Oil prices breaking above $100 fuel expectations of rate hikes! Will the Fed act next week?

Synchronized monetary tightening by the ECB and the Bank of Japan may trigger repricing of risk assets, and the narrowing U.S.-Japan interest rate differential by 2027 could lead to a substantial contraction in carry trade positions.

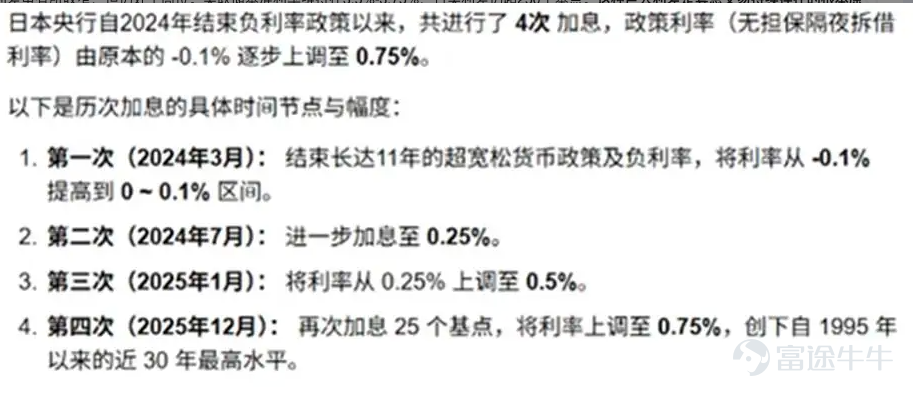

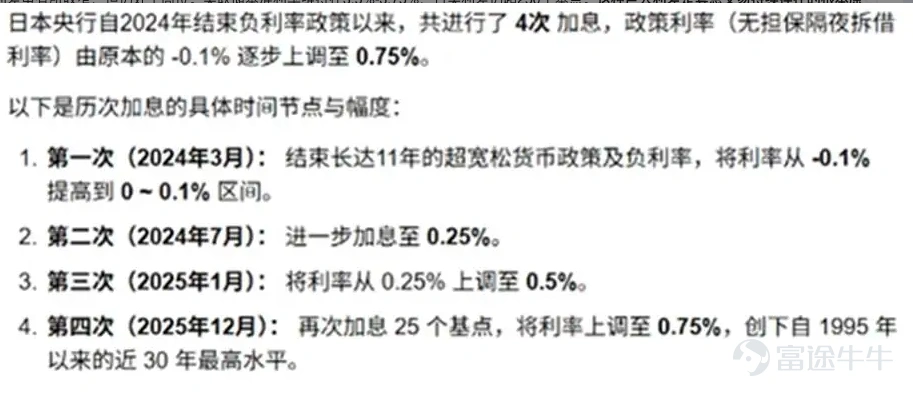

On June 16, the Bank of Japan (BOJ) voted 7 to 1 to officially raise its policy rate—the unsecured overnight call rate—from 0.75% to 1.0%. This move pushed Japanese rates to their highest level since 1995.

The Bank of Japan’s 25-basis-point rate hike to 1% theoretically compresses carry trade margins, prompting some capital to unwind positions and flow back into Japan. However, given the relatively modest magnitude of the rate hike and the fact that markets had already almost fully priced it in (with a 98% probability), the likelihood of large-scale unwinding of carry trades in the near term remains low.

1. Will this trigger a global liquidity squeeze?

There will be localized liquidity drainage effects, but a catastrophic global liquidity crunch in the short term is unlikely.

Carry trade unwinding pressure remains within manageable levels: During the era of ultra-low interest rates, global investors heavily borrowed cheap yen to invest in higher-yielding overseas assets. With Japan’s policy rate now at 1.0%, the cost of yen funding has risen significantly, which will indeed prompt some investors to sell overseas assets and buy back yen to repay debt.

