Strong rebound in March non-farm payroll! Will there still be a rate cut this year?

Options Sir's Macro View | FOMC kicks off tonight! No doubt about staying put, but which of the three scenarios will dominate the market?

At 2:00 AM Beijing time on March 19, the Federal Reserve's new interest rate decision will be announced, while the current market is under pressure. $S&P 500 Index (.SPX.US)$ 、 $Nasdaq Composite Index (.IXIC.US)$ Both falling to their lowest levels this year, the Middle East conflict has pushed oil prices back to above $100 per barrel, and market sentiment remains cautious. This FOMC meeting appears to have almost no suspense on the surface:The Fed’s current policy rate remains at 3.50%-3.75%, and the market widely expects no rate adjustment tonight.

What’s truly important is not the ‘no change’ itself, but how the Fed will redefine this increasingly conflicting macro combination: On one hand, the U.S. February CPI was up 2.4% year-on-year, and core CPI rose 2.5% year-on-year, suggesting inflation seems somewhat under control; on the other hand, Nonfarm payrolls decreased by 92,000 in February, with unemployment rate at 4.4%, combined with Q4 2025 GDP growth revised down to 0.7%, showing a clear slowdown in growth.

More importantly,Tonight's meeting comes with the dot plot and economic forecasts. The statement will be released at 14:00 EST, with Powell holding a press conference at 14:30. Therefore, what the market will truly trade on is the 'path,' not the 'outcome'.

What investors should watch most tonight is not the interest rate decision but four more critical signals.

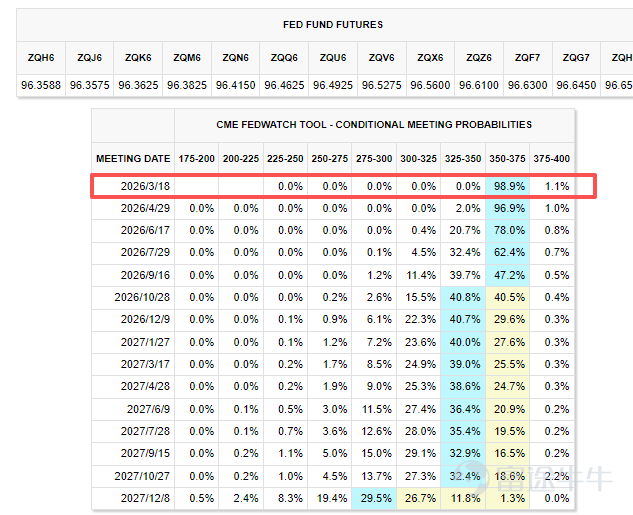

First, check if the dot plot has turned even more hawkish.In December last year, the Fed's median projection still pointed to only one rate cut in 2026; Currently, Goldman Sachs, Standard Chartered, and Jefferies are highly consistent in their views: the median forecast for interest rate cuts in 2026 remains at one time, most likely to be realized in the second half of the year.

Goldman Sachs expects that the March dot plot will maintain this view, but the distribution of dots is likely to shift: the oil price shock has heightened inflation concerns among some officials, potentially pushing 2-3 dots higher; on the other hand, both Goldman Sachs and Citi have noted that the weakening job market, with unemployment approaching 4.6%, could pull some dots lower.

If tonight’s new dot plot shifts from 'one' rate cut towards 'zero,' or even signals that 'tighter policy may be necessary if inflation picks up again,' the market will interpret this meeting as a de facto hawkish repricing. Conversely, if the dot plot broadly maintains the framework of 'one rate cut,' it suggests that the Fed has not been completely swayed by short-term oil price shocks.

Second, observe how the economic forecasts are revised.

The most noteworthy aspect isn’t this year’s nominal data, but whether the Fed simultaneously lowers growth forecasts, raises unemployment forecasts, and lifts inflation projections.If all three occur simultaneously, the market will immediately recognize an issue: the Fed is not facing a normal slowdown, but rather an environment closer to 'stagflationary disruptions.' Reuters has already pointed out that the current focus of internal debate within the Fed is whether the Iran conflict resembles more of a growth shock, an inflation shock, or the 'most difficult combination' of both.

Third, observe how Powell characterizes the oil price shock.

This is actually the most critical question tonight. If Powell emphasizes that the rise in oil prices is more of an 'exogenous, short-term, reversible' supply disruption and clearly states that the Fed is more focused on whether core inflation and inflation expectations are spiraling out of control, then the market will interpret this as 'the Fed does not urgently regard an energy shock as comprehensive re-inflation.' However, if he repeatedly stresses the lessons from 2022 and expresses concerns that energy prices could spill over into broader prices and expectations, it would mean that the Fed is starting to view this shock as more severe. The analysis cited by Reuters has already mentioned that some economists are even beginning to discuss a question that was hard to imagine just weeks ago:Is there room to reopen discussions about rate hikes in 2026?。

Fourth, observe whether the Fed's sensitivity to growth and financial conditions has increased.

US retail sales for January fell month-over-month 0.2%, fourth-quarter GDP was notably revised downward, and February employment data was also weak, meaning that as long as the Fed slightly emphasizes 'tightening credit,' 'falling asset prices,' or 'rising uncertainty,' the market will interpret this as: although the Fed hasn't turned dovish, it has begun to acknowledge that the combination of high oil prices and high interest rates is eroding demand.

What impact do the three major scenarios have on your portfolio?

Scenario One: 'Hold steady + verbally cautious + largely unchanged dot plot' (mainstream institutional consensus)

Powell announces maintaining interest rates unchanged, keeping his tone balanced, acknowledging the inflationary pressure brought by oil prices without overemphasizing panic, and the dot plot maintains expectations of one rate cut in 2026.

