saturated and hyper-competitive—has left the brand missing out on substantial growth opportunities in lower-tier markets, where large pools of potential customers remain untapped.

Store closures have become commonplace during expansion. In 2025, while opening 156 new stores, the company shuttered 13 others, primarily due to declining mall foot traffic, rising rents, or mall closures. Rapid expansion has come at the expense of thorough site selection and due diligence, leaving many new outlets fundamentally unprofitable and raising serious concerns about expansion quality.

The recent trademark controversy has further exposed internal management flaws. Weak oversight of external legal counsel, inadequate pre-emptive media risk assessment, and delayed initial crisis response all point to shortcomings. Since going public, the brand’s heightened visibility means even minor management lapses get amplified—impacting public sentiment, stock price, and foot traffic alike—highlighting significant gaps in its crisis management capabilities.

In fact, it’s not just Xiao Noodles— the entire Chinese noodle restaurant segment is now hitting a growth ceiling, grappling with industry-wide challenges that all players must confront.

Today, neighborhood stalls, regional brands, and national chains all compete in the same crowded space, offering highly homogenized products. With little differentiation, businesses resort to price cuts and discount vouchers to lure customers, trapping the entire industry in a race to the bottom. Compounded by annual increases in ingredient costs, rent, and labor expenses, most noodle shops are stuck with net profit margins of just 5%–8%, earning only meager returns through sheer hard work.

Market expansion presents a dilemma. Tier-1 and Tier-2 cities are already oversaturated with stores, fragmenting customer traffic. While lower-tier markets appear promising, they pose their own hurdles: significant regional taste variations, high supply chain setup costs, and entrenched local noodle brands that fiercely defend their home turf—making it extremely difficult for national chains to break through.

Today, whether chain noodle restaurants or small street-side eateries, all heavily rely on food delivery channels, with many brands deriving over 30% of their revenue from deliveries. Platform commissions, delivery fees, and promotional expenses stack up layer by layer, further squeezing already razor-thin profit margins. Moreover, online traffic is controlled by the platforms, resulting in highly unstable revenue.

Zhu Danpeng pointed out that, from a category perspective, noodles inherently offer high kitchen efficiency—a significant advantage. However, in the 'post-delivery era,' speed of order fulfillment has become equally critical in the delivery segment, substantially eroding noodles’ original efficiency edge and naturally weakening the category’s competitiveness.

Chinese-style noodles traditionally emphasize flavor and artisanal craftsmanship. Pursuing nationwide standardization often strips away their unique characteristics, while rigidly preserving regional flavors makes rapid replication and store expansion difficult. This dilemma plagues the entire industry. Consequently, it’s extremely rare to see a dominant brand with high customer loyalty, and consumers tend to choose casually.

Based on total gross merchandise value (GMV) in 2024, Xiao Noodles claims to be China’s fourth-largest operator of Chinese noodle restaurants, yet its market share stands at just 0.5%. This indicates that Xiao Noodles’ ambitions and ideal targets—centered solely on expanding and deepening its presence in the noodle segment—are exceedingly ambitious. Compounding the challenge, different types of noodles are inherently regional, and consumer preferences vary widely. Even if the average ticket price is lowered to around RMB 29, it remains higher than most local noodle shops in the category.

Finally, there’s the perennial tension between expansion and risk control. Chain restaurants cannot grow without opening new outlets, but rapid store rollouts inevitably bring risks such as poor site selection, declining product quality, and chaotic personnel management. Franchise models also heighten food safety concerns. Striking the right balance between store-opening speed and operational quality remains a long-standing, unresolved challenge for the entire industry.

As of June 16, 2026, a search for 'Xiao Noodles' on the Heimao Complaints platform yielded 134 complaints, covering issues such as spoiled food, poor service attitude, and unreasonable deductions or charges related to prepaid and membership cards. (Produced by Harbor Financial)

Harbor Business Observer, Xiao Xiuni

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1