Major Governance Overhaul! Is It Time to Invest in PDD Holdings?

Earnings & Options Strategy | Temu’s Breakthrough and Domestic Defense: Can PDD Holdings’ Latest Earnings Report Ease Market Anxiety?

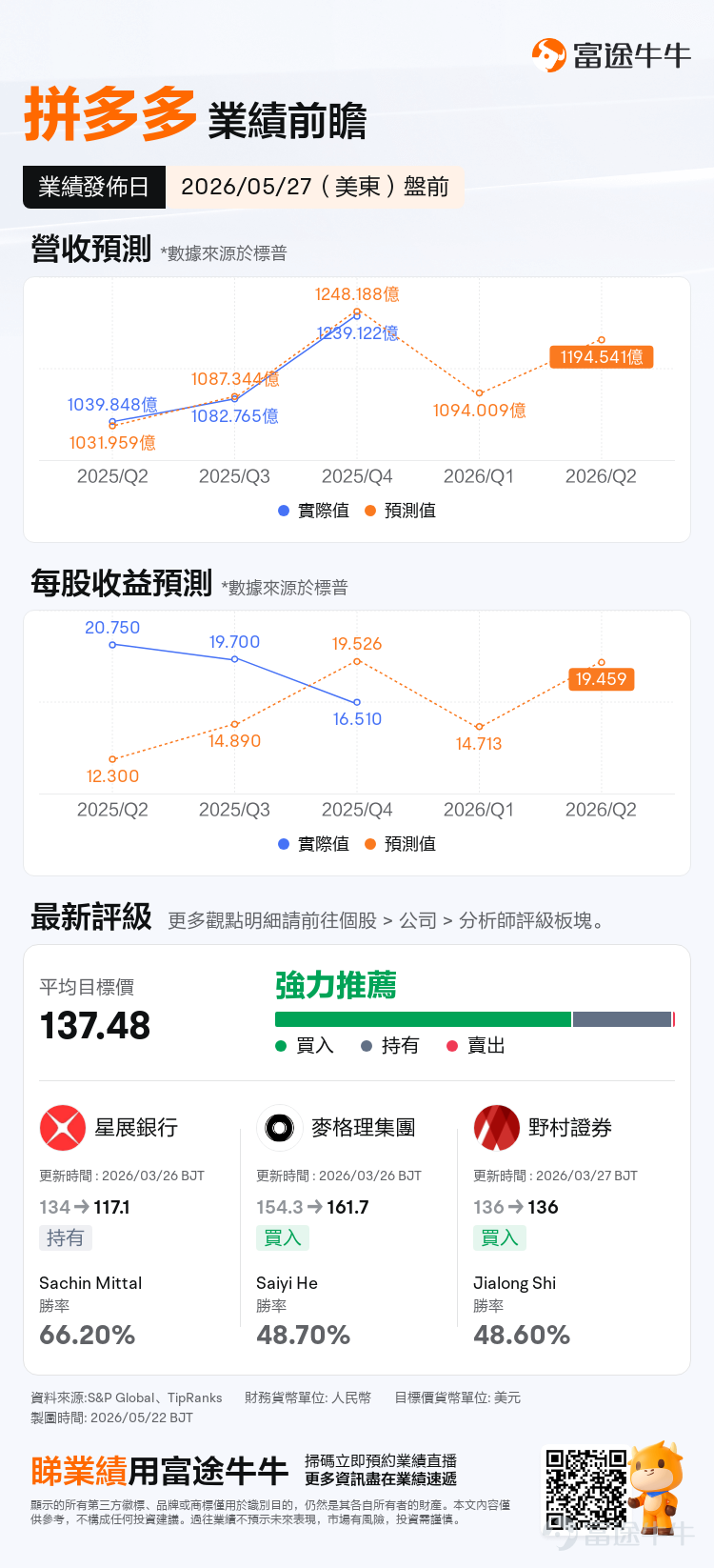

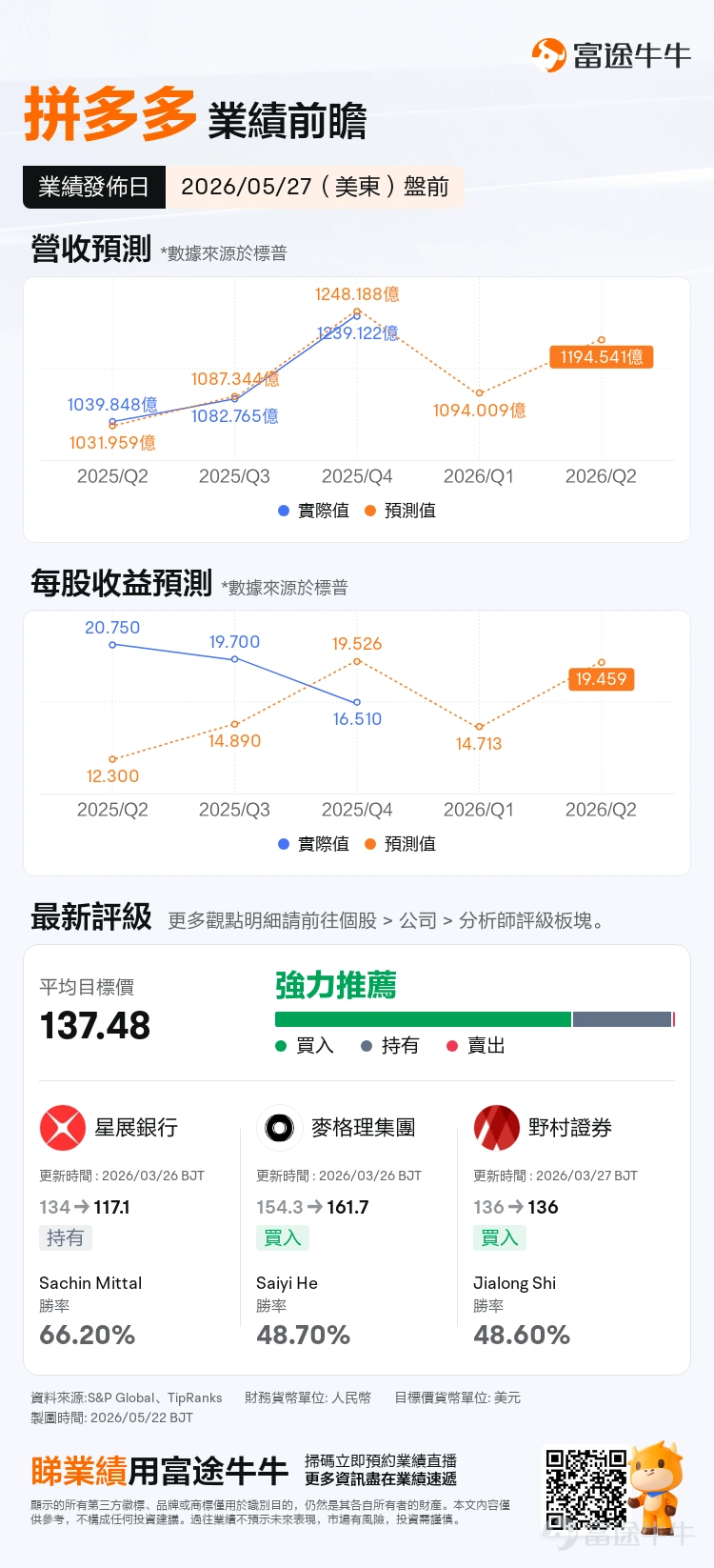

$PDD Holdings (PDD.US)$ PDD Holdings will release its Q1 2026 earnings report before the market opens on Wednesday, May 27, Eastern Time. This report offers several key points of interest: whether revenue can sustain its recovery, whether profit margins can halt their downward trend, and whether regulatory and fulfillment costs related to Temu will continue to weigh on market expectations.

Market consensus estimates show that PDD Holdings’ first-quarter revenue is expected to be approximately RMB 109.4 billion, up from RMB 95.67 billion in the same period last year, implying a year-over-year revenue growth rate of roughly 15% based on market expectations; EPS is forecast at RMB 14.713.

Lingering concerns from last quarter: revenue growth remains intact, but profit visibility has weakened.

PDD Holdings reported fourth-quarter 2025 revenue of RMB 123.912 billion, an increase of 12% year-over-year; online marketing services and other revenue rose 5% year-over-year, while transaction services revenue grew 19% year-over-year. On the surface,platform revenue continues to grow, but pressure on profitability has become quite evident.. Net income attributable to shareholders for the fourth quarter was RMB 24.541 billion, down 11% year-over-year; non-GAAP net income attributable to shareholders was RMB 26.295 billion, down 12% year-over-year.

From a cost structure perspective, cost of revenue increased 15% year-over-year in the fourth quarter, which the company attributed primarily to higher fulfillment expenses, bandwidth and server costs, and payment processing fees; sales and marketing expenses amounted to RMB 34.352 billion, up from RMB 31.357 billion in the same period last year; research and development expenses also rose year-over-year. As of the end of 2025, PDD Holdings held RMB 422.3 billion in cash, cash equivalents, and short-term investments,the company’s balance sheet remains very strong, but the market is concerned about how long these funds will continue to be invested and when such investments will translate back into profit realization.。

This represents PDD Holdings’ core current valuation dilemma: the company still possesses strengths in value-focused e-commerce, transaction services, and cross-border expansion, yet the market lacks sufficient confidence in the timing of profit realization.

Three key focal points of this earnings report

1. Assess whether revenue recovery stems from high-quality growth

The market expects PDD Holdings’ first-quarter revenue to rise from RMB 95.672 billion a year ago to nearly RMB 110 billion. While this growth rate itself is not low, the stock price will not hinge solely on top-line figures. Investors will further dissect whether the revenue growth stems from a recovery in online marketing services or from transaction services; whether it is driven by a rebound in merchant advertising spending or by subsidies and low-price strategies boosting gross merchandise value.

If the recovery in online marketing services is more pronounced,it would indicate improved merchant willingness to advertise and stronger ad monetization capability on the platform.If transaction services show stronger growth, it would signal that the platform’s transaction volume remains resilient. However, if revenue growth comes alongside continued rapid increases in sales and marketing, fulfillment, and payment processing costs, the market’s assessment of earnings quality would be discounted.

2. Assess whether Temu’s regulatory and fulfillment costs continue to weigh on valuation

Temu remains PDD Holdings’ most promising business segment, yet it faces certain uncertainties. According to market analysts, Temu’s low-price cross-border direct-mail model is encountering regulatory pressure in several major markets, with evolving trade policies, tax regulations, data governance rules, and product compliance requirements. Following the Q4 earnings call, PDD Holdings’ management also noted that shifting regulatory frameworks across different countries and regions are creating greater challenges and uncertainty.

Moreover, the U.S. has eliminated the de minimis exemption for packages valued under USD 800, and the European Union has agreed to abolish the VAT exemption for parcels under EUR 150. Temu previously relied on these de minimis exemptions, low-cost direct shipping, and China’s supply chain efficiency to scale rapidly. These policy changes could increase fulfillment, tariff, and compliance costs.

Therefore,This earnings call will require close attention to how management addresses cost pressures faced by Temu in the U.S. and European markets, as well as whether semi-managed operations, local warehouses, and supply chain restructuring are improving fulfillment efficiency. If management can outline a clearer path toward cost control, the valuation discount reflecting Temu’s uncertainty could ease; if they continue to emphasize regulatory and trade environment shifts, the market may further compress PDD Holdings’ valuation.

