Micron reports earnings after the market close on Wednesday—could the sharp pullback present a buyin

Samsung's Q1 profit is expected to soar 8-fold! How to capitalize on the storage supercycle? Keep this list of core stocks and ETFs handy.

The frenzy over AI infrastructure construction is creating a super bottleneck in chip supply, and Samsung Electronics is reaping the greatest benefits from this round of price increases.

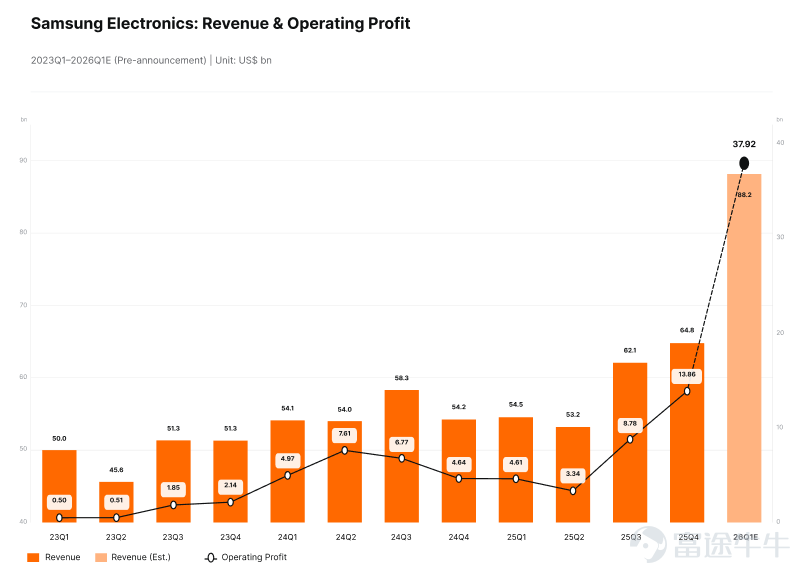

April 7,$CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$On April 7, the company released a highly impactful preview of its Q1 2026 performance: Samsung expects consolidated operating profit for January to March to be approximately57.2 trillion Korean won(approximately $37.9 billion), a year-on-year increase of over8 times—last year's same period was only 6.69 trillion Korean won.

What does 57.2 trillion represent?This not only sets a new record for Samsung’s highest-ever quarterly profit, but also reaches 1.3 times the company’s projected profits for the full year of 2025 (about 43 trillion Korean won)—literally 'one quarter’s earnings surpassing an entire year’s.'

Even more impressive is that, driven by strong demand for memory chips, Samsung has completed price negotiations with key clients for Q2 DRAM contracts,with prices surging approximately 30% from Q1.

Bank of America Securities analyst Kim Sunwoo explained the logic behind the better-than-expected results:“Due to client expectations of further price increases, actual contracted prices were higher than expected, which is why results exceeded forecasts.”

The impressive macroeconomic and industry data is already clear. How will this blockbuster earnings report guide the subsequent trends in the memory sector? Which core US and Hong Kong stock targets may benefit from this wave of ‘profit spillover’? We’ll break it down for you.

Two Major Catalysts for Samsung's Stock Movement: Pricing Power and Governance Turning Point

Despite recent short-term fluctuations in Samsung's stock price caused by rising energy costs amid geopolitical tensions in the Middle East, better-than-expected Q1 results have quickly drawn Wall Street’s attention to a strong fundamental turnaround.

Following the release of an impressive Q1 earnings preview,JPMorgan believes that investors' focus will now shift to the Q1 consolidated earnings report, scheduled for release on April 30, and the subsequent earnings call. There are two reasons for this:

1) As customers negotiating long-term agreements (LTAs) prefer Q2 pricing over Q3 as the base price, Samsung Electronics may seek to implement significant price hikes in Q2;

2) With cleanroom capacity still being a key bottleneck, both clients and investors will continue to strongly advocate for increased capital expenditure (capex) to meet excessive demand. Semiconductor equipment stocks, particularly those related to advanced memory and logic chips, are likely to remain in focus for investors.

Although most investors may still value memory stocks based on the price-to-book (P/B) ratio, significantly outperforming profits could prompt us, along with market consensus, to raise forecasts, thereby boosting book value and increasing shareholder returns.The stock price is also expected to return to recent highs.

Additionally,More crucially, it has been reported that the Samsung family will pay off the remaining inheritance tax owed for the late former chairman Lee Kun-hee within this month.This marks the formal conclusion of one of the largest inheritance tax payments in South Korean history.

After paying the inheritance tax, the Samsung family will alleviate financial pressure. Analysts believe that completing this payment may mark a turning point for Samsung, enabling it to overcome financial and governance constraints related to the succession process. Lee Jae-yong was acquitted last year in an improper merger case, freeing him from legal difficulties. Coupled with strong overall performance in sectors like Samsung Electronics' semiconductors, the removal of uncertainties in Samsung’s management will be largely achieved once the inheritance tax is settled.

Some analysts believe that Samsung may next increase its investments in semiconductors, artificial intelligence, and biopharmaceuticals, and may accelerate business restructuring.

How to understand the global memory industry and which companies are worth watching?

To seize investment opportunities in the storage industry, fellow investors first need to understand the storage architecture of AI systems. If we compare the storage architecture of an AI system to the human memory system, it is actually a 'four-layer pyramid' with clearly defined levels where performance and cost are precisely matched:

At the very top is AI's 'working memory'—HBM (High Bandwidth Memory).This is the most valuable, fastest, yet also the scarcest space in the entire pyramid due to capacity constraints. It is directly physically packaged with GPUs and stores core model weights. For example, in an 8-GPU H100 server, the total HBM capacity is only about 800GB, but it serves as the high-speed engine determining the limits of AI computation.

