NVIDIA publicly showcases CPO switches—could optical communication stocks be turning around?

Research report sparks sell-off! SemiAnalysis turns bearish on CPO and 800V architecture—real downside or massive overreaction?

Since the beginning of this year, 800VDC (800-volt direct current) and CPO (co-packaged optics) have undoubtedly been the two dominant narratives in the semiconductor market.

However, a report released overnight by the well-known AI industry analyst firm SemiAnalysis caught the market off guard. The report directly indicated that the adoption timelines for these two core AI data center technologies will be delayed: $NVIDIA (NVDA.US)$ Shipments of the 800VDC power architecture are now expected to be delayed until 2028, while mass production of CPO may be pushed back to 2028 or even 2029.

The simultaneous downward revision of these two key expectations has not only instantly triggered severe volatility in the optical communications sector but also sparked intense debate across the industry and capital markets regarding future technology roadmaps and investment opportunities.

So, what signals did SemiAnalysis’s report actually send to provoke such a sharp market panic? Is this a fundamental bearish shift in industry logic, or merely indiscriminate selling driven by emotional overreaction? This article will break it down for fellow investors, cutting through the noise to clarify the path ahead for investment.

I. The Report at the Eye of the Storm: Why Are Both Key AI Technologies Facing Delays?

In this report, SemiAnalysis presented two core assertions with potentially disruptive implications for the market.

1. 800VDC Architecture: Delayed Until 2028; ±400VDC Remains on Schedule

The market originally anticipated that 800VDC would see explosive adoption in 2027, but it now appears that its large-scale rollout has been postponed to 2028 and beyond.

a. Efficiency considerations of cloud providers:Industry rumors suggest that hyperscalers are hesitant about NVIDIA's dominant 800VDC architecture. They believe that receiving power from a 350–450VDC grid, stepping it up to 800VDC, and then stepping it down again to 50VDC for compute trays is an inefficient process.

b. Not a hard requirement for the Rubin architecture:The adoption rate of 800VDC will remain low in the second half of 2026 through 2027, as NVIDIA’s Vera Rubin architecture does not mandate 800VDC (it can still accept 50VDC). This architecture will only become essential in higher-power generations such as Rubin Ultra or Feynman.

c. ±400VDC remains on track:As another high-voltage DC architecture, ±400VDC is primarily used for hyperscalers’ in-house ASIC deployments and is still on schedule for rollout in the second half of 2026.

2. Physical and economic barriers facing CPO

Regarding co-packaged optics (CPO), SemiAnalysis believes market expectations for 2027 shipment volumes are overly optimistic. System-level integration challenges and low yields for scale-out CPO switches currently pose major obstacles to mass production.

a. Stringent yield math:Even under optimistic assumptions—where the assembly yield for a single optical engine reaches 95%—the total system yield for an ASIC system integrating 32 COUPEs (co-packaged optical engines) would be only about 19% (0.95^32).

b. Integration and Testing Challenges:During onboard system testing of NVIDIA Spectrum 6 CPO, insertion loss exceeding 3.5 dB was observed, consuming the entire optical channel budget. Since rework is not feasible on the soldered switch substrate, every COUPE must be perfect after coupling.

c. Commercialization Timeline Delays:

◦ Scale-out CPO Switches— Wall Street currently forecasts shipments of over 60,000 to 100,000 scale-out CPO switches in 2027. However, constrained by the aforementioned yield issues, current production rates fall far short of this target, and reports expect this forecast to be revised downward in future models.

◦ Scale-up Interconnects— 2029 will be the true inflection year: The large-scale adoption of CPO is expected only from 2029 onward. By then, key projects such as AWS, AMD, and NVIDIA’s Feynman will ramp up meaningfully, and optical engine technology will have fully matured.

II. Market Impact and Stock Revaluation

At the individual stock level,SemiAnalysis believes that technology delays are often accompanied by significant reshuffling in capital markets—recent 'winners' may become 'losers' in the short term, and vice versa.