3. Monitor whether domestic e-commerce competition is easing

PDD Holdings' domestic business remains the core profit driver. Over the past few quarters, platforms including Alibaba, JD.com, and Douyin E-commerce have intensified their focus on low pricing, subsidies, instant retail, and merchant ecosystem development, intensifying competition in China's e-commerce market and putting pressure on PDD Holdings' profit margins.

Growth of PDD Holdings' original China platform cooled in the fourth quarter, linked to consumers cutting back on discretionary spending and weak consumer confidence in China. However, subsequent signals from official media suggesting an end to the e-commerce price war temporarily boosted PDD Holdings' share price.

If this earnings report shows a recovery in advertising revenue from its domestic main platform, easing subsidy pressures, and a decline in sales and marketing expense ratios,the market will be more inclined to believe that PDD Holdings' core profit base remains solid.However, if the domestic main platform also shows clearer signs of investment pressure, uncertainties surrounding Temu would be further amplified.

Three post-earnings scenarios

Bullish scenario: EPS significantly beats expectations, and the stock price retests above USD 100.

The bullish scenario requires several conditions to materialize simultaneously: revenue meets or exceeds the market expectation of RMB 110 billion, EPS meaningfully surpasses the expected range, sales/marketing and fulfillment costs show improvement, and management provides clearer commentary on Temu’s compliance costs and domestic competitive pressures.

Under this combination, the market would resume pricing in a margin recovery for PDD Holdings. In the near term, the USD 100 level represents both the upper bound of implied volatility during earnings week and a psychological resistance point; if both the earnings report and the earnings call deliver positive updates, the stock could test levels above USD 100.

Neutral scenario: revenue meets expectations, modest profit recovery, and continued stock price consolidation.

In a neutral scenario, PDD Holdings' revenue broadly meets market expectations, and EPS is close to the expected range, but expense ratios show no significant improvement. Management continues to emphasize long-term investments, evolving external conditions, and competitive pressures.

This outcome isn't bad for fundamentals, but it’s unlikely to drive a rapid valuation recovery. The stock price may continue to trade sideways within the $90–$100 range. For options buyers, this type of environment often leads to situations where directional calls are correct, but the magnitude of movement is insufficient, causing option premiums to erode quickly.

Bearish scenario: Margins remain under pressure

Triggers for the bearish scenario include revenue falling short of the market expectation of approximately RMB 109 billion, with fulfillment, sales and marketing, and supply chain investments continuing to push costs higher. If management further signals increasing complexity in the external environment and heightened long-term investment commitments, the market would likely further downgrade its medium-term earnings visibility for PDD Holdings.

