[2026 Outlook] Plan Ahead! Share the Investment Opportunities You Are Optimistic About

2026 Outlook | Nomura, JPMorgan, and other investment banks unanimously predict: The storage industry is expected to enter a supercycle by 2026! Which investment opportunities should be closely watched?

Fellow investors, 2025 is coming to an end, and as we face a brand-new 2026, instead of anxiously chasing trends, it’s better to calm down and understand the direction of the market. Stay tuned.@Niuniu Classroomto unlock your investment roadmap in real time. In the new year, let’s stay calm and patient, proceed steadily for long-term success, and slowly grow our wealth together.

In 2025, the explosion of AI computing power reshaped the global storage market landscape.

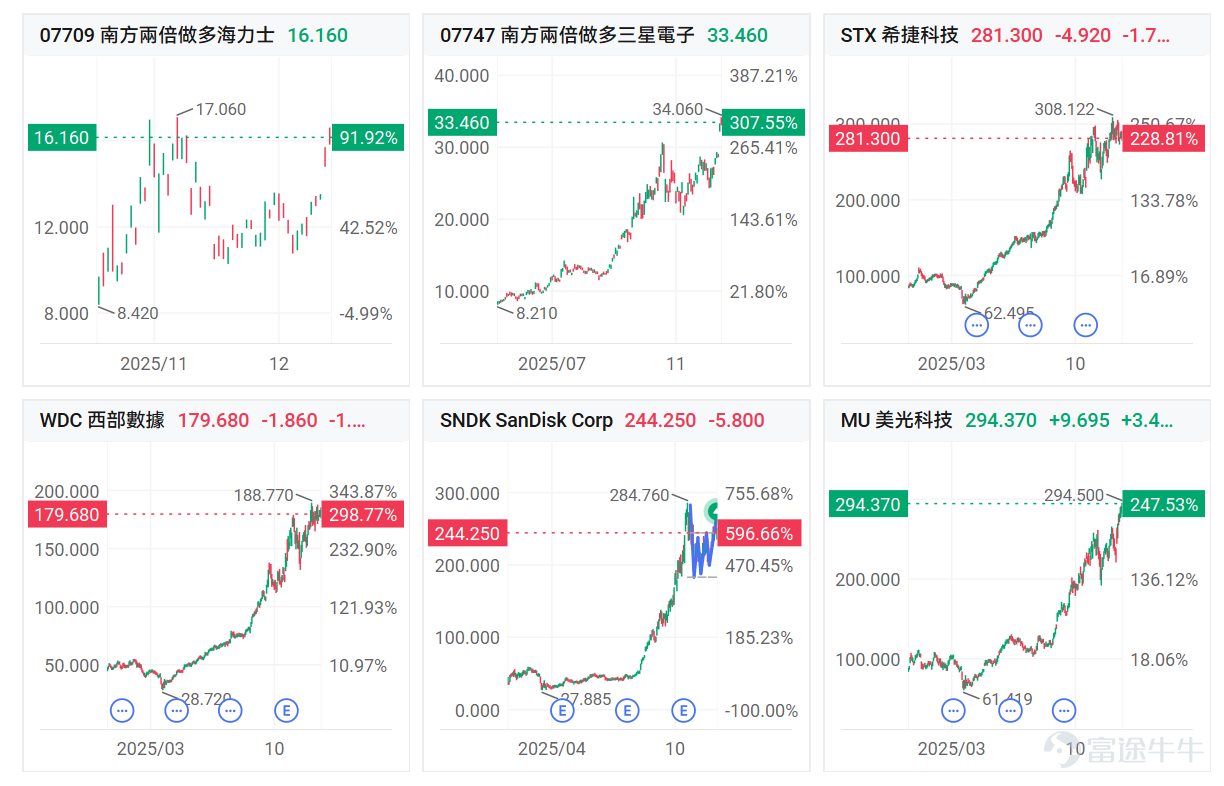

Looking at this year’s storage concept stocks, these companies have entered a super bull market, among which $SanDisk (SNDK.US)$ rose nearly 600% year-to-date, $Western Digital (WDC.US)$ 、 $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$ surged almost threefold, $Seagate Technology (STX.US)$ 、 $Micron Technology (MU.US)$ increased more than twofold, and $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$ , listed less than two months ago, has already risen nearly 100%.

![Fellow investors, 2025 is coming to an end, and as we face a brand-new 2026, instead of anxiously chasing trends, it’s better to calm down and understand the direction of the market. Stay tuned.[Share Link: @Niuniu Classroom]to unlock your investment roadmap in real time. In the new year, let’s stay calm and patient, proceed steadily for long-term success, and slowly grow our wealth together. In 2025, the explosive growth of AI computing power reshaped the global storage market landscape. Looking at this year's storage-related stocks, these companies have experienced a super bull market, with some $SanDisk (SNDK.US)$ rising nearly 600% year-to-date, $Western Digital (WDC.US)$ 、 $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$ surging almost threefold, $Seagate Technology (STX.US)$ 、 $Micron Technology (MU.US)$ increasing more than twofold, while $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$ , which has been listed for less than two months, has already risen nearly 100%. Looking ahead to 2026, where will the capital flow indicators point? After an in-depth analysis, [Share Link: Chip]and[Share Link: Optical communications]we focus on a key segment of the AI landscape to exclusively reveal potential opportunities for fellow investors:The storage industry in 2026, as viewed by Wall Street's leading banks, and the key investment opportunities it holds. Nomura, JPMorgan, and other major investment banks have collectively predicted: the storage industry is poised to enter a supercycle! The global surge in demand for AI training and inference computing power, coupled with the consumer electronics boom driven by edge AI...](https://nnqimage.futunn.com/sns_client_feed/900080/20251230/web-1767093841004-8LUpr0peee.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Looking ahead to 2026, where will the capital wind vane point? After an in-depth forecast,ChipandOptical communicationswe focus on a key component of the AI landscape, exclusively revealing to fellow investors:Wall Street's leading banks' perspective on the storage industry in 2026 and the critical investment opportunities hidden within.

Nomura, JPMorgan, and several other investment banks have unanimously predicted: the storage industry is poised to enter a supercycle!

The global explosive expansion of AI training/inference computing power demand, along with the consumer electronics demand recovery driven by the edge AI boom, has comprehensively fueled exponential growth in demand for DRAM/NAND series storage products.Particularly in the DRAM segment, which occupies the largest share of Samsung, SK Hynix, and Micron’s storage businesses—specifically HBM storage and server-grade high-performance DDR5. Additionally, enterprise SSD demand within the NAND sector has recently shown a sharp increase.

In fact, over recent months, the exceptionally robust earnings reported by the world’s top three memory chip giants—Samsung Electronics, SK Hynix, and Micron—as well as storage leaders such as Western Digital and Seagate, have ledinvestment banks on Wall Street, including Nomura, JPMorgan, and Morgan Stanley, to proclaim the arrival of a 'storage supercycle.'

Nomura Securities recently stated thatthis 'storage supercycle,' which began in the second half of this year, is expected to last at least until 2027.And the earliest that truly meaningful new supply will emerge is likely to be in early 2028.

The Nomura analyst team stated,Investors should continue to overweight leading memory companies in 2026, with the investment theme focused on the 'price-profit-valuation' triple play for memory chips in 2026,rather than treating memory purely as a single HBM-related theme. The firm expects the three major memory chip companies to achieve record-high profitability.

JPMorgan stated that the current cycle will be the longest and strongest upcycle for memory in history.

After a significant rise in memory stocks over the past three months, pushing their combined market value close to the $1 trillion mark, what’s next?JPMorgan’s answer is very clear: continue to go long.

Based on a valuation framework using 'market capitalization / total addressable market (TAM),' JPMorgan forecasts that the memory market size will reach approximately $420 billion by 2027. Using the median price-to-sales (P/S) ratio of 3.5x from the cycles in 2018 and 2021, the combined market cap of leading memory and storage manufacturers could approach $1.5 trillion by 2027.This implies that, from current levels, leading players still have more than 50% upside potential.

Source: JPMorgan

According to a Morgan Stanley report,the traditional memory storage market is entering a powerful 'super cycle' driven by supply shortages.It is projected that DDR4 contract prices may surge over 100% in the first quarter of 2026, with NOR Flash prices also set to rise significantly. The report believes the current cycle is far from over, stating that market profit forecasts are overly conservative and it is too early to take profits now.

According to a UBS report,the storage industry is currently facing an unprecedented supply-demand imbalance.In terms of DRAM, the supply shortage is expected to persist until the first quarter of 2027, with DDR demand growing by 20.7%, significantly outpacing supply growth. The NAND shortage is projected to extend until the third quarter of 2026. This will drive the strongest upcycle in the memory sector in nearly 30 years.

Moreover, media reports indicate that tech giants are actively seeking to procure memory chips, with Google, Amazon, Microsoft, and Meta placing open-ended orders with Micron in October,notifying the company that they will accept all available capacity regardless of price.

