Strong rebound in March non-farm payroll! Will there still be a rate cut this year?

Hormuz Risk Reassessment: How Should We Invest When Oil Prices Surge to $110?

The situation in the Middle East has persisted for weeks, with recent escalations signaling an extreme stress test for global markets regarding a 'supply-side shock.' As Brent crude surpasses $110, expectations of Federal Reserve rate cuts have been pushed back due to re-inflation risks. Investors now face not just volatility but a restructuring of asset pricing logic.

Supply Shock and the Specter of Re-Inflation

The chain reaction from the recent Middle East situation has shifted market trading focus from 'geopolitical disruptions' to 'persistent supply shocks.' As of March 19, Brent crude surged to $112.86 per barrel during intraday trading. Damage to Qatar's Ras Laffan LNG hub and attacks on Saudi energy facilities have intensified concerns.The risks associated with the Strait of Hormuz—the 'chokepoint' for global energy supplies—are being repriced.

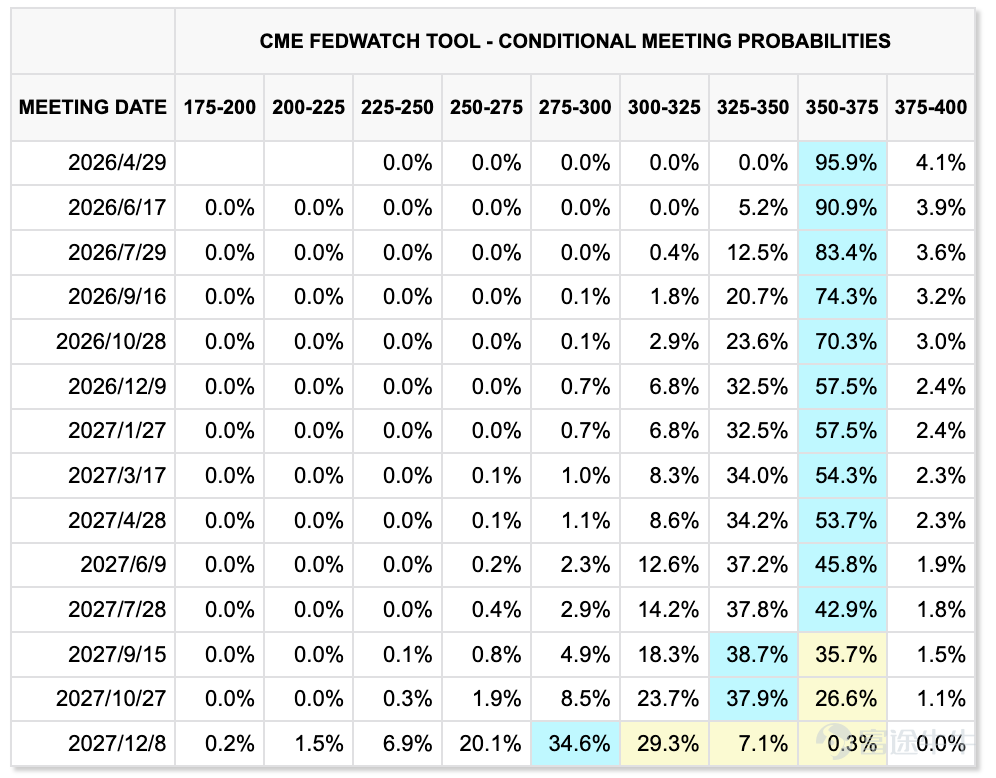

This is not an isolated energy event. The Strait of Hormuz handles nearly 20% of global oil supplies and about 20% of LNG trade flows; any blockage or disruption would naturally carry strong inflationary spillover effects. Meanwhile, the Federal Reserve maintaining the federal funds rate at 3.5%-3.75%, along with the dot plot signaling only one rate cut this year,has created a 'Higher for Longer' interest rate environment alongside persistently high oil prices.。

The market currently stands at a crossroads of conflicting expectations:

- Scenario 1: Rapid Recovery: If transport routes are restored within weeks and extreme risk premiums recede, the EIA forecasts oil prices to return below $90 by 2026.

– Scenario 2 Long-Tail Disruption: If the production halt extends, oil prices will experience a severe transmission akin to the 1970s. BofA and Standard Chartered have significantly raised their forecasts, warning of deeper permeation of oil prices into the economic system.

This atmosphere is reminiscent of a rehearsal for '1970s-style reflation': on one side, cost-push from the supply side, and on the other, equity assets undergoing dual repricing in terms of growth and interest rates. The BofA Global Fund Manager Survey shows that cash allocation rebounded sharply from 3.2% in January to 4.3% in March,marking the largest monthly increase since the pandemic in 2020.The logic of institutional investors has shifted from 'gambling elasticity' to 'liquidity defense.'