Options strategy: Prefer limited-risk structures to express views

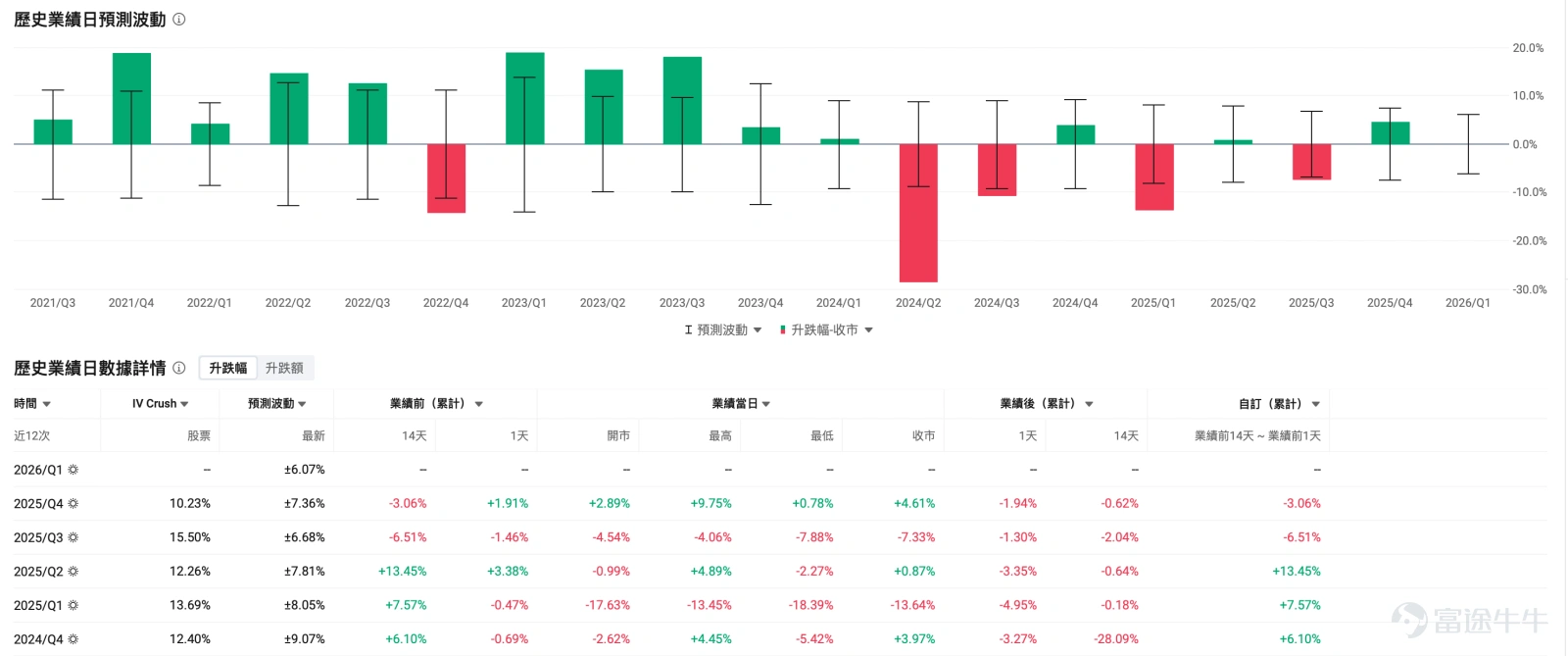

Based on current options market signals, the market is pricing in roughly ±6% implied move around earnings day. In the prior three quarters, PDD Holdings’ stock rose modestly on two earnings days and declined once.

Bullish on post-earnings rebound: Bull Call Spread

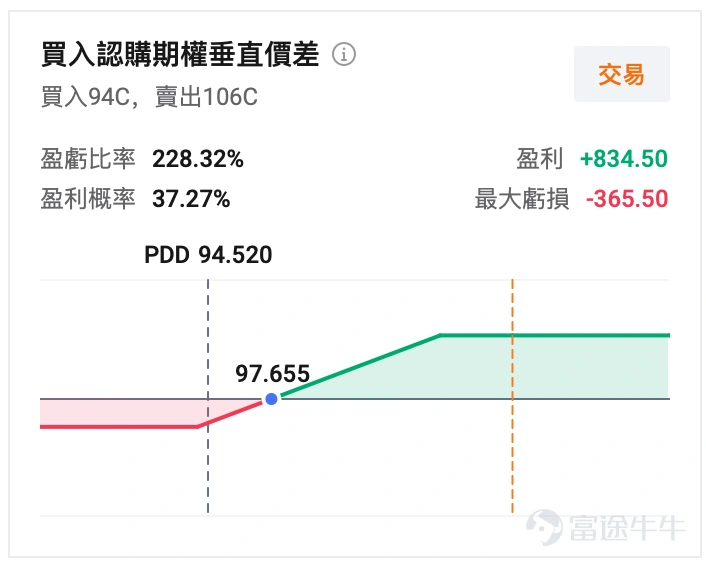

If investors believe PDD Holdings’ earnings report will reflect margin improvement and that the stock has a chance to move above $100, they could consider using a bull call spread to express a moderately bullish view. Compared to buying calls outright, a bull call spread reduces premium costs in a high implied volatility (IV) environment and partially offsets losses from the post-earnings IV crush.

