"AI Bottleneck Trade" Ignites Upstream Sector—Who’s Raking in the Profits?

From core chips and advanced packaging to foundational equipment: How to capture the 'price surge' upside in the AI supply chain?

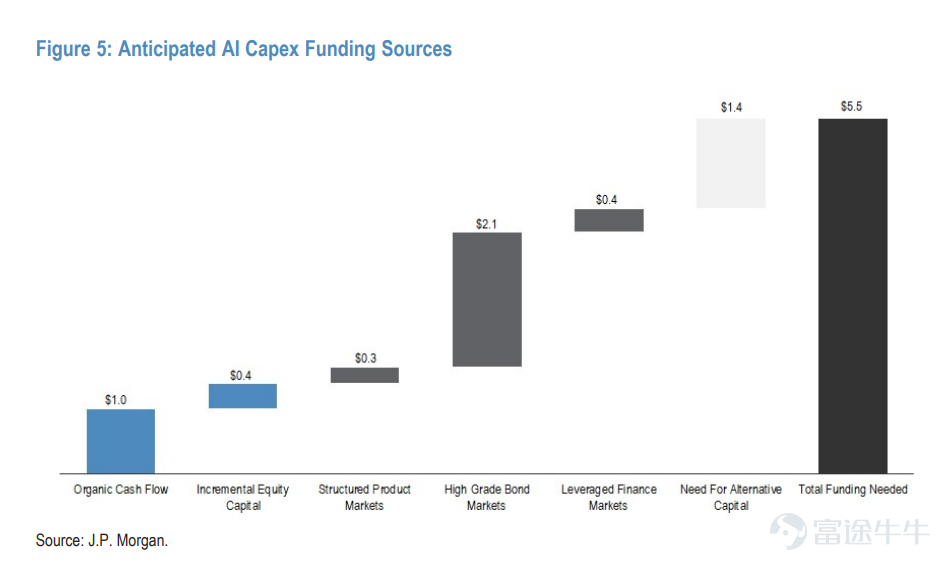

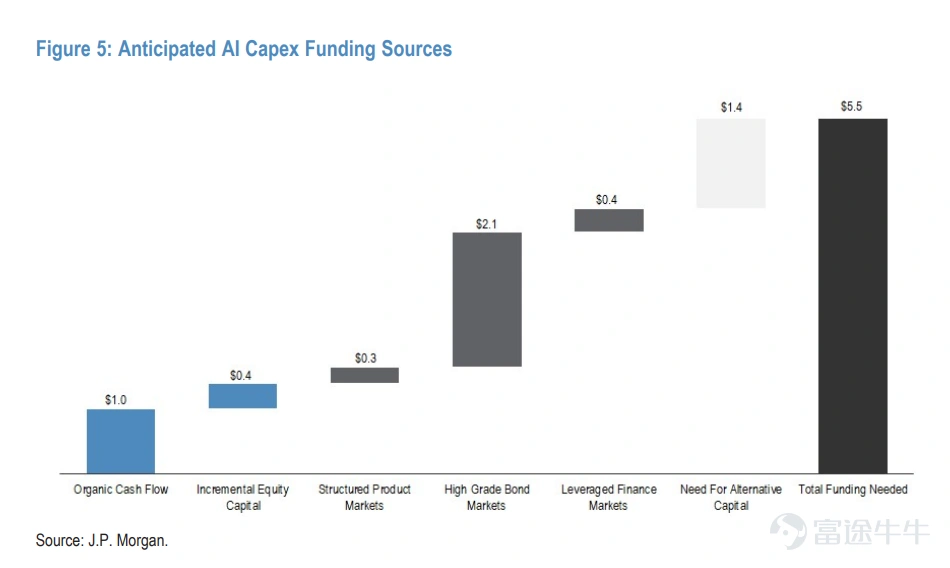

Recently, JPMorgan released a landmark research report titled 'AI Capex 2.0: If You Build It, They Will Finance It,' revealing a staggering figure to global investors:Global AI capital expenditure is projected to reach $5.5 trillion by 2030.

In this unprecedented 'spending war,' the arms race among the U.S. Big Four cloud giants ( $Alphabet-A (GOOGL.US)$ 、 $Amazon (AMZN.US)$ 、 $Microsoft (MSFT.US)$ and $Meta Platforms (META.US)$ ) continues to escalate, with combined investments expected to reach as high as $700–$725 billion in 2026 alone. Even Taiwan Semiconductor, the undisputed core 'shovel seller,' $NVIDIA (NVDA.US)$ recently announced plans to raise funds through the issuance of up to $20 billion in senior-grade bonds.

Tech giants are aggressively taking on debt (with an estimated $4.1 trillion financed via debt) to secure their AI positions, signaling thatthe 'inflationary era' of AI computing power has officially arrived.。This robust demand, driven by massive capital expenditures, is triggering a superstorm sweeping across the global semiconductor and hardware infrastructure supply chain.

Starting from the initially most scarce GPUs and extending to high-bandwidth memory (HBM), this wave has now fully expanded to semiconductor equipment, advanced packaging, optical communications, and various electronic components. Faced with such a vast supply chain, how can investors best capture promising opportunities?

How should we understand the upstream AI price-increase logic?

China Merchants Securities stated that the current AI industry chain is undergoing a rare structural repricing.Upstream computing power resource prices continue to inflate due to inelastic supply constraints,while downstream token consumption prices continue to deflate due to leaps in model capabilities and intensifying market competition.

From a direct catalyst perspective, the upstream inflation trade stems from price-hike trends.First, Korean suppliers notified Samsung and SK Hynix of a 70%–90% increase in the contract price for tungsten hexafluoride (WF6) for 2026. This was further exacerbated by supply disruption risk warnings issued in April by key Japanese WF6 suppliers such as Kanto Denka, amplifying the price-hike narrative. Additionally, CCTV Finance’s report on rising electronic-grade cloth prices has further fueled the ongoing upstream inflation trend.

From a market risk appetite standpoint, the pursuit of earnings-per-share (EPS) extremes provides fertile ground for price-hike-driven trades.At this stage of the global bull market, valuations are already elevated, making further multiple expansion difficult; thus, EPS has become the most universally embraced investment focus. Capital is flowing into positions aligned with upward EPS revisions. Given their clear logic and easily trackable data, price-hike narratives naturally emerge as the preferred vehicle for EPS-focused trades.

From a medium-term perspective, upstream inflation arises from supply-demand imbalances.Major cloud providers’ significantly increased capital expenditures have created near-'infinite' demand for upstream hardware products. However, upstream manufacturers face lags in capacity expansion, resulting in persistent supply shortages relative to demand. For instance, both Samsung and SK Hynix explicitly stated in their April–May 2026 earnings calls and analyst meetings that AI-driven memory shortages will persist into 2027 and beyond, with some key customers already securing 2027 capacity in advance. In such a supply-rewarding environment, an inflationary upstream landscape will continue to drive price-hike-led market moves.

How can investors capture promising opportunities?

MarchThe 'Inflation Era' of AI computing power has arrived! Unveiling how to capture price increases across the entire industrial chain and investment opportunities?An article once wrote,The further upstream the computational power chain (chips, memory, GPUs),,the greater the physical constraints and the more advantageous the industrial landscape,the stronger and longer-lasting the certainty of price increases.;The further downstream,(cloud services, IDCs), the more vendors there are and the fiercer the competition,the weaker the certainty of price increases.Based on this, fellow investor Niuniu has compiled a related chart for investors' reference:

The first wave: The absolutely scarce 'core computing engines' and 'contract manufacturing/packaging'

Since GPU computing power directly determines the upper limit of Token supply,Core computing engine - chipsExploded first.

Computing brain:Dominating here are oligarchs with absolute pricing power, such as $NVIDIA (NVDA.US)$、 $Advanced Micro Devices (AMD.US)$、 $Broadcom (AVGO.US)$ 。

Capacity lifeline:Once a chip is designed, it must rely on“Wafer fabrication” and “advanced packaging and testing”. Taiwan Semiconductoroccupies a core position here, while companies like $SMIC (00981.HK)$ 、 $ASE Technology (ASX.US)$ 、 $Amkor Technology (AMKR.US)$and $ASMPT (00522.HK)$ are also experiencing a revaluation due to tight capacity.

The second wave: Expansion extends into 'storage' and 'communication networks'

As the demand for AI agents with ultra-long context memory surges, price hikes are spreading rapidly.

Storage price hikes: It's a foregone conclusion that storage chip prices will rise in 2026. DRAM is expected to increase by 60%-88% for the year, while NAND could see increases of 38%-74%. Related companies such as $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$、 $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$、 $Micron Technology (MU.US)$、 $SanDisk (SNDK.US)$ 、have seen astonishing gains this year.

Additionally, regarding HDDs $Western Digital (WDC.US)$ 、 $Seagate Technology (STX.US)$ they are also worth watching closely,After conducting intensive research on Asian markets, Morgan Stanley has issued a strong signal: the HDD industry will face a supply shortfall of 300 exabytes (EB) by 2026, expanding to 400 EB in 2027/2028; suppliers' internal target pricing is $25–30 per terabyte (TB), double the current price; under an extremely optimistic scenario, Seagate and Western Digital could see their EPS grow tenfold over three years.

Optical communication infrastructure: The larger the computing cluster, the higher the communication requirements between nodes. This has spurred a massive 'optical communication network'sector rally. From silicon photonics manufacturers $Marvell Technology (MRVL.US)$ 、 $Fabrinet (FN.US)$, to optical module leaders $Lumentum (LITE.US)$ 、 $Coherent (COHR.US)$, to fiber-optic segment players $Corning (GLW.US)$and $YOFC (06869.HK)$ , indium phosphide $AXT Inc (AXTI.US)$ The entire supply chain is benefiting from the spillover of demand.

Third wave: Spreading to surrounding 'infrastructure' and 'cloud/model' sectors

The enormous computational power beast requires massive energy and extreme cooling to sustain operations.

Energy and Cooling:Infrastructure and key componentsand intermediarypower management and analog chipsare beginning to gain momentum. $Texas Instruments (TXN.US)$、 $Monolithic Power Systems (MPWR.US)$Analog chip and power management giants, as well as those specializing in liquid cooling solutions, $Vertiv Holdings (VRT.US)$are becoming the "water carriers" of the market. Meanwhile, underlying materials like CCL copper-clad laminates (e.g., $KINGBOARD HLDG (00148.HK)$ 、 $KB LAMINATES (01888.HK)$ ) and MLCCs (e.g., $Vishay Intertechnology (VSH.US)$ ), electronic components $CNBM (03323.HK)$ are also experiencing simultaneous volume and price increases due to surging high-end demand.

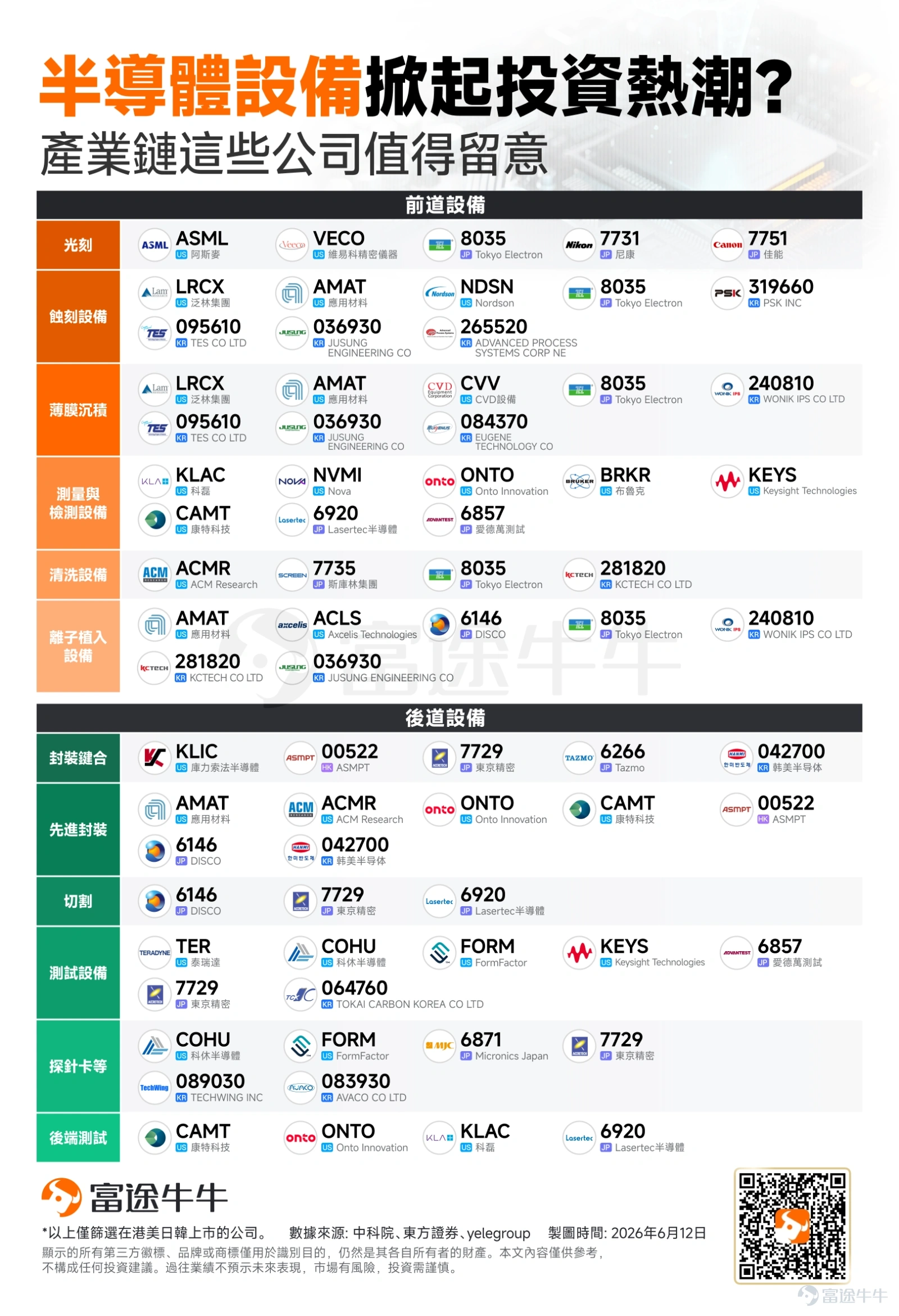

Wave Four: Core Semiconductor Equipment – The 'Foundational Pillar' of Compute Expansion

As global semiconductor capacity expansion accelerates across the board, the spillover effect from capital spending is penetrating deeper downstream. From top-tier chip manufacturing equipment to critical server assembly components, these 'hidden champions' are entering a supercycle. Previously,“ASML Holding and Applied Materials Surge to New Highs! Capacity Expansion Ignites Semiconductor Equipment Supercycle—Who’s the Next Hidden Champion?”Yiwen also compiled the latest semiconductor equipment-related stocks, as detailed below:

1. Front-end equipment: Core of wafer manufacturing

Front-end processes involve highly precise physical and chemical engineering, presenting extremely high technical barriers. The market has long been dominated by a few major equipment giants from Europe and the U.S.

a. Lithography equipment

$ASML Holding (ASML.US)$ is the undisputed global leader in the lithography equipment market.Its extreme ultraviolet (EUV) technology is the only solution available for wafer fabs to advance to 7-nanometer and below advanced nodes, giving it exceptional pricing power and irreplaceability.

$Veeco Instruments (VECO.US)$ focuses on compound semiconductor processes and advanced packaging technologies.Its core products include metal-organic chemical vapor deposition (MOCVD) and laser annealing equipment, giving it a distinct market share advantage in power devices and micro-display technologies.

b. Etching and thin-film deposition

$Applied Materials (AMAT.US)$ It is the world's largest semiconductor equipment manufacturer by revenue.It offers a highly comprehensive product portfolio covering thin film deposition (CVD/PVD), etching, ion implantation, and chemical mechanical planarization (CMP), playing a critical role in multi-material engineering for advanced processes.

