Major Governance Overhaul! Is It Time to Invest in PDD Holdings?

PDD Holdings: Stockpiling Resources, Biding Its Time to Dominate

Author | Ding Mao

Editor |Zhang Fan

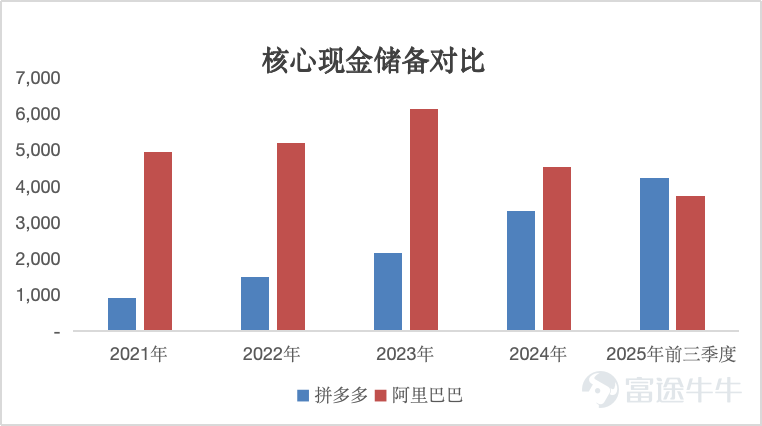

In the Q3 2025 earnings report, PDD Holdings' core cash reserves soared to 423.8 billion yuan, officially surpassing Alibaba to become the 'cash king' of China's internet industry.

Chart: Comparison of Core Cash Reserves between Alibaba and PDD Holdings Data Source: Wind, 36Kr compilation

Market opinions on this massive sum are mixed. Some call it 'strategic redundancy' for weathering tough times, while others criticize it as 'resource wastage' due to inefficiency.

As internet giants scramble to capitalize on AI, fiercely compete in instant delivery, and even woo capital markets with large-scale buybacks and dividends, PDD Holdings stands out as a 'financial ascetic,' stubbornly piling cash into its vault.

So, where does PDD Holdings’ enormous cash reserve come from? And what strategic ambitions does it conceal?

01. Full Asset 'Monetization'

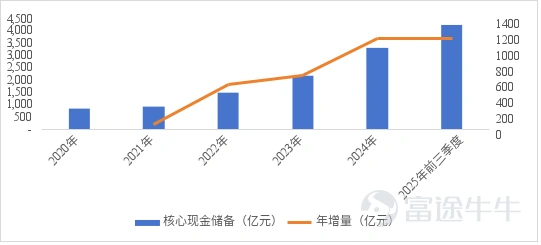

Since crossing the breakeven point in 2021, PDD Holdings' cash reserves have shown a trend of rapid expansion.

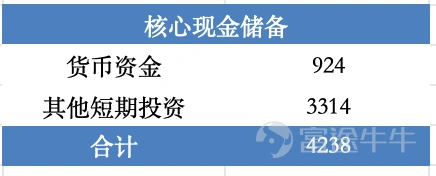

As of Q3 2025, PDD Holdings' core cash reserves reached 423.8 billion yuan, accounting for 69% of total assets, surging by 115.4 billion yuan year-over-year and increasing by 92.2 billion yuan compared to the end of 2024. Of this, cash funds amounted to 92.4 billion yuan, and other short-term investments totaled 331.4 billion yuan.

Chart: PDD Holdings Core Cash Reserves Data Source: Wind, 36Kr compilation

Chart: Trend of PDD Holdings' core cash reserve changes Data source: Wind, 36Kr compilation

If we examine PDD Holdings’ 'cash pool' from multiple perspectives, the data is even more astonishing:

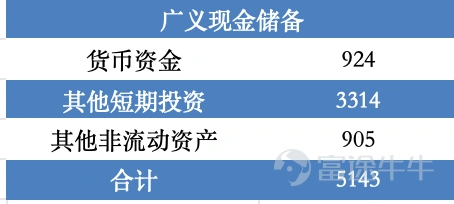

When considering long-term potential funds such as time deposits, held-to-maturity investments, and available-for-sale financial assets placed under 'other non-current assets,' the company's broad cash reserves have approached 520 billion yuan, accounting for nearly 84% of total assets.

Chart: PDD Holdings' broad cash reserves Data source: Wind, 36Kr compilation

If restricted cash is further included, then from a broader perspective, the scale of PDD Holdings' cash-like assets approaches 600 billion yuan, accounting for over 96% of total assets.

Chart: PDD Holdings' broad cash-like assets Data source: Wind, 36Kr compilation

This means that PDD Holdings' balance sheet has almost been 'fully monetized.' The extremely high liquidity ratio makes it resemble a 'money market fund' with transparent assets, massive scale, and strong liquidity.

Moreover, when viewed from the more stable net cash dimension, PDD Holdings has very low financial leverage. In Q3 2025, the company had only about 5 billion yuan in short-term debt. After deduction, its net cash exceeded 380 billion yuan. In comparison, Alibaba, also known as a 'cash-generating machine,' had cash reserves of 373.6 billion yuan during the same period, which is also at an extremely high level. However, after deducting 281.6 billion yuan of long- and short-term debt, its net cash was only around 92 billion yuan.

