Meta績后暴跌!AI燒錢太猛嚇崩股價?

Futu Research | After the results, the stock price fell by more than 15%, was Meta unfairly punished?

Meta released its first-quarter financial report after the US market on April 24. The performance exceeded expectations across the board, but it fell by more than 15% after hours, echoing last week's Netflix scenario. The results were largely in line with market expectations.Futu Research | Will Meta be able to move forward against headwinds?The judgement in advance was basically consistent.

![Meta released its first-quarter financial report after the U.S. market closed on April 24th, with performance exceeding expectations across the board. However, it plunged over 15% after hours, echoing Netflix's fate last week. This is in line with the predictions in the preview.[Share Link: Futu Research | Will Meta be able to move forward against headwinds?]Next, let's analyze Meta's performance this quarter and project the subsequent stock price changes. I. How did the company perform this quarter? I. How did the company perform this quarter? 1. The advertising business continues to perform well. The majority of Meta's revenue comes from advertising business, driven by strong growth in advertising revenue, Meta's 24Q1 revenue increased significantly by 27% year-on-year to $36.46 billion, surpassing Bloomberg's consensus expectations, becoming the fastest revenue growth quarter since 21Q4. Core advertising business revenue was $35.64 billion, up 26.8% year-on-year. As we mentioned in the previous foresight, Meta's outstanding performance in Q1 is basically as expected, mainly benefiting from the following factors: (1) The strong US economy is the cornerstone supporting the growth of Meta's advertising business. In the first quarter of 2024, the US economy was very strong, with an optimistic employment environment, the US unemployment rate further decreased to 3.8% in March. At the same time, US consumer spending continued to show resilience, with a month-on-month increase of 0.7% in March retail sales, with the highest growth in e-commerce. E-commerce was the biggest driver of the company's advertising business growth this quarter, followed by the gaming and entertainment industries. With strong economic support, advertising recovery has been evident...](https://nnqimage.futunn.com/sns_client_feed/12106320/20240425/1714044951961-dd50d0a48a.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Next, let's analyze the performance of Meta this quarter and speculate on the subsequent changes in stock price.

1. How did the company perform this quarter?

1. The advertising business still performs exceptionally well.

The vast majority of Meta's revenue comes from the advertising business. Driven by strong growth in advertising revenue, Meta's revenue in 24Q1 increased significantly by 27% to $36.46 billion, exceeding Bloomberg's consensus expectations, becoming the fastest revenue growth quarter since 21Q4. Core advertising revenue was $35.64 billion, a year-on-year increase of 26.8%.

As we mentioned in the outlook earlier, Meta's outstanding performance in Q1 is basically as expected, mainly benefiting from the following factors:

(1) The strong US economy is the cornerstone supporting the growth of Meta's advertising business.

The US economy in the first quarter of 24 is very strong, with an optimistic employment environment. In March, the US unemployment rate further decreased to 3.8%. At the same time, US consumer spending remains resilient, with a month-on-month increase of 0.7% in retail sales in March, with the largest increase in e-commerce. E-commerce is the biggest driver of the company's advertising business growth this quarter, followed by the gaming and entertainment industries.

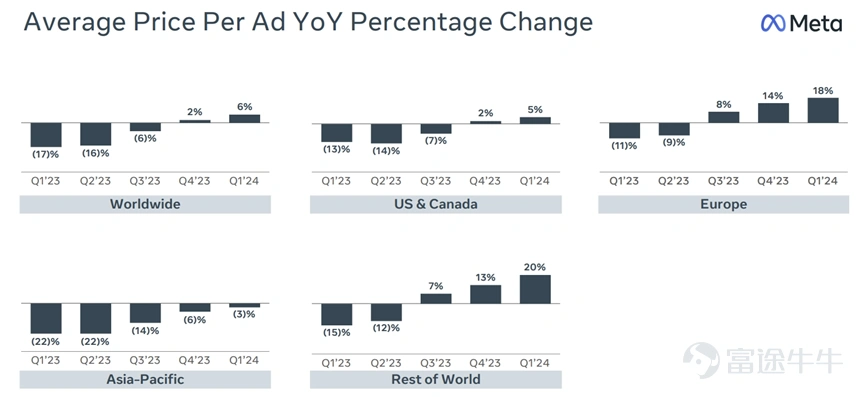

Supported by a strong economy, advertising has notably recovered. In 24Q1, the company's advertising exposure increased by 20% year-on-year, and strong demand from advertisers drove a 6% year-on-year increase in the company's advertising prices.

Chart: Changes in advertising prices

Source of information: Company's official website

(2) The strong social ecosystem advantage makes Meta the preferred choice for advertisers

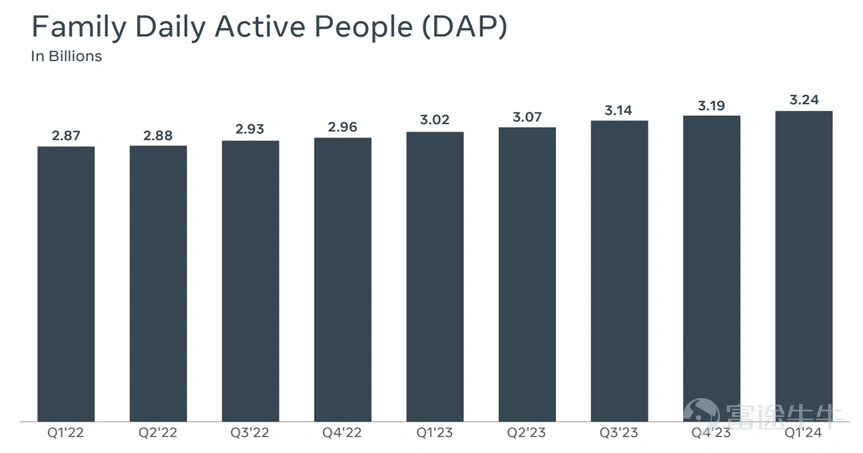

Meta owns globally renowned social software such as Facebook, Instagram, and WhatsApp, holding an almost monopolistic position in the social ecosystem. With such a large user base, the total daily active users of all social software in 24Q1 were 3.24 billion, achieving a 7% year-on-year and 1.6% month-on-month growth, demonstrating strong social ecosystem barriers. With a massive user traffic, Meta naturally becomes the first choice for many advertisers.

Chart: DAP data

Source of information: Company's official website

(3) AI applications have improved advertising ROI

Meta fully utilizes AI tools to enhance the precision of ad recommendations while maximizing the reduction of user interference, aiming to increase the monetization rate of social software (including WhatsApp, Reels, and other text and video products); the company has launched many automated empowered advertising products for advertisers, and the scalable Gen AI advertising tools significantly increase the ROI of ad placements. In addition, Meta also has a powerful open-source AI large model called 'Llama,' but it is still a long way from monetization.

2. The loss margin of the metaverse business has narrowed.

In 24Q1, the company's metaverse business revenue increased by 30% year-on-year to $0.44 billion, mainly benefiting from the growth in Quest headset sales. However, the metaverse business is still in a loss position, with an operating loss of $3.846 billion in 24Q1, a narrower loss compared to 23Q1.

Chart: Revenue by department

Source of information: Company's official website

Second, EPS doubled, so why did the stock price fall instead?

As a light asset-operating internet company, Meta's net income growth will significantly outpace revenue growth during the upturn cycle of the company.

Under the excellent cost optimization and expense control of the company, the gross margin in 24Q1 reached 81.79%, achieving significant improvements both year-on-year and quarter-on-quarter. At the same time, operating expenses only experienced a single-digit growth rate of 4.49%, mainly due to a further decline in marketing expenses compared to the previous year. As a result, the company's net income increased by 116.66% year-on-year to $12.369 billion, with diluted EPS increasing by 114.09% to $4.71 year-on-year.

Chart: EPS growth situation

Source of information: Company's official website

Why did Meta's stock price drop significantly despite the doubling of EPS growth?

1. The company's Q2 revenue guidance fell short of expectations, confirming the risk of slowing performance.

The company expects Q2 revenue to be around 36.5-39 billion U.S. dollars in 2024, with a growth rate lower than market expectations, triggering concerns about the company's future performance slowdown. While the company achieved a doubling of EPS in Q1 2024, one of the reasons was a significant year-on-year decline in EPS in Q1 2023. Meta's explosive EPS growth started in the second half of 2023, so under the effect of a high base, the performance growth rate in the second half of 2024 is likely to slow down significantly, returning to a relatively stable growth level.

As we previously mentioned in the earnings conference call preview,Meta's current valuation is not low, and only maintaining extremely high, above-expectation performance growth can support the current stock price.One,With the slowdown in performance growth and the weakening of the company's growth prospects, it will impact the company's stock price, repeating the scenario of Netflix's stock price falling after last week's earnings.

2. Increased investment in AI and the metaverse has raised concerns in the market.

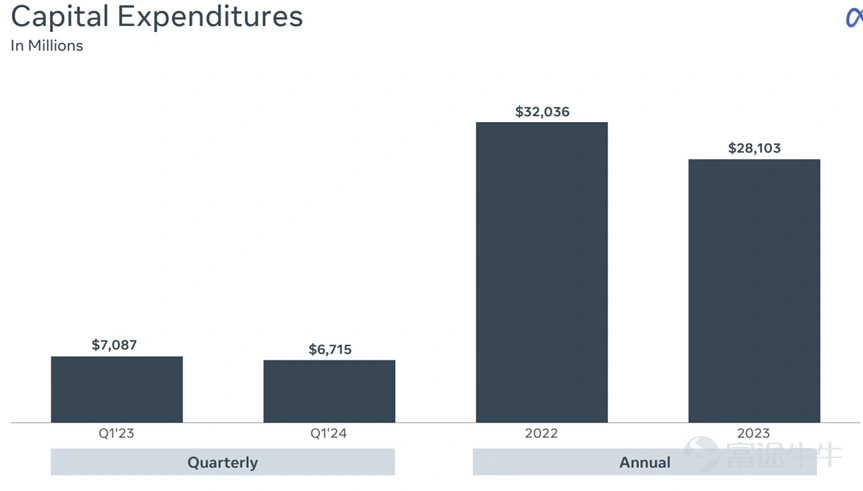

The company's management mentioned in the earnings conference call that they plan to invest more funds in AI infrastructure in the coming years. Another long-term plan is to continue investing heavily in the metaverse, with the metaverse business operating losses expected to increase significantly year-on-year.

As a result, the company has significantly increased its capital expenditure for the fiscal year 24, with total annual capital expenditure expected to increase by $40 billion, an increase of $5 billion from previous forecasts, and significantly higher than the $28.1 billion in fiscal year 23. Taking into account the growth in infrastructure investment and legal costs, the company expects total expenditures for the year 24 to be in the range of $96-99 billion, an increase of $2 billion from the lower end of the expenditure range compared to the previous forecast of $94 billion.

One of the important reasons for the significant drop in Meta's stock price in the last round was Zuckerberg's large-scale attack on the metaverse leading to excessive erosion of free cash flow. This time, Meta's announcement of a large-scale attack on AI and the metaverse makes it hard for the market not to worry about history repeating itself.For shareholders, in the current turbulent macro environment and fragile market sentiment, AI and the "big pie" of the metaverse may be hard to swallow, so it is a better choice for the company to retain more funds for shareholder returns.

Chart: Company's capital expenditure situation

Source of information: Company's official website

Therefore, we can see that once the company's valuation rises to a relatively high level, market expectations for the company's future performance growth rate will also increase accordingly. It requires very outstanding performance to sustain the stock price increase. Even if the quarterly performance remains outstanding, once the company's future growth may slow down, or other risk factors emerge, in the current fragile market sentiment, the stock price will experience a significant pullback.

3. What is the investment value of Meta in the future?

So how should we invest in Meta? It can be viewed from two aspects: EPS and shareholder returns:

1. Regarding EPS

Supported by a strong US economy and robust ecological barriers, it is expected that the company's advertising business will remain strong. However, due to the high base effect, the revenue and profit growth rates in the next three quarters are likely to slow down significantly. Therefore, it is expected that the growth rate of EPS in the 24 fiscal year will significantly decline compared to the 73% growth rate in the 23 fiscal year.

2. In terms of shareholder returns

In 24Q1, the company repurchased $14.6 billion worth of shares and spent $1.3 billion on dividends. Meta previously announced an increase of $50 billion in repurchases based on $30.9 billion, leaving a remaining repurchase amount of $66.3 billion in the future.

In 24Q1, the company's free cash flow was $12.531 billion, an 81% year-on-year increase. The free cash flow for the 23 fiscal year was $43.847 billion. Considering that the significant increase in capital spending in the 24 fiscal year partially offset the growth in operational cash flow, it is expected that the free cash flow for the 24 fiscal year will be around $50 billion.

Based on the repurchase intensity in the first quarter, it is expected that around $40-50 billion can be repurchased in the 24 fiscal year, using up most of the cash flow.With a market cap of $1.25 trillion, shareholder returns are approximately around 3.2%-4%, lower than the current risk-free rate of around 4.65%. The risk lies in the potential reduction in share buyback scale by the company in the following quarters, leading to shareholder returns lower than our expectations.

Therefore, we can adopt corresponding investment strategies based on different scenarios:

1. The EPS growth rate of fiscal year 24 fell from fiscal year 23 (73%), but still maintained a high growth rate of around 30%. The EPS growth rates for fiscal years 25 and 26 slowed to around 15%, and the free cash flow is relatively healthy, providing sustainable shareholder returns. Giving a PE (TTM) of 23-25x, the target price for the company is around $444-483. Investors can wait for a pullback in the company's stock price to bottom out before entering. They can consider selling a put with a strike price below $400 to earn the premium and reduce the purchase cost. If holding the stock and bullish on Meta in the long term but expecting short-term stagnation, they can consider a covered call strategy to earn the premium.

2. Assuming that investments in AI and the metaverse result in a significant increase in capital expenditures and cost expenses, the company's performance growth in fiscal year 24 will significantly slow down, with free cash flow being severely consumed, making shareholder returns unsustainable. In this case, the stock price will see a significant pullback. Investors can consider adopting a short-selling strategy by buying puts.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (9)

to post a comment

32

75