$Lam Research (LRCX.US)$ It is one of the dominant global oligopolists in etching and thin film deposition equipment.Its technology holds an industry-leading position in processing high-aspect-ratio 3D NAND flash memory and advanced logic chips with complex 3D structures.

$Nordson (NDSN.US)$ It specializes in high-precision fluid dispensing and surface treatment equipment.Its technology is widely used for precise application of chemicals and adhesives in semiconductor manufacturing and packaging processes.

$CVD Equipment (CVV.US)$ It is a specialized equipment vendor focused on customized chemical vapor deposition (CVD) systems,primarily serving niche markets with specific material and specialty coating requirements.

c. Metrology and inspection equipment

$KLA Corp (KLAC.US)$It is the global leader in wafer process control and yield management equipment.It provides optical and electron-beam inspection solutions and is a key supplier for wafer fabs to manage nanoscale defects during process scaling.

$Nova (NVMI.US)$ It specializes in advanced dimensional metrology and material analysis.Its metrology tools deliver precise data on complex 3D structures, helping wafer fabs optimize their processes.

$Onto Innovation (ONTO.US)$& $Camtek (CAMT.US)$: Both companies are major players in the process control segment and have recently benefited from demand for AI chip advanced packaging (such as CoWoS and HBM), leading to significant growth in shipments of their high-precision inspection equipment for wafer-level packaging.

$Bruker Corp (BRKR.US)$: Originally founded as a manufacturer of high-performance scientific instruments, it now offers automated X-ray metrology and atomic force microscopy (AFM) solutions in the semiconductor industry for advanced analysis of microscopic crystal structures.

$Keysight Technologies (KEYS.US)$It provides comprehensive electronic design and test solutions,A key provider of critical testing services across the semiconductor lifecycle, from early chip design verification to post-manufacturing high-frequency circuit testing.

d. Cleaning and ion implantation

$ACM Research (ACMR.US)$ Focuses on semiconductor cleaning equipment.Leveraging its proprietary megasonic cleaning technology, it effectively addresses complex 3D structure cleaning challenges and is gradually expanding into advanced packaging.

$Axcelis Technologies (ACLS.US)$ Focuses on ion implantation equipment.Benefiting from rising demand for third-generation semiconductors such as silicon carbide (SiC) driven by the electric vehicle and green energy sectors, its ion implantation equipment revenue has shown strong growth.

2. Back-end equipment: Packaging and testing

As the cost of advancing Moore's Law escalates, advanced packaging has become essential to sustain chip performance improvements, significantly boosting capital expenditures on back-end equipment.

a. Packaging bonding and advanced packaging

$ASMPT (00522.HK)$ As a global leader in semiconductor packaging and surface mount technology (SMT) equipment,Its business covers traditional wire bonding equipment and is actively expanding into advanced packaging equipment such as thermocompression bonding (TCB) and hybrid bonding, making it a core indicator stock in the Hong Kong market for tracking advanced packaging trends.

$Kulicke & Soffa Industries (KLIC.US)$ It is a traditional global leader in wire bonding equipment.Its products are primarily used in mature packaging processes for automotive electronics, industrial control, and mass-market consumer electronics, providing stable cash flow.

b. Testing equipment and probe cards

$Teradyne (TER.US)$ It is one of the two global giants in automated test equipment (ATE).(the other being $Advantest (6857.JP)$ )。responsible for functional and performance testing of system-on-chip (SoC), AI accelerators, and memory chips before they leave the factory.

$Cohu Inc (COHU.US)$ specializes in test handlers, temperature control subsystems, and test contactors.ensuring testing stability and handling efficiency for chips under extreme temperature conditions.

$FormFactor (FORM.US)$is a global leader in advanced probe cards.Probe cards are a critical consumable in the wafer testing phase, with demand highly correlated to chip shipment volumes and design complexity.

Summary

In the 'inflationary era' of AI computing power, capital inevitably concentrates in core segments that possess pricing power and face supply constraints. Investors should trace the supply chain from downstream to upstream, closely monitor capacity expansion progress, equipment delivery lead times, and product pricing trends across each segment, and identify high-quality companies truly capable of converting substantial capital expenditures into tangible profits.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (18)

to post a comment

295

1112