AI Boom vs. Tight Liquidity: Will the US Stock Rally Continue?

[Weekly Market Insights] Easing of US-China tensions reconfirmed, how to grasp the rotation rhythm amid higher-than-expected PPI?

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/8d65e4db8ea9b762b9eea881ad10219e.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Guide to this week's strategies for the US and Hong Kong markets:

Trump's visit to China confirms easing again, how to grasp the rotation rhythm?

Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side?

[Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm?

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/962ac327fea61fe28c9e9b7687788ac0.jpg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

[I. Macroeconomic Observations]

1.1 International Macroeconomic:

The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold?

The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, with approvals granted for some Chinese companies to purchase NVIDIA chips. However, this remains largely symbolic and does not represent structural opening. Overall, this visit to China did not yield any massive orders or comprehensive trade agreements; instead, it featured symbolic purchases and institutional arrangements that reaffirmed the trade truce, carrying greater symbolic than economic significance.

The United States and China reached consensus on the Iran issue,with China agreeing to gradually reduce its reliance on Iranian energy and shift toward increased imports of U.S. energy, and pledging not to supply weapons to Iran.In the meantime,U.S. April PPI came in well above expectations, heightening upstream inflationary pressures, further dampening market expectations for a near-term Fed rate cut. The 10-year Treasury yield broke above 4.5%, while the 30-year yield hit 5.045%, its highest level since last July.Rising long-end rates are exerting clear downward pressure on high-valuation assets.

US April PPI exceeded expectations Source: US Labor Bureau 2026-05-16

US-Iran negotiation scenarios Source: FTNN 2026-05-16

1.2 Domestic Macroeconomics:

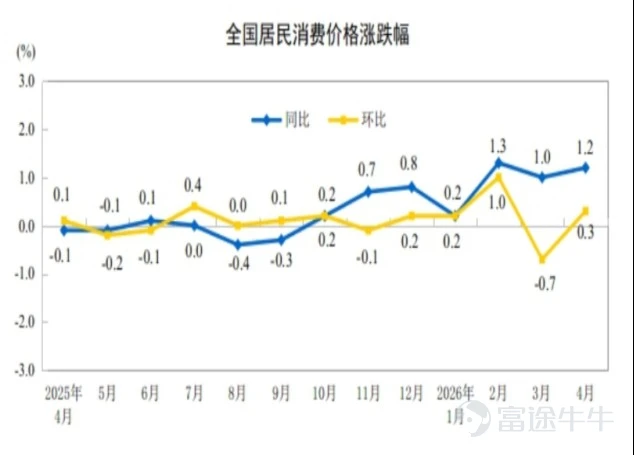

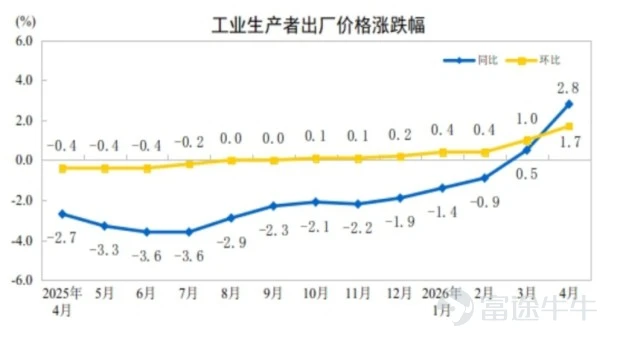

China's April CPI/PPI Rebound: Driven by Upstream or Domestic Demand Recovery?

April PPI increased 2.8% year-on-year and 1.7% month-on-month, mainly driven by three sectors: oil and gas extraction (up 28.6% year-on-year), petroleum and coal processing (up 14.2% year-on-year), and chemical raw materials (up 8.9% year-on-year), collectively contributing approximately 1.5 percentage points. Domestically, coal mining and ferrous metal smelting industries also saw a month-on-month increase. CPI rose 1.2% year-on-year, core CPI increased 1.2% synchronously, but the core consumer goods CPI excluding gold prices was only about 0.97%, with industrial consumer goods declining 0.2% month-on-month.

The current inflation recovery reflects more of a combination of 'upstream cost-push and weak downstream pricing power' rather than a full-scale overheating of domestic demand. The pricing power of mid- and downstream consumer manufacturing remains weak, domestic demand recovery is still moderate, and comprehensive inflationary pressure driven by end-user demand has yet to emerge.

Source: National Bureau of Statistics 2026-05-16

Source: National Bureau of Statistics 2026-05-16

[Section Two: Market Views]

2.1 US Stock Market

S&P slightly up, Nasdaq slightly down; how to respond as macro narrative returns?

$S&P 500 Index (.SPX.US)$ The entire week rose by 0.13%,$NASDAQ 100 Index (.NDX.US)$ Down 0.08%. Last week, US stocks began pricing in macro narratives. After the 10-year Treasury yield broke through 4.5% and WTI crude oil surpassed $105 per barrel, the market started worrying about micro profitability being impacted, sector divergence intensified, and growth stocks sensitive to interest rates faced greater adjustment pressure.

In the short term, a moderately positive stance remains, but expectations for index-level aggressive moves need to be lowered. The drivers of US stock market highs—AI capital expenditure, better-than-expected earnings, and easing geopolitical tensions—all experienced marginal disturbances in the second half of last week.From a medium-term perspective, the expansion of profits, continued operating leverage, and deeper AI adoption still support high valuations, but the tolerance of valuation and momentum to rising oil prices, inflation, and long-term interest rates has significantly decreased. Wash's most likely short-term policy mix is balance sheet reduction + unchanged interest rates, which is favorable for US stocks and gold, while US bond yields are more volatile.The core significance of the meeting between the leaders of China and the US lies in reducing tail risks rather than directly boosting profitability. The S&P 500 forward 12-month P/E ratio is 22.3 (as of May 14).

S&P 500 forward 12-month P/E ratio 22.3 (May 14) Source: Bloomberg, Futu Private Wealth compilation

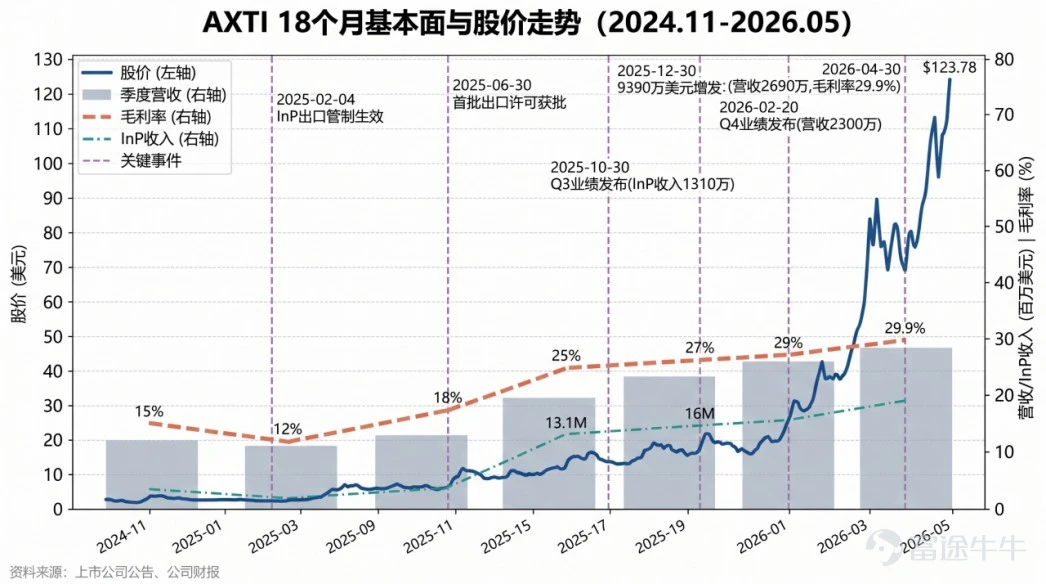

Focus Stocks$AXT Inc (AXTI.US)$ :The core supplier of InP (Indium Phosphide), the most scarce foundational material in the AI optical interconnect chain.

Management clearly stated in the Q1 earnings call that, driven by AI applications and the data center upgrade cycle, demand for InP wafers is significantly increasing, with InP revenue accounting for slightly more than 50% of total revenue. Q2 guidance confirms revenue of approximately $34 million, with upside potential if additional licenses are approved.An inflection point in performance has emerged as the product mix shifts towards high-margin InP, with some products beginning to increase in price. Q2 is expected to see non-GAAP EPS of $0.06-$0.08.。

InP demand and order strength remain extremely high, with Q2 expected to be the largest InP quarter in the company's history. China-related revenue doubled in Q1 and is expected to double again in Q2.Clear capacity expansion plan: InP quarterly capacity expected to reach approximately $35 million by the end of 2026, and increase to $65-70 million per quarter by the end of 2027 or early 2028.. Major global players are concentrated in $Sumitomo Electric Industries (5802.JP)$ 、 $AXT Inc (AXTI.US)$ 、 $JX Advanced Metals (5016.JP)$ The market anticipates a 4-6 times growth in substrate demand over the next 3-5 years, with customer certification, yield rates, and size upgrades all posing as barriers.Future stock price drivers will depend on quarterly revenue delivery, sustained gross margins, and the efficiency of capacity ramp-ups. The company is currently in the validation period following confirmation of an inflection point in fundamentals.

Source: Company announcements and financial reports, Futu Private Wealth Research compilation

2.2 Hong Kong Stock Market

Hang Seng Index fell 1.63% this week; where are the structural opportunities after positive catalysts have been priced in?

The Hang Seng Index fell 1.63% for the week, with average daily turnover reaching HKD 266 billion, an increase of about HKD 25 billion compared to last week. Southbound trading via Stock Connect recorded a net inflow of HKD 9.3 billion. Large-cap tech stocks and semiconductors opened high but closed lower.The weakening of the index is more due to external disturbances and profit-taking at higher levels, while southbound buying has not significantly retreated.On Friday alone, there was a net inflow of HKD 24.9 billion. The proportion of short-selling dropped to 10.99%, indicating that the market is undergoing portfolio adjustments rather than panic, given the high turnover and low short-selling activity.

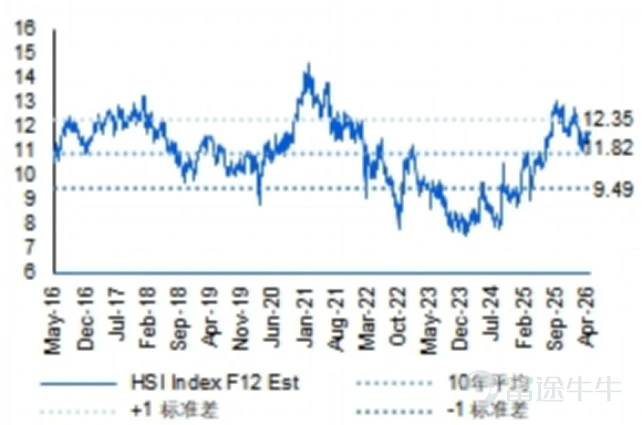

In the short term, Hong Kong stocks have entered a neutral consolidation phase at the index level, but the outlook remains cautiously optimistic for the medium term, with structural allocation opportunities becoming clearer than last week. After positive catalysts were realized in the second half of last week, there was a lack of new drivers, while US Treasury yields, oil prices, and foreign investor risk appetite continued to weigh on the market.The key difference between Hong Kong and US stocks lies in valuation advantages, and structural opportunities have not disappeared.Prioritize AI internet, export chains, and high-dividend stocks. Technology leaders are shifting growth drivers towards advertising, cloud, AI, and efficiency improvements, favoring leading platforms and companies with strong cash flow.The Hang Seng Index's forward 12-month price-to-earnings ratio stood at 11.82 as of May 15, making it an attractive valuation.

The forward 12-month P/E ratio of the Hang Seng Index stood at 11.82 (May 15). Source: Bloomberg, collated by Futu Private Wealth

Focus Stocks$LENS (06613.HK)$ :Vertically integrated platform targets in consumer electronics, robotics, and AI servers.

First-quarter profits faced pressure, but the mid-term growth logic remains intact. On the contrary, opportunities in robotics, foldable screens, automotive glass, and AI servers have become more evident across four key areas.The company has built a vertically integrated platform spanning from core components to modules and full-system assembly, covering liquid metal, aluminum-magnesium alloy structural parts, six-axis force sensors, head modules, joint modules, dexterous hands, and complete robot assembly, demonstrating strong potential as an industry chain leader.

