The Federal Reserve launches reforms! How to position for the Worshe era?

Global Weekly Outlook | US May CPI Re-enters the '4% Era,' China's Foreign Trade Continues Strong Growth

On the macroeconomic front

United States: May CPI Re-enters the '4% Era,' Inflationary Pressures Broaden, Fed Rate Hike Expectations Strengthen

US inflation data for May rose broadly across the board. Headline CPI increased 4.2% year-over-year—the highest since April 2023—marking a return above the 4% threshold for the first time in three years. Core CPI rose 2.9% year-over-year and 0.2% month-over-month, slightly below expectations. Surging energy prices driven by Middle East geopolitical tensions were the main driver of this inflationary wave, with sharp increases in gasoline and diesel prices spilling over into transportation, food, air travel, and other sectors across the economy.Compounded by AI-driven investment pushing up electricity and semiconductor prices, inflationary pressures have spread from energy to broader sectors of the economy, showing significantly greater persistence.Wholesale inflation has heated up in tandem, with May's PPI surging 1.1% month-over-month—far exceeding expectations. Gasoline prices within industrial consumer goods saw accelerated gains, and service prices continued to rise. A resilient labor market coexists with high inflation: May ADP employment growth beat expectations, wage growth remained steady, and the robust labor market further bolstered market expectations for rate hikes.Following the data release, market bets on a Fed rate hike this year rose sharply, with some traders pricing in a potential hike as early as September and nearly a 70% probability of a hike by December.Although the slight month-over-month decline in core CPI has eased some rate-hike pressure, inflation remains well above the 2% target. Coupled with energy supply chain disruptions that are unlikely to heal quickly, the Fed is highly likely to hold rates steady at its June meeting. However, the hawkish stance of 'higher for longer' will be further reinforced, leaving the door open for a rate hike later this year.

China: Foreign trade continues strong growth with structural improvements; PPI rises while CPI remains moderate, highlighting economic resilience

On China’s side, May macroeconomic data showed robust external demand, a recovery in industrial activity, and moderate price levels, underscoring solid underlying economic resilience. In foreign trade, total imports and exports in the first five months reached RMB 20.68 trillion, up 15.3% year-over-year, with May alone posting a 16.9% increase—marking three consecutive months exceeding RMB 4 trillion.Export structures continue to improve, with high-tech and high-value-added machinery and electronics accounting for over 60% of exports. Green products such as lithium batteries and wind turbines saw significant export growth; imports also rose strongly in parallel.Imports in the first five months increased 20.5% year-over-year, with May alone up 21.5%—marking three straight months of growth exceeding 20%, reflecting robust domestic industrial demand. On the price front, May CPI rose 1.2% year-over-year but declined 0.1% month-over-month; core CPI was up 1.1% year-over-year, indicating stable consumer market conditions and well-contained inflation. PPI climbed 3.9% year-over-year—the highest so far this year—and rose 0.5% month-over-month.This was primarily driven by rising prices in non-ferrous and ferrous metal processing industries, supported by AI and manufacturing investment demand underpinning industrial product prices.Meanwhile, a pullback in international oil prices led petroleum-related sectors to shift from price gains to declines.

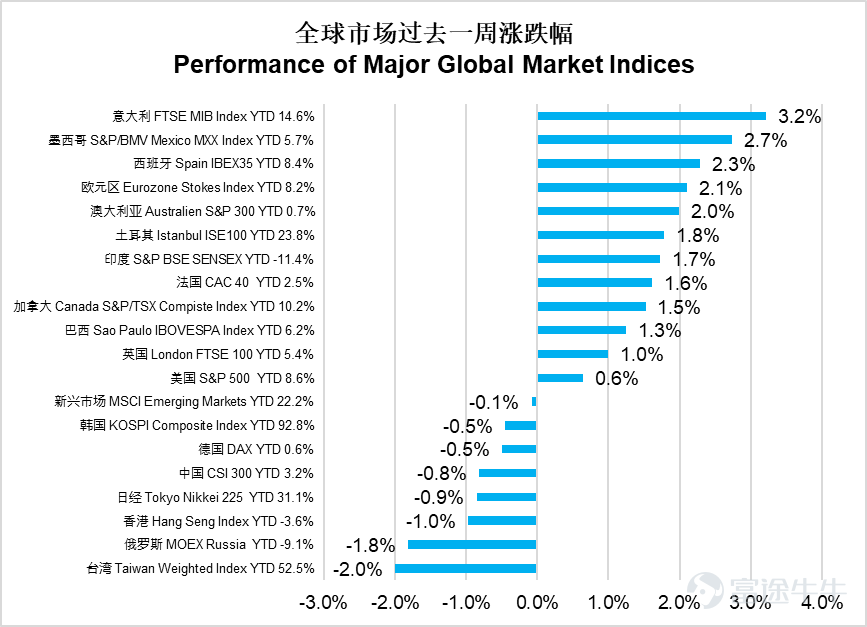

In the equity market,

Global markets last week showed clear regional divergence, with markets across Europe and the U.S. generally strengthening, while Asia-Pacific markets came under broad pressure.Europe, the U.S., and several emerging markets delivered strong performances, with Italy's FTSE MIB rising 3.2% for the week to lead global gains,Mexico’s IPC (MXX), Spain’s IBEX 35, and the Eurozone’s STOXX 600 advanced by 2.7%, 2.3%, and 2.1%, respectively, while markets in Australia, India, Canada, and the U.K. also moved higher in tandem.Asia-Pacific markets weakened overall, with Taiwan’s Weighted Index falling 2.0%—the steepest decline in the region,Russia’s MOEX, the Hang Seng Index, the Nikkei 225, the CSI 300, and South Korea’s KOSPI all posted modest declines. Overall, developed markets in Europe and the U.S. showed robust momentum, while Asia-Pacific markets broadly corrected, and emerging markets exhibited mixed performance.