The second layer down is AI's 'short-term memory'—DRAM (server memory).As a flexible buffer outside the GPU, its capacity is typically 4 to 5 times that of HBM. It primarily holds KV Cache—the context just entered by users, data that needs frequent access but does not occupy the GPU core, all temporarily stored here to ensure smooth conversation flow.

The third layer is AI's 'long-term memory'—SSD (solid-state drive), with NAND Flash being its core medium.This acts like a physical filing cabinet that won’t forget even when powered off. With capacities ranging from 1TB to 15TB, it stores knowledge bases required for RAG retrieval, massive user session archives, and agent state data. The NAND medium perfectly hits the sweet spot of 'large capacity and low cost,' making it the backbone storage solution in the AI inference era.

At the very bottom lies the 'deep subconscious' of AI — HDD (mechanical hard drives).This is like a dusty basement warehouse. Although it remains largely invisible in daily AI inference tasks, it plays a critical role in cold archiving of massive training datasets and extreme disaster recovery scenarios, thanks to its cost-effectiveness, forming the base of the pyramid.

So which core stocks are worth paying attention to? Previously,‘2026 Outlook | Nomura, J.P. Morgan, and other investment banks unanimously predict: The storage industry may see a super cycle by 2026! What investment opportunities should be watched?’we also compiled related concept stocks in the memory industry, as follows:

First of all, $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$and$CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$these are the two giants in the global memory chip field, currently benefiting from the AI wave and strong demand for high-bandwidth memory (HBM),Both companies have promising earnings prospects, with their stock prices hitting new highs repeatedly. The two firms are increasing R&D efforts to capture the HBM4 market and drive the transition from traditional memory to high value-added AI memory.

In the US stock market, the clearest reflection is, $Micron Technology (MU.US)$。Micron has just announced revenue of $23.86 billion for the second quarter of fiscal 2026, stating that record results were driven by strong demand, tight industry supply, and the strategic value of memory in the AI era.Therefore, when Samsung also reports significant earnings surprises, investors naturally interpret this as further evidence that the memory cycle remains robust.

Yes$SanDisk (SNDK.US)$The mapping is also positive, but the logic is slightly different.SanDisk has greater exposure to NAND flash memory and enterprise SSDs. In the most recent quarter, SanDisk reported revenue of $3.03 billion, with its data center revenue surging 64% quarter-over-quarter, driven by large-scale AI deployments from AI infrastructure builders and major tech customers. If Samsung is signaling that memory and storage demand remains tight, flash-related stocks will also be drawn into this narrative logic.

Regarding$Western Digital (WDC.US)$and$Seagate Technology (STX.US)$Although this connection is more indirect, it remains very real.AI generates massive amounts of data, much of which ultimately needs to be stored in low-cost bulk storage. During its Innovation Day, Western Digital stated that 90% of its revenue is currently driven by AI and cloud; Seagate, on the other hand, noted that AI applications are boosting data generation and value, driving enormous demand for cost-effective exabyte-level storage in data centers.

For investors who don’t want to bet solely on individual stocks and prefer to capture the entire storage sector, $Roundhill Memory ETF (DRAM.US)$this provides an excellent investment path.It allows investors to easily track the core leaders in global memory and storage devices, encompassing well-known companies such as Micron, Samsung, SK Hynix, SanDisk, Western Digital, and Seagate. The emergence of this type of DRAM ETF essentially addresses a key pain point: it successfully isolates pure 'storage exposure' from traditional national indices, transforming it into an asset that investors can trade independently.

Calm Reflection Amid the Frenzy

Despite Samsung delivering what could be called an 'explosive' performance, the game of cyclical stocks always peaks amidst optimism. For investors closely tracking the AI infrastructure supply chain, the following three potential risk signals must be carefully considered behind the dazzling earnings:

Macroeconomic Headwinds: The 'butterfly effect' triggered by Middle East conflicts.The direct impact of geopolitical conflicts is the surge in energy costs and uncertainty in the supply of critical materials. It is well-known that electricity is one of the largest operational expenses for AI data centers. If energy prices remain high, tech giants may be forced to cut their overall capital expenditures (Capex) — which would undoubtedly affect and potentially weaken upstream demand for memory chips. Market concerns are already reflected in stock performance: Samsung's share price has retreated by about 11% since the conflict began.

Technological Impact: Tech Giants’ ‘Cost-Cutting’ BacklashIn addition to the macro environment, the evolution of underlying technologies could also reshape demand patterns. For instance, Google’s recently released memory-saving technology 'TurboQuant' — an innovation aimed at optimizing models and reducing hardware dependency — has triggered market concerns over whether long-term AI memory demand might be compressed. This factor is also considered by investors as one of the key catalysts behind the recent sell-off in the memory chip sector.

Cycle Concerns: Entering the Mid-to-Late Stage of 'Price Competition'The memory industry cannot escape the gravitational pull of strong cyclical trends. Ryu Young-ho, senior analyst at NH Investment & Securities, stated frankly: 'Market concerns over the peak of memory price increases are intensifying. Currently, it appears we have moved past the early upward cycle and entered the mid-to-late stages.' He emphasized,Whether Samsung can successfully sign long-term agreements (LTA) with customers to lock in semiconductor profits will be a core factor in maintaining its valuation.

Meanwhile, Avril Wu, senior vice president of TrendForce, pointed out a dangerous leading indicator: spot prices for DRAM fell last week. The reason is straightforward — 'End-user demand can no longer absorb such high pricing.' Since spot prices are typically higher than contract prices and are the most sensitive to market conditions, this weakening indicator has undoubtedly sounded an alarm for overly bullish sentiment.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (34)

to post a comment

122

258