Interest rate differentials remain intact, with no reversal yet: Although major overseas economies such as the U.S. and Europe are also adjusting their policies in response to domestic inflation dynamics, their benchmark rates remain substantially higher than Japan’s 1.0%. While the absolute interest rate gap between the yen and other major currencies has narrowed, it has not been entirely erased, making a sudden, panic-driven, stampede-style repatriation of global capital unlikely.

Structural reallocation into yen-denominated money market funds (MMFs): The 1.0% rate is now attracting significant inflows from Japanese institutional investors who previously allocated cash to overseas money market instruments, prompting them to shift toward yen-denominated fixed-income solutions (such as yen MMFs). This represents a long-term liquidity drain, but it is a gradual process.

2. Impact on Risk Assets: Certainty Realized and Structural Divergence

As this rate hike was already fully priced in by the market, and geopolitical tensions have recently eased (e.g., a U.S.-Iran peace agreement alleviating supply chain and oil-related concerns), markets did not collapse. Instead, they exhibited notable structural divergence:

Japanese Equities: Following today’s Bank of Japan policy announcement, the market reacted with clear relief—often described as 'the other shoe dropping'—as the statement did not signal a more aggressive hawkish stance. The Nikkei 225 even briefly surpassed the 70,000 mark intraday for the first time in history. Significant internal divergence emerged: financial stocks benefited from widening interest rate differentials, while export-oriented companies faced downward pressure due to expectations of a stronger yen. Semiconductor equipment makers such as Tokyo Electron, Kioxia, and Advantest led gains, whereas exporters sensitive to yen appreciation underperformed.

Yen Exchange Rate and Bond Market: USD/JPY currently remains stable above 160. Meanwhile, Japan’s 10-year government bond yield rose to 2.645% today, reflecting market repricing amid expectations of entrenched inflation and higher borrowing costs.

Global High-Risk / High-Valuation Assets: For liquidity-sensitive assets such as U.S. tech stocks or cryptocurrencies, Japan’s rate hike marks the end of the era of globally abundant cheap money. Their long-term valuations will face stricter scrutiny, and liquidity-driven rallies will become harder to sustain.

3. Japan May Continue Raising Rates Through 2027–2028 to Alleviate Inflation and Yen Depreciation Pressures

This rate hike is seen as a significant milestone in Japan’s monetary policy normalization process., but the author believes this will not mark the end of the current tightening cycle. The Bank of Japan has clearly stated it will continue raising its policy rate and adjust the degree of monetary easing based on developments in economic activity, prices, and financial conditions. Overnight index swap market data shows a roughly 60% probability of another 25-basis-point rate hike by December, indicating that markets have some expectation for further tightening.

Inflationary pressures as a driver: Tensions in the Middle East have pushed up international oil prices, leading Japan’s corporate goods price index (CGPI) to rise 6.3% year-on-year in May—the highest since March 2023. The Bank of Japan warned that cost pass-through triggered by higher crude oil prices is spreading relatively quickly through business-to-business transactions, which could broaden into other categories, posing an upside risk to core inflation exceeding the 2% price stability target.

Formation of a wage-price spiral: The outcome of Japan’s 2026 Shunto wage negotiations exceeded expectations, with overall corporate wage growth projected at around 5.02%, marking the third consecutive year above the 5% threshold. Labor shortages and rising wages are providing endogenous momentum to inflation, and the Bank of Japan hopes this will foster a virtuous cycle of higher wages, stronger consumption, and sustained inflation.

Yen depreciation pressure: The USD/JPY exchange rate recently returned to the 160 level, hitting a near-one-year high and approaching the intervention threshold set by the Japanese government. Yen weakness is further elevating import costs and intensifying domestic inflationary pressures. Following today’s rate hike, the USD/JPY rate only pulled back slightly before rebounding above the 160 mark, underscoring that the interest rate differential between the U.S. and Japan remains the primary factor weighing on the yen—further suggesting that the pace and magnitude of the Bank of Japan’s rate hikes remain insufficient.

After the rate hike, the interest rate differential between the yen and major currencies such as the U.S. dollar and euro narrowed somewhat but remains elevated. With the Federal Reserve’s benchmark rate held steady at 3.5%–3.75%, the U.S.–Japan rate gap still exceeds 250 basis points. This substantial spread remains the fundamental driver behind persistent carry trades and a key constraint preventing a reversal in the yen’s depreciation trend.

Over the past two years, Japan exited negative interest rates in 2024, and biannual rate hikes have since become the norm. Market expectations for the Bank of Japan’s future path are also fairly aligned, with another 50–75 basis points of hikes anticipated by the end of 2027.

Chart: Bank of Japan rate hike trajectory

Source: Internet

4. Global Central Bank Policy Coordination Effects

The Bank of Japan's rate hike is not an isolated event but part of a broader global shift in monetary policy, creating a coordination effect alongside the European Central Bank’s rate hikes and the Federal Reserve’s maintenance of high interest rates, collectively reshaping the global liquidity environment.

European Central Bank Leads with Rate Hike: On June 11, the European Central Bank announced a 25-basis-point rate hike, raising the deposit facility rate to 2.25%. This decision was directly driven by the energy crisis triggered by Middle Eastern geopolitical tensions, which pushed eurozone inflation to 3.2% in May—well above its 2% target. ECB President Lagarde noted, "Surveys indicate that economic activity is slowing, and domestic demand will be weaker than expected."

Federal Reserve Policy Stance: On June 18, the Federal Reserve held rates steady (with a 98.5% probability), but new Chair Waller signaled a 'hawkish wait-and-see' approach, emphasizing that 'higher rates need to be sustained for longer,' removing dovish language and hinting at potential future hikes. The dot plot shifted toward neutrality, lifting market expectations for a rate hike in 2027, though almost no action is anticipated in 2026.

Bank of England Policy Divergence: On June 18, the Bank of England kept its policy rate unchanged at 3.75%, but clear divisions emerged within the Monetary Policy Committee. Chief Economist Pill and MPC member Greene, among other hawks, supported a rate hike, while Governor Bailey stressed that the current policy stance was 'effectively already actively tightening.'

Manifestation of Coordination Effects: The combination of synchronized rate hikes by the European and Japanese central banks alongside the Fed’s sustained high-rate policy has created a 'tightening resonance' effect, lifting the global risk-free rate benchmark and altering asset pricing dynamics. This could exert repricing pressure on global risk assets and lead to marginally tighter liquidity conditions.

Emerging market stress: Against the backdrop of tightening global liquidity, emerging markets face a 'triple bind': imported inflation intensifies, risks of currency depreciation and capital outflows rise, and countries with high external debt see sharply elevated sovereign default risks. Currencies such as the Mexican peso, Korean won, and Indonesian rupiah may face depreciation pressure due to capital repatriation.

Simultaneous rate hikes by the European Central Bank and the Bank of Japan, along with potential further hikes by the Federal Reserve, will trigger shifts in global liquidity.

If the Bank of Japan maintains its current pace of hiking rates once every six months, its policy rate could reach 1.5%–1.75% by end-2027. At that point, a narrowing interest rate differential between the U.S. and Japan could lead to a substantial unwinding of carry trades, exerting a more pronounced impact on global liquidity.

If core CPI remains persistently above the 2% target and yen depreciation pressures continue unabated, the Bank of Japan may need to accelerate its pace of rate hikes further.

Following the release of interim earnings reports, unless AI-related hardware and software tech companies deliver further upside surprises in earnings or capital expenditure, investor funds may gradually rotate into defensive sectors, and market sentiment could turn increasingly cautious.

Risk Disclosure: The above content is for personal sharing purposes only and does not constitute any investment advice. Please assume all risks yourself.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment