百度大漲9%!無人駕駛風口再起?

百度2026Q1業績深度分析:AI業務佔比首破50%,雲增速領跑三巨頭

一、業績核心亮點:結構性拐點確認

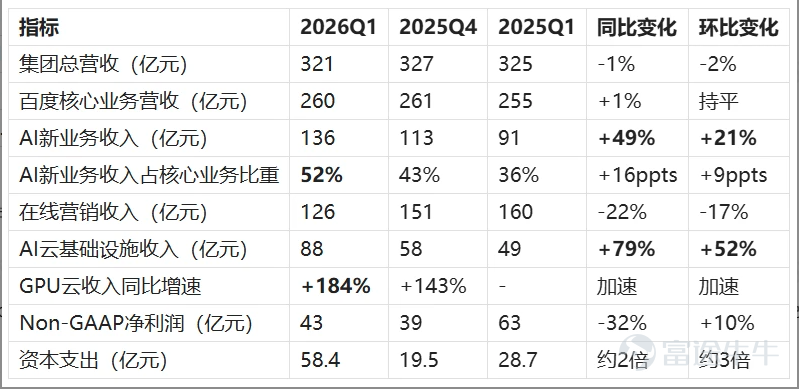

1.1 核心財務數據

百度2026年第一季度實現總營收321億元,環比下降2%;百度核心業務營收260億元,同比增長1%,在連續數個季度下滑後首次恢復正增長。據百度業績披露,這一增長主要由AI雲業務驅動。

數據來源:公司業績

核心判斷:2026Q1是百度戰略性拐點——AI新業務佔百度核心業務收入首次突破50%(達52%),標誌着公司估值邏輯從"AI賦能搜索公司"正式轉型爲"帶着傳統業務的AI公司"。

1.2 業務板塊表現

強勢板塊:AI雲基礎設施收入88億元,同比+79%。GPU雲業務增速從上季度143%進一步提升至184%,成爲核心增長動力。Apollo Go Q1完成320萬次全無人駕駛行程,武漢單城已實現盈虧平衡。

穩定板塊:AI應用收入25億元,同比持平。文心助手日活同比翻倍,秒噠月活環比增長70%。AI原生營銷服務收入23億元,同比+36%,但體量尚小。

承壓板塊:傳統廣告業務的結構性挑戰

在線營銷服務收入126億元,同比-22%,其中傳統搜索廣告同比-29%。核心矛盾在於AI搜索的推進侵蝕了廣告貨幣化率——生成式AI回答替代了傳統搜索廣告位,但AI原生廣告體系尚未成熟。AI原生營銷服務雖然同比增長36%,但23億元的體量遠不足以對沖傳統搜索廣告102億元、下滑29%的衝擊。

筆者認爲,廣告下滑已被充分定價。關鍵預期差在於AI原生營銷服務的增長斜率能否在下半年加速——若數字人+Agent組合在廣告主ROI驗證後大規模採用,可能比市場預期更早實現對沖。

二、AI業務深度解析:三大引擎與差異化優勢

2.1 文心大模型:應用驅動路線與生態壁壘

管理層強調模型通過應用創造價值,堅持應用驅動迭代路線。文心5.1已登頂LM Arena中文模型文本榜1、搜索榜1。核心應用包括AI搜索、數字人(成本下降80%,支持24種語言)、秒噠無代碼平台(月活環比增長70%)等。

生態壁壘:百度App月活6.79億,文心助手MAU 2億+,構成流量飛輪:搜索產生數據→數據訓練文心→文心強化搜索→用戶留存→商業化變現→研發投入。這種"應用入口+雲平台+模型生態"的協同佈局強化了百度在AI產業中的平台地位。

2.2 智能雲:全棧優勢驅動增速與利潤率雙升

雲業務加速邏輯:AI雲基礎設施收入從2025Q1的49億元增長至2026Q1的88億元,增速從+34%加速至+79%,GPU雲增速從+128%加速至+184%。管理層指出,企業AI需求從訓練轉向大規模推理部署,推理算力需求密度遠高於訓練階段,驅動收入指數級增長。

全棧四層架構:百度是全球極少數提供完整四層AI全棧的公司:雲基礎設施(崑崙芯)→深度學習框架(飛槳)→基礎大模型(文心+千帆)→AI應用。這種架構的核心價值在於層間協同創造成本護城河——用自研芯片跑自研框架再跑自研模型,每層的效率提升都會被下一層放大,形成競爭對手無法簡單複製的成本結構優勢。

崑崙芯差異化:單AI算力集群超3萬顆加速器大規模商用部署,全面兼容主流大模型。崑崙芯的三重價值:內部降本(爲文心、Apollo提供算力)、對外差異化(GPU供應受限環境下提供額外選擇)、未來擴張路徑(2026年計劃發佈M100芯片,2027年M300芯片)。

千帆MaaS平台:支持DeepSeek、智譜AI、MiniMax等主流模型,外部客戶日均token消耗量達去年同期近7倍。管理層強調百度通過全棧AI能力,在同等算力資源下實現更高throughput,本質是推理效率領先。

利潤率改善路徑:GPU雲(毛利率目標35-40%)佔比提升+AI應用訂閱(天然高毛利)+Apollo Go盈虧平衡複製,將驅動雲業務整體利潤率結構性改善。這與阿里雲"利潤率爲第二目標,增長優先"的策略形成對比。

資本支出壓力:Q1 Capex高達59.2億元(爲Q4的3倍),現金儲備2793億元提供安全邊際,但持續高Capex將壓制短期EPS。Capex折舊將在2-3個季度後體現在成本端。

管理層指引:全年增速不低於40%,長期毛利率目標25-30%,經營利潤率目標20%+。

2.3 Apollo Go:從驗證階段邁向規模化盈利

2026Q1完成320萬單(同比+120%),累計超2200萬單,覆蓋全球27城,武漢單城已實現盈虧平衡。海外擴張進展:歐洲(瑞士測試、倫敦Uber/Lyft合作)、中東(迪拜全無人運營+獨立App)、國內(海南機場接駁)。

風險:海外監管進展不及預期是主要風險。市場對Apollo估值仍施加折價(對標Waymo),反映商業化路徑的保留態度。武漢盈虧平衡是積極信號,但能否向更多城市複製、海外定價環境是否真的更優,仍需時間驗證。

三、三巨頭對比與百度雲增速領先原因

3.1 核心數據對比

數據來源:各公司業績及業績會紀要

3.2 百度雲增速領先的三大核心驅動因素

百度AI雲基礎設施同比增速79%,GPU雲增速184%,顯著超越阿里雲38%和騰訊雲20%。這一增速領先是多重結構性因素疊加的結果。

驅動因素1:崑崙芯供給側差異化

百度是國內極少數既有大規模自研AI芯片又實現外部商業化的雲廠商。崑崙芯提供內部降本+對外差異化+未來擴張路徑。客戶在供需偏緊時更關注穩定性,利潤率更優。

挑戰在於需持續高強度研發投入保持技術領先。阿里平頭哥產能改善後將形成競爭,字節也在加大自研芯片投入。崑崙芯外部商業化規模仍需擴大。

驅動因素2:需求從訓練轉向推理,百度更受益

企業AI需求從訓練轉向推理,推理算力需求密度遠高於訓練階段。百度獨特優勢:Apollo全球27城運營本身是最大規模推理需求方之一,將內部需求轉化爲對外推理服務能力展示,吸引自動駕駛、具身智能等行業客戶。疊加金融、央企、手機廠商等多行業AI部署需求擴容。

驅動因素3:騰訊雲外部供給受限的市場讓渡

騰訊GPU資源被內部多個高優先級場景瓜分(混元研發、微信AI Agent、廣告遊戲AI),外部雲業務被動讓步,爲百度提供市場窗口期。

騰訊明確表示下半年國產ASIC芯片產能改善後將向外部釋放更多GPU算力。百度當前部分市場份額受益於騰訊暫時性收縮,下半年競爭將趨於激烈。

四、投資價值判斷與核心邏輯

百度2026Q1業績質量好於市場預期,AI驅動業務突破50%是結構性轉折點;雲業務增速領先的背後是全棧自研(崑崙芯+PaddlePaddle+文心)帶來的真實競爭優勢,而非單純價格戰。

短期來看,廣告拖累仍將持續,AI原生營銷23億元體量仍小,不足以抵消傳統搜索的下滑速率。Capex三倍擴張帶來的折舊將在2-3個季度後體現在成本端,利潤率壓力不容忽視。

中期需要監控以下關鍵指標:

崑崙芯IPO進展(價值解鎖的一級催化劑)

AI雲基礎設施增速能否在Q2-Q3 2026維持60%+(驗證需求不是一次性爆發)

GPU雲毛利率改善的量化數據

AI原生營銷服務能否在2026年底佔到廣告收入20%+

崑崙芯IPO進展(價值解鎖的一級催化劑)

AI雲基礎設施增速能否在Q2-Q3 2026維持60%+(驗證需求不是一次性爆發)

GPU雲毛利率改善的量化數據

AI原生營銷服務能否在2026年底佔到廣告收入20%+

長期(2-3年):百度是全球AI基礎設施轉型中最獨特的標的之一——既有媲美Waymo的自動駕駛資產(Apollo累計22億公里里程),又有類Google的AI全棧能力,還有類比Arm的芯片分拆潛在路徑。當前估值對應的是傳統互聯網廣告衰退邏輯,而非AI全棧公司的成長邏輯,存在估值重評的結構性機會。

風險提示

本文所述觀點僅代表筆者個人研究和分析,不構成任何投資建議。文中涉及的公司、行業及市場分析均基於公開信息和合理推測,可能存在信息滯後或理解偏差。投資有風險,入市需謹慎。

本文所述觀點僅代表筆者個人研究和分析,不構成任何投資建議。文中涉及的公司、行業及市場分析均基於公開信息和合理推測,可能存在信息滯後或理解偏差。投資有風險,入市需謹慎。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論

發表評論

3