Countdown to NVIDIA's conference: AI computing power and storage sectors may benefit—what to invest

From Persistent Declines to Expectation Gaps: Have the Downward Pressures on China's Internet and Consumer Sectors Reached a Tipping Point?

I. Why Have These Sectors Continued to Decline? What Common Pressures Is the Market Pricing In?

In the past, the decline in China’s internet and consumer sectors was often oversimplified as: weak macro conditions lead to weak stock prices. But why hasn’t the market been willing to systematically increase positions even after valuations have clearly retreated? The answer may lie not just in valuation levels, but in the fact that investor confidence—in demand, profitability, capital flows, and policy transmission—has yet to recover.

First, consider demand-side factors. Although consumer and internet companies appear to belong to different sectors, both fundamentally hinge on the same variable: whether households are willing to spend and businesses are willing to expand. According to data from China’s National Bureau of Statistics, year-over-year growth in total retail sales of consumer goods was only 0.2% in April 2026, with cumulative growth for January–April at just 1.9%. Structurally, categories tied to property—such as automobiles, home appliances, furniture, and building materials—are under clear pressure. For consumer companies, this directly lowers revenue growth assumptions; for internet firms, segments like e-commerce GMV, advertising spending, local services, and on-site travel and hospitality are also constrained by weak consumer sentiment.

More importantly, the market is seeing not just weak consumption in a single month, but continued caution from the household sector. Weak income expectations, a strong propensity to save, and low willingness to take on leverage all point to one reality: household consumption behavior has shifted from expansionary to defensive. Consumption hasn’t disappeared—it has simply become more cautious, more price-sensitive, and more focused on value for money. Such a consumption environment can support revenue resilience for some companies, but it makes it difficult for the market to proactively re-rate the sector upward.

The second common pressure comes from real estate. Real estate is not merely an industry-specific variable—it is a key component of household balance sheets. A significant portion of Chinese household wealth is tied up in housing assets, and falling home prices suppress consumption through three channels: the wealth effect, risk appetite, and income expectations. Even if household cash flows haven’t deteriorated significantly, sustained declines in asset prices will still prompt households to defer large expenditures, reduce debt, and increase savings. For consumer stocks, this means big-ticket and discretionary spending are unlikely to regain trend-like elasticity; for internet companies, advertising budgets from real estate-linked sectors—such as home furnishings, autos, financial services, and local service providers—are also unlikely to recover quickly.

The third common pressure stems from capital flows. Since 2026, the performance of A-shares and Hong Kong equities has not been a broad-based bull market but has instead been highly concentrated in areas such as AI, semiconductors, computing power, and telecommunications. Recently, within CITIC’s Level-1 sectors, electronics and telecommunications have significantly outperformed other industries, while less crowded segments like consumer and financial stocks have continued to experience outflows. In other words, the declines in internet and consumer stocks are driven not only by fundamentals but also by relative crowding-out effects resulting from extreme concentration in investor preferences.

The fourth common pressure arises from policy transmission. Policies aimed at boosting consumption—such as trade-in programs, support for platform economies, and measures against 'involution'—do provide a floor, but the market is increasingly focused on whether these policies can translate into corporate earnings. If policy only drives short-term sales volumes, the stock price reaction tends to be fleeting; only when policies improve household income expectations, employment outlooks, inventory turnover, discount rates, and profit margins can sector valuations undergo a systematic upward revision.

Therefore, what the market is currently pricing in is a combination of factors: persistently weak demand, unresolved drag from real estate, uncertain profit margins, capital chasing high-momentum themes, and policy support that has yet to translate into earnings upgrades. This combination explains why low valuations alone do not automatically attract buying interest.

II. Internet and Consumer Sectors Should Be Viewed Separately: Similar Declines, But Different Underlying Issues

Beyond these shared pressures, the idiosyncratic challenges facing internet and consumer sectors differ. Bundling the two together simply as 'domestic-demand assets' obscures their distinct valuation constraints.

The core tension for the internet sector lies in uncertainty around profit margins—not merely declining revenues. In the past, Chinese internet companies commanded high valuations because they exhibited high growth, high profitability, and strong network effects simultaneously. Now, all three of these pillars are being reassessed. User growth has matured, e-commerce GMV elasticity has diminished, advertising revenue has become more dependent on macro-level consumption and merchant sentiment, and local services face increasingly fierce competition in a saturated market.