Beneficiary sectors (established solution providers benefiting from delayed technology adoption):

a. Traditional power and gray-area infrastructure:The delay in 800VDC adoption extends the lifecycle of existing large-scale UPS (uninterruptible power supply) businesses, benefiting companies such as $Vertiv Holdings (VRT.US)$ . Meanwhile, it also provides longer growth runway for $Forgent Power Solutions (FPS.US)$ , Legrand, and Schneider—electrical equipment suppliers.

b. Copper interconnects and pluggable optics:The delay in CPO directly confirms that copper remains the core interconnect solution for vertically scaled networks, benefiting companies such as $Amphenol (APH.US)$ 、 $Semtech (SMTC.US)$ and $MACOM Technology Solutions (MTSI.US)$ . At the same time, $Marvell Technology (MRVL.US)$ 、 $Zhongji Innolight (300308.SZ)$ 、 $Eoptolink Technology Inc., (300502.SZ)$ 、 $Tower Semiconductor (TSEM.US)$ 、 $STMicroelectronics (STM.US)$ 、 $Astera Labs (ALAB.US)$ companies focused on pluggable transceivers will continue to experience strong growth.

c. CPO testing equipment:Since system-level yield is the biggest pain point, it has become critical to ensure every optical engine is flawless before assembly, $Teradyne (TER.US)$ and $FormFactor (FORM.US)$ test equipment suppliers such as these will be among the first to benefit.

Pressured segments (aggressive tech players lacking near-term catalysts):

a. Pure-play wide bandgap semiconductor suppliers:Demand for both wide bandgap and silicon-based semiconductors is relatively neutral at ±400VDC, whereas 800VDC is where materials like silicon carbide (SiC) truly see explosive adoption. Delays in 800VDC deployment mean that $Wolfspeed (WOLF.US)$ and $Navitas Semiconductor (NVTS.US)$ companies like these have lost a key near-term catalyst supporting their high valuations.

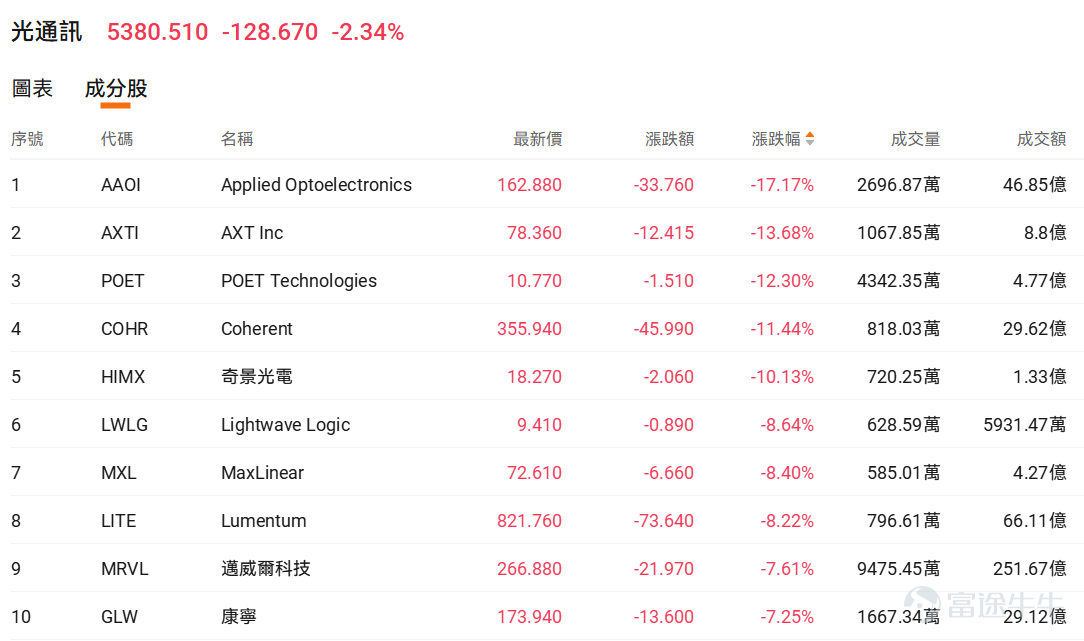

b. Optical companies overly reliant on CPO: $Lumentum (LITE.US)$ 、 $Coherent (COHR.US)$ 、 $Himax Technologies (HIMX.US)$ 、 $Applied Optoelectronics (AAOI.US)$ companies like these face valuation downside risks due to excessively high market expectations for their CPO shipment volumes.

