騰3億回來了!能否守住三萬億市值?

Tencent '930', once again?

On August 18th, 19th, and 22nd, the Hang Seng Index$Hang Seng Index (800000.HK)$Gains and losses were -0.8%, 0.05%, and -0.42% respectively, while Tencent’s were 3%, 0.77%, and -1.46%, with its market value returning near three trillion Hong Kong dollars. This indicates that after Tencent released its earnings report on the 17th, overall market sentiment has stabilized.

The earnings report shows that in the second quarter of 2022, Tencent$TENCENT (00700.HK)$Generated revenue of 134 billion yuan, a year-on-year decrease of 3%, marking its first-ever negative growth; net profit (Non-IFRS) was 28.139 billion yuan, down 17% year-on-year, with the decline narrowing for two consecutive quarters.

In the first half of this year, Tencent generated revenue of 269.505 billion yuan, a year-on-year decrease of 1%, with net profit (Non-IFRS) at 53.7 billion yuan, down 20% year-on-year.

This quarter, Tencent's value-added service business revenue declined by less than 0.5% year-on-year to 71.683 billion yuan, with games showing a negative year-on-year growth of 1%, reaching 42.5 billion yuan, but social networks growing by 1% to 29.2 billion yuan.

In corresponding terms, Alibaba's China commerce segment (calendar year) also fell by 1%, marking its first contraction since going public.

In fact, against the backdrop of macroeconomic growth pressure and the downturn in the internet industry, both companies’ core businesses contracted in the second quarter. However, it is worth noting that the declines did not exceed 1%.

The impact of short-term adverse factors cannot alter the stabilization and bottoming-out trend of these two leading internet enterprises since the beginning of the year.

At the same time, the financial report showed many positive signals. The revenue share of fintech and enterprise services further consolidated, with Channels expected to shoulder the important task of WeChat commercialization. R&D investment continued to rise while marketing expenses narrowed, achieving a higher-than-expected net profit (Non-IFRS) through cost reduction and efficiency improvement.

However, from a longer-term perspective, Tencent still needs fundamental new growth drivers to break into a new development phase.

As in the 2018 '930' transformation, Tencent not only achieved its strategic goal of expanding from C-end to B-end but also saw its stock price soar to HKD 747.1 within just over two years.

Today, Tencent's stock price has fallen nearly 60% from its peak, facing multiple difficulties in the operating environment, with several performance indicators continuing to decline. Does Tencent need another transformation?

01 Transformation is already substantially underway

Looking back at Tencent’s changes since last year, it becomes clear that transformation has been substantially underway, such as capital restructuring via dividend distribution, continuous ‘cutting losses and retaining profits’ in operations, and optimizing personnel performance evaluations.

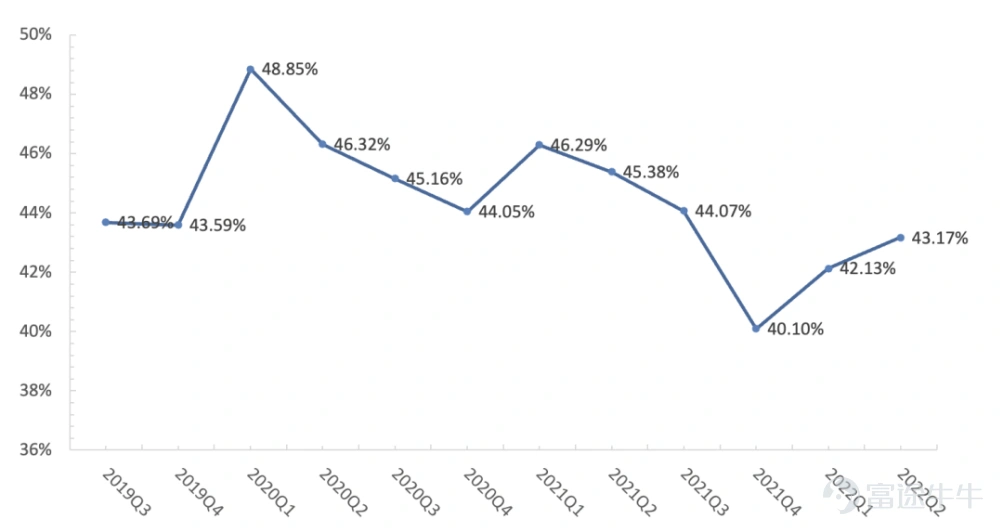

This earnings report feels more like a summary of a phase, primarily reflecting ‘cost reduction and efficiency improvement.’ Core financial metrics such as gross margin, expense spending, and net profit (Non-IFRS) all performed well.