Facing tight supply conditions, there has been a fundamental shift in customer procurement strategies. Major cloud service providers have begun signing pre-purchase orders (PPOs) extending to 2027 or even 2028 to ensure long-term supply security. These agreements lock in supply volumes but not prices, leaving room for suppliers to increase pricing.

Additionally, the impact of the memory shortage is being passed on to consumers, with Xiaomi and Realme warning that they may need to raise prices. Xiaomi stated that it would offset higher memory costs through price increases and by selling more high-end phones, adding that other business segments would help cushion the impact.

What investment opportunities should be closely monitored?

As the memory industry is experiencing a supercycle characterized by strong demand and limited supply, the valuation of memory-related stocks is being readjusted. Fellow investors have also identified key companies in the supply chain that are worth monitoring, providing references for investors:

![Fellow investors, 2025 is coming to an end, and as we face a brand-new 2026, instead of anxiously chasing trends, it’s better to calm down and understand the direction of the market. Stay tuned.[Share Link: @Niuniu Classroom]to unlock your investment roadmap in real time. In the new year, let’s stay calm and patient, proceed steadily for long-term success, and slowly grow our wealth together. In 2025, the explosive growth of AI computing power reshaped the global storage market landscape. Looking at this year's storage-related stocks, these companies have experienced a super bull market, with some $SanDisk (SNDK.US)$ rising nearly 600% year-to-date, $Western Digital (WDC.US)$ 、 $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$ surging almost threefold, $Seagate Technology (STX.US)$ 、 $Micron Technology (MU.US)$ increasing more than twofold, while $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$ , which has been listed for less than two months, has already risen nearly 100%. Looking ahead to 2026, where will the capital flow indicators point? After an in-depth analysis, [Share Link: Chip]and[Share Link: Optical communications]we focus on a key segment of the AI landscape to exclusively reveal potential opportunities for fellow investors:The storage industry in 2026, as viewed by Wall Street's leading banks, and the key investment opportunities it holds. Nomura, JPMorgan, and other major investment banks have collectively predicted: the storage industry is poised to enter a supercycle! The global surge in demand for AI training and inference computing power, coupled with the consumer electronics boom driven by edge AI...](https://nnqimage.futunn.com/sns_client_feed/900080/20251230/web-1767093841640-D2rMIJWhAE.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Before delving into the study of the memory industry, let’s first introduce fellow investors to various technical terms and classifications:

Before delving into the study of the memory industry, let’s first introduce fellow investors to various technical terms and classifications:DRAMIt is Dynamic Random Access Memory (DRAM), used for temporary data storage, which disappears after power loss;

NAND Flashis a type of non-volatile memory where data is retained even after power loss and is used in SSDs and USB flash drives;

HDD refers totraditional hard disk drives that use magnetic storage, offering slower speeds but lower costs and larger capacities.

In other words,Imagine we are someone working in an office: DRAM would be your desk, NAND Flash would be your filing cabinet, and HDD would be the large archive in the corner of the office.

In summary: The CPU (you) retrieves items from DRAM (the desktop) for processing, and once processed, results or documents requiring long-term storage are saved back to NAND (drawers) or HDD (archives).

![Fellow investors, 2025 is coming to an end, and as we face a brand-new 2026, instead of anxiously chasing trends, it’s better to calm down and understand the direction of the market. Stay tuned.[Share Link: @Niuniu Classroom]to unlock your investment roadmap in real time. In the new year, let’s stay calm and patient, proceed steadily for long-term success, and slowly grow our wealth together. In 2025, the explosive growth of AI computing power reshaped the global storage market landscape. Looking at this year's storage-related stocks, these companies have experienced a super bull market, with some $SanDisk (SNDK.US)$ rising nearly 600% year-to-date, $Western Digital (WDC.US)$ 、 $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$ surging almost threefold, $Seagate Technology (STX.US)$ 、 $Micron Technology (MU.US)$ increasing more than twofold, while $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$ , which has been listed for less than two months, has already risen nearly 100%. Looking ahead to 2026, where will the capital flow indicators point? After an in-depth analysis, [Share Link: Chip]and[Share Link: Optical communications]we focus on a key segment of the AI landscape to exclusively reveal potential opportunities for fellow investors:The storage industry in 2026, as viewed by Wall Street's leading banks, and the key investment opportunities it holds. Nomura, JPMorgan, and other major investment banks have collectively predicted: the storage industry is poised to enter a supercycle! The global surge in demand for AI training and inference computing power, coupled with the consumer electronics boom driven by edge AI...](https://nnqimage.futunn.com/sns_client_feed/900080/20251230/web-1767093840804-JNlFjZMcGa.webp/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Thus, this industry includes the world’s largest DRAM and HBM supplier $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$ , the world's second-largest DRAM supplier and third-largest HBM supplier $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$ , one of the world’s top three DRAM suppliers, the second-largest HBM supplier, and the fourth-largest player in the global NAND market $Micron Technology (MU.US)$ , the fifth-largest player in the global NAND market $SanDisk (SNDK.US)$ , the world’s two largest hard drive manufacturers$Western Digital (WDC.US)$ 、 $Seagate Technology (STX.US)$ ;

, and the global leader in NAND flash memory controller solutions $Silicon Motion Technology (SIMO.US)$ , as well as a U.S.-based memory IP company $Rambus (RMBS.US)$ , a global leader in memory storage technology $Marvell Technology (MRVL.US)$ , and memory packaging vendors.$Lam Research (LRCX.US)$ , a system specializing in thin-film deposition processes for memory chips$Applied Materials (AMAT.US)$ ; a leader in enterprise memory storage technology$NetApp (NTAP.US)$ , a global leader in memory storage technology$Everpure (P.US)$ 。

Among the most noteworthy developments, the three major storage chip giants—Samsung Electronics, SK Hynix, and Micron—have concentrated the majority of their production capacity on High Bandwidth Memory (HBM) systems. These advanced memory products require sophisticated manufacturing processes, with significantly higher complexity in fabrication and packaging compared to DDR-series and HDD/SSD storage chips.As these leading storage chip manufacturers continue to shift their capacity toward HBM, it has largely contributed to a supply shortage of traditional hard disk-based storage products.

Currently, the competitive landscape of the HBM market remains relatively stable, with SK Hynix expected to maintain approximately 70% of the HBM4 market share.In the next-generation Rubin architecture, SK Hynix is anticipated to become the primary supplier. Additionally, the company may also emerge as the preferred HBM3E supplier for Google's TPU 7p, with Samsung serving as the secondary supplier.

In fact,Whether it is Google’s vast TPU AI computing clusters or NVIDIA’s extensive AI GPU computing infrastructure, both rely heavily on HBM storage systems fully integrated with AI chips.Moreover, as major tech companies accelerate the construction or expansion of AI data centers, there is an increasing demand for server-grade DDR5 memory,as well as enterprise-level high-performance SSDs/HDDs.

Therefore, analysts at Morgan Stanley pointed out thatData is the 'crude oil driving artificial intelligence,' and hard disk drive manufacturers will be significant beneficiaries.The analysts stated: "Given the consistently cyclical nature of the HDD industry, the market is currently overlooking a key point: as long-term growth momentum strengthens and structural profit margins improve, $Western Digital (WDC.US)$and $Seagate Technology (STX.US)$valuations will continue to surpass historical levels."

In addition, Goldman Sachs noted in its latest research report that SanDisk's Q3 results exceeded expectations across the board, becoming the direct trigger for boosting market confidence.The firm raised $SanDisk (SNDK.US)$its target price to $280, stating that the NAND flash memory market will remain undersupplied through 2026, granting manufacturers significant pricing power,which will ultimately translate into soaring profit margins. The bank increased its EPS forecasts for 2025-2027 by an average of 79%, attributing tight capacity driven by AI server demand as a key factor behind the supply-demand imbalance. The market has yet to fully digest the profit explosion potential of this supercycle.

Bank of America believes that the rapid growth in data center demand is significantly driving NAND flash memory pricing, and the high gross margins of enterprise SSD products will become a major profit driver. The bank has raised its earnings per share forecast for SanDisk’s fiscal year 2026 by 15.4% to $8.The firm also substantially raised SanDisk's target price from $125 to $230.and maintained a Buy rating. Analysts at Bank of America believe that,amid an AI-driven storage supercycle, the price-to-book valuation multiple of this NAND supplier should be re-rated to a level of 3-4 times.

Overall, the storage industry is entering a 'boom cycle.' However, Minsheng Securities also highlighted relevant risks:

1. This cycle is AI-driven, and if CSP (Cloud Service Provider) capital expenditures fall short of expectations, it could adversely impact the memory industry, directly affecting the recovery of the cycle.

Currently, AI inference is primarily centered around KV Cache processing. Should there be a paradigm shift in inference technology, it could lead to changes in the memory hierarchy system and potentially have an adverse impact on storage requirements.

If the development of separate manufacturing for Logic die (logic chips) falls short of expectations, affecting the mass production timelines of DRAM technologies such as 4F2, it may result in unfavorable implications for the supply dynamics within the FAB and DRAM industries.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

141

331