The Paradox of Safe Havens: Why Is Gold Falling Too?

Facing surging oil prices and geopolitical conflicts, the short-term weakness of gold has left many investors puzzled, with gold futures breaking below the key level of $5,000 per ounce on March 18.

The underlying logic involves a double barrier of 'liquidity squeeze' and 'real interest rates':

1. Dollar Liquidity Siphon Effect: During the most intense initial phase of geopolitical shocks, the dollar is often the first choice for safe-haven flows. Investors tend to sell various assets, including gold, to secure dollar liquidity.

2. High holding costs due to elevated interest rates:As inflation expectations rise, the market is betting that the Federal Reserve will delay interest rate cuts, and the increase in real yields on U.S. Treasuries is putting direct pressure on gold.

However, short-term volatility has not undermined gold's medium-term logic. Data from the World Gold Council shows that as of February 2026, global physical gold ETFs have recorded net inflows for nine consecutive months, with their assets under management reaching a new high of $701 billion. The continued central bank gold-buying spree and geopolitical uncertaintieshave provided solid medium- to long-term 'bottom support' for gold prices.。

Building a defensive framework: From cash to options hedging

In volatile markets, relying solely on one asset for defense often appears insufficient. What deserves more attention now is constructing a three-layered defensive framework:

The first layer remains cash or cash equivalents.When geopolitical shocks bring supply-side impacts with 'unknown durations,' the role of cash is not only to prevent drawdowns but also to retain liquidity for the next round of mispricing. The current move by institutions to increase cash holdings does not mean they are bearish on everything; rather, they are waiting for clearer visibility and reserving firepower for future opportunities.

The second layer consists of a base position in gold ETFs.For most ordinary investors, gold ETFs are more suitable as a 'medium-term defensive asset' than chasing individual mining stocks, futures, or highly leveraged derivatives. They also play an important role in long-term asset allocation.

The third layer involves using options to hedge against downside risk.For investors with a heavy position in US stocks, the most reasonable approach right now is not to bet naked on direction, but to use an option structure with controllable costs and known maximum losses to manage the portfolio's Beta first.

Cash-like instruments:

The underlying assets are ultra-short-term US Treasury bonds/T-Bills ETFs, which have low credit risk and minimal volatility: $iShares 0-3 Month Treasury Bond ETF (SGOV.US)$$SPDR Bloomberg Barclays 1-3 Month T-Bill ETF (BIL.US)$

Gold ETF Toolkit:

Gold: $SPDR Gold ETF (GLD.US)$$iShares Gold Trust (IAU.US)$, as well as leveraged ETFs $ProShares Ultra Gold (UGL.US)$$ProShares UltraShort Gold (GLL.US)$which can be used to speculate on short-term gold volatility opportunities

Gold mining stock ETFs: $VanEck Gold Miners Equity ETF (GDX.US)$ These carry significant equity Beta, making them offensive instruments rather than pure hedging tools, and they possess stronger offensive attributes. $MicroSectors Gold Miners 3X Leveraged ETN (GDXU.US)$

Options Defensive Strategies:

Under the logic chain of 'rising oil prices—delayed rate cuts—valuation contraction,' the risk of holding positions without protection is extremely high. Below are three practical hedging approaches:

1. Bear Put Spread:

a.Applicable Scenarios: Concerned about a systemic market pullback in the next 1-3 months.

b.Operation: Buy at-the-money Puts while selling Puts with a lower strike price.

c.Advantages: Effectively reduces premium costs and precisely manages downside risks, especially when negative feedback has already emerged in the S&P 500 and Nasdaq.

2. Protective Collar Strategy:

a.Applicable Scenarios: Holding core tech stocks like NVIDIA and Microsoft, unwilling to reduce positions but worried about valuation compression.

b.Operation: Buy Puts to lock in downside risk while selling out-of-the-money Calls to collect premiums that offset costs.

c.Core: Sacrifice some potential upside in exchange for stable net asset value during periods of extreme volatility.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

In the coming weeks, the market's performance will depend on the evolution of the following three variables:

1. Repair rate: The extent of damage and progress in repairs at the Strait of Hormuz and surrounding facilities.

2. Transmission depth: Whether oil prices fully trigger inflation expectations through gasoline and freight costs, forcing the Federal Reserve to shift to 'hawkish rate hikes' rather than merely 'delaying rate cuts'.

3. Real interest rates: When will the US Dollar Index and real yields on US Treasuries stop putting short-term pressure on gold?

In this unclear situation, a defensive matrix of 'cash + gold base + options hedging' might be a more robust survival strategy than blindly guessing market direction.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

7

12