嗶哩嗶哩將自願在港交所雙重上市,如何解读?

Is Bilibili listed on the market again? What is the difference between a dual listing and a secondary listing?

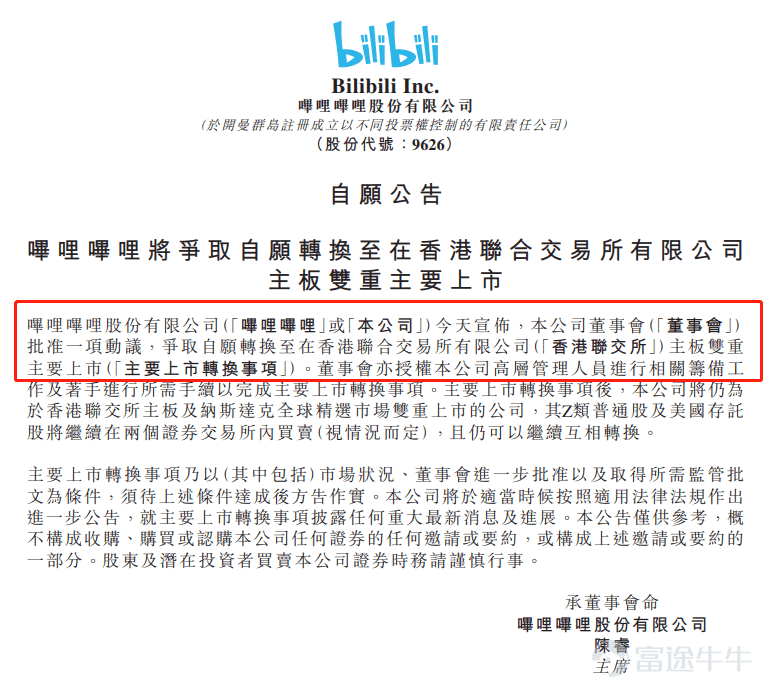

On Wednesday, according to documents from the Hong Kong Stock Exchange, Bilibili will voluntarily seek a dual listing on the Hong Kong Stock Exchange. Dual listing means that both capital markets are the first place of listing.$BILIBILI-W (09626.HK)$It is currently listed for the second time on the Hong Kong Stock Exchange.

According to the announcement, Bilibili's board of directors approved a motionSeek a voluntary transition to a dual main listing on the main board of the Stock Exchange of Hong Kong Limited.After the main listing conversion matters, the company will remain a dual listed company on the main board of the Hong Kong Stock Exchange and the Nasdaq Global Select Market. Its Class Z common stock and American depository shares will continue to be traded within the two stock exchanges (depending on the circumstances), and can still continue to convert between them.

What is dual listing? How is it different from a secondary listing?

There are different paths for Chinese securities companies to return to the Hong Kong stock market. They are mainly divided into: 1) privatization and delisting before applying for listing in Hong Kong; 2) main listing in Hong Kong (dual listing); and 3) secondary listing.

Since privatization and delisting costs are high, and re-listing after delisting faces some uncertainty, we will focus on the more mainstream dual listings and secondary listings here.

I. Comparison of basic concepts

Dual primary listing (dual primary listing) means that both capital markets are the first place of listing. When it is already listed in the US market, it is issued and listed in the Hong Kong market according to local market rules. The rules it must abide by are exactly the same as the requirements for companies that have initially publicly issued shares in Hong Kong. Stocks in the two markets cannot circulate across markets, and stock price performance is relatively independent, which may cause price differences.

$BEONE MEDICINES (06160.HK)$It has been listed on multiple occasions. In February 2016, the company was listed on the US Nasdaq and raised US$182 million; on July 29, 2018, it was dual-listed in Hong Kong and issued a total of 65.6 million common shares, accounting for 8.55% of the expanded share capital, and finally raised US$902 million.

Secondary listing (secondary listing) means that a company lists the same type of stock in both places and realizes cross-market circulation of shares through international custodian banks and securities brokers. This method mainly exists in the form of depository receipts (DR for short).

Under this distribution method, banks first buy a certain amount of shares of foreign companies and keep all of these stocks in banks, then the banks package these stocks and sell securities representing this basket of stocks. In the US, these securities are called ADR.

If the company is listed for the second time through a financing type DR, the source of the underlying shares is the company's newly issued common stock. In terms of pricing, the corresponding DR is converted using the company's market price in the original market as the reference price on the day of pricing, and a price is determined by the issuer after agreement with the underwriter. This is also the secondary listing method chosen by most Chinese securities such as Alibaba, Baidu, and NetEase to return to Hong Kong.

II. Comparison of distribution policies

1. Dual listing

Compared to a secondary listing, a dual listing needs to simultaneously meet the various management requirements of the two places for listed companies, and the overall requirements will be much stricter. If a company chooses to do a dual major listing in Hong Kong, the rules it must abide by are no different from the requirements for companies that initially publicly issue shares in Hong Kong. It must comply with all relevant “Listing Rules” of the Hong Kong Stock Exchange. The newly revised “Listing Rules” in 2018 make detailed regulations on the listing of Greater Chinese and overseas companies in Hong Kong.

2. Secondary listing

If a company is only listed for a second time in Hong Kong, the Stock Exchange expects that the company's securities will mainly be traded on overseas exchanges and be supervised by the supervisory authority of the main place of listing. Therefore, for applicants seeking a second listing, the Stock Exchange will adopt relatively relaxed review standards, and there are many exemptions and preferential policies.

Secondary listing requirements for listed companies to remain in placeVIE structureAlso, different voting rights structures need to meet certain requirements (listed sector, listing time and market capitalization size), etc., and at the same time provide methodological guidelines for companies that are eligible and want to return to the Chinese market for financing. The details are:

1) Must be listed on an eligible listed exchange (NYSE, NASDAQ, or London Stock Exchange main market) and maintain a good compliance record for at least two full fiscal years;

2) The market value at the time of listing was at least HK$40 billion, or at least HK$10 billion at the time of listing, and revenue of at least HK$1 billion in the most recent audited fiscal year.

III. Liquidity comparison

1. Dual listing:It refers to the phenomenon where the same company is listed separately on two different stock exchanges for financing. The typical double listing phenomenon in China is “A+H” listing.Dual listed stocks cannot circulate across markets. However, according to Xiaopeng Motor's previous announcement, some of its shares listed for the second time using depository certificates are allowed to achieve cross-market circulation after cancellation of depository certificates.

This time, the Bilibili announcement also stated that after the main listing conversion matters, the company will remain a dual listed company on the main board of the Hong Kong Stock Exchange and the Nasdaq Global Select Market. Its Class Z common stock and American depository shares will continue to be traded within the two stock exchanges (depending on the situation), and can still continue to be converted to each other.

2. Secondary listing:The full convertibility of ADR (American Depositary Receipts) issued by China Securities and Hong Kong stocks makes the prices of secondary listed stocks in the Hong Kong market closely linked to the US market. Since the shares of the two places are completely exchangeable, and the Hong Kong dollar is linked to the US dollar, the price difference between the two places can basically be ignored after ignoring some taxes and fees and friction between transaction time and cost.

IV. Discussion of advantages and disadvantages

1. Dual listing

The advantage is that it fully meets the regulatory requirements of the two places, is not much different from local listings, is more easily accepted by international investors, and is also easier to comply with A-share market regulation and integration into Hong Kong Stock Connect and lay the foundation for a return to the A-share market for three subsequent listings.

For example, BeiGene was officially included in the Hong Kong Stock Exchange on September 4, 2020, and after a double listing in the US and Hong Kong, it then took steps back to A-shares. On January 29, 2021, the Shanghai Stock Exchange officially accepted the BeiGene Science and Technology Innovation Board listing application. BeiGene plans to raise 20 billion yuan, sponsored by CICC and Goldman Sachs Gaohua. If it successfully lands on the Science and Technology Innovation Board this time, it will become the first innovative pharmaceutical company to be listed in three countries (US stock, H share, and A share).

From the company's perspective, the dual listing has expanded its shareholder base and increased its influence in the global market, thus enabling the company to finance in other securities markets and further expand its business to other markets.

The disadvantage is that it is necessary to meet the regulatory requirements of both places at the same time, the listing process is more complicated, and it takes more time and money.

2. Listed on both sides

The advantage is that the regulatory requirements to be met are relatively simple. Compared with dual listings, there are more exemptions from preferential terms, and the cost of listing is lower.

The disadvantages are: the pricing is basically the same as the original market, and if the price of the original market fluctuates and falls out of the pricing range at the time of subscription, the risk of a new breakout is higher; another disadvantage is that it is more difficult to be included in the Hong Kong Stock Exchange in the future (the mainland has reached an agreement with the Hong Kong Stock Exchange. The content of the agreement includes excluding companies with a second listing and weighted voting rights from the list of Shanghai and Shenzhen-Hong Kong Stock Exchange, unless the Shanghai Stock Exchange, Shenzhen Stock Exchange, and Hong Kong Stock Exchange revise the agreement).

This issue of knowledge cards

Dual listing and secondary listing: there is a big difference between regulation and cross-border circulation

Concept analysis of dual listing and secondary listing:

Dual listing refers to the phenomenon where the same company is listed separately on two different stock exchanges for financing. The typical double listing phenomenon in China is an “A+H” listing.

Secondary listing means that a company lists the same type of stock in both places. Through international custodian banks and securities brokers, shares can be distributed across markets. The secondary listing method mainly exists in the form of depository certificates.

The biggest difference between the two is:

(1) Regulatory aspects: Dual listed companies are required to fully comply with the regulations of the two exchanges, and second-listed companies are exempt from some rules.

(2) In terms of cross-market circulation: Dual listed stocks cannot circulate across markets. Some stocks listed for the second time using a depository certificate are allowed to achieve cross-market circulation after cancellation of the depository certificate.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (12)

to post a comment

37

99