"AI Bottleneck Trade" Ignites Upstream Sector—Who’s Raking in the Profits?

Tech giants like Meta and Anthropic are ramping up AI computing power! What’s the outlook for the new cloud (Neocloud) sector?

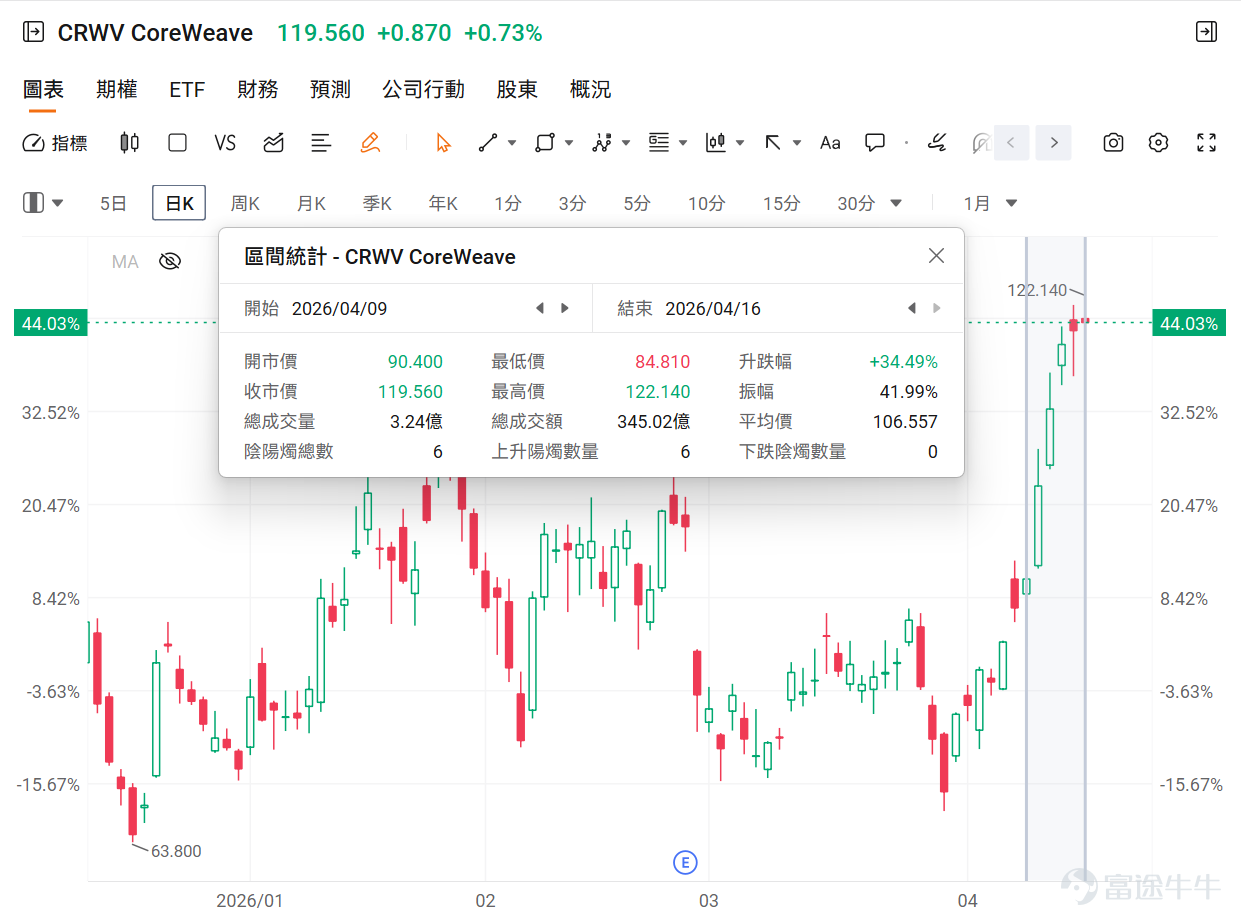

AI computing infrastructure provider, $CoreWeave (CRWV.US)$ Raked in a whopping $33.8 billion super order within just one week.

On April 9, CoreWeave was the first to announce a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined the fray, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion.

This wave of positive news has made CoreWeave the market focus, and since April 9, the company's cumulative increase has approached 35%.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776420819077-QEzPgrbhmE.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

However, CoreWeave's celebration is just the tip of the iceberg. Apart from these positives, what profound changes have occurred recently in the 'New Cloud (Neocloud)' industry centered around AI computing power rental and infrastructure? Which key players are worth paying attention to? This article will provide you with an in-depth analysis.

What recent changes have occurred in the entire Neocloud industry?

1. Key Catalyst: GPU Rental Prices See Strong 'V-Shaped' Rebound

The most direct catalyst for the current rise in the industry sector,is the increase in computing power rental fees.

On April 7th,'Breaking the Depreciation Curse! GPU Rental Fees Surge, How Far is Neocloud's 'V-Shaped' Rebound?'the article pointed out that according to the latest data from semiconductor research firm SemiAnalysis, the one-year lease contract price for the H100 has rebounded strongly from a low of $1.7 per hour in October 2025 to $2.35 in March this year, with an increase of nearly 40%.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776420808647-UU0Ayp3Hej.webp/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

It’s worth noting that, similar to the memory market, there is a significant difference between spot prices and long-term agreement (LTA) prices in computing power rentals.For example, taking the long-term service agreements signed between CoreWeave and OpenAI, or IREN and Microsoft, their prices are determined at the time of signing.Although the specific amounts are confidential, these agreements typically set price ceilings to hedge against the risk of market price fluctuations due to volatile demand, along with strict Service Level Agreements (SLAs) and penalties for delayed delivery.

This creates a significant expectation gap: Affected by the long-term contract pricing, an analysis of Q4 and Q1 financial reports from leading hash rate leasing companies shows that their profit margins have not yet seen a significant increase. However, under the ongoing supply-demand imbalance for computing power,when future contracts are up for renewal, suppliers will hold strong bargaining power, with the potential to raise prices by 30% or even more.This sets the stage for a future surge in profitability.

II. Ecosystem Integration of Giants: Large Orders Surge, Cross-Cloud Collaboration Deepens

In addition to CoreWeave's astonishing wave of multi-billion-dollar orders, traditional cloud giants are also accelerating their ecosystem layout for the AI era.

Recently, $Oracle (ORCL.US)$ and $Amazon (AMZN.US)$ Cloud service provider AWS announced the expansion of 'multi-cloud cooperation,' connecting OCI (Oracle Cloud Infrastructure) with AWS interconnection products to establish enterprise-grade private connections. This move breaks down past ecosystem barriers and deepens collaboration between both parties in the AI database sector, enabling customers to run applications and transfer data across clouds seamlessly without building their own physical networks. This marks the competition in the Neocloud era shifting from solo battles to deeper underlying computing power and database interconnectivity.

III. Epic Market Bonanza: Scale Set to Reach $400 Billion

The global emerging cloud computing market is in a historic high-growth phase.

According to the latest forecast from Synergy Research Group, the global Neocloud market is set for explosive growth — the total market size is expected to soar from approximately $35 billion in 2025 to nearly $400 billion by 2031, with a compound annual growth rate (CAGR) as high as an astonishing 58%. Cloud infrastructure remains the absolute growth cornerstone.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776420900626-diYBAAvJsO.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

The core engine driving this growth is the full commercialization of generative AI. From model training to inference deployment, the demand for underlying cloud computing power from AI applications is expanding exponentially. At the same time, the popularization of AI has given rise to numerous new SaaS applications, together forming a dual-driven pattern of 'computing power + applications.' Data centers are the physical foundation supporting all of this.

CMB Securities noted that based on the Q4 2025 earnings calls of major CSPs, large-scale infrastructure expansion remains a clear strategic direction. However, compared to the future computing power demand curve disclosed by AI vendors, the industry still faces a significant computing power gap. Given the difficulty for traditional CSP expansion cycles to fully meet this demand, Neocloud continues to be in a favorable window for expansion.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776420906650-RWxlrN0p2n.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

In summary: All data and forecasts clearly indicate thatThe greatest commercial value of the AI era is consolidating at the infrastructure layer.This is not only about the flourishing of software applications but also represents the extreme exploitation of underlying computing power and physical space. In the technological competition over the next few years,Whoever controls the 'cloud and computing power' super gateway will hold the ultimate power to define the next generation of the internet.

Which core players deserve close attention?

CMB Securities stated that AI Neocloud refers to new cloud computing providers specializing in GPU computing rental services. These pure GPU cloud platforms offer customers cutting-edge performance and flexibility. The AI Neocloud market is vast and serves as the most important driver of GPU demand growth, with Neocloud's demand expected to grow to more than one-third of total demand.

Previously, Niuniu compiled a list of core North American Neocloud vendors as follows:

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776420935725-gbhWSfx47D.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

According to CMB Securities’ research report, considering the ranking of cloud service capabilities and evaluating current cloud service agreement orders, key attention will be given to leading Neocloud vendors listed on US stock exchanges with cloud service agreements exceeding tens of billions. $CoreWeave (CRWV.US)$ 、 $NEBIUS (NBIS.US)$ 、 $IREN Ltd (IREN.US)$and$Oracle (ORCL.US)$ Specifically:

1. CoreWeave: The Aggressive New Giant in AI Cloud Infrastructure

$CoreWeave (CRWV.US)$The business model is essentially that of a computing power broker.Unlike traditional cloud service providers, the company does not offer CPUs, storage, or security services but focuses solely on renting out GPU computing power.Customers are mainly divided into two categories,one being tech giants like Microsoft and OpenAI, which require urgent capacity expansion and contribute the vast majority of revenue; the other being smaller AI companies unable to build their own GPU clusters. The company’s business model means that the ability to secure GPUs determines customer stickiness.

CoreWeave specializes in bare-metal services, directly providing hardware computing power.CoreWeave offers fast, reliable, large-scale bare-metal GPU services—providing thousands, or even potentially millions, of GPU devices at once. CoreWeave eliminates the traditional virtualization layer (hypervisor) and runs Kubernetes directly on physical machines. This architecture removes the additional overhead and performance loss caused by virtualization, achieving the lowest latency and highest performance. CoreWeave's analysis shows that traditional virtualized environments can waste up to 65% of effective GPU computing capacity, and the bare-metal architecture aims to solve this pain point.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776421029455-SjON04nao3.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Currently, CoreWeave is actively expanding its scale, increasing active power capacity to approximately 850MW, with contracted power capacity reaching 3.1GW.Among this, CoreWeave will develop a new data center campus in Kenilworth, New Jersey, with a capacity of up to 250MW. This is CoreWeave’s first greenfield data center project specifically for artificial intelligence, with the first phase expected to be delivered by 2026. The company expects the vast majority of contracted power capacity to be operational within the next 12 to 24 months.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776420831136-fpeBvEObEG.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Currently, CoreWeave holds a large number of major client computing power rental orders,Including but not limited to: (1) A major cooperation agreement with NVIDIA worth up to $63 billion. It commits to purchasing all of CoreWeave's unsold computing power capacity over the next decade. (2) Announced an agreement to provide Meta with $142 billion worth of AI cloud infrastructure, along with an expanded cooperation worth an additional $210 billion. (3) Reached a new cooperation agreement with OpenAI valued at $65 billion. The total contract amount has surged to $224 billion. (4) A multi-billion-dollar order agreement with Anthropic.

Additionally, it is worth noting that CoreWeave possesses industry-leading capabilities in acquiring GPUs.CoreWeave is NVIDIA’s first Elite Partner (the highest level) and also the first AI cloud provider to offer NVIDIA RTX PRO 6000 Blackwell GPUs on a large scale.

2. Nebius: Vertically Integrated AI Infrastructure Provider

A full-stack infrastructure provider in Europe. $NEBIUS (NBIS.US)$ Originally founded as Yandex N.V. in 1989, after the Russia-Ukraine conflict, all non-Russian assets of Yandex were spun off to become Nebius, including a data center in Finland, $2.3 billion in cash reserves, and a range of other divisions. The company resumed trading on the exchange on October 21, 2024, positioning itself as a European AI infrastructure and service provider, building full-stack infrastructure including GPU clusters, cloud platforms, tools, and developer services.

Following its transformation, Nebius’ market capitalization has rapidly increased.NVIDIA participated in the financing.As of Q4 2025, Nebius operates seven data centers across Europe, the US, and the Middle East. Nebius will continue to expand its capacity, with projected contracted power capacity exceeding 3.0 GW by the end of 2026 (up from last quarter’s guidance of 2.5 GW), with connected power ranging from 800 MW to 1 GW.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776421052505-9lWWXaGc88.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Nebius is a Preferred Partner of NVIDIA and is also one of the six global cloud service providers on NVIDIA's Reference Platform Cloud Partner (Reference Platform NCP).

Nebius provides a full-stack platform,integrating software toolchains with the core goal of building an end-to-end cloud service platform capable of serving as a 'production-grade inference platform.' Nebius not only serves top AI tech companies that train their own models but also attracts many small or medium-sized development and research teams within large enterprises. These customers have relatively limited technical capabilities and are more willing to pay for an 'out-of-the-box' complete solution, thus placing greater value on the comprehensive software abstraction layer services provided by Nebius.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776421061097-h4WHlQq3MJ.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

3. Iren: Green computing power infrastructure provider based on renewable energy

From mining facilities to computing power plants. $IREN Ltd (IREN.US)$ Founded in 2018 by brothers Daniel Roberts and William Roberts in Sydney, Australia, the company’s initial mission was to become a sustainable Bitcoin mining firm powered entirely by renewable energy. In response to volatility in the cryptocurrency market, the company decisively initiated a strategic transformation, focusing investment in the AI cloud services sector, while temporarily halting the expansion of its Bitcoin mining operations.

The company's latest guidance maintains a projection to achieve $3.4 billion in annualized run-rate revenue (ARR) from AI Cloud services by the end of 2026.Among this, Microsoft contracts are expected to contribute approximately $1.94 billion in ARR, with around 63,000 GPUs deployed at the British Columbia campus anticipated to bring in about $1.5 billion in ARR.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776421078787-M3NThu6bgr.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Iren owns seven self-built data center campuses located in British Columbia, Canada, as well as Texas and Oklahoma in the United States; currently, four data centers are operational, with a running capacity of 810MW and contracted electricity exceeding 4.5GW.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776421083222-SmQG3qq41E.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776420827657-GDFJWIUAk0.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

The Childress campus Horizon 1 (50MW IT load) has been recently completed, while construction and equipment procurement for the Horizon 2 site are ongoing; Sweetwater 1 (1.4GW) is expected to be powered up by April 2026, and Sweetwater 2 (600MW) is planned to go live by the end of 2027; the existing 160MW capacity in British Columbia, Canada, is being continuously transitioned from ASICs to GPUs, with the goal of completing this by the end of 2026.

Mining firms transitioning into AI benefit primarily from their vast and low-cost power and land resources.Bernstein analysts pointed out that mining companies' grid-connected power can reduce AI data center deployment time by 75%, with very low capital expenditure required to retrofit existing facilities, making them ideal partners for AI cloud providers. This model allows mining companies to quickly enter the market and seize the opportunity.

