Viral Biotech's stock opened higher on its first day of trading! Are you bullish on its future perfo

Futu Research | How much is the value of CR Beverage's IPO subscription?

China Resources Beverage (02460) will be listed on the Hong Kong Stock Exchange from October 15 to October 18, 2024, with an expected listing date of October 23, 2024. In this IPO, China Resources Beverage plans to issue 0.348 billion shares, with 11% for public offering, 89% for placement, and an additional 15% for over-allotment option.

The offer price will not exceed HK$14.5 per share, and is expected to be not less than HK$13.5 per share, with a board lot size of 200 shares.

If calculated at HK$14.50 per share, China Resources Beverage plans to raise no more than HK$5.04 billion.

Source: Prospectus

Let's evaluate the current IPO situation of China Resources Beverage and see if it is worth subscribing to.

What is the main business of China Resources Beverage?

CR Beverage's main business covers a wide range, including the production and sales of packaged drinking water (including drinking purified water, natural mineral water, etc.) and ready-to-drink soft drinks (such as tea beverages, fruit juice, coffee beverages, etc.), with multiple well-known brands including Yi Bao, Zhi Ben Qing Run, Zuo Wei Tea Affair.

Source: Prospectus

However, we mainly found that the company's focus is on drinking water, with other beverage products accounting for a small proportion.

Source: Prospectus

Here is where it differs from Nongfu Spring. When we look at Nongfu Spring's financial report, we can see that water products do not make up a large proportion. Therefore, compared to Nongfu Spring, CR Beverage currently relies mainly on drinking water, while Nongfu Spring has a more comprehensive multi-category strategy. Therefore, logically, CR Beverage's valuation should be lower than that of Nongfu Spring.

Source: Prospectus

So let's take a look atAs a consumer product, how is the channel construction of CR Beverage?

In terms of channels, distribution is mainly used, while pricing is based on various factors such as product positioning, production cost, market competition, and the reasonable profit level of dealers and direct customers in the sales network. Therefore, we can see that CR Beverage still needs to fully consider the profit of dealers and leave enough profit margin.

Source: Prospectus

So our basic judgment on CR Beverage lies in the industry space of bottled water.

From the perspective of the prospectus, the industry can currently maintain a growth of roughly 7-8%, however, from a more conservative investment standpoint, we can consider a growth rate of around 5%.

Source: Prospectus

In the end, whether CR Beverage can achieve growth still requires observation of its strategic tactics.We can see from the prospectus:

The future strategy and tactics of China Resources Beverage will revolve around the following core areas. Overall, focusing on developing channels and production capacity, improving product categories, advertising-centric marketing, the strategy appears to be quite comprehensive:

1. Channel efficiency improvement and omni-channel expansion

China Resources Beverage will fully leverage its advantages in traditional channels, further expand its geographical coverage, and strive to enhance the overall quality of dealers to strengthen penetration capabilities in the lower-tier markets. At the same time, enhance product display and exposure in strategic retail outlets, actively exploring the potential of e-commerce channels.

2. Capacity expansion and optimization

China Resources Beverage will accelerate the pace of building its own factories, expand and improve the production capacity of existing factories, while enhancing automation and intelligence levels to achieve efficient operations.

3. Product research and innovation enhancement

China Resources Beverage will focus on expanding product portfolios, enhancing brand positioning and consumer recognition. For example, by enriching the packaging of drinking water products and varieties to meet a wider range of consumer needs, and further exploring beverage categories with huge market potential.

4. Sports Marketing Strategy Deepening

In the end, if Nongfu Spring continues to develop steadily, it will be a beverage company with a revenue growth rate of over 5%. The current market's attention is mostly on the high dividend sector, so what about Nongfu Spring's dividend policy?

From the original text in the prospectus, we can see that 'We currently have no dividend policy or predefined dividend payout ratio,' so there should be a certain degree of valuation discount here.

Combining the above conditions, we can continue to comprehensively analyze and conclude.Nongfu Spring is a steadily growing company that needs a more clear dividend policy.

Alright, now we need to look at the valuation level:

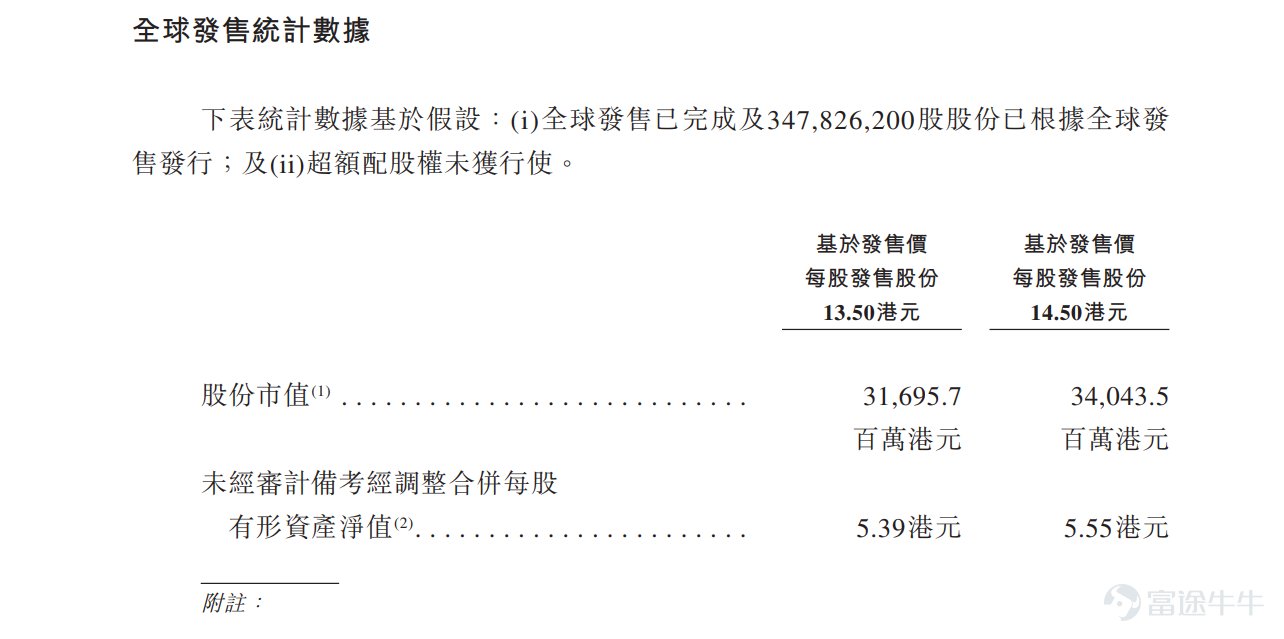

China Resources Beverage's IPO market cap range is between 31.7 billion Hong Kong dollars and 34 billion Hong Kong dollars, with a forward PE ratio of approximately 18-20 times. As mentioned earlier, China Resources Beverage is currently undervalued compared to Nongfu Spring to a certain extent. Nongfu Spring's PE ratio is about 23 times, with an overall undervaluation space of about 10-20%. Currently, we evaluate from three dimensions: fundamentals, valuation, and sentiment.

From the fundamental perspective, China Resources Beverage has room for further upside.

In terms of valuation, China Resources Beverage is relatively reasonable. If the large cap continues to stabilize and move upward in the future, there is a certain upward elasticity, which appears more likely at the moment.

In terms of market sentiment, the IPO sentiment is currently in a recovery phase.

Overall, China Resources Beverage has a certain level of institutional allocation demand, with some short-term investment value for IPO subscriptions, but the expected profit margin is relatively average.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (8)

to post a comment

26

23