The Courier Industry After the Price War: More Intense Competition, Stronger Performance

Two years of intense price wars in the industry, compounded by recurring COVID-19 outbreaks, have been a severe challenge for express delivery companies. Now, however, these companies are finally on the verge of emerging from the crisis.

The easing of the price war began in April last year, when the Yiwu Postal Administration ordered the suspension of operations at certain distribution centers in Yiwu for Best Express and J&T Express due to predatory pricing. Since then, a series of policy measures have been introduced, leading to a gradual rebound in per-parcel rates across the industry and a return to healthy competition.

The easing of the pandemic has spurred a recovery in the industry. According to data from the State Post Bureau, in May 2022, China's express delivery companies handled a total of 9.24 billion parcels, a month-on-month increase of 23.5%.

"Rising to the top" signifies a reduction in pressure, but it also marks a quiet shift in the industry's competitive dynamics. Companies are now shifting their focus to strengthening internal capabilities and pursuing external mergers and acquisitions, rather than simply chasing growth in scale. This sector, though largely out of the spotlight, is nonetheless of paramount importance—and it is entering a new, even more intense phase of competition.

Profit Recovery: A Long and Arduous Journey

"Price wars" were once the primary source of pressure on the industry: profit margins at last-mile delivery outlets were squeezed, frontline delivery personnel saw their incomes decline, and companies as a whole faced mounting profit pressures.

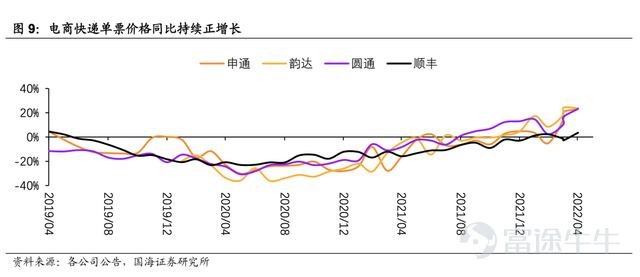

A turning point came last September: the Regulations of Zhejiang Province on Promoting the Express Delivery Industry were reviewed and adopted, prompting domestic express delivery companies to collectively announce increases in delivery fees; at the end of the month, ZTO Express, Yunda Express, J&T Express, and other carriers successively issued the "Notice on Standardizing Service Prices in the Express Delivery Market," effectively "correcting" the price-driven approach.

Since then, the year-on-year change in per-parcel prices in the industry has shifted from negative to positive. So far this year, express delivery companies have seen improvements in both their operational metrics and financial performance.

On one hand, overall parcel volumes at delivery firms have increased. According to data from Zheshang Securities, total domestic parcel volume for January–May reached 40.953 billion pieces, up 3.28% year on year. Meanwhile, according to Guohai Securities, with the exception of SF Express—whose revenue per parcel declined by 0.05% year on year from January to May—the revenue per parcel at other major delivery companies has been rising. Among them, Yunda, Shentong, and Yuantong have seen relatively stronger recovery, with their revenue per parcel increasing by more than 10% year on year in the first five months of 2022.

Growth in service prices and parcel volumes directly impacts the first-quarter performance and profitability of express delivery companies. According to the latest financial reports from these firms, Yunda, Yuantong, and Shentong all posted year-on-year revenue growth of more than 30% in the first quarter, while ZTO Express recorded a 22.1% increase in revenue over the same period.

The growth rate of gross profit for express delivery companies is even more pronounced: ZTO Express and Yunda Express both saw their gross profits increase by nearly 50% year on year; SF Express and STO Express both recorded year-on-year growth in gross profit of over 150%; YTO Express's year-on-year growth in gross profit exceeded 100%; JD Logistics also saw a recovery in performance in the first quarter of this year, with revenue reaching RMB 27.351 billion, up 22% year on year, and gross profit increasing by 533.48% year on year.

From May to June this year, express delivery companies continued to see growth in both revenue per parcel and total parcel volume.

According to statistics from Guohai Securities, in May, Yunda, Yuantong, and Shentong Express all posted year-on-year growth of more than 23% in revenue per parcel; SF Express, by contrast, saw a year-on-year increase of 3.55% in revenue per parcel. In terms of volume, Shentong and Yuantong Express both recorded year-on-year growth of over 5% in May, while SF Express posted a 4.4% year-on-year rise in parcel volume during the same period; only Yunda Shares experienced a year-on-year decline of 7.88% in parcel volume, attributable to the impact of the Beijing outbreak.

Driven by the waning impact of the pandemic and the boost from the 618 shopping festival, China's postal and express delivery sector handled approximately 940 million parcels collected during the Dragon Boat Festival holiday, a 17% increase compared with the same period last year. Meanwhile, about 970 million parcels were delivered, up 13.1% year on year.

With the dual pressures easing, express delivery companies have finally weathered the storm—but that doesn't mean they've entered a comfort zone.

Over the longer term, the trend of margin pressure on express delivery companies has become increasingly evident. In the first quarter of this year, although some firms experienced a modest improvement in gross margins, these remained at relatively low levels compared with previous years. The underlying reason is that, unlike in the past, per-parcel prices are still subdued, while parcel volumes have risen and costs for transportation, labor, and other inputs continue to climb.

Take ZTO Express as an example: from 2017 to 2021, the company's gross profit margins were 33.27%, 30.47%, 29.95%, 23.15%, and 21.67%, respectively. In the first quarter of this year, ZTO Express's gross profit margin dropped to 20.49%; Yunda and SF Express have seen their gross profit margins decline steadily over the past five years; YTO's gross profit margin rebounded somewhat in the first quarter of this year, but remains below its 2018 level; JD Logistics' gross profit margin declined in 2021 but has since recovered in the first quarter of this year.

With room for profit recovery still available across the parcel-delivery industry, what has become of J&T Express, which once sparked a price war in the sector?

Since entering the Chinese market in 2020, J&T Express has consistently been a complex player. On the one hand, backed by the Bubugao Group, it has pursued a low-price strategy to achieve rapid expansion; just ten months after its entry, J&T's daily parcel volume exceeded 20 million. According to the logistics self-media outlet 'Yizhan,' J&T's current average daily throughput across its entire network has not only surpassed but also stabilized at over 40 million parcels.

Based on publicly available data for January–April this year, J&T Express ranks third in parcel volume, behind only ZTO Express and Yunda Express. However, despite its rapid growth, J&T faces several challenges, including relying solely on low pricing to capture market share and offering services with limited reliability. Recently, the company has also been repeatedly embroiled in negative headlines related to wage arrears, cargo congestion, and transportation accidents.

As the industry's price war eases, J&T Express's low-price strategy is no longer as effective. To tap new growth opportunities, the company has been steadily expanding into overseas markets, with aggressive expansion in regions such as the Middle East and Mexico.

Meanwhile, another round of intense competition has begun in the express delivery industry.

Moving Toward High-Dimensional Competition

As price wars are no longer the primary mode of competition in the industry, express delivery companies are turning their attention to the 'long term' and seeking breakthroughs for sustainable, long-term growth.

Here, 'the distant horizon' refers to the refinement and optimization of the logistics value chain. For instance, in the last-mile delivery segment, Yunda is rolling out its 'station-to-door delivery' service, thereby accelerating the transformation of its non-directly operated network into a more directly managed model.

"The last mile" represents the final link in the logistics fulfillment chain, and all major express delivery companies are making moves in this area. For example, SF Express launched Fengchao in 2015; Yunda began developing its last-mile service infrastructure in 2019, encompassing service outlets, express supermarkets, MiGuan self-pickup lockers, and collaborative delivery platforms; Shentong has vigorously promoted its internally developed last-mile store brand, "Miao Station," across its express delivery network; and ZTO established its last-mile delivery team, "Tuxi," in 2021.

Beyond the last mile, courier companies are all taking "developing the entire logistics chain" as their future focus. Among them, SF Express and JD.com Logistics, which target the mid-to-high-end market, are leading the way.

Supply chain capabilities are the strengths of SF Express and JD.com Logistics. According to SF Express's financial report, driven by growing supply chain demand and the consolidation of Kerry Logistics, its supply chain and international business segment grew by nearly 200% last year. In April this year, although domestic express delivery business declined year-on-year due to the pandemic, SF Express's supply chain and international business revenue more than tripled year-on-year. According to JD.com's first-quarter financial report, revenue from integrated supply chain customers reached RMB 17.9 billion, accounting for 65.33% of total revenue, a year-on-year increase of 16.2%.