Robots represent the most valuation-sensitive new growth driver,with combined shipments of humanoid and quadruped robots exceeding 10,000 units for the full year, and the Yong’an campus has the capacity to produce 500,000 embodied AI robots annually.Foldable displays are the most certain catalyst in the second half of 2026,with ultra-thin glass (UTG) and related components serving as key supplies; module shipments are expected to start contributing from May onward, with significantly higher per-unit value compared to traditional smartphones.

AI server orders remain robust, with active capacity expansion underway in locations such as Songshan Lake. SSD solid-state drives from the Xiangtan campus began mass shipments in March 2026, while HDD glass substrates have entered the verification and small-scale trial production phase.Near-term focus should be on the shipment cadence of foldable displays and progress in securing robot orders.

Source: Company announcements and financial reports, Futu Private Wealth Research compilation

[III. Focus for This Week]

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/e5cc107703f0dc69424d383cab4a6bdf.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

[4. Major bank views]

US Stock Summary:We maintain a cautiously optimistic near-term stance but recommend downgrading expectations for index-level aggressive upside. Earnings dispersion, sustained operating leverage, and deeper AI adoption support elevated valuations; however, linear extrapolation based on the prior six weeks’ unidirectional upward trend is unwarranted. Valuations and momentum now show significantly reduced tolerance for rising oil prices, inflation, and long-end interest rates.Market sentiment remains fragile with high sector concentration, and most individual stocks are still below their 52-week highs. Priority should be given to AI-focused sectors, semiconductors, and large technology companies with strong earnings certainty.

Hong Kong Stock Summary:In the short term, index levels have entered a neutral consolidation phase, but the outlook is not pessimistic in the medium term; structural allocation opportunities have become clearer compared to last week.US Treasury yields, oil prices, and foreign investor risk appetite continue to weigh on Hong Kong stocks. However, supported by a low base, year-on-year PPI is expected to remain high or exceed 3% in the coming months. MSCI China’s Q1 2026 earnings show initial signs of improvement, with a mild recovery anticipated starting in the second half of the year.Overweight AI internet, export chains, and high dividend stocks; underweight real estate-related sectors. The barbell strategy remains the optimal choice at present.

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/dac05689bf2ac88a68633191266bd5e4.jpg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

[5. Simulated Portfolio]

Weekly performance for May 1st

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/f6a42a539a60bc0a78a73bd985d63606.jpg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

5.2 Profit and loss attribution

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/c0317cf2f3feb835452f6f13ea2fdf47.jpg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

5.3 Portfolio adjustment strategy

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/622685ab466ec3166293e1ebfcd767b3.jpg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

5.4 Update portfolio

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/d824780cc477bf30e6c52cd79f6d7fb2.jpg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

![Guide to this week's strategies for the US and Hong Kong markets: Trump's visit to China confirms easing again, how to grasp the rotation rhythm? Higher-than-expected PPI pushes US Treasury yields above 4.5%, how will high-valuation markets respond to pressure on the denominator side? [Live Broadcast Reservation] Today at 16:30, Futu's Chief Investment Research Expert will join you to look ahead at this week’s market. Positive news emerges during the visit to China, how to grasp the rotation rhythm? [Share Link: Market First Sound Weekly Call | Positive news from the China visit keeps coming, how to grasp the rotation rhythm?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: The outcomes of Trump's visit to China and the higher-than-expected PPI, how will policy paths unfold? The results of Trump's visit to China are mainly reflected in three aspects:First, a clear procurement intention was expressed, with China expressing willingness to purchase more US energy, reaching procurement arrangements for aircraft, agricultural products (soybeans, beef), and energy categories.Second, the advancement of trade institutionalization, both parties plan to establish a dedicated institution to supervise the implementation of agreements and form institutional arrangements for non-sensitive areas, marking significant progress in Sino-US economic and trade relations;Third, there is symbolic easing in the technology sector, approving some Chinese companies to purchase NVIDIA chips, but this is only symbolic and does not constitute structural openness. Overall, no mega-deals or comprehensive trade agreements emerged from this visit to China...](https://nnqimage.futunn.com/sns_client_feed/988889/20260518/e32d8de6bb72cdcd39036381e39533d3.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Risk Disclosure

This material is provided by Futu Securities International (Hong Kong) Limited. The data and referenced data are for reference only. Past performance of the assets does not reflect future performance, and their accuracy, completeness, and reliability cannot be guaranteed. The information does not constitute investment, legal, accounting, or tax advice, nor does it consider individual investment objectives, financial situations, or specific needs. It does not constitute any recommendation, invitation, offer, or solicitation to buy structured products.