III. Is this fundamentally bearish, or merely an emotional overreaction?

Just as market panic spreads, frontline industry developments are telling a very different story.

1. NVIDIA Executive 'Debunks Rumors' of CPO Delay

At the same time that the SemiAnalysis report was widely circulating among institutional circles, veteran semiconductor and tech investment journalist Tae Kim conducted a one-on-one interview with Gilad Shainer, Senior Vice President of NVIDIA Networking, during Computex. The executive’s comments stood in sharp contrast to the report’s conclusions.

There is no delay in the second-half CPO product delivery schedule. The Spectrum-X Ethernet CPO switch will enter mass production and begin ramping up customer deliveries strictly as planned in the second half of 2026.

He distinguished between limited commercial validation and full-scale network-wide replacement: the second half of 2026 will primarily involve small-volume rollouts to leading supercomputing customers, followed by steady capacity expansion in 2027—contrary to institutional claims of a complete halt.

The inter-rack optical interconnect roadmap for the Rubin server platform remains unchanged. CPO and traditional pluggable optical modules will coexist long-term, with no risk of the technology path being abandoned.

Additionally, the CEO of Lumentum recently stated:CPO products are expected to begin shipping in the second half of 2027 and officially hit the market in 2028.NPO (Near-Packaged Optics) has recently gained rapid industry attention, with lower implementation barriers than CPO and a market potential that may even exceed CPO.

2. Computex and Institutional Sources Jointly Refute Pessimistic Outlook on 800VDC

At the recently concluded 2026 Taipei International Computer Show (Computex),NVIDIA has explicitly incorporated HVDC (High-Voltage Direct Current) power options into the reference design for the Vera Rubin NVL144.(PSU/BBU specifications reach up to 660kW and 560kW, respectively.) Meanwhile, industry giants such as Delta Electronics, Lite-On, Flex, and Vertiv showcased their HVDC solutions at the exhibition. Delta’s management even provided clear guidance:HVDC adoption is expected to reach approximately 20% by the VR200 generation.

Guojin Securities offered an objective analysis of the underlying industry logic:

1) NVIDIA’s 800VDC architecture was originally scheduled for introduction with Rubin Ultra—meaning the entire power delivery chain, from outside the rack to inside the server, would be upgraded to support 800V. Thus, there was never an expectation that Rubin would begin shipping with HVDC.

2) In fact, major hyperscalers like Meta, Microsoft, and Google have already started placing ±400V HVDC orders with leading power supply manufacturers this year. It should be emphasized that ±400V and 800VDC are not entirely separate technical paths; they share strong continuity in system topology, power component selection, control strategies, and supply chain support—the primary differences lie in voltage levels and the timing of safety/compliance adaptations.

3) At this stage, ±400V better meets existing safety regulations and engineering deployment requirements, making it a more suitable transitional solution prior to the full-scale rollout of 800VDC.

In other words, CSPs’ decision to initially adopt ±400V does not indicate a delay or invalidation of the 800VDC trend; rather, it signals that HVDC power architectures have progressed from theoretical discussion to actual order validation.

IV. Summary: Underlying demand remains robust—awaiting value reversion

Meanwhile, multiple high-frequency data points released intensively this week further corroborate that underlying demand for AI infrastructure remains strong, with no fundamental reversal observed:

Fiber optics see simultaneous volume and price increases: Fujikura, a fiber optics giant, has raised data center cable prices, benefiting from concentrated orders placed by North American hyperscale cloud providers.

Component makers report explosive earnings: Chieh Hoo, a leading rack rail manufacturer, is experiencing a strong procurement wave, with monthly revenue surging 47% month-over-month.

Major AI chip order confirmed: Reports indicate Google and Intel are discussing a massive order for up to 6 million TPUs.

Core storage partnership locked in: SK hynix and NVIDIA have formally agreed on a multi-year storage collaboration deal, securing future capacity.

Overall, considering actual supply chain developments and strong industry endorsement,the recent sector-wide selloff triggered by the SemiAnalysis report may essentially represent capital markets recalibrating expectations around the timeline for new technology adoption, rather than a fundamental rejection of the overall AI data center outlook.After this emotional overreaction subsides, fundamentally sound stocks that were unfairly sold off could present an excellent recovery opportunity.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (58)

to post a comment

183

1026