In recent years, Tencent's gross margin has remained stable above 40%. Although revenue growth has been suppressed since Q2 of last year, optimization of content costs in the advertising business, cutting loss-making fintech and enterprise service projects, and three years of self-developed cloud migration have cumulatively saved RMB 3 billion in costs, leading to a sequential decrease in operating costs and a gross margin increase for three consecutive quarters.

Source: Company financial reports

The total amount of period expense spending also began to decrease sequentially starting last quarter. Marketing expenses dropped by 21% compared to the same period last year, with their share of revenue significantly narrowing from 11% in the previous quarter to 6%.

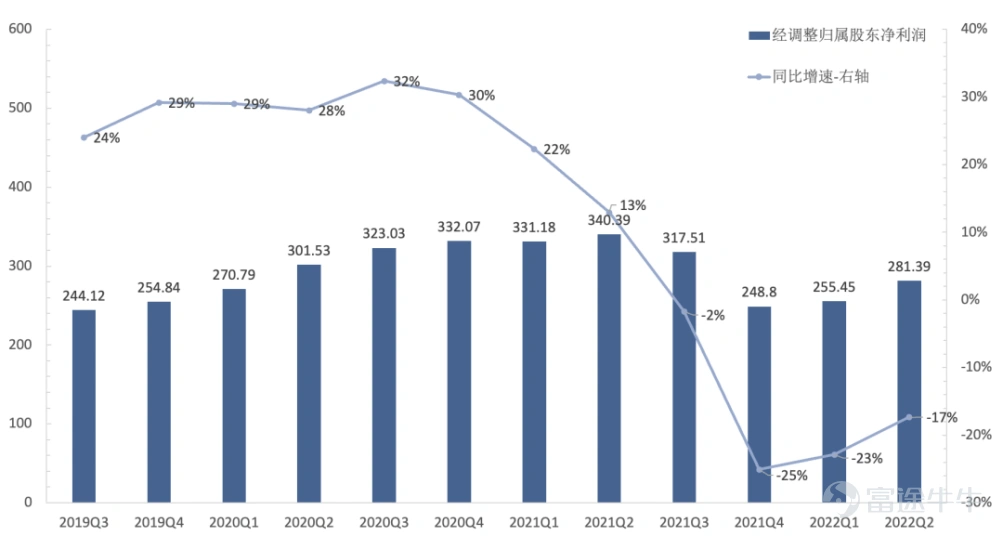

From the perspective of profit trends, net profit (Non-IFRS) bottomed out starting in Q4 2021, and as of this quarter, the year-over-year negative growth has narrowed for two consecutive quarters.。