On-demand retail offers a telling example. Alibaba, JD.com, and Meituan are all competing for dominance in on-demand retail and local fulfillment gateways. While this segment holds considerable long-term potential, in the near term it entails higher subsidies, heavier warehouse and logistics investments, and more complex organizational commitments. For investors, the issue isn’t whether these businesses generate revenue, but whether new revenue comes at the cost of lower margins. If revenue growth coincides with margin compression, the market will struggle to restore platform companies’ valuation multiples to previous levels.

AI presents a similar dynamic for internet firms. Over the long run, AI could enhance ad targeting efficiency, drive cloud service demand, improve content creation productivity, and strengthen enterprise software capabilities. However, in the short term, AI primarily manifests as increased capital expenditures, model training and inference costs, product subsidies, and organizational restructuring. The market won’t automatically re-rate internet companies simply because 'AI is a long-term opportunity'—unless it sees clear evidence that AI investments translate into high-margin revenue or improved operational efficiency.

The issue facing the consumer sector lies in shifts in consumption structure. Households aren’t refraining from spending altogether; rather, they are shifting away from high-ticket items, strong brand premiums, and high-margin scenarios toward essential goods, value-oriented channels, services, and more cost-effective choices. Many listed consumer companies previously relied on brand premiums, channel advantages, and stable offline inventory turnover—assumptions now being repriced.

In one sentence: the internet sector’s challenge is whether platform companies can defend their profit pools, while the consumer sector’s challenge is whether consumer firms can retain pricing power amid structural shifts. Both sectors face macro demand headwinds, but the validation metrics for valuation recovery differ.

III. Have the suppressive factors reached an inflection point? What is the market’s underpriced expectation gap?

What truly matters now isn’t whether these suppressive factors have fully vanished, but whether they’ve shifted from 'further deterioration' to 'marginal stabilization.' Once the market continues pricing based on the most pessimistic linear extrapolation while actual data begins showing bottoming-out stability, an expectation gap will emerge.

The first expectation gap lies in consumption demand itself. The market sees weak headline retail sales, but may be underestimating the resilience of essential consumption. According to Huachuang Securities research, April’s headline retail sales appeared weak, but this figure includes volatile categories such as gold and jewelry, oil price fluctuations, and policy-sensitive items like appliances, autos, PCs, and tablets—whose sales were heavily influenced by the timing of trade-in subsidies. Excluding these volatile and policy-driven categories, the remaining core non-discretionary consumption segment—which accounts for over 80% of total retail sales—has not continued deteriorating. This portion better reflects the 'true consumption base' and has stabilized since late 2024.

The significance of this assessment isn’t to prove that consumption has strongly rebounded. On the contrary, its greatest value lies in redefining 'weakness.' Weak headline retail sales confirm genuine pressure on aggregate demand; however, the stabilization of essential consumption at a low level indicates that households’ basic spending capacity hasn’t collapsed further. For investors, this implies the market may have mispriced 'low-level stability' as 'ongoing deterioration.' The true inflection point on the demand side isn’t an immediate strong recovery in consumption, but rather the moment the market recognizes that the consumption base has stopped declining further.

The second expectation gap concerns housing market expectations. The market tends to wait for a nationwide property price reversal before discussing consumer recovery, yet consumer valuations might only require the interruption of overly pessimistic real estate sentiment. The National Bureau of Statistics’ interpretation of April 2026 data for 70 major cities shows that first-tier city residential prices rose month-over-month, and the number of cities reporting flat or rising new-home prices increased. While this signal isn’t sufficient to confirm a nationwide property turnaround, it does suggest the drag from real estate may be transitioning from 'broad-based deterioration' into a 'period of localized stabilization observation.'