Investors should note that structured products are not collateralized. If the issuer or guarantor becomes insolvent or defaults, investors may not recover part or all of the receivables. The price of structured products can rise or fall sharply, and investors may suffer total losses. When purchasing, investors rely on the creditworthiness of the issuer and guarantor.

Bull and bear certificates have a mandatory redemption mechanism and may be terminated early. In such cases: (i) N-class bull and bear certificate investors will not receive any amount, while (ii) the residual value of R-class bull and bear certificates may become worthless.

Investors should carefully review the listing documents (including subsequent supplements to the listing documents) and supplementary listing documents regarding the relevant risks and details of structured products and assess the risks independently.

The products described on this page are structured investment products involving derivatives. They have not been authorized by the Hong Kong Securities and Futures Commission (SFC) for public offering in Hong Kong and are not available for public investment in Hong Kong. They are also not protected by the Investor Compensation Fund. Investing in structured investment products is not equivalent to investing in their underlying assets.

The structured investment products described on this page are not listed or may not have an active or liquid secondary market. Investors must bear the credit risk and bankruptcy risk of the issuer, guarantor, and/or other identified counterparties (as applicable). Investors should also note that the issuer may terminate the investment early.

Investment involves risks. Investors should proceed with caution and fully understand that they may lose their entire investment. Before making any investment decision, investors should carefully read and understand the sales documents and terms and conditions of the relevant investment products (including the risk disclosures contained therein). Investment decisions should not be based solely on this content. Seek appropriate professional advice if necessary.

General Disclaimer

The author of this report is a licensed person under the Hong Kong SFC. Neither the analyst nor his/her associates hold any financial interests in the listed corporations discussed in this research report.

This report is prepared by Futu Securities International (Hong Kong) Limited ("Futu Securities"). By receiving and/or viewing this report (including any related attachments), the holder represents and warrants that they are entitled to receive this report under the following terms, and agrees to be bound by the restrictions contained herein. Any non-compliance with these restrictions may constitute a violation of applicable laws.

Without the prior written consent of Futu Securities, this report and the information contained herein may not be reproduced, copied, or stored in any form (i) or directly or indirectly distributed or transferred to any other person for any purpose (ii).

Futu Securities shall not be liable for any direct or indirect loss arising from the use of the materials contained in this report. The information in this report comes from sources believed to be accurate and reliable at the time of issuance, but this report is not intended to include all information required by investors and may be affected by delays, obstructions, or interceptions in transmission.

Futu Securities does not expressly or impliedly guarantee or represent the adequacy, accuracy, completeness, reliability, or fairness of any such information or opinions. Therefore, Futu Securities and its affiliates (collectively referred to as the "Futu Group") shall not be liable for any type of loss (including but not limited to any direct, indirect, or consequential losses) resulting from actions taken by third parties relying on the content of this report.

All content, products, and services in this report are intended solely for users in the Hong Kong Special Administrative Region and are for general circulation only. They do not constitute an offer or solicitation to buy or sell any investment product. The report does not consider any specific investment objectives or financial situation. Individual investors should seek independent professional advice from a financial advisor and refer to the sales documents and/or the latest published information regarding the suitability of ETFs, including risk factors associated with specific investment products.

The data in this report is derived from publicly available sources and analysts believe the information to be reliable. All investments involve risks, and investors may lose their entire investment amount. Any past performance, estimates, forecasts, or simulated results are not necessarily indicative of future performance of any investment.

The relevant ETF has not been and will not be authorized by the Hong Kong Securities and Futures Commission under Section 104 of the Securities and Futures Ordinance. This report does not constitute an advertisement, invitation, or document under Section 103 of the Securities and Futures Ordinance that invites the Hong Kong public to acquire interests in or participate in collective investment schemes.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

6

4