Iren leverages its mining network, access to low-cost electricity (3.5 cents/kWh), grid connection capabilities, and internal engineering expertise to develop a vertically integrated high-density data center. This vertical integration model eliminates reliance on third-party hosting providers, and more importantly, removes all associated counterparty risks, enabling Iren to debug GPU deployments faster and maintain full control over execution and uptime.

4. Oracle: Traditional database giant transitions into an AI cloud infrastructure powerhouse

$Oracle (ORCL.US)$ At the annual investor conference held on October 17, 2025, in Las Vegas, clearer guidance updates were provided regarding the gross margin of artificial intelligence infrastructure projects, the latest order situation, and the company’s long-term financial goals, further boosting market confidence:

GPU Cloud Gross Margin:For example, taking AI workload infrastructure projects (such as data centers), a six-year AI infrastructure project with total revenue of $600 billion could achieve a gross margin of 35%, and this level of gross margin 'is also relevant even for the largest customers.'

GPU Cloud Large Agreement Status:Within 30 days of the previous quarter, Oracle's cloud computing division, Oracle Cloud Infrastructure, had booked $65 billion in new commitments, including a $20 billion deal with Meta, while the latest $65 billion in orders all come from clients outside OpenAI.

Long-Term Financial Target Guidance Raised:Revenue is expected to reach $225 billion by fiscal year 2030, significantly higher than the average analyst estimate of $198 billion. Additionally, the company expects adjusted earnings per share (EPS) to reach $21 at that time, compared to the current consensus estimate of $18.5. Previously, at the end of 2024, Oracle announced that in FY2029, annual revenue would grow to at least $104 billion.

![AI computing infrastructure supplier $CoreWeave (CRWV.US)$ Within just a week, it secured massive orders worth up to $33.8 billion. On April 9, CoreWeave announced a $21 billion expansion agreement with Meta; then on the 10th, it successfully secured a multi-year contract worth $6.8 billion with Anthropic. On the 15th, Jane Street, a giant in quantitative trading, also joined in, signing a $6 billion computing power procurement agreement and injecting an additional $1 billion. This wave of positive news has made CoreWeave the market focus, with its cumulative increase nearing 35% since April 9. However, CoreWeave's rally is just the tip of the iceberg. Beyond these positives, what profound changes have occurred recently in the 'new cloud (Neocloud)' industry centered on AI computing power rental and infrastructure? Which core players should we be closely watching? This article will provide an in-depth analysis. What recent changes are happening in the Neocloud industry as a whole? I. Core Catalyst: GPU rental prices experience a strong 'V-shaped' reversal The most direct catalyst for this round of sector growth,Due to the rise in computing power rental fees. On April 7th,[Share Link: Breaking the Depreciation Curse! GPU Rental Fees Soar, How Far is Neocloud’s ‘V-Shaped’ Rebound?]In an article...](https://nnqimage.futunn.com/sns_client_feed/900080/20260417/web-1776421109816-TeCsozjo5Q.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Summary

Overall, China Merchants Securities believes that the rise of AI Neocloud is fundamentally driven by the overflow demand for AI computing power due to structural mismatches in supply and demand, the outsourcing demand for assets brought about by changes in capital structure, and the combined effects of evolving technical requirements and ecosystem interest restructuring. Both domestic and overseas AI giants have a continuous incentive to seek computing power leasing firms for outsourcing their computing needs.

The bank argues that the long-term value of Neocloud providers stems from three core competencies: firstly, control over scarce computing resources (such as GPUs, electricity, etc.), which determines their scalable growth potential; secondly, deep optimization capabilities in AI infrastructure, which determine the cost structure, utilization, and profitability per unit of computing power; and thirdly, the ability to manage financial leverage, which dictates the efficiency of commercial returns.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

50

125