A systematic re-rating of the consumer sector certainly depends on household balance sheet repair. However, stock prices don’t necessarily need to wait until nationwide home prices turn positive year-over-year to start reacting. If secondary-market home prices, listing volumes, transaction cycles, and high-end residential sales improve first in core Tier-1 cities, market concerns about further declines in household asset values could ease ahead of broader recovery. According to National Business Daily, in Q1 2026, transactions of residences priced above RMB 30 million in China’s four Tier-1 cities rose 14% year-over-year, with luxury home sales in Guangzhou and Shenzhen surging over 100%. While luxury sales have limited impact on the overall housing market, they serve as an early signal of shifting asset allocation preferences among high-net-worth individuals. The real inflection point on the property side isn’t immediate price increases, but rather the cessation of persistent expectations of further declines that fuel new pessimism.

The third expectation gap lies in capital positioning. The market assumes capital won’t flow back into consumer and internet stocks, yet low positioning itself is creating room for rebound elasticity. The fundamental investment case for AI and semiconductors remains intact, but crowded trades and industry trends aren’t synonymous. When capital becomes excessively concentrated in a few high-momentum sectors, low-position assets get continuously abandoned—until their relative returns, valuations, and positioning reach extreme levels. On the evening of May 22, seven semiconductor supply chain companies—Zhongwei Company, Montage Technology, ASR Microelectronics, Changxin Botech, Canaan Quantum, Jingsheng Shares, and Gowell Micro—announced share reductions. Based on closing prices that day, the total divestment amounted to RMB 12.692 billion, marking the highest single-day semiconductor-sector divestment of the year. This signal shouldn’t be simplistically interpreted as a reversal of industry trends, but at the trading level, it indicates marginal shifts in behavior among industrial insiders in the most crowded segments.

At this stage, a common phenomenon emerges: even modest fundamental improvements can trigger significant price elasticity due to low expectations and light positioning. Consumer and internet stocks may not yet exhibit clear right-side momentum, but conditions are ripe for trading on expectation gaps. The true inflection point on the capital side may not be the end of the AI theme, but rather when the risk-reward profile of overcrowded sectors begins shifting—and lightly held assets regain eligibility for comparative consideration.

IV. When Will the Genuine Turning Point Arrive: Current Phase and Signal Chain

The most appropriate characterization of the current phase is not that 'a reversal has already been confirmed,' but rather that we are in the 'late stage of bottom-testing and early stage of bottom-consolidation.' Point-in-time stabilization signals have already emerged, but broad-based recovery has yet to be confirmed; left-side expectation gaps are beginning to form, but right-side trend signals remain insufficient. This phase assessment itself is not a conclusion; its primary value lies in helping identify what signals are needed for a genuine turning point.

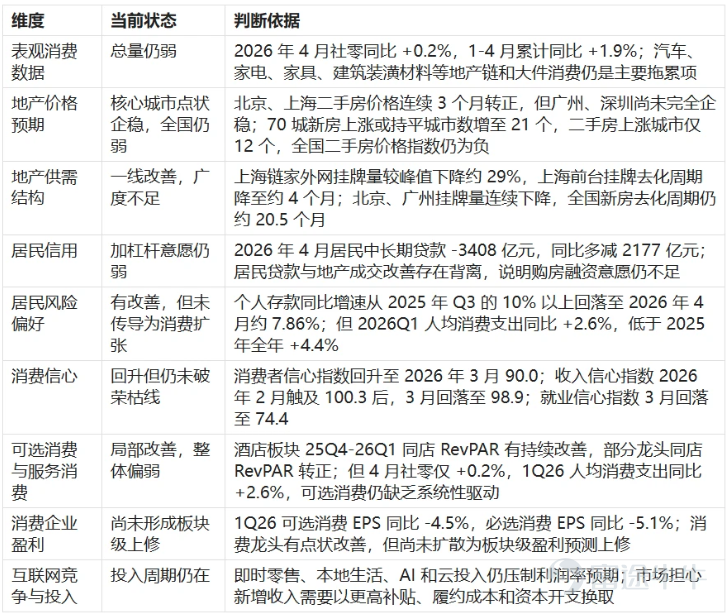

Data sources: National Bureau of Statistics, People's Bank of China, Wind, research reports from various brokerages; compiled by the author

The implication behind this table is that not all indicators are deteriorating at present; rather, 'leading indicators have partially stabilized, core credit indicators remain absent, and earnings and capital flow indicators have yet to confirm improvement.' Signs of stabilization at low levels have already appeared in property prices and basic consumption, but household medium- to long-term loans and earnings forecasts for consumer companies remain weak. Therefore, the current phase cannot yet be defined as a right-side recovery; it more closely resembles a bottom-consolidation period where left-side expectation gaps are just beginning to emerge.