U.S. equities edged modestly higher last week, $S&P 500 Index (.SPX.US)$with the index gaining 0.6% for the week, as sector rotation favored value stocks while growth and communication services lagged.The materials sector stood out with a 3.0% gain, while consumer staples and financials also strengthened, rising 2.6% and 2.0%, respectively. Real estate and industrials also posted steady gains. Communication services underperformed, declining 1.9% for the week, and energy slipped modestly by 0.4%.Health care, information technology, consumer discretionary, and utilities all registered modest weekly gains, reflecting a market environment where value-oriented defensive sectors outperformed, while growth sectors remained lackluster.

Hong Kong equities underwent a modest correction last week, with the Hang Seng Index declining 1.0% for the week.Significant divergence emerged across sectors, as consumer discretionary, technology, and energy stocks weakened sharply, while financials and consumer staples posted gains against the broader downtrend.Consumer discretionary, energy, and Hang Seng Tech led the declines, falling by 4.8%, 4.0%, and 3.7% respectively. Utilities, materials, telecoms, healthcare, and information technology also saw modest pullbacks.Only a few sectors advanced against the trend: financials rose 1.9%, standing out positively, while consumer staples and conglomerates posted modest gains.The market overall exhibited a clear divergence, with growth and cyclical sectors undergoing deep corrections while value-oriented financial stocks demonstrated notable resilience.

Bond Market

Global bond markets continued to recover over the past week. The Global Aggregate Index rose 0.41%, the U.S. Aggregate Index gained 0.52%, U.S. investment-grade corporate bonds advanced 0.55%, and U.S. high-yield corporate bonds increased by 0.45%. The Emerging Markets USD Bond Aggregate Index climbed 0.51%, while the China USD Credit Bond Index rose 0.16%.

On the rates front, U.S. Treasury yields broadly declined: the 2-year Treasury yield fell 7 basis points to 4.08%, and the 10-year Treasury yield dropped 5 basis points to 4.48%.

Market outlook

– Europe has taken the lead in hiking interest rates to counter energy-driven inflation, while Asia faces pressure from a strengthening U.S. dollar and capital outflows.

The core tension confronting markets currently is that energy price shocks triggered by the Middle East conflict are fueling global inflation, while economic growth momentum and policy space vary significantly across economies.The U.S. faces a triple constraint of high inflation, strong employment, and elevated valuations, forcing the Federal Reserve to keep interest rates higher for longer.Europe has already led the way in raising interest rates to counter the energy shock; Asian markets are under pressure from a stronger dollar and capital outflows. May’s year-on-year CPI of 4.2%, exceeding expectations, has further narrowed the Federal Reserve’s room for rate cuts.Markets have already priced in a 12.6% probability of a rate hike in July, and policy uncertainty will continue to weigh on risk asset valuations.

Next week’s FOMC meeting will be the most important near-term catalyst.This will be the first monetary policy meeting chaired by new Fed Chair Warsh, drawing intense market focus on the updated dot plot and economic projections. If Warsh delivers a hawkish signal, tech stock valuations could face further downward pressure. Meanwhile, U.S.-Iran talks have signaled a potential agreement within the next few days; substantive progress in these peace negotiations could drive oil prices sharply lower, easing global inflationary pressures. On Friday, SpaceX successfully completed its record-breaking IPO, closing 19% higher on its debut day with a market valuation of $2.1 trillion.Concerns about capital diversion effects have subsided, and liquidity could flow back into other sectors.

Key economic data and events this week

On Tuesday, China will release its May industrial production data and retail sales figures.

On Wednesday, the U.S. will release its May retail sales data.

On Thursday, the U.S. will announce the FOMC interest rate decision.

Disclaimer: The issuer of this report is E Fund Asset Management (Hong Kong) Co., Ltd. This report does not constitute an invitation or recommendation to invest in fund units. Fund unit subscriptions can only be made using application forms accompanied by the fund prospectus. Investment involves risks; fund prices may rise or fall, and past performance is not indicative of future results. Before investing, investors should carefully read the fund prospectus (including the 'Risk Factors' section) to understand the investment risks related to the fund. This report may only be distributed in certain jurisdictions. In any jurisdiction where distributing such information or making any invitation or recommendation is prohibited, or where distributing this report or making an invitation or recommendation to any person would be illegal, this report does not constitute such distribution or invitation or recommendation. This document has been exempted from prior review and approval by the Hong Kong Securities and Futures Commission, and has not been reviewed by the SFC. SFC approval does not imply promotion or endorsement of the plan, nor does it guarantee its commercial merits or performance, nor does it indicate suitability for all investors, or endorsement of suitability for any particular investor or category of investors. All rights reserved © 2026. E Fund Asset Management (Hong Kong) Co., Ltd.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

1