In this scenario, the market will digest the news calmly. It will likely interpret it as 'not more hawkish than feared,' leading to a mild relief rally in risk assets.This is especially true for growth sectors previously weighed down by front-end rates. The S&P 500 and Nasdaq 100 ETFs are likely to consolidate around their yearly lows or even experience a slight recovery; defensive sectors and commodity-related segments remain resilient, with energy ETFs showing strong resistance to declines, while interest-rate-sensitive assets see limited volatility.

Scenario Two: More Hawkish Than Expected

Typical characteristics include the dot plot shifting towards 'zero rate cuts' or Powell clearly emphasizing inflation, stressing that energy shocks may lead to broader second-round effects.

In such a case, the market’s initial reaction typically focuses less on the long end and more on the 2-year U.S. Treasury yield, with a stronger dollar pressuring technology and high-valuation growth stocks. What the market fears most right now is not that there will be no rate cut tonight but that the Fed tightens its future easing path even further.Reuters has already noted that investors are highly sensitive to any mention of 'revisiting rate hikes.' Currently, the 2-year yield is particularly sensitive to shifts in policy expectations.

The tech sector and growth stocks are most sensitive to delayed rate cut expectations, $Invesco QQQ Trust (QQQ.US)$ 、 $iShares Russell 2000 ETF (IWM.US)$ often leading the declines; energy and commodity sectors (such as energy ETFs and Exxon Mobil) historically show relative resilience, while long-term U.S. Treasury ETFs face noticeable pressure.

Scenario Three: More Dovish Than Expected (Low-Probability Reversal)

This means that although the Fed does not cut rates, it significantly lowers growth forecasts and raises unemployment projections, with Powell placing greater emphasis on weakening demand and cooling employment. He tends to view oil price shocks as one-off disturbances and is unwilling to tighten further due to energy prices.

In this scenario, interest rate-sensitive assets, long-duration sectors, and gold are more likely to receive support, with the market re-betting on an earlier rate cut starting in the second half of the year.In fact, even though war and rising oil prices have disrupted expectations, many economists in the Reuters survey still believe thatJunecould be the first rate cut of the year. This indicates that there is a camp in the market where 'growth concerns outweigh inflation concerns.' Interest rate-sensitive sectors will benefit the most, including residential construction ETFs (such as Horton Homes, Lennar), the Russell 2000 small-cap ETF, and gold ETFs among other physical assets, all of which will see significant gains against the backdrop of declining real interest rate expectations.

It should be noted, however, that the sustainability of this dovish reaction depends on an external variable:whether oil prices can fall back quickly.. If oil prices do not retreat, any rebound driven by a 'dovish Fed' can easily be eroded by subsequently higher inflation expectations.

Options strategy

Recently, $SPDR S&P 500 ETF (SPY.US)$ and $Invesco QQQ Trust (QQQ.US)$Both experienced a round of pullbacks from their late February highs, and current technical indicators show weakening downward momentum, with funds beginning to flow in at lower levels, entering an oversold recovery phase.

As of March 13, the IV percentile for SPY was 85%, while for QQQ it was 74%. The implied volatility (IV) of both recently retreated somewhat from its highs, and the high Put/Call ratio indicates caution. This suggests that the options market expects significant volatility in future stock prices, but panic has eased compared to previous highs. Against the backdrop of three overlapping sources of volatility—'FOMC decision + Triple Witching Day + geopolitical risks'—market volatility is expected to remain elevated.

(1) Trade with the trend

On days of major economic events (such as the Wednesday FOMC decision) or technical events (such as Friday's Triple Witching Day), investors anticipating rapid and sharp directional breakouts may consider buying same-day expiry options with higher leverage for short-term trend-following trades, or wait for confirmation of direction after the 2:00 PM statement and 2:30 PM press conference before engaging in trend trading.

For example, if the price of QQQ breaks through a key resistance level with high trading volume, buy call options with a strike price slightly higher than the current price; otherwise, buy put options. Choose the contract with the highest trading volume to ensure liquidity.

It should be noted that the capital allocation for a single trade should be relatively small, and a strict stop-loss level must be set, as the value of options can quickly drop to zero on the expiration day.

(2) Short volatility

If it is expected that the market will not experience extreme one-sided movements but rather fluctuate within a certain range, an Iron Condor strategy can be considered. This involves simultaneously selling an out-of-the-money call option and an out-of-the-money put option while buying further out-of-the-money call and put options to limit risk, forming a four-legged combination.

This is a more trading-oriented approach and may not be suitable for beginners. The rationale is: before the FOMC meeting, volatility expectations are often priced into options; if QQQ moves within a limited range after the meeting, market makers selling options are more likely to profit. However, if QQQ surges or plunges significantly in one direction, losses will expand, so it is essential to use a protective structure rather than selling options uncovered.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

Finally, here's a small perk for fellow investors—welcome to claim it!Options Beginner Pack

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Futu's simulated trading challenge is now open for registration! Zero cost, zero risk, and you could win stock cash vouchers!For more details, click here

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in buying and selling options can be substantial. In some cases, your losses may exceed the initial margin amount deposited. Even if you set contingent orders, such as 'stop-loss' or 'limit' orders, these may not necessarily prevent losses. Market conditions may make these orders unexecutable. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any account deficit arising from this. Therefore, before trading, you should study and understand options and carefully consider whether such trading suits you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures upon exercising options and at expiration, as well as your rights and obligations when exercising options and at expiration.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

30

27