Both companies continue to invest heavily in supply-chain capabilities. According to SF Express's financial report, the company's R&D spending increased by 15.43% in 2021. In addition to digitally and intelligently upgrading its logistics network, another key area of research is smart supply-chain technology.

According to the prospectus released by JD.com Logistics in 2021, it is expected that about 20% of the net proceeds from the IPO will be used to develop advanced technologies related to supply chain solutions and logistics services within 12 to 36 months after the listing. This year, JD.com Logistics is focusing on building its logistics network by launching the "Weaving Network Plan," which aims to construct 43 large-scale smart logistics parks under the "Asia No.1" brand and approximately 1,400 warehouses nationwide to establish logistics infrastructure and systems, thereby meeting merchants' more diversified inventory management needs.

The competitive edge of the "Three Tong and One Da" express delivery companies lies in pricing; however, homogeneous services and cutthroat price wars make it difficult to build sustainable long-term competitiveness. Consequently, optimizing the logistics value chain has become a key strategic focus for these firms at present.

For example, in recent years, Yunda's capital expenditures have primarily been directed toward the construction of sorting centers, the acquisition of automated equipment, the enhancement of transportation capacity and capabilities, and research and development in technology. ZTO Express, by contrast, has placed a strong emphasis on building logistics infrastructure, earning it the industry nickname "infrastructure fanatic." Currently, more than 90% of its transit hubs are company-operated, and the proportion of self-owned trunk-line freight vehicles exceeds 85%. According to its 2021 financial report, land and buildings accounted for roughly 75% of total capital expenditures, with the remainder allocated to the purchase of vehicles and automated equipment.

In terms of infrastructure, in addition to investments in land and automated equipment, Yuantong has also been ramping up its aviation operations in recent years. By the end of 2021, the company operated a fleet of 10 aircraft of its own, making it the only express delivery firm within the Tongda group to own an airline. Furthermore, in January of this year, construction officially commenced on the Yuantong Jiaxing Air Logistics Hub, a global air logistics hub project in which Yuantong is a key participant.

Meanwhile, STO Express has established origin warehouses in key industrial clusters, offering tailored solutions to merchants that help reduce their logistics burdens and improve shipping efficiency. This strategic move enables the company to enter the e-commerce last-mile delivery segment, further expand its express-delivery ecosystem, and pursue new growth opportunities.

In terms of building core competencies, express delivery companies are currently ramping up efforts to develop deeper and more robust logistics networks. Externally, the industry has seen three investment and M&A deals over the past year, accelerating industry consolidation.

Over the past year, the largest acquisition in the express delivery industry was carried out by SF Express. In September last year, SF completed the acquisition of a controlling stake in Kerry Logistics for HKD 17.555 billion. Kerry Logistics is the largest international logistics company listed on the Hong Kong Stock Exchange. With the completion of this acquisition, Kerry Logistics Network will become part of SF's International Division, helping SF expand its operations beyond mainland China and the Hong Kong and Macao regions.

Another major acquisition came from JD.com Logistics. In March this year, JD.com Logistics acquired Deppon Express for RMB 9 billion. Deppon Express was once the "king of less-than-truckload shipping" in the express delivery industry, leading the domestic mid-to-high-end express transportation market. After acquiring Deppon, JD.com instantly gained 140 warehouses and 30,000 service outlets.

Last year, J&T Express acquired Best Inc.'s express delivery business for approximately RMB 6.8 billion. Best Inc. boasts a well-established delivery network and a seasoned team, while also serving a large base of Taobao merchants. As a latecomer in the industry, J&T's strategy is to leverage capital to accelerate its geographic expansion.

Compared with developed countries, China's express delivery industry still has considerable room for improvement in terms of scale, market concentration, and logistics efficiency. The "volume-for-price" model is no longer dominant, and "high-quality development" has emerged as the new industry trend. Now that the industry has reached a critical inflection point, a new phase of intense competition has quietly begun.

$STO Express Co.,Ltd. (002468.SZ)$$YTO Express Group (600233.SH)$$YUNDA Holding Group (002120.SZ)$$S.F. Holding (002352.SZ)$$JD LOGISTICS (02618.HK)$

$STO Express Co.,Ltd. (002468.SZ)$$YTO Express Group (600233.SH)$$YUNDA Holding Group (002120.SZ)$$S.F. Holding (002352.SZ)$$JD LOGISTICS (02618.HK)$

©️ DeepSound Original · Author | Li Xindi

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3