PDD Holdings reported Q1 revenue of RMB 106.2 billion—has its share price already hit bottom?

With the acquisition of Himalaya, can Tencent Music win this defensive battle?

(This article was authored by Dolphin Research, and published by Titanium Media with authorization)

By Dolphin Research

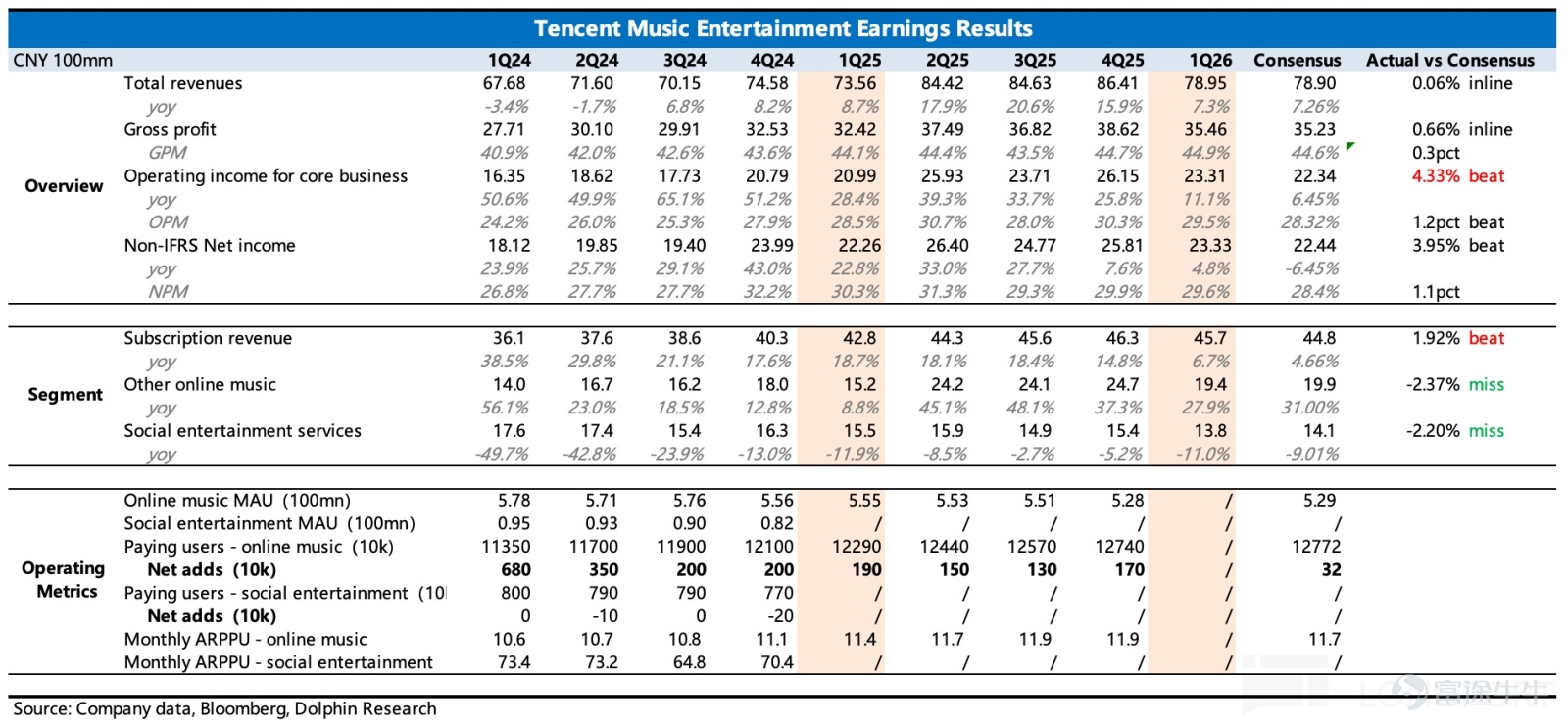

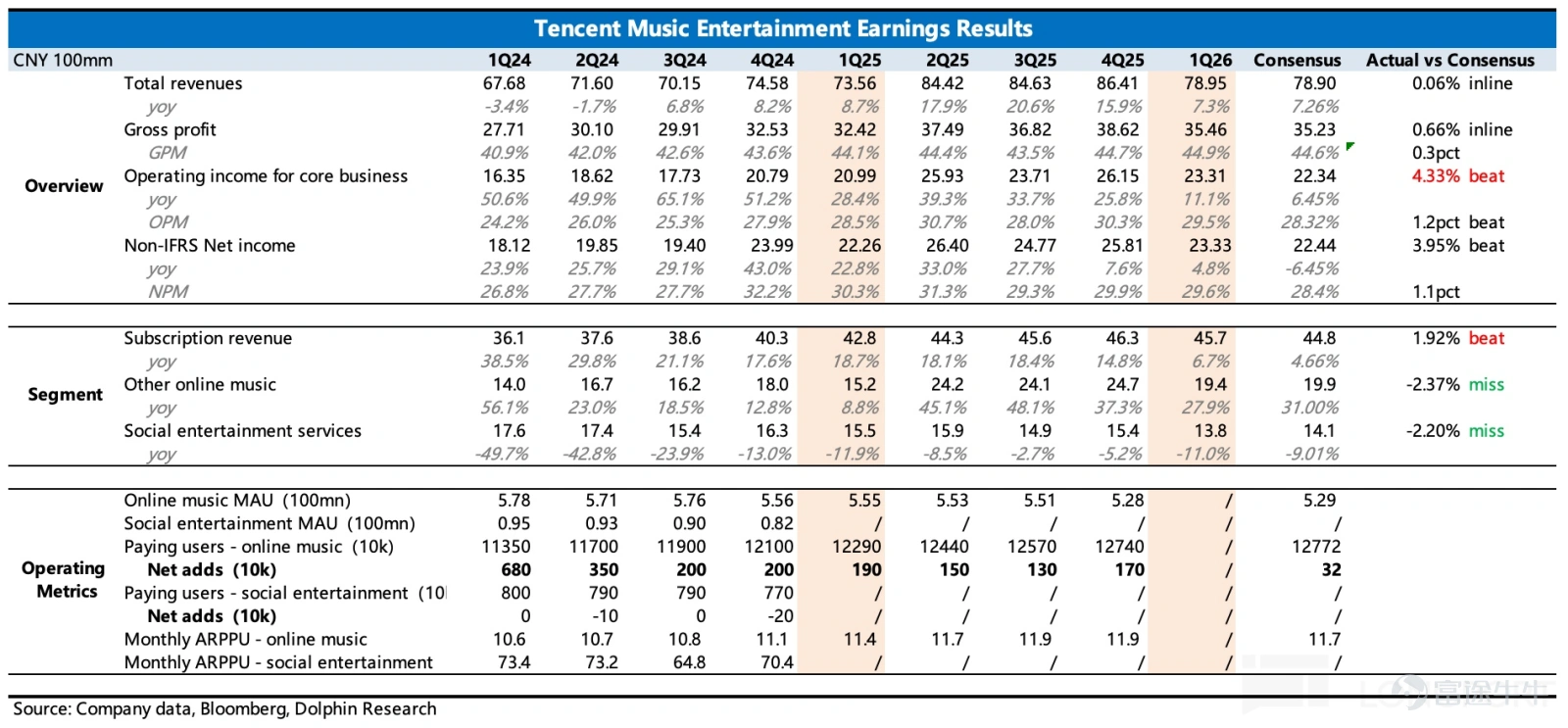

Tencent Music (TME.US) Q1 results were largely in line with expectations, aligning closely with the guidance from the previous quarter, though expenses came in slightly lower than the market anticipated. Overall, it reflects a situation where core subscription growth is showing signs of fatigue under competitive pressure and the company needs to continuously expand non-subscription music monetization channels.

However, compared to the earnings themselves, the news disclosed pre-market about the approval of the Himalaya acquisition is more noteworthy. This not only means that Tencent Music can accelerate business integration and incorporate audiobook users, but also signals that share repurchases for 'self-rescue' may begin.

Specifically:

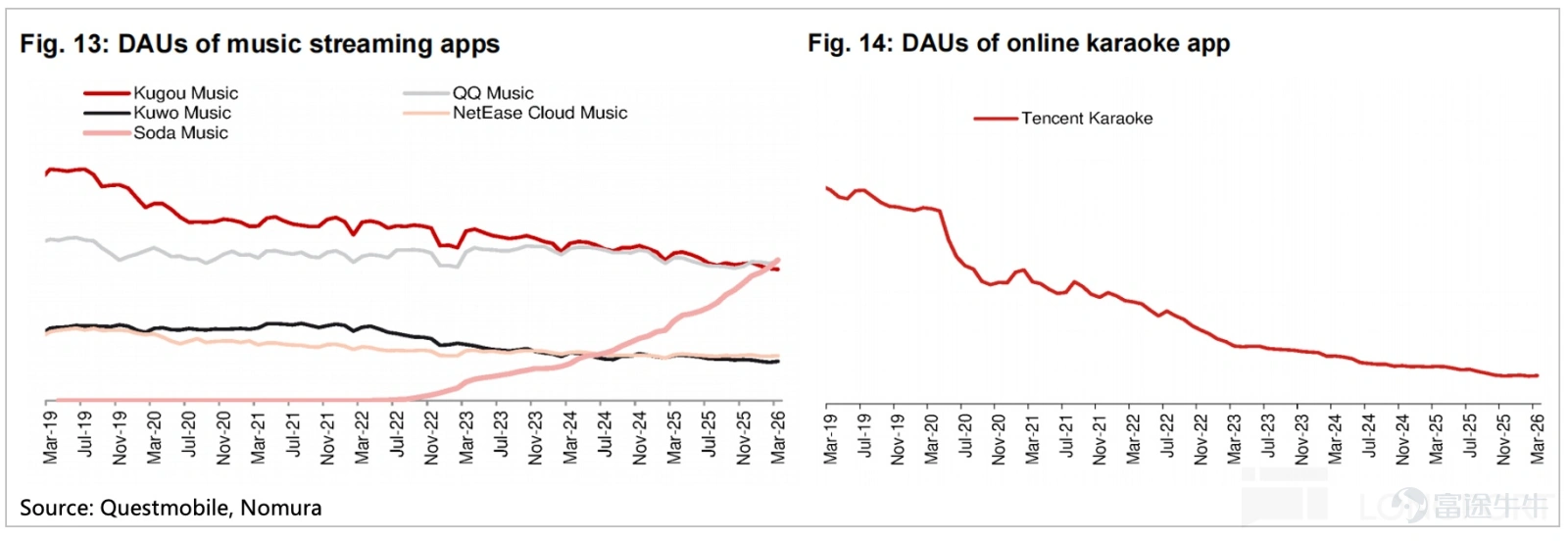

1. The ecosystem still needs continuous defense:Regarding user data, the company has stopped disclosing it since this year. Dolphin Intelligence combined the data trend from QuestMobile and reverse-calculated subscription revenue to roughly outline Q1's situation for reference only:

The MAU in the first quarter continued to decline quarter-over-quarter, with an overall stable rate of decrease. However, more effort is needed to maintain the 500 million user ecosystem. The merger with Himalaya could be an opportunity, as historically, there hasn't been much overlap between Himalaya's core users and Tencent Music's users.

However, the appeal of AI and free music platforms continues to weaken the attractiveness of licensed music. Fundamentally, it remains a competition between platforms. Therefore, even if accelerating internal cannibalization, it is essential to embrace AI actively to reduce the speed at which users leave the platform.

2. Weak subscription growth:Revenue growth in the first quarter was 6.6%, slightly above expectations but still masked underlying weakness. Following the company’s strategy last quarter of lowering the payment threshold to boost user retention, Dolphin Intelligence estimates that Q1 added approximately 1 million net new subscribers, with ARPPU declining to RMB 11.7 (for reference only).

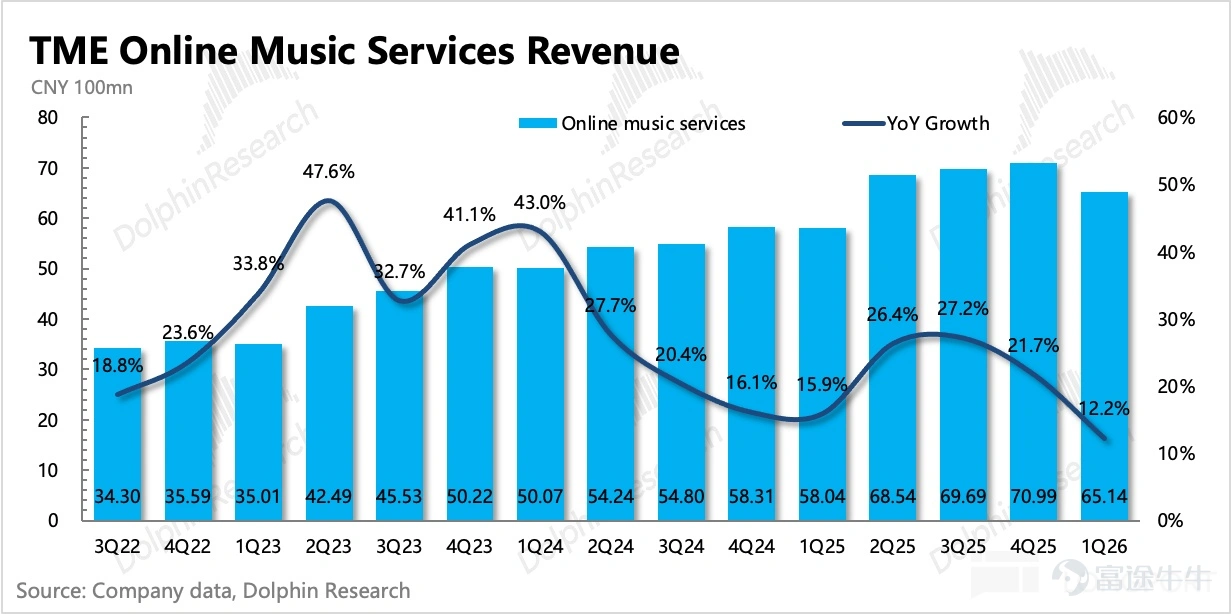

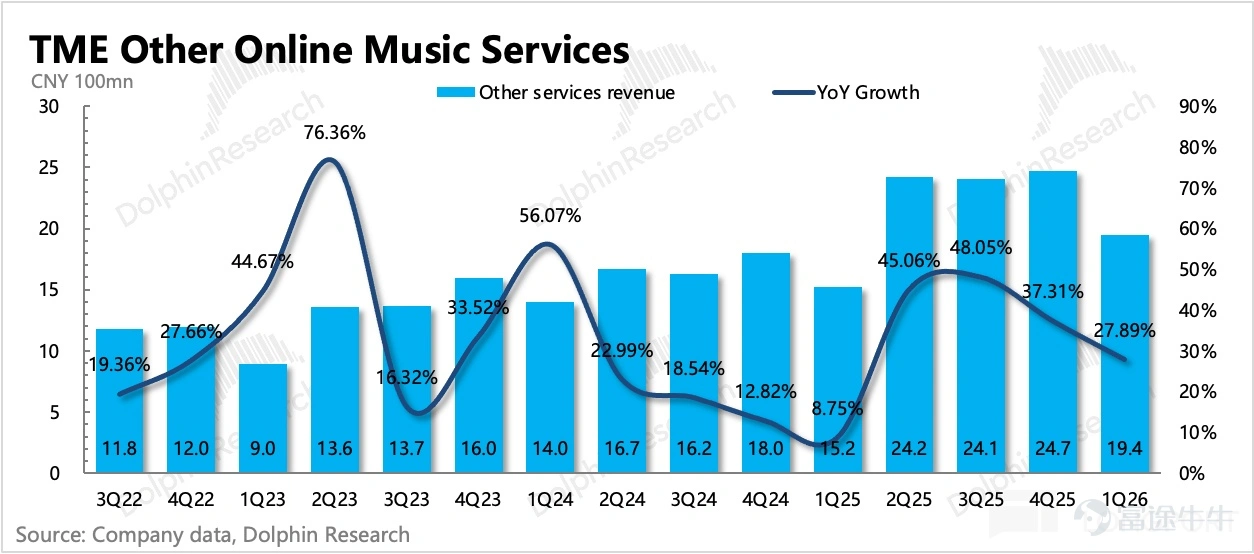

3. Music derivatives remain relatively strong:Other music-related income (advertising + offline concerts + digital albums, etc.) grew by 28%, slowing quarter-over-quarter, likely due to the later timing of Chinese New Year in Q1 amplifying the impact of a relatively quieter concert season. Despite being below expectations, this growth is still considered robust. Jay Chou’s new album released at the end of March received weaker feedback compared to his previous album four years ago, but some revenue should still be recognized next quarter.

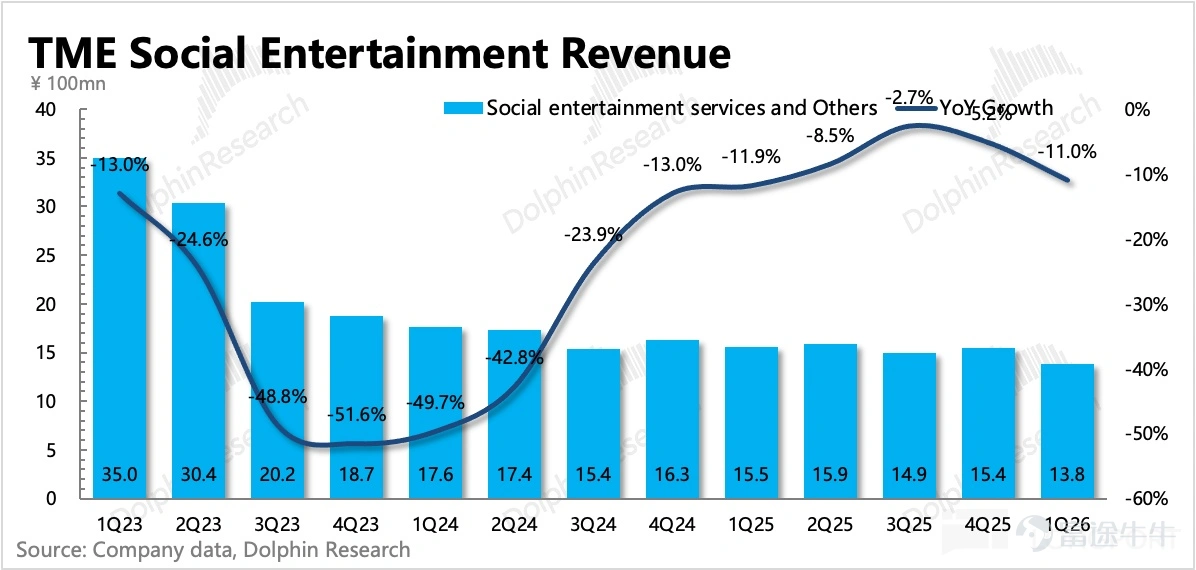

4. Social entertainment deteriorates again:Social entertainment, which was thought to have stabilized, saw a 11% drop in Q1 revenue, worsening quarter-over-quarter. We need to listen to the earnings call to understand the reasons. Dolphin Intelligence speculates that, apart from live streaming continuing to be impacted, K-song services were significantly affected by traditional competitors and AI. Currently, one of the main applications of AI among C-end users is song covers, which overlaps with the K-song experience, leading to a continued decline in Q&M Dental’s active users.

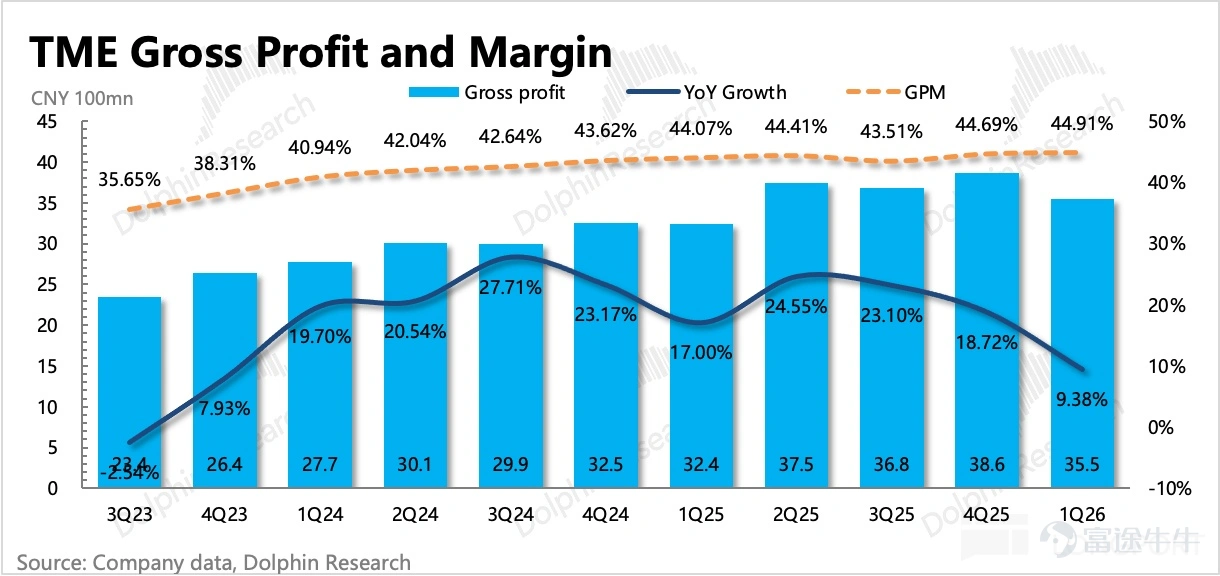