In the author’s view, the genuine turning point will not arrive via a single data point, but rather through a chain of confirming signals. Sector performance will progress through three stages: stabilization, expectation-gap-driven rebound, and fundamental reversal.

The first stage is the stabilization phase. During this phase, we need to see continued stability in basic consumption, no further deterioration in core-city property markets, no further decline in consumer confidence, and no escalation in competition among internet platforms. This phase does not correspond to a major rally, but rather to valuations ceasing to contract further.

The second stage is the expectation-gap-driven rebound phase. Catalysts could include consumer data outperforming pessimistic expectations, reduced crowding in AI or semiconductor trades, stabilization in core-city property markets spreading to more cities, or internet platforms strengthening share buybacks and profit discipline. A key feature of this phase is that stock price elasticity may exceed the actual pace of fundamental improvement, as prior expectations and positioning have already fallen to very low levels.

The third stage is the confirmation of fundamental reversal. This phase requires sustained improvement in household medium- to long-term loans, rising consumer income and employment confidence, upward revisions to consumer-sector earnings forecasts, recovery in internet advertising revenue, cooling platform competition, and sustained rotation of capital flows from AI and dividend-paying sectors toward consumer and internet stocks. Only at this stage might these sectors transition from expectation-gap-driven trading into systematic allocation.

We currently appear to be in a window observing the transition from the first stage toward the second—not yet in the third stage.

V. Key Indicators to Monitor Going Forward

The author believes that the following leading indicators warrant ongoing attention:

Whether month-over-month prices of existing homes in core cities have stabilized for multiple consecutive months.

Whether the number of cities (out of 70 tracked) reporting month-over-month flat or rising home prices continues to increase.

Whether the volume of existing homes listed for sale declines and the time-on-market shortens.

Whether household medium- to long-term loan growth shows sustained improvement.

Whether the growth rate of household deposits moderates and the gap between deposits and loans narrows.

The consumer confidence index, particularly its subcomponents on income expectations and employment expectations.

Whether same-store sales of discretionary consumption show signs of improvement.

Whether discount rates offered by consumer-facing companies narrow and inventory turnover improves.

Whether the number of consumer-sector companies receiving upward revisions to earnings forecasts increases.

Whether the consumer and internet sectors have consistently outperformed on a relative basis, and whether capital is rotating from AI and high-dividend stocks toward domestic demand.

Among these, the most critical are the first three housing market indicators and the seventh and eighth micro-level corporate signals.

Because, ultimately, the market needs to believe in two things:

Households are willing to spend, and businesses are able to make profits.

These indicators collectively address one key question: Is the market pricing in a short-term bounce, or is it beginning to believe in a fundamental turnaround?

Conclusion

China’s internet and consumer sectors have not yet entered a clear right-side recovery, but the narrative is no longer solely about 'further fundamental deterioration.' Reported consumption data remains weak, yet essential consumer spending shows resilience at low levels; the property sector continues to weigh on sentiment, but core cities are starting to show localized signs of stabilization; capital is still chasing AI and semiconductors, yet extreme crowding itself is increasing the potential upside for less crowded assets.

In my view, the real source of mispricing isn’t that consumption has already strongly rebounded or that the internet sector has re-entered a high-growth cycle. Rather, the market may be incorrectly pricing 'low-level stability' as 'continued deterioration.' Until household credit conditions, corporate profitability, and capital flows broadly improve, these sectors remain better suited for a structural opportunity approach. However, if baseline consumption resilience persists, pessimistic expectations on property are disrupted, and crowded AI trades begin to unwind, the rebound elasticity of internet and consumer stocks could significantly exceed current market consensus.

Risk Warning

The views expressed in this article reflect only the author’s personal research and analysis and do not constitute investment advice. Company, industry, and market analyses referenced herein are based on publicly available information and reasonable assumptions, and may suffer from information lags or interpretive errors. Should household income and employment expectations continue to weaken, property prices resume their decline, platform competition intensify further, or AI-related themes continue to absorb capital, the timing of a recovery in internet and consumer sectors could be further delayed.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2