Energy transition accelerates! Which electric vehicle stocks stand to benefit the most amid high oil

[Opportunity Express] 'White Petroleum' Amid the Energy Crisis: Is Lithium Set for a Second Wave of Growth?

As tensions between the US and Iran continue to escalate, with the Strait of Hormuz nearly closed, crude oil prices repeatedly surge to new highs. While global attention is focused on the flames of the Middle East and oil tankers, another resource crucial to the future of energy cannot be overlooked: lithium, a silvery-white lightweight metal.

Just as oil is the lifeblood of the industrial age, lithium serves as the cornerstone of the electrification era, an indispensable core element for electric vehicle batteries and energy storage.Lithium resources have thus earned the nickname "white petroleum."

Currently, the global lithium market stands at a critical turning point, with a complex shift driven by geopolitical conflicts, supply chain restructuring, and surging demand unfolding.

Can the recovery of the cycle carry the momentum into wave 2?

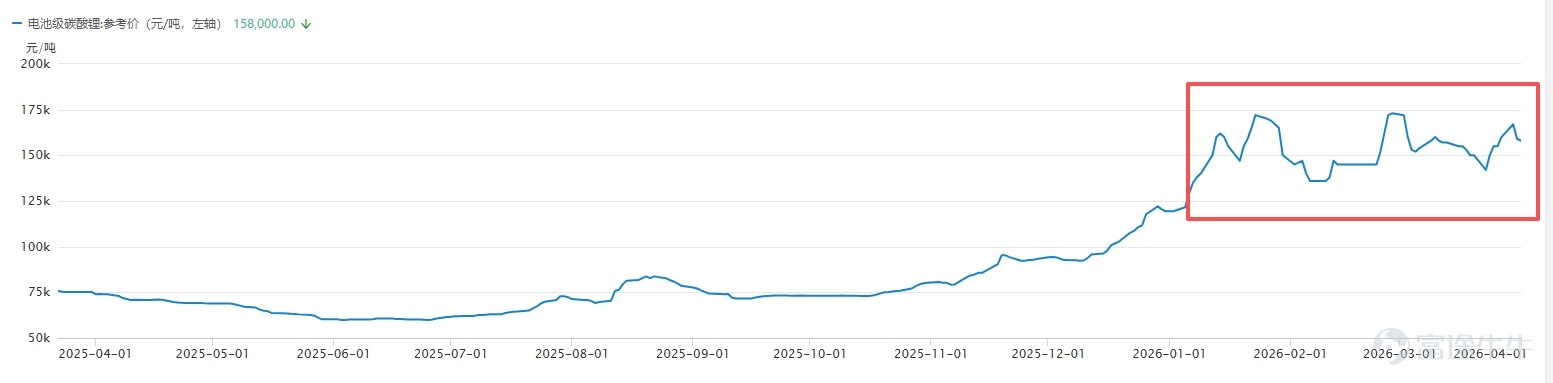

The previous downturn in the lithium industry was devastating. From 2023 to the first half of 2025, battery-grade lithium carbonate prices plummeted from a peak of CNY 567,600 per ton to CNY 58,000 per ton, a drop of over 89%. Overall industry operating rates hovered around 50%, while the operating rate of mica smelting capacity fell to near 30%. Some mines in Australia shut down, industry giants incurred losses, and market confidence hit rock bottom.

However, a turning point began to emerge in the second half of 2025.The unexpected surge in energy storage demand became the key driver – a phenomenon fueled by the AI computing revolution that has given rise to the "energy storage narrative." The global data center construction boom is accelerating the growth of lithium demand for industrial energy storage, making energy storage the core variable in the lithium market’s transition from "cyclical rebound" to "structural rebalancing."

In short, Wave 1 (the rebound starting in the second half of 2025) will be primarily driven by the energy storage narrative, with lithium carbonate futures rebounding from a mid-year low of 59,000 yuan per ton to a level of 150,000 yuan per ton.