Source: Company financial reports

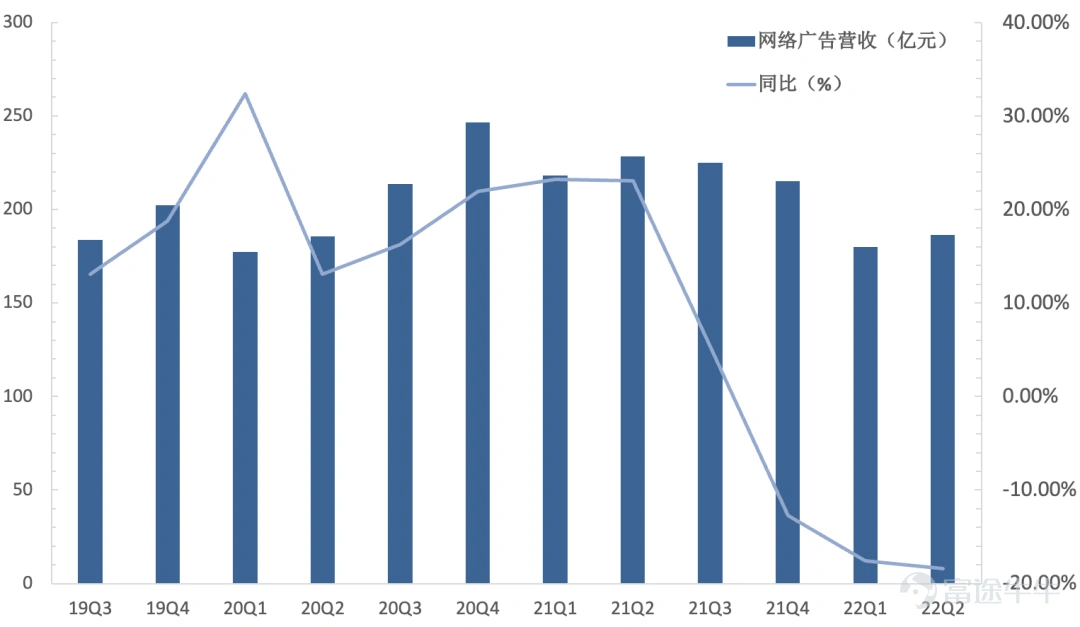

However, in terms of revenue, it is still constrained by the macroeconomic downturn, with online advertising being the most affected.

The earnings report shows that the online advertising business revenue for the quarter fell 18% year-over-year to 18.6 billion yuan, marking the third consecutive quarter of negative growth year-over-year, but saw a slight increase quarter-over-quarter.

Source: Company financial reports

This was mainly due to the impact of the pandemic on first-tier cities between April and May, leading to weak demand in traditionally strong advertising sectors such as internet services, education, and finance, causing significant headwinds for the entire internet industry’s advertising business.

In the second quarter of this year, Alibaba's customer management revenue (mainly ad revenues from Taobao and Tmall platforms) declined 10% year-over-year, further declining compared to Q1’s zero growth; Baidu’s ad revenue fell 4% year-over-year and 17% quarter-over-quarter in Q1.

However, as the pandemic subsided, the situation has improved.

According to the latest 'Overview of Advertising Market Investment Data H1 2022' released by CTR, ad spending in China’s advertising market (including online platforms) fell 11.8% year-over-year in the first half. In June, ad spending dropped 9.2% year-over-year but rose 6.9% month-over-month, continuing the recovery trend seen in May (May year-over-year/month-over-month: -24.1%/+9.5%).

The gaming business has also been impacted by the macro environment. The earnings report shows that domestic gaming revenue fell 1% year-over-year to 31.8 billion yuan this quarter, while international gaming revenue dropped 1% year-over-year to 10.7 billion yuan.

As a leader in the global gaming industry, Tencent has been deeply affected by the sluggish global economy.

A report by Ampere Analysis pointed out that after seven consecutive years of growth, the gaming market is expected to see its first decline this year; GI analysts also noted that the US gaming market has experienced year-over-year declines for seven consecutive months.

In the three months ending June, disappointing results were reported by several gaming giants, including Microsoft, Sony, and Nintendo.

According to the 'January-June 2022 China Game Industry Report,' the actual sales revenue of China's gaming market in the first half of the year was 147.789 billion yuan, a year-on-year decrease of 1.8%, with approximately 666 million gamers, reflecting a year-on-year drop of 0.13%.

In the phase of a saturated market, the claim that 'games are immune to economic recessions' no longer holds true; meanwhile, Tencent and NetEase have gone a full year without obtaining new game licenses.

Affected by this, value-added service businesses containing games experienced a slight year-on-year decline, but their revenue share still reached 53%. Notably, Video Account ads have become an 'important opportunity' for monetization within the WeChat ecosystem.

Currently, total user time spent on Video Accounts has exceeded 80% of Moments, total video views have increased more than 200% year-on-year, AI-recommended video views have grown over 400% year-on-year, and both the number of daily active creators and daily average video uploads have increased more than 100% year-on-year.

Social networking provides Tencent with its fundamental traffic base and is also one of only two business segments showing positive growth this quarter. By the end of June 2022, the combined monthly active users of WeChat and WeChat reached 1.299 billion, a year-on-year increase of 3.8% and a quarter-on-quarter rise of 0.8%, with a net quarterly increase of 11 million users.

The number of paying members for Tencent’s value-added services increased by 2% year-on-year to 235 million. The number of paying subscribers for Tencent Video reached 122 million at the end of June, while the number of paying members for Tencent Music grew year-on-year to 83 million.

Abundant traffic resources imply significant monetization potential. During the earnings call, Tencent also stated that Video Account revenues are expected to surpass Moments ad revenue in the future, though user experience will remain the top priority.

02 Optimization and transformation remain the main theme

The '930' reform in 2018 had the most critical strategic direction: 'embracing industrial internet,' strengthening TOB capabilities, and shifting away from a revenue structure dominated by consumer internet businesses.

This strategy continues to this day.

Therefore, it can be considered that the ongoing or upcoming transformation is a continuation and deepening of the previous 930 reforms rather than a rejection. Thus, optimization and transformation remain the main theme, with the pursuit of 'quality growth' being the key characteristic.

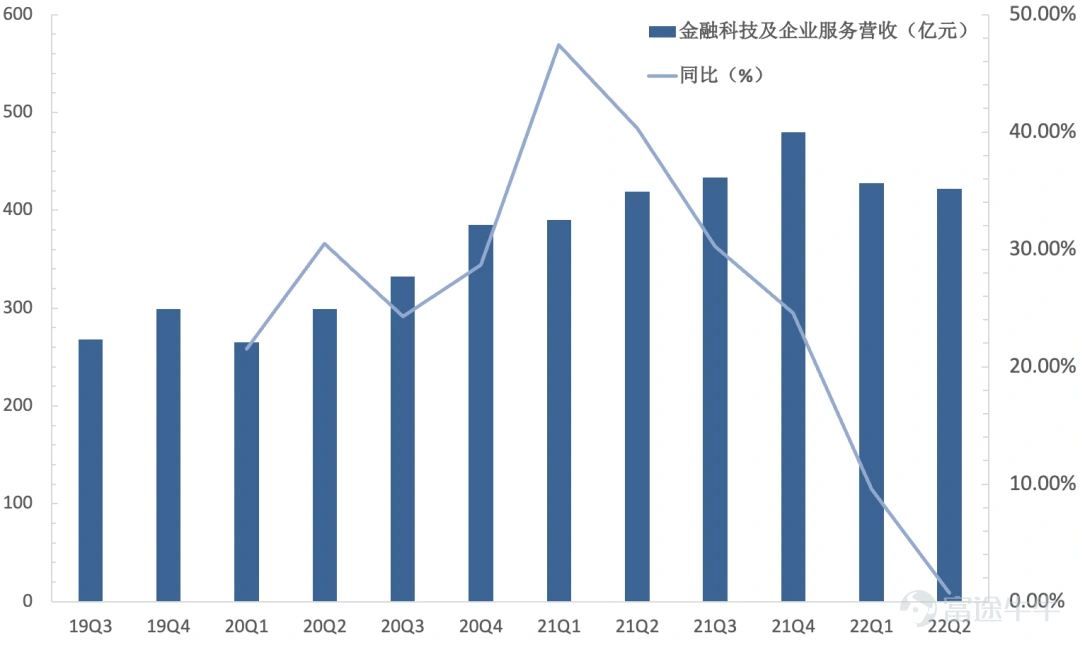

The financial report shows that the fintech and enterprise services segment generated revenue of 42.208 billion yuan, accounting for 32% of total revenue, representing a year-on-year increase of 1%. Compared to other segments, this was one of the few areas with positive growth.。

Source: Company financial reports

This indicates that Tencent's 'integration of digital and real economies' is accelerating, and its efforts to 'optimize revenue structure' are ongoing.

Source of information: Public information

This is also the guiding principle behind Tencent's 'cost reduction and efficiency improvement': decisively shutting down non-core businesses that fail to gain traction. Of course, other major internet companies such as Alibaba, Baidu, JD.com, and ByteDance have also significantly scaled back their operations.

In 2022, the entire internet industry faced the dilemma of 'traditional growth reaching its ceiling and innovation hitting roadblocks.' In good years, profitable projects could cover losses; in bad times, they had no choice but to cut them off.

For instance, Tencent's enterprise services business, which is primarily cloud-based, has seen heavy capital investment at the IaaS level since Tencent began focusing on it in 2018, significantly reducing overall gross profit and net profit margins.

Tencent Cloud operates '70 availability zones across 27 geographic regions globally, with over 1 million servers in total, forming a global distributed cloud computing infrastructure.'

However, the construction cost of a single data center can easily reach hundreds of millions, indicating the massive investment involved.

Among all IDC application scenarios, internet giants like Alibaba, Tencent, and Huawei are also among the primary players in the 'East Data West Calculation' initiative. Data shows that Chinese internet companies account for 60% of downstream applications in data centers.

For a long time, in terms of specific cloud services, Tencent Cloud has been operating at a loss to gain market share, causing the overall sector’s costs to remain high.

In the last quarter, the cost of the fintech and enterprise services segment increased by 11% year-over-year, marking two consecutive quarters where cost growth outpaced revenue. However, this quarter's year-over-year decline was only 1%, indicating that cloud projects have proactively scaled back loss-making initiatives, resulting in corresponding cost reductions.

From the perspective of business focus, Tencent will lean more towards PaaS and SaaS solutions in the future, aiming to achieve profitability sooner. Nevertheless, cloud computing also represents the externalization of mature technological capabilities within enterprises. This applies to AWS, Google, and Alibaba Cloud as well—Tencent Cloud is no exception.

The financial report shows that Tencent invested 15.01 billion yuan in R&D this quarter, representing a 17% increase year-over-year and accounting for 9% of total revenue. Since 2019, Tencent's cumulative R&D investment has exceeded 151.6 billion yuan.

Guided by the dual strategies of 'open-source collaboration' and 'self-developed cloud adoption,' Tencent has made continuous breakthroughs in cutting-edge fields such as AI, chips, operating systems, servers, edge computing, and quantum computing.

For instance, Tencent Cloud's computer vision capabilities have ranked among the global top 2, and its fourth 7-nanometer chip, 'Xuanling,' is set to undergo tape-out by the end of the year.

Tencent's R&D efforts have rapidly shifted from application-layer development to foundational infrastructure construction. Not only is it capable of supporting current operations, but there are intentions to build a technological reserve for the next industrial cycle.

A new wave of the industrial cycle is already brewing. According to IC Insights, leading international chip manufacturers’ expansions primarily focus on more advanced processes (e.g., 5nm). Meanwhile, the global rollout of 5G is accelerating, with early outlines of 6G beginning to emerge.

03 'Hardware' Will Be the Main Logic of the Cycle

All signs indicate that Tencent's previous '930' transformation achieved a leap from consumer-oriented (C-end) to business-oriented (B-end), but it remains only halfway complete. In the second half or during the next '930,' Tencent will transition from software applications to hardware terminals.

This aligns with the policy direction of hard technology innovation and also meets Tencent's practical needs as a 'digital assistant.' Hardware innovation is an essential path to breaking through the bottleneck of 'digital-real integration.'

Under this dual influence, Tencent first underwent changes in its investment strategy. Since last year, it has actively invested in several sub-sectors of hard technology, including chips, robotics, new energy, autonomous driving, smart manufacturing, and industrial internet.

Examples include photovoltaic unicorn GCL Photovoltaic Technology, battery unicorn GAC Aion, autonomous driving software developer ZeroTruck Technology, robotic process automation company Shadow Knife RPA, quantum computing firm IQM; in the chip sector, apart from Enflame Technology, there are DPU provider Cloud Leopard Intelligence, GPU company Moore Threads, switch chip provider Yunhe Smart Networks, DRAM manufacturer CXMT, and Photon Semiconductor, among others.

According to PEDATA MAX data, as of August this year, Tencent has invested in over 30 companies, with more than half being hard technology projects.

Additional data shows that between 2019 and May 18, 2022, Tencent’s investments in real economy sectors such as high-end manufacturing and automotive transportation accounted for 47% of its total investments during the same period, exceeding traditional core business-related investments by six percentage points.

Data source: IT Juzi

During the earnings call, Tencent also stated, 'From a long-term development perspective, focusing on investments in hard technology, chips, and other cutting-edge technology fields will be more valuable.'

But for Tencent, what holds more cyclical significance than investing is personally entering the field, which carries nearly the same strategic importance as 'shifting from C-end to B-end.' This issue, I believe, Ma Huateng has been contemplating.

In 2015, at the first World Internet Conference, when Ma Huateng was asked who might disrupt WeChat, he responded, 'The root cause lies in the evolution of internet information terminals.'

He believed that 'Every 20 years or so, the evolution of terminals brings significant shifts to the entire information industry and even the broader economic landscape. We’re thinking about what the next generation of information terminals might be—cars, wearable devices, or perhaps AR, VR, and other virtual reality and augmented reality technologies?'

In fact, this also determines whether Tencent can stand firm when the next cycle arrives.

Thus, over the years, around this 'terminal,' Tencent has initiated a series of technological ecosystem layouts, culminating in the establishment of the XR department this year.

Considering Ma Huateng’s earlier thoughts, these moves are by no means idle pawns; the initial intent to acquire an AR hardware manufacturer reflects its strategic aim for 'software-hardware integration.'

The core logic here is that Tencent's accumulated R&D patents over the years require hardware as a vehicle for monetization. This earnings report shows that, as of June 30, 2022, Tencent's number of authorized patents in major countries and regions worldwide exceeds 27,000, with more than 90% being invention patents.

These patented technologies are actually more worthy of monetization than Video Accounts, hold greater industrial value, and represent Tencent's new increment in the true sense, albeit with higher difficulty. However, they can complement Video Accounts, representing current profitability and future prospects, respectively.

As far as XR headsets are concerned, there are numerous application scenarios in key areas where Tencent is focusing its efforts: high-end manufacturing, traditional industries, smart cockpits, and AI healthcare.

Whether it can create a new generational leap in these fields, Tencent needs to prove itself with 'AI + hardware.' At the same time, this can address the regret of not having any foothold in physical economy products or material supply chains within the current industry ecosystem.

On the other hand, while WeChat’s position seems consolidated—whether it be ByteDance’s direct ventures like 'Duoshan' or 'Feiliao,' Xiaomi’s 'Miliao,' the fleeting 'Bullet Messenger,' or even Fetion—none have posed a substantial threat. In reality, however, danger has never been far away.

From a global competitive landscape perspective, Facebook, leveraging the natural advantage of English and acquisitions, formed the combination of Facebook + Instagram + WhatsApp + Messenger, collectively boasting over 3 billion users, making it the absolute leader in the global social domain.

Although Tencent has captured all Chinese-speaking users, it can only rank second. Whether WeChat expands globally or China opens its social market to WhatsApp domestically, a clash between the two is inevitable.

Data.ai's released data shows that Instagram and TikTok lead in terms of global downloads and consumer spending, while TikTok leads among video apps.

As of the first quarter of 2022, TikTok has nearly 1.4 billion users globally, with an expected reach of 1.8 billion by the end of this year. Therefore, ByteDance only lacks an effective transition path from 'short-video social' to 'chat social'.

Perhaps the reason ByteDance is actively laying out its metaverse strategy lies here, similar to Meta’s intention to replace mobile phones with VR.

Welshmen XR data shows that global VR shipments reached 2.33 million units in the second quarter of this year, a year-on-year increase of 31%. Lenovo and Skyworth have recently launched VR products, while new products from Pico, Meta, and Apple are on the way.

In fact, Tencent doesn’t have much time left. Of course, the direction of Tencent's hardware breakthrough could be robotics, as it represents the ultimate form of AI + hardware currently visible, and Tencent's technical level in related fields is among the world's leading.

However, the evolution of the next generation of hardware terminals still requires leadership from a GPT (General Purpose Technology). This is a key guiding technology in major technological changes, whose unconventional 'creative destruction' can enable overall social production to break free from existing paradigms.

Currently, this GPT technology is very likely to be artificial intelligence. So, will Tencent be the one to overcome the bottlenecks in large-scale commercial application and technological development of artificial intelligence? Or will it be an unknown competitor?

Perhaps this mystery will be answered in Tencent's next '930' transformation.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (6)

to post a comment

59

38