A more conservative approach is to buy an at-the-money call and sell a higher-strike call near $100 or $105. This structure suits scenarios where a mild to moderate upside move is expected. The trade-off is a capped maximum profit; if PDD Holdings surges sharply after earnings, the payoff will be less than that of a naked long call.

For existing stockholders: Protective Put or Collar

Investors who already hold shares of PDD Holdings and are bullish on the company over the long term—but concerned about a potential post-earnings gap down—can use a protective put to hedge against downside risk. Buying puts near $88 or $90 can provide insurance against earnings-related volatility.

To reduce the cost of this insurance, investors can consider a collar strategy.This involves holding the underlying stock while simultaneously buying a put at a lower strike and selling a call near $100 or $105.This strategy lowers the cost of protection but caps upside potential. It is better suited for investors who prioritize drawdown control.

Willing to buy at lower levels: Cash-Secured Put

If an investor believes in the medium- to long-term value of PDD Holdings but prefers not to buy shares outright ahead of earnings,they could consider selling cash-secured puts near $85 or $88.This strategy collects premium income in exchange for the possibility of acquiring shares at a lower price.

The key prerequisite for this approach is that the investor must genuinely be willing to purchase PDD Holdings shares at the strike price. If earnings significantly disappoint, the stock could gap below the strike, and the premium received would offer only limited cushioning.

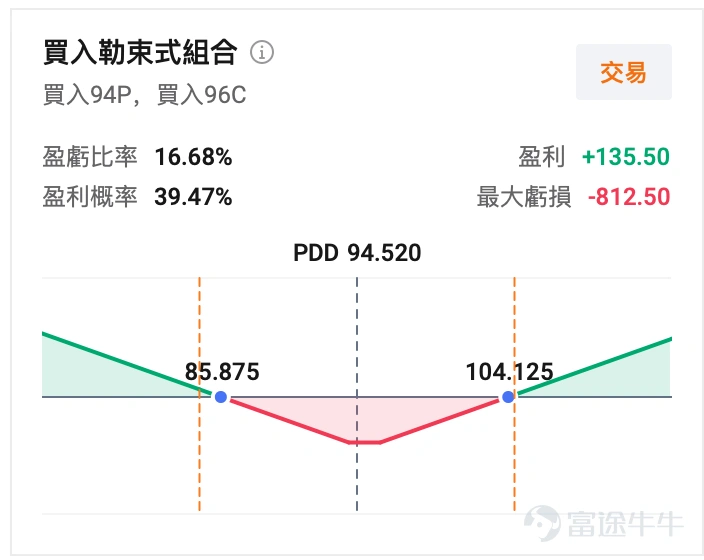

Betting solely on large moves: Long strangles require caution.

If investors believe post-earnings volatility will significantly exceed what is currently priced in by the market, they may consider a straddle. However, PDD Holdings’ current Implied Volatility (IV) Rank and IV Percentile are both relatively high, meaning that buying both legs of the options requires even greater realized volatility to cover the cost.

Based on current implied volatility levels, the stock price would need to clearly break out of the $88–$101 range for buyers to gain an advantage. If the stock remains within this range after earnings,straddles are vulnerable to dual pressures from insufficient directional movement and a decline in implied volatility.。

PDD Holdings’ current share price has already priced in considerable concerns.Expectations for a recovery in revenue growth are relatively clear, and the valuation is not high; however, the market still lacks a compelling reason to reposition or add exposure.The reason is that investors have yet to see a clear equilibrium among domestic competitive pressures, Temu’s regulatory costs, fulfillment expenses, and platform ecosystem investments.

For the underlying stock, $100 represents the first psychological level post-earnings; for options, the implied move of around 6% for earnings week is already fairly substantial, making spread strategies, protective structures, or cash-secured puts more suitable for managing risk.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

7

27