It is worth noting that although energy storage has experienced relatively rapid growth in recent years,demand for power batteries (represented by the light blue bars in the chart below) still dominates lithium battery demand,which is also an important reason for lithium prices entering a prolonged period of volatility after rising.

Data source: IEA.

Entering 2026, especially following the escalation of geopolitical tensions between the US and Iran, the core market contradiction shifts to whether, under the dual pressures of a traditional energy crisis and a new geopolitical landscape, the price momentum initiated by the energy storage narrative can successfully transition and usher in a strongersecond wave (Wave 2).?

Currently, high oil prices are producing a dual acceleration effect:

Economic acceleration: Rising crude oil prices have significantly improved the economics of electric vehicles compared to fuel-powered cars,The risk-averse sentiment among consumers and businesses has quickly translated into strong demand for new energy vehicles, a trend that has been particularly evident in overseas markets recently.

Strategic acceleration: Amid geopolitical crises, new energy sources have been redefined as strategic resources related to 'full-chain self-controllability and energy security'.Countries’ motivation to reduce dependence on oil has increased dramatically, pushing new energy power generation and energy storage from 'optional configurations' to 'infrastructure',which further amplifies the demand for lithium resources.

This crisis has brought an 'acceleration' in demand for lithium. If the conflict in the Middle East drags on, the demand for power batteries, which constitutes the largest share of demand, is expected to see a sustained rebound.

Triple shock, supply side faces hard constraints

The impact of the US-Iran conflict on the lithium sector goes far beyond the linear logic of 'rising oil prices → accelerating new energy substitution'.The deeper transmission path lies in the fact that the conflict has caused a direct physical impact on lithium mining itself through the energy supply chain.This is a core risk that the market has not yet fully priced in.

The central hub of this transmission chain is Australia, the world's leading supplier of lithium resources. While Australia’s lithium mining industry appears to boast the highest quality hard rock spodumene resources globally (accounting for about 30% of global supply), its entire operational system relies heavily on an extremely fragile imported diesel supply chain.

The mining sector is the largest consumer of diesel in Australia, with processes from ore extraction, crushing, and beneficiation to transportation over hundreds of kilometers all highly dependent on diesel power.Australia’s domestic crude oil resource endowment and refining capacity are severely inadequate, with nearly 90% of refined oil products (including diesel) reliant on imports.The primary sources of diesel imports include Singapore, South Korea, and China, where refineries themselves rely heavily on crude oil from the Middle East.

As of March 2026, Australia’s total national diesel inventory can only last 15 to 30 days.This makes it one of the countries with the lowest inventory levels among International Energy Agency member states.At remote mining sites, fuel inventories may only suffice for about three weeks. This “high consumption + high import reliance + low inventory” model renders the 'fuel artery' of Australia’s lithium mines exceptionally vulnerable.

The production halt risks caused by interruptions in basic energy supplies are more destructive than mere cost increases, potentially causing rigid shortfalls in a short period that cannot be offset by price adjustments.

In addition, the supply side is currently facing two major constraints:

On one hand, policy interventions by resource-rich nations have become the new norm. In February this year, Zimbabwe, a key lithium resource country, announced the suspension of all lithium raw ore and concentrate exports to promote local processing. While this move has limited impact on companies that have already invested in deep processing, it signals that the 'low-cost free-flow era' for lithium resources may be coming to an end, forcing the market to pay a premium for ongoing policy uncertainties.

On the other hand, domestic supply elasticity is also constrained. The resumption pace of some mica-based lithium mines in Jiangxi remains uncertain. Additionally, CATL's large lithium mine (with an annual capacity of 65,000 tons of lithium carbonate equivalent) has halted production due to an expired license, with its resumption unclear, further weakening the buffer capacity on the supply side.