From the perspective of financial stability, PDD Holdings, without foreign debt pressure, clearly possesses near-optimal cash quality and risk resistance.

02. Continuous Hematopoiesis and Ultimate Preservation

So, how did PDD Holdings accumulate this massive cash reserve on its balance sheet?

In terms of funding sources, companies typically derive their resources from four channels: shareholders (original capital), creditors (interest-bearing leverage), supply chain (interest-free liabilities), and retained earnings (internal cash generation).

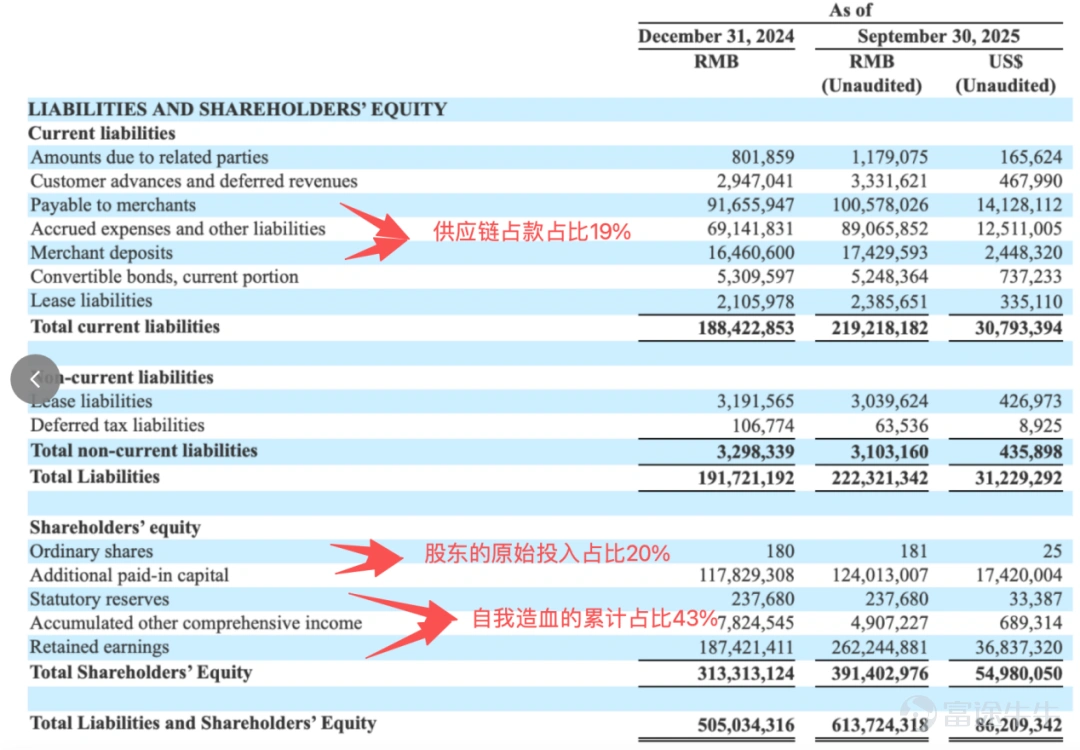

By analyzing PDD Holdings’ Q3 2025 balance sheet, its operating resources present a 'tripod' structure:

(1) During the reporting period, the company’s share premium was approximately RMB 124 billion, accounting for 20% of net assets, reflecting the initial momentum injected by the capital markets.

(2) In the same period, the combined total of the company’s merchant payables and merchant deposits amounted to around RMB 118 billion, representing 19% of net assets. This is an interest-free leverage created through timing differences in payments and economies of scale, leveraging PDD Holdings’ industry influence.

(3) The company’s retained earnings were approximately RMB 262.4 billion, accounting for 43% of net assets. This represents the cumulative net profit driven by the company’s high profitability, making it the healthiest source of resources.

Image: Breakdown of Pinduoduo's Resource Sources Data Source: Company Financial Reports, Organized by 36Kr

It is evident that the continuous accumulation of past profits has become PDD Holdings’ core source of funding. This robust self-sustaining capability stems from PDD Holdings’ exceptionally high profitability and cash conversion efficiency.

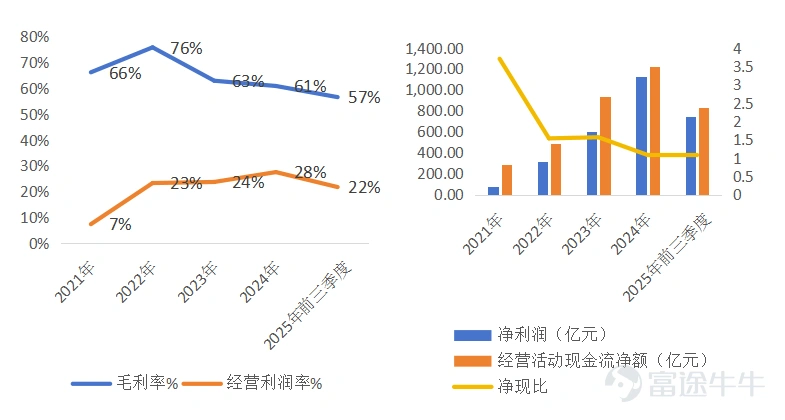

Over the past five years, PDD Holdings’ gross margin has remained stable at around 60%. Since achieving independent profitability in 2021, with the release of economies of scale, its operating margin has consistently been above 20%. Meanwhile, from 2021 to now, PDD Holdings’ net cash ratio has remained consistently greater than 1, meaning all profits have been converted into cash, indicating extremely high cash content in earnings.

