京東Q1業績超預期!許冉接任CEO

Quarterly Review: Behind the change of CEO of JD, there are many crises

Before commenting on the JD Quarterly Report, I recommend that you read the article we wrote earlier --It wasn't just price that made JD fallMuch of the logic and analysis is actually continued in this year's quarterly report, so I won't go into detail here.

Let's talk about opinions first:

1. For the first time, JD's two main categories, electronic appliances and Nippon 100, both showed negative year-on-year growth. This is probably because a large number of products in these two fields participated in JD's 10 billion subsidy. Judging from the current internal situation in China's e-commerce industry, the price war cannot bring any advantage to JD;

2. In the first quarter, non-GAAP net profit increased sharply by 68% to 7.9 billion yuan, up 8% month-on-month. Due to the decline in commodity revenue, the main driving force behind the sharp increase in net profit was cost reduction, and there is room for cost reduction, and the marginal effects brought about by it are already showing signs of weakening;

3. Communicate with a leading computer manufacturer. Although preparations should be made to participate, I don't have much hope for this year's “618.” Some of the more popular categories will have some reluctance to sell and insure the price. The core essence is that there are too few categories in demand; there is no way to guarantee one's own profit without doing this.

Let's look at the data again:

In the first quarter of this year, JD Group achieved positive year-on-year revenue growth, reaching 243 billion yuan, up 1.4% year on year, down 1.8% month on month; non-GAAP net profit of 7.9 billion yuan, up 68% year on year, up 8% month on month; operating cash flow was -21.61 billion yuan, an increase of nearly 58 times year on year.

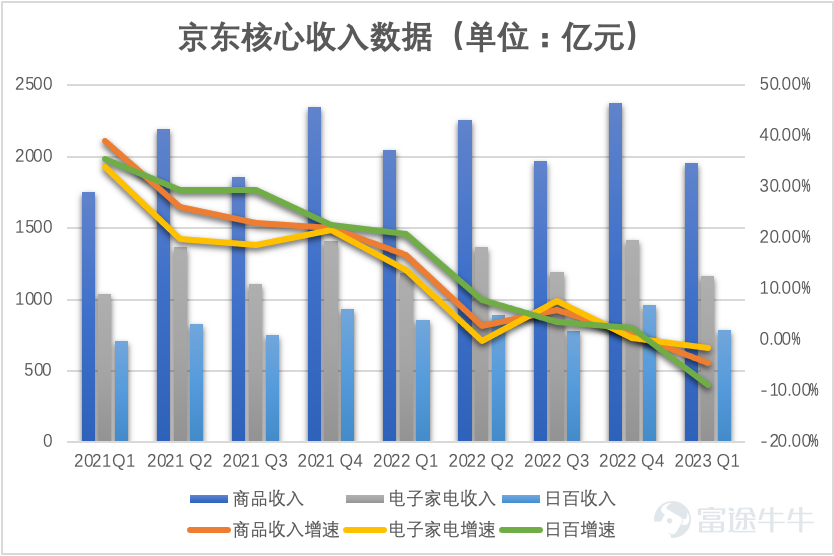

Looking at the scale of core revenue, JD achieved product revenue of 195.64 billion yuan in the first quarter of this year, down 17.7% from the previous month and 4.3% from the previous year. This is the first negative year-on-year increase in the past two years. Among them, revenue from the electronic home appliance category was 116.7 billion yuan, down 1.44% year on year, and revenue from the daily 100 category was 78.6 billion yuan, down 8.65% year on year. This is also the first time in the past two years that there has been negative growth at the same time.

![Before commenting on the JD Quarterly Report, I recommend that you read the article we wrote earlier --[Share Link: It wasn't just price that made JD fall]Much of the logic and analysis is actually continued in this year's quarterly report, so I won't go into detail here. Let's talk about opinions first: 1. For the first time, JD's two main categories, electronic appliances and Nippon 100, both showed negative year-on-year growth. This is probably because a large number of products in these two fields participated in JD's 10 billion subsidy. Judging from the current internal situation in China's e-commerce industry, the price war cannot bring any advantage to JD; 2. In the first quarter, non-GAAP net profit increased sharply by 68% to 7.9 billion yuan, up 8% month-on-month. Due to the decline in commodity revenue, the main driving force behind the sharp increase in net profit was cost reduction, and there is room for cost reduction, and the marginal effects brought about by it are already showing signs of weakening; 3. Communicate with a leading computer manufacturer. Although preparations should be made to participate, I don't have much hope for this year's “618.” Some of the more popular categories will have some reluctance to sell and insure the price. The core essence is that there are too few categories in demand; there is no way to guarantee one's own profit without doing this. Let's look at the data again: In the first quarter of this year, JD Group achieved positive year-on-year revenue growth, reaching 243 billion yuan, up 1.4% year on year, down 1.8% month on month; non-GAAP net profit of 7.9 billion yuan, up 68% year on year, up 8% month on month; operating cash flow was -21.61 billion yuan, an increase of nearly 58 times year on year. From the core...](https://nnqimage.futunn.com/12232716/editor_image/491870edb0623153a3d88b80656a1896.png/big?imageMogr2/ignore-error/1/format/webp)

The trend in this chart is actually quite obvious; JD's growth rate is in a continuous downward channel. As a comparison, according to data from the Ministry of Commerce, the country's online retail sales in the first quarter of this year were 3.29 trillion yuan, up 8.6% year on year; of these, online retail sales of physical goods were 2.78 trillion yuan, up 7.3% year on year. JD's data for the first quarter is contrary to the trend of e-commerce retail sales across the country. This is a pretty bad sign.

Arguably, soon after the first quarter of this year began, Liu Qiangdong made a big “10 billion retail” subsidy, vowing to fully regain his price advantage; however, in reality, compared with the price war that Liu Qiangdong participated in at the beginning of the boom in e-commerce, the marginal effect of the 10 billion subsidy was actually too small; it brought about a decline in revenue for JD.

As a result, the current situation is very embarrassing: the money has been spent, nothing has been wasted, and it is still necessary to continue with several companies. It is really difficult to give growth expectations for the next three quarters.

Of course, there isn't no good news either. Today, CEO Xu Lei officially retired and CFO Xu Ran took over. It is seen as a sign that Liu Qiangdong has further strengthened his control over JD. Under continuous cost reduction measures, JD still has spare time to contribute higher profits. Coupled with Liu Qiangdong's return, it still gives people a high level of confidence.

However, how long will the increase in profits brought about by the cost reduction last? Does the e-commerce market in Sangtian, Canghai still have room for Liu Qiangdong to take off with JD? These questions are all unknown. What is more certain is that this year's 618 is probably the weakest 618 in history.

I had a conversation with a friend who works as a marketer at a computer manufacturer two weeks ago, and his answer was quite sincere. The current 3C market is really difficult to do. Traditional categories are difficult to sell. Only relatively new categories such as game books and all-purpose books have incremental demand. All manufacturers are hoping for a good income from this piece. Everyone is working hard not to let the price drop, but what this has brought about is that this part of the demand is gradually being suppressed.

“There will always be an inflection point. I can't stand such a high price. It's probably Double Eleven by the end of this year,” he said. In a situation where incremental demand is difficult to find, how much room for imagination can JD bring investors after entering a negative growth channel?$JD.com (JD.US)$$JD-SW (09618.HK)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (10)

to post a comment

9

11