The original market consensus was that the lithium industry would still experience a slight surplus in 2026. However, the sudden change in the US-Iran situation has prompted institutions to revise their forecasts to tight balance or even substantial shortages.

Why are salt lakes more noteworthy than lithium mines?

Lithium mining (hard rock mining) Highly reliant on large diesel-powered mining equipment and transport fleets, it is extremely sensitive to the physical supply of fossil fuels. Whether it’s Australia’s spodumene mines or African lithium projects, they all face dual risks of soaring diesel costs and potential supply disruptions.They are the 'losers' in this round of the energy crisis. Although rising lithium prices bring revenue benefits, uncertainty on the cost and production fronts remains relatively high.

Lithium extraction from salt lakes tells a completely different story. It is primarily distributed across South America’s 'lithium triangle' (Chile, Argentina) and Tibet/Qinghai regions in China. The production process mainly relies on solar evaporation in salt flats, reducing dependence on external energy sources like diesel.Mature salt lake projects boast the lowest cash production costs globally, offering strong resistance to price fluctuations. During periods of rising lithium prices, profit margins can expand significantly.

For investors seeking to allocate lithium resources globally, these companies not only own salt lake assets but also generally engage in diversified global resource deployment:

$Albemarle (ALB.US)$ : The absolute leader in the global lithium industry, its business spans lithium, bromine, and catalysts. Its lithium resource pillar includes long-term leasing rights to Chile's Atacama Salt Lake (one of the highest-grade and lowest-cost salt lakes globally) and partial interests in Australia’s Greenbushes mine. The company is one of the largest lithium product suppliers globally, serving all mainstream battery and automobile manufacturers. Its scale, cost advantages, and deep client binding make it a 'stabilizing' asset within the lithium cycle.

At the end of last year, the Niumao Classroom also analyzed ALB, providing a detailed introduction to the company’s resource layout and financial status. Fellow investors who are interested can revisit it, and we welcome everyone to keep an eye on the Niumao Classroom~

$Sociedad Quimica Y Minera De Chile (SQM.US)$ : The core asset is the mining rights to Chile’s Atacama Salt Lake, which is also one of the lowest-cost lithium sources globally. SQM and ALB both have significant operations at this salt lake. The company is also a major global producer of iodine, potassium, and specialty fertilizers.Its lithium business is growing rapidly, making it a pure-play benchmark for salt lake lithium extraction.

$GANFENGLITHIUM (01772.HK)$:On the salt lake front, Ganfeng has built a vast asset portfolio in Argentina, involving four salt lake projects, though their operational history is relatively short compared to Atacama Salt Lake.

$TIANQI LITHIUM (09696.HK)$:Tianqi holds approximately 20% of SQM shares through its wholly-owned subsidiary, making it the second-largest shareholder of SQM.

Here, I’d like to remind fellow investors,During the first wave of rising lithium prices last year, these companies generally accumulated significant gains,Market sentiment and capital博弈 have been fully ignited, with the price itself already reflecting significant volatility. If the situation in the Middle East eases quickly and the Strait of Hormuz resumes navigation, the logic of scarcity could weaken rapidly.

From the current perspective, the narrative around lithium has evolved from purely AI-driven growth to a dual-driver phase characterized by 'rigid demand growth' combined with 'supply vulnerability crisis.' The energy crisis triggered by the US-Iran conflict unexpectedly struck at the heart of lithium mining, adding to policy risks in Zimbabwe and insufficient domestic supply elasticity to form a triple supply shock, which is highly likely to catalyze and amplify the upward cycle of lithium prices.

Risk Disclosure: This content does not constitute a research report and is for reference only. It should not be used as the basis for any investment decision. The information involved in this article is not a comprehensive description of the mentioned securities, markets, or developments. Although the source of the information is considered reliable, no guarantee is provided regarding its accuracy or completeness. Additionally, no assurance is given regarding the accuracy of any statements, opinions, or forecasts provided herein.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

14

52