有沒有一種戰法可以穿越牛熊市?

Lexion Outdoor Faces Significant Performance Pressure: Annual Dividend of 65 Million Exceeds Net Profit, OEM Model Constraints Remain Unsolved

As the world's largest fishing gear manufacturer, Lexion Outdoor International Limited (hereinafter referred to as Lexion Outdoor) has attracted significant market attention on its road to an IPO. This company, which has over 30 years of industry experience and grew from OEM origins to become a hidden champion in the sector, launched its third attempt at a main board listing by the end of 2025 after two previous filings with the Hong Kong Stock Exchange, with CICC serving as the exclusive sponsor.

However, issues exposed in the latest prospectus, such as significant performance fluctuations, high customer concentration, and reliance on the OEM model, combined with related-party transaction controversies involving controlling shareholder Taipusen Group, have cast a shadow over this IPO journey.

Performance remains unsatisfactory, with dividends exceeding net profit for the period

It is reported that Lexion Outdoor’s development can be traced back to 1993. The core operating entity, Zhejiang Lexion Outdoor Products Co., Ltd., was established in June 2022, while the listing entity completed its equity structure adjustment in 2024. After more than 30 years of accumulation, the company has built a global sales network, with clients including international brands like Decathlon, RapalaVMC, PureFishing, and UK-based brands such as Fox and Nash. Currently, its products are sold in over 40 countries, covering mature markets in Europe and America, as well as emerging regions like China and Southeast Asia. According to Frost & Sullivan data, the company ranked first among global fishing gear manufacturers with a 23.1% market share based on 2024 revenue.

However, the leading position failed to bring stable financial performance. During the reporting period (2022, 2023, 2024, and January-August 2025), the company's operating revenues were RMB 818 million, RMB 463 million, RMB 573 million, and RMB 460 million, respectively, with annual profits of RMB 114 million, RMB 49 million, RMB 59 million, and RMB 56 million. In 2023, revenue fell by 43.4% year-over-year, while net profit dropped by 57%. Although there was a recovery in 2024, it still remains significantly below the peak profitability seen in 2022. The company explained that the sharp decline in 2023 was mainly due to consumers shifting back to other entertainment activities after the public health crisis subsided, resulting in a natural slowdown in demand for fishing gear.

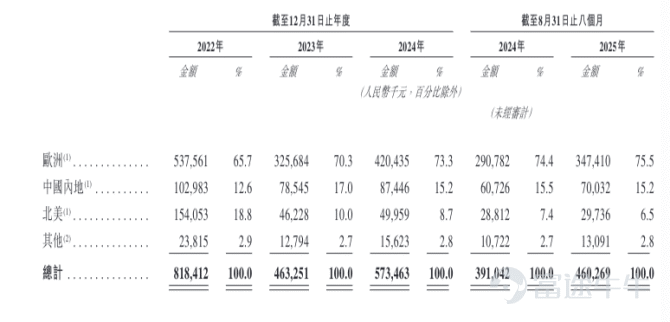

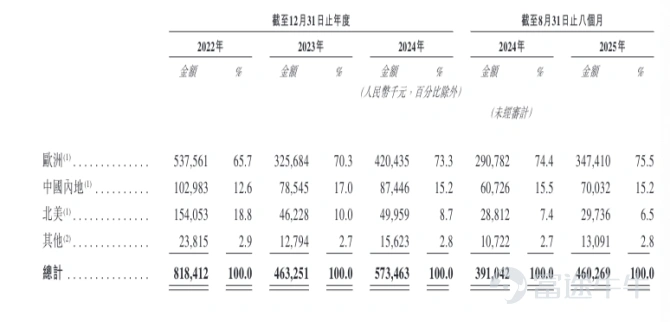

Performance in regional markets added to the uncertainty. From 2022 to 2024, revenue from Europe decreased from RMB 538 million to RMB 420 million, a drop of 21.8%; revenue from North America plummeted from RMB 154 million to RMB 50 million, down 67.6%; and revenue from mainland China slightly declined from RMB 103 million to RMB 87 million, a decrease of 15.1%. The company stated that European and American markets surged in 2022 as the low-social-interaction nature of fishing aligned with pandemic-driven consumer preferences, but orders naturally receded after the pandemic waned in 2023. Meanwhile, the Chinese market managed to stabilize declines through strategies such as acquiring new customers and focusing on brand clients.

Signs of market recovery emerged in the second half of 2024. As of August 2025, European revenue increased from RMB 291 million to RMB 347 million, growing by 19.5%; revenue from mainland China rose from RMB 61 million to RMB 70 million, an increase of 15.3%; and North American revenue stabilized within the range of RMB 29-30 million.

Notably, despite profits not yet fully recovered, the company proceeded with a substantial cash dividend. In July 2024, the board approved a dividend payout of RMB 65 million to the controlling shareholder Zhejiang Taipusen, exceeding the net profit for the period (RMB 59.4 million) by 9.4%.

Calculated by shareholding ratio, Yang Baoqing was the primary beneficiary of this dividend, receiving RMB 61.6 million. He indirectly holds 88.06% of shares through GreatCast and, as the sole shareholder of Taihong—the general partner of Outrider Partnership—controls 6.71% of equity held by the partnership, bringing his total control over issued capital to 94.77%.

Renowned financial audit expert Liu Zhigeng commented: 'The dividend decision made by Lexin Outdoor indeed carries certain risks, analyzed from four aspects: 1) Direct risk of dividend exceeding net profit: Cash flow pressure—with a 2024 net profit of RMB 59.4 million but dividends of RMB 65 million, the excess must be covered by other funds, potentially affecting daily operations; debt risk—if cash reserves are insufficient, borrowing or asset sales may be required, increasing financial costs; funding chain risk—tight cash flow post-dividend could impact key investments like R&D and market expansion. 2) Significant lack of prudence—due to the company’s single business model, fragile product structure, and weak risk resistance, dividends should have been more conservative. 3) Harm to long-term development—most companies maintain dividend ratios at 30%-50% of net profit, whereas Lexin Outdoor far exceeds industry norms, negatively impacting long-term growth.'

4) Recommendations: Based on the above, it is advised that the company optimize its business structure to reduce reliance on a single market and cautiously manage dividend ratios to ensure financial stability and meet normal funding needs for R&D, operations, and market expansion.

Related-party transactions pose concerns, being both a customer and a supplier.

Additionally, Lexin Outdoor faces operational risks associated with highly concentrated client structures and related-party transactions. Its OEM/ODM clients primarily include outdoor equipment brands and retailers. During the reporting period, revenues from the top five clients accounted for 57.5%, 57.2%, 57.7%, and 54.9% of total revenue, respectively, while revenues from the largest client represented 17.9%, 15.7%, 15.4%, and 17.7% of total revenue, respectively.

Supplier concentration is also relatively high. The company’s suppliers mainly consist of raw material providers (including hardware and fabric suppliers). During the reporting period, procurement amounts from the top five suppliers accounted for 30.9%, 27.2%, 31.7%, and 34.9% of total procurement, respectively, while those from the largest supplier represented 14.2%, 12.8%, 11.2%, and 14.8% of total procurement, respectively.

More notably, Lexin Outdoor has complex related-party transactions with its controlling shareholder. Taipusen Group was one of the top five customers in each year during the reporting period and also ranked among the top five suppliers. The services procured by the company from Taipusen Group mainly included warehousing and processing services. During the reporting period, the procurement amounts were RMB 83.1 million, RMB 33.7 million, RMB 48.1 million, and RMB 20.9 million, accounting for 14.2%, 12.8%, 11.2%, and 7.8% of the total procurement during the same period, respectively.

The products purchased by Taipusen Group from the company mainly included chairs, beds and other accessories, tents, and bags. During the reporting period, the revenue generated from these sales was RMB 88.8 million, RMB 61 million, RMB 62 million, and RMB 54.4 million, accounting for 10.9%, 13.2%, 10.8%, and 11.8% of the total revenue during the same period, respectively.

This cross-relationship of being both a customer and a supplier obviously raises suspicions of potential interest transfers. During the reporting period, the gross profit margin from sales to Taipusen Group was 12.5%, 18.2%, 20.7%, and 21.2%, which was lower than the company’s overall gross profit margin of 23.2%, 26.6%, 26.6%, and 27.7% during the same period.

Lexin Outdoor stated that its sales to and purchases from Taipusen Group were not conditional on each other. All sales and purchase transactions with Taipusen Group were conducted under normal commercial terms and fair principles during the ordinary course of business. The terms of the agreements signed between the company and Taipusen Group were basically consistent with those signed with other suppliers and customers.

Coincidentally, another top-five client, Client B, also acted as the company's supplier in 2024. Client B is a professional sporting goods retailer, specializing in outdoor and sports products. This client owns a subsidiary responsible for supplying raw materials, so Client B also provides raw materials to its own clients.

The raw materials purchased by the company from Client B were mainly fabrics. Client B’s core business is outdoor product sales, and it typically provides exclusive raw materials to OEM/ODM suppliers, including the company, to ensure product quality and control material costs. During the reporting period, the procurement amounts from Client B were RMB 1.6 million, RMB 0.6 million, RMB 0.9 million, and RMB 4.2 million, accounting for 0.3%, 0.2%, 0.2%, and 1.6% of the total procurement during the same period, respectively.

The products purchased by Client B from the company mainly included chairs, beds and other accessories, tents, and bags. During the reporting period, the sales revenue from Client B was RMB 93.6 million, RMB 72.8 million, RMB 88.4 million, and RMB 81.5 million, accounting for 11.4%, 15.7%, 15.4%, and 17.7% of the total revenue during the same period, respectively. The company explained that its cooperation arrangement with Client B was neither a bundled transaction nor a back-to-back transaction arrangement.

Over 90% reliance on contract manufacturing, weak momentum for proprietary brands

Lexin Outdoor adopts a dual business model, combining original equipment manufacturing/original design manufacturing (OEM/ODM) capabilities with a growing proprietary brand manufacturing (OBM) business to meet diverse market demands. With a rich product portfolio, advanced product design and development capabilities, a flexible supply chain, and strict quality control systems, the company provides full-process OEM/ODM solutions from product design to manufacturing for outdoor fishing gear brands, and has become a leading provider of OEM/ODM solutions in the global fishing gear sector.

The deep-rooted challenge in the company’s business model lies in its over-reliance on OEM/ODM contract manufacturing, with more than 90% of revenue coming from “private label production” for international brands such as Decathlon, RapalaVMC, and PureFishing. During the reporting period, income from the OEM model accounted for as high as 94.1%, 90.2%, 92.3%, and 93.1% of total revenue.

Although the company acquired the British brand Solar in 2017 in an attempt to build a proprietary brand portfolio, the results were lackluster. Solar's sales in 2024 increased about threefold compared to 2018, but its absolute scale remains small, contributing less than 10% to overall revenue. During the reporting period, the proportion of the proprietary brand (OBM) business was 4.1%, 8.5%, 7.2%, and 6.6%, respectively.

Jian Junhao, a well-known strategic positioning expert and founder of Fujian Huace Brand Positioning Consulting, stated: 'More than 90% of Lexin Outdoor’s revenue relies on OEM, which, while providing stable orders and cash flow in the short term, suffers from weak bargaining power, thin profit margins, and vulnerability to customer and industry cycle impacts, resulting in insufficient risk resistance. Although its proprietary brand Solar has tripled its sales compared to 2018, its revenue contribution is only 6.6%-8.5%, and the growth has not translated into a second growth curve. The core bottleneck lies in insufficient brand investment, underdeveloped channel and marketing systems, and resource allocation conflicts between OEM and OBM. To break through, it needs to increase R&D and brand investment, leverage manufacturing advantages accumulated through OEM, create differentiated products, and gradually increase the OBM share to enhance profitability and risk resistance.'

In terms of R&D investment, during the reporting period, the company's R&D costs were 523,000 yuan, 3.906 million yuan, 3.538 million yuan, and 3.821 million yuan, respectively. In contrast, sales and distribution expenses for each period were 12.332 million yuan, 14.196 million yuan, 16.939 million yuan, and 14.895 million yuan, respectively, indicating a clear characteristic of 'heavy marketing, light R&D'.

From the perspective of industry trends, the global fishing gear market is moving towards branding and intelligent development. According to Frost & Sullivan data, the global market size reached 140.9 billion yuan in 2024 and is expected to grow to 194.1 billion yuan by 2029. However, Lexin Outdoor remains trapped in the OEM model, lacking influence in key areas such as brand premium, technological innovation, and channel control. If it cannot accelerate the construction of its proprietary brand, even if it successfully lists on the Hong Kong Stock Exchange, its long-term investment value remains questionable. (Produced by Harbor Finance)

Xu Huijing, Harbor Commercial Observer

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment