Strong rebound in March non-farm payroll! Will there still be a rate cut this year?

Options Sir's Macro View | Repeated conflicts in the Middle East, has the market become desensitized? Can we be a bit more optimistic now?

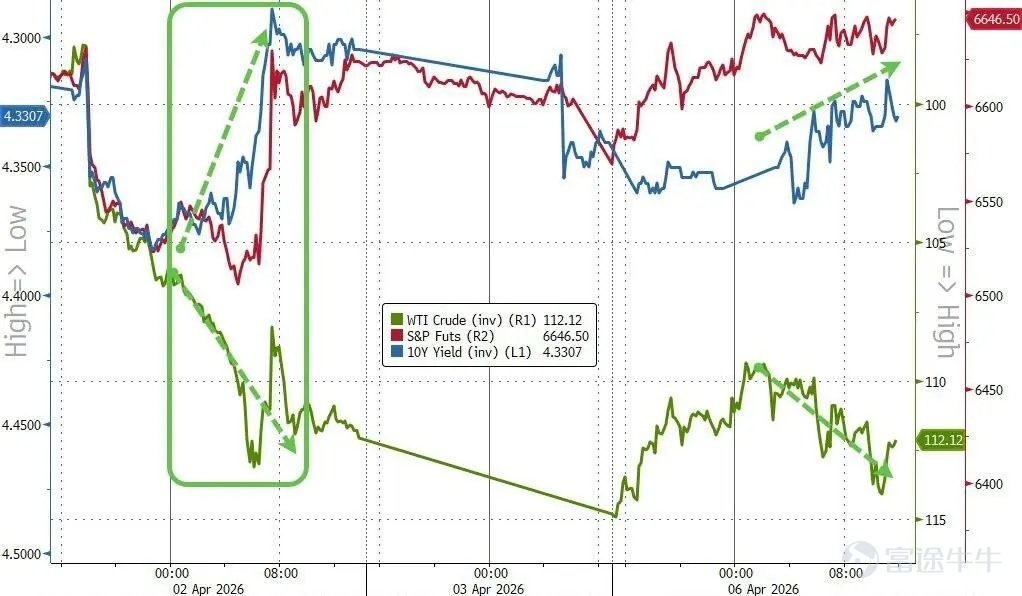

The US-Iran conflict has lasted five weeks, with various overnight reports surrounding the war with Iran continuing. However, the market is showing a new reaction to the war: despite oil prices (the green line inversely representing WTI crude) continuing to rise, US stocks (the red line representing the S&P index) have 'risen instead of fallen'.

On April 6,$S&P 500 Index (.SPX.US)$ and $Nasdaq Composite Index (.IXIC.US)$ both recorded their fourth consecutive trading day of gains, $Crude Oil Futures (JUL6) (CLmain.US)$ Closing above $112, the 10-year US Treasury yield retreated to around 4.33%. So far, $S&P 500 Index (.SPX.US)$ and $Dow Jones Industrial Average (.DJI.US)$ has rebounded above its 200-day moving average, and the Nasdaq closed exactly at the 200-day moving average; if it continues to rise tonight, it may break through.Only a few hours remain before the deadline for Iran to accept the agreement. During the Asian trading session on Tuesday, the performance of various asset classes remained generally stable.

Citadel Securities analyst Nohshad stated in the latest research report: 'Neither side intends to take the more costly next step; the negotiation window is opening, and the Strait of Hormuz is ultimately expected to "naturally reopen." As tail risks recede, the stock market may rebound ahead—there's no need to wait for the smoke to clear, only for the risk boundary to become clear, and capital will move accordingly.'

This rare divergence of simultaneous stock and bond rallies with oil prices independently rising has led the market to start discussing whether repeated Middle East conflicts have desensitized investors. Is it now the right time to position?

The market is no longer fully pricing every headline, and the boundaries of the game are becoming clearer.

From the sentiment of Reddit users, there is growing numbness toward Trump’s repeated statements.Although factors such as the 48-hour ultimatum headlines and inflation concerns are still reasons for investor hesitation, with a defensive stance prevailing, initial positive signals have emerged from various data, including valuations being compressed to extremes and cross-asset sentiment entering oversold territory.

Figure: Trump's Evolving Ultimatum

This 25,000-word field research report released by Citrini Research on April 6 over the weekend caused significant fluctuations in the market. According to Citrini’s analysis, the Strait of Hormuz is not “completely closed” as the market imagined but rather Iran has established ade facto navigation management systemIn any scenario, the ultimate outcome isThe Strait of Hormuz has reopened, the only difference being who controls it and who collects the 'toll.' Given the domestic political situation in the US and the high cost of full-scale war, Iran believes that the first two scenarios are highly likely, giving them a strong chance of success.

This means that the market's most feared tail risk of the 'permanent closure of the Strait of Hormuz' is less likely. The path will ultimately lead to the opening of the strait; it’s just a matter of time.

Image: The report analyzes Iran’s calculations through a decision tree diagram.

In the recent bout of volatility, tech growth stocks have been the hardest hit, something everyone can feel.The question is, does a drop in price mean that fundamentals have deteriorated as well?

The forward P/E ratio of MAG7 has rapidly contracted from 31.2x at the beginning of the year to 23.7x, representing a nearly 24% compression, which is now close to the overall valuation level of the S&P 500. However, at the same time, the forward earnings of these companies continue to reach new highs, with the IT sector’s profit margins leading the entire market.According to Reuters data on March 31, the expected earnings growth rate for the US tech sector in 2026 remains at 43%, significantly higher than the S&P 500’s overall level of 18.8%.

In other words, the current market pressure on tech and AI-related stocks is more a result of shifts in risk appetite, oil prices, interest rates, and revaluation of valuations, rather than a systematic collapse in earnings.

Of course, this does not mean blind optimism for tech stocks. In 2026, tech giants’ AI infrastructure investment is expected to reach approximately $635 billion. High oil prices and more expensive energy will directly test the logic behind this capital expenditure. If energy costs remain persistently high, the AI supply chain could face pressures on profit margins and spending plans. For this reason, the market is currently discounting many AI assets.

So, a more reasonable view at this point is neither "AI is finished" nor "AI will immediately recover across the board," but rather:Many quality assets have already been repriced, but whether they can continue to recover depends on earnings verification.This is also why the upcoming earnings season is critical. The market has already started trading ahead of the Q1 earnings season, using performance to test two things:First, whether corporate profits have been significantly eroded by high oil prices and high interest rates; second, whether there has been any substantial loosening in AI capital expenditure and return expectations.The former relates to whether the recovery at the index level can hold, while the latter pertains to whether growth stocks can regain dominance.

Stock prices may rise, but sentiment does not necessarily warm up in tandem.

The market has indeed started to become 'desensitized,' but this desensitization is more akin to numbness to noise rather than immunity to risk.

A concerning signal emerged in the US stock options market yesterday:The overall trading volume of US stock options hit a new low for the year.The main decline came from call options, particularly those of popular individual stocks like Mag7, chips, and memory, which saw significant contraction.

Based on historical experience,the market's interim bottom is often accompanied by an increase in panic trading, which means a rise in options trading volume. When panicked investors are aggressively buying put options or selling at a loss, trading volume tends to spike significantly. However, the current contraction in trading volume reflects heavy investor hesitation: everyone is waiting, too afraid to act, neither willing to buy the dip nor to cut losses.

Retail flow data from J.P. Morgan shows that US individual investors have recently shifted from the familiar 'buy the dip' strategy to a more defensive 'sell the rip,' with trading activity dropping sharply from the January peak, as more funds have moved into defensive assets and inverse ETFs. In other words, this is not an environment where widespread enthusiasm has returned and people are rushing to buy the dip. Many are still in defense mode, questioning whether this might just be a dead cat bounce.

The initial rebound comes from position and valuation adjustments,A broad-based recovery in sentiment often requires another round of data and event confirmation. At this juncture, it feels more like a shift from extreme pessimism toward neutrality, but we haven't reached the stage where aggressive moves can be justified.

Can we be more optimistic now? How should investors respond?

The core focus of market positioning this week isn't simply answering the question 'Has the bottom been reached?' That question is too absolute. A more practical question would be:Is this the right time to gradually increase risk exposure? For some, the answer may be yes; but it may not suit everyone.Particularly around the evening of April 7, a key geopolitical juncture, and the inflation data release between April 9 and 10, markets face considerable uncertainty risks.

What will truly determine whether the market can extend this round of recovery further is yet to be seen.In the short term, there are three things to focus on:

First, whether the situation in the Strait of Hormuz escalates further in a negative direction.

Second, whether high oil prices show up more prominently than expected in the PCE and CPI data.

Third, whether the Q1 earnings season can demonstrate that earnings have not been battered as much as prices.

(1) For investors with inherently low risk appetites,

Taking aggressive bottom-fishing positions at this point may not offer an attractive risk-reward ratio. Especially around the key geopolitical events on the evening of April 7 and the inflation data release between April 9 and 10, the market faces significant gap risks.

(2) For short-term traders who are comfortable with high volatility,

You can focus on thoseValuations have dropped but earnings support remains.areas. On the other hand, sectors that have already been heavily crowded by the logic of conflict might not be the most comfortable entry points, even if their underlying logic remains correct.

Prioritize Bull Call Spreads in bullish market conditions.Such structures feature 'visible maximum losses and limited costs.' By using a controlled cost, seize rebound opportunities while managing short-term volatility risks. Wait for clearer reversal signals and gradually increase positions after these signals appear, rather than rushing to take a full position at once. Let’s illustrate this strategy with an example: $Invesco QQQ Trust (QQQ.US)$ As an example for strategy implementation:

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

(2) For investors with higher risk appetites who are also interested in accumulating positions amid volatility,

Investors may consider cash-secured put options. This strategy essentially predefines a cost-effective entry point for potential technical pullbacks while enhancing returns or cushioning potential losses by collecting premiums.

The strike price should be set at a strong support level where you are willing to hold the underlying asset. This provides a safety buffer during stock price fluctuations and corresponds to the technical support zone in case the rebound fails and prices retreat.

It is important to note that in a highly volatile market environment, this strategy carries higher risks. Sufficient cash must be reserved to cover exercise obligations, ensuring the 'cash-secured' nature of the strategy and avoiding margin risks.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

Finally, here's a small perk for fellow investors—welcome to claim it!Options Beginner Pack

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Futu's simulated trading challenge is now open for registration! Zero cost, zero risk, and you could win stock cash vouchers!For more details, click here

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in buying and selling options can be substantial. In some cases, your losses may exceed the initial margin amount deposited. Even if you set contingent orders, such as 'stop-loss' or 'limit' orders, these may not necessarily prevent losses. Market conditions may make these orders unexecutable. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any account deficit arising from this. Therefore, before trading, you should study and understand options and carefully consider whether such trading suits you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures upon exercising options and at expiration, as well as your rights and obligations when exercising options and at expiration.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (2)

to post a comment

19

20