Strong rebound in March non-farm payroll! Will there still be a rate cut this year?

Global Weekly Review | US nonfarm payroll data unexpectedly plunged, triggering broad declines across global stock markets

On the macroeconomic front

United States: Non-farm payroll data unexpectedly plummeted, strong service sector but economic momentum diverges

Last week, the US focused on non-farm payrolls, services, retail, and inflation-related data.The unexpected sharp decline in February's non-farm payrolls emerged as the key highlight, with overall economic momentum showing clear divergence.In terms of the labor market, February's non-farm payrolls unexpectedly dropped by 92,000, far below market expectations for an increase of 59,000. The unemployment rate rose to 4.4% month-over-month, while the Labor Department revised down data for December 2025 and January 2026, with a combined reduction of 69,000 jobs, highlighting underlying concerns in the labor market.The main reasons for this decline in non-farm payrolls were strikes by healthcare workers in New York and California, severe weather impacts, and job cuts at the industry level.Notably, federal government employment has fallen by a cumulative 11% since its peak in October 2024. However, there are positive signals in the labor market: ADP reported an addition of 63,000 jobs (the largest increase since July of last year), and corporate layoffs fell sharply in February, stabilizing overall. The service sector showed strength, with the February ISM Services Index rising to 56.1.This is the highest level since mid-2022, with significant increases in new orders and backlogs indexes, improved export demand, and easing inflationary pressures in the services sector contrasting with rising input costs in manufacturing.On the retail front, January retail sales fell 0.2% month-over-month (the first drop since October last year), impacted by sluggish auto sales and weather disruptions. However, core control group sales grew month-over-month, indicating residual consumer momentum. A tax refund boost is expected to lift consumption in the first half of the year.

China: February PMI was weighed down by seasonal factors, with manufacturing continuing to contract and non-manufacturing seeing slight improvement.

China’s key data point for February was the PMI series, which showed diverging sentiment due to seasonal factors such as the extended Lunar New Year holiday. The long-term stabilization foundation remains intact.The manufacturing PMI fell to 49.0%, contracting for the second consecutive month, with all five sub-indexes in contraction territory.The main drag was the production index, with declines in new orders and new export orders reflecting tightening demand. Large enterprises’ PMI rebounded against the trend, while small and medium-sized enterprises continued to show weak sentiment. Industrial goods prices maintained their upward momentum. The non-manufacturing business activity index rose slightly by 0.1 percentage points to 49.5%, showing a modest improvement in sentiment.The service sector was boosted by the Spring Festival holiday effect, with high business confidence in consumption-related industries such as accommodation and catering, while the construction sector saw a decline in confidence due to the holiday.The composite PMI output index fell to 49.5%, indicating an overall slowdown in corporate production and business activities. A seasonal rebound in manufacturing PMI is expected in March.

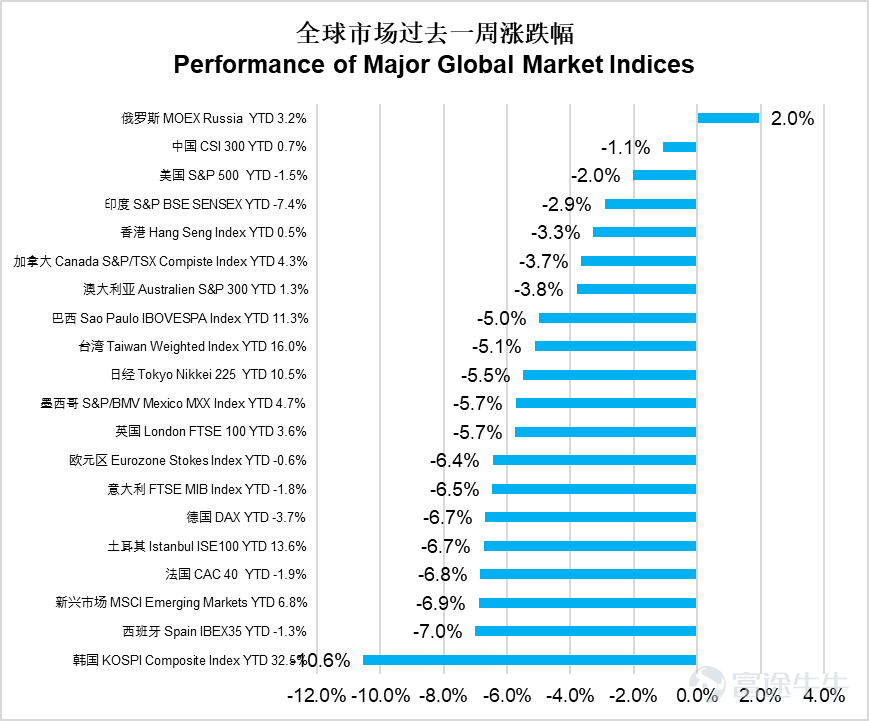

In terms of the equity market

Last week, global markets generally plummeted, driven primarily by escalating geopolitical conflicts.The outbreak of the US-Iran war resulted in the assassination of Iran's Supreme Leader, with the conflict spreading across the entire Middle East region. The blockade of the Strait of Hormuz triggered fears of an energy crisis after Iran declared full control over this crucial global oil passage. Brent crude oil surged past $85 per barrel at one point, and numerous flights to the Middle East were canceled worldwide.The South Korean Composite Index plunged 10.6%, leading global declines.Spain’s IBEX 35 fell 7.0%, while France’s CAC 40 dropped 6.8%. Emerging markets as a whole declined 6.9%, with the Hang Seng Index falling 3.3% and the CSI 300 dropping 1.1%. Russia’s MOEX rose 2.0% against the trend, becoming the only major market to close higher.The US S&P 500 fell 2.0%, a relatively moderate decline.

The US energy sector bucked the trend by rising 1.0%, becoming the only sector to post gains.The information technology sector fell 0.4%, the smallest decline. However, the materials sector plummeted 7.2%, consumer staples dropped 4.9%, healthcare fell 4.6%, and industrials declined 4.1%. Communication services and utilities both fell 2.1%, while real estate dropped 2.3%. The financial sector slid 1.8%, and consumer discretionary fell 1.4%.Renewed inflation expectations have sparked concerns about monetary policy, with markets expecting that the Federal Reserve may delay interest rate cuts. The yield on the 10-year US Treasury bond continued to rise.

The energy sector in Hong Kong stocks rose against the trend by 3.7%, showing outstanding performance, utilities increased by 0.5%, and telecommunications edged up by 0.1%.However, raw materials plummeted by 7.8%, non-essential consumption fell by 5.8%, and diversified enterprises dropped by 4.6%. Both finance and healthcare declined by 4.4%, while real estate and construction fell by 4.1%. The Hang Seng Tech Index fell by 3.7%, information technology decreased by 2.1%, and industrials fell by 3.0%. Essential consumption declined by 2.3%.The market showed a pattern of energy rising alone while most sectors fell.

In the bond market,

Global bond markets slightly retreated overall in the past week,The global composite index fell by 1.75%, the US composite index fell by 0.96%, US investment-grade corporate bonds fell by 0.95%, and US high-yield corporate bonds fell by 0.44%. The emerging market USD bond composite index fell by 1.09%, and the China credit bond index in USD fell by 0.68%.

In terms of interest rates, US Treasury yields rose overall,The 2-year US Treasury yield rose by 19 basis points from last week to 3.56%, and the 10-year US Treasury yield rose by 20 basis points to 4.14%.

Market Outlook

– Uncertainty from Middle Eastern geopolitical conflicts impacts the globe; crude oil supply may be disrupted

Middle Eastern geopolitical conflicts have become the core focus of the market. As the conflict continues, its uncertainty will keep affecting global financial markets.As of the latest close, oil prices have broken through 90 USD. With the theoretical shutdown of the Strait of Hormuz, subsequent oil prices are expected to remain more likely to rise than fall. Betting sites predict that oil prices will exceed 100 USD by the end of March. The current oil price reflects a baseline scenario where the intensity of conflict remains at the present level, with the Persian Gulf and other major oil-producing countries unaffected, keeping oil prices oscillating within the range of 85 to 95 USD.However, if the conflict escalates further, affecting the production and transportation of other major oil-producing countries, crude oil supplies are expected to experience substantial disruptions.Oil prices will exceed 100 USD.The market is already concerned about the impact of high oil prices on US inflation.US Treasury yields surged significantly this week. The Federal Reserve will face a dilemma: on the one hand, recent employment data was significantly below expectations due to the impact of AI, one-off extreme weather, and strikes; on the other hand, prolonged high oil prices will severely affect US inflation.The market has already adjusted its expectation for interest rate cuts by the Federal Reserve this year from 2-3 times previously to 1-2 times. If oil prices continue to rise, this rate cut expectation may be further lowered.Historically, in US midterm election years, the US stock market generally experiences large-scale pullbacks, especially in the second quarter of the year. Investors need to prepare for an increasingly volatile market.

Key economic data and events this week

On Monday, China will release February's CPI and PPI data as well as January-February aggregate financing data.

On Tuesday, China will announce January-February import and export data.

On Wednesday, the US will release February's CPI data.

The US will release January durable goods orders data, the revised Q4 real GDP, and the January PCE price index on Friday.

All rights reserved © 2026. E Fund Management (Hong Kong) Co., Limited.The issuer of this report is E Fund Asset Management (Hong Kong) Co., Ltd. This report does not constitute an invitation or recommendation to invest in fund units. Fund unit subscriptions can only be made using application forms accompanied by the fund prospectus. Investment involves risks; fund prices may go up or down, and past performance is not indicative of future results. Before investing, investors should carefully read the investment risks related to the fund in the fund prospectus (including the 'Risk Factors' section). This report may only be distributed within certain jurisdictions. In any jurisdiction where distribution of such information or making any invitation or recommendation is prohibited, or if distributing this report or making an invitation or recommendation to any person constitutes a violation of the law, this report does not constitute such distribution or invitation or recommendation. This document is exempt from prior review and approval by the Hong Kong Securities and Futures Commission (SFC) and has not been reviewed by the SFC. SFC recognition does not imply a recommendation or endorsement of the scheme, nor does it guarantee the commercial merits or performance of the scheme, nor does it represent that the scheme is suitable for all investors, or endorse its suitability for any individual investor or class of investors.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1