Figure: Comparison of Pinduoduo's Gross Margin and Operating Profit Margin Data Source: Wind, compiled by 36Kr

Not only that, but while generating extremely strong inflows, PDD Holdings has maintained an ultra-lean expenditure structure.

On one hand, as a platform company operating on a brokerage model, its asset base is extremely light—it has no inventory overhang and requires no heavy investment in fixed assets, thus it faces almost no depreciation costs or impairment losses. On the other hand, while competitors frequently expand into unrelated fields, PDD Holdings has remained focused on its core e-commerce business, avoiding massive capital expenditures. Moreover, as a giant still in its growth phase, the company adheres to a long-term strategy of not issuing dividends, not engaging in share buybacks, and rarely taking on external debt.

This combination of 'high profitability, high cash conversion, low expenses, and low distribution' has ultimately resulted in vast resources accumulating on the balance sheet as a cash stronghold.

More notably, the 'cash pool' exceeding 500 billion yuan itself generates secondary cash flow through interest income. Based on conservative yield estimates, this translates to annual interest income of 15-20 billion yuan. This not only further boosts PDD Holdings’ net profit but also provides internal funding for the continuous expansion of the company’s operations.

03. The Costly 'Strategic Option'

So why does PDD Holdings hold such a massive cash reserve?

First, the enormous cash reserves serve as the 'ballast' to solidify PDD Holdings’ domestic foundation.

E-commerce, at its core, serves as the 'venue' connecting 'people' with 'goods,' with its primary value lying in reducing costs and improving efficiency to deliver consumers more options, faster delivery, better quality, and savings. PDD Holdings’ advantage lies in 'savings,' but this isn’t just about low prices. Instead, it embeds digital tools into suppliers’ production processes, leveraging big data to help merchants develop market-responsive products, thereby achieving efficient matching between 'people' and 'goods.'

However, as China’s internet红利 (internet user growth) reaches its ceiling, the moat protecting the e-commerce industry is far less secure than imagined. The resurgence of price wars within the year again demonstrates that industry dynamics can shift at any moment due to saturation attacks by competitors. In this context, a large cash reserve gives PDD Holdings the confidence to stabilize its core business and withstand extreme competition.

Second, it serves as the capital source for PDD Holdings to explore new growth opportunities.

The slowdown in the e-commerce industry's growth rate in recent years has forced giants to seek new growth areas; PDD Holdings has set its sights on cross-border e-commerce.

Relying on China’s robust supply chain advantages, Temu has initiated a 'lightning-fast' global expansion with ultra cost-effectiveness, achieving a scale close to its domestic main platform in just three years. However, global expansion is no easy feat and requires substantial financial backing to maintain strategic resilience in customer acquisition subsidies and global infrastructure development.

More importantly, amidst the normalization of trade fluctuations, strong financial resources provide Temu with a 'buffer' to handle global regulatory volatility and tariff risks, ensuring that its supply chain and business operations remain resilient even when sudden changes in overseas policies cause costs to surge.

Finally, it lays the foundation for PDD Holdings to reconstruct its moat and achieve an 'industrial leap.'

If PDD Holdings' early expansion was based on relatively lower traffic costs driven by social裂变 effects, then as the marginal benefits diminish, PDD Holdings' growth engine has shifted from 'traffic leverage' to 'industry leverage.' The integration and upgrading of the supply chain, along with digital empowerment, are the key factors determining success in this competition. Unlike traditional giants' asset-heavy models, PDD Holdings chooses to transform heavy investments into a sharp tool for digital R&D, deeply reforming traditional supply chains.

This 'light investment' approach to 'heavy asset' segments essentially uses strong financial redundancy to hedge against the risks of technological change, ensuring the company can patiently refine underlying efficiencies, pushing the competitive boundary from traffic distribution to production efficiency, and enabling a smooth transition from 'scale-driven' to 'value-driven' as the industry enters a phase of存量competition.

In summary, although PDD Holdings' massive cash reserves have raised some market concerns about capital efficiency, fundamentally, this large sum resembles an expensive 'strategic option,' sacrificing short-term capital returns for strategic initiative in the face of future global regulatory fluctuations, intensifying domestic competition, and technological changes. This gives PDD Holdings the most certain chips in an uncertain era.

*Disclaimer:

The content of this article represents the author’s perspective.

The market carries risks, and investment requires caution. Under no circumstances does the information or opinions expressed in this article constitute investment advice to any person. Before making an investment decision, investors should consult professionals and make prudent decisions if necessary. We do not intend to provide underwriting services or any other services that require specific qualifications or licenses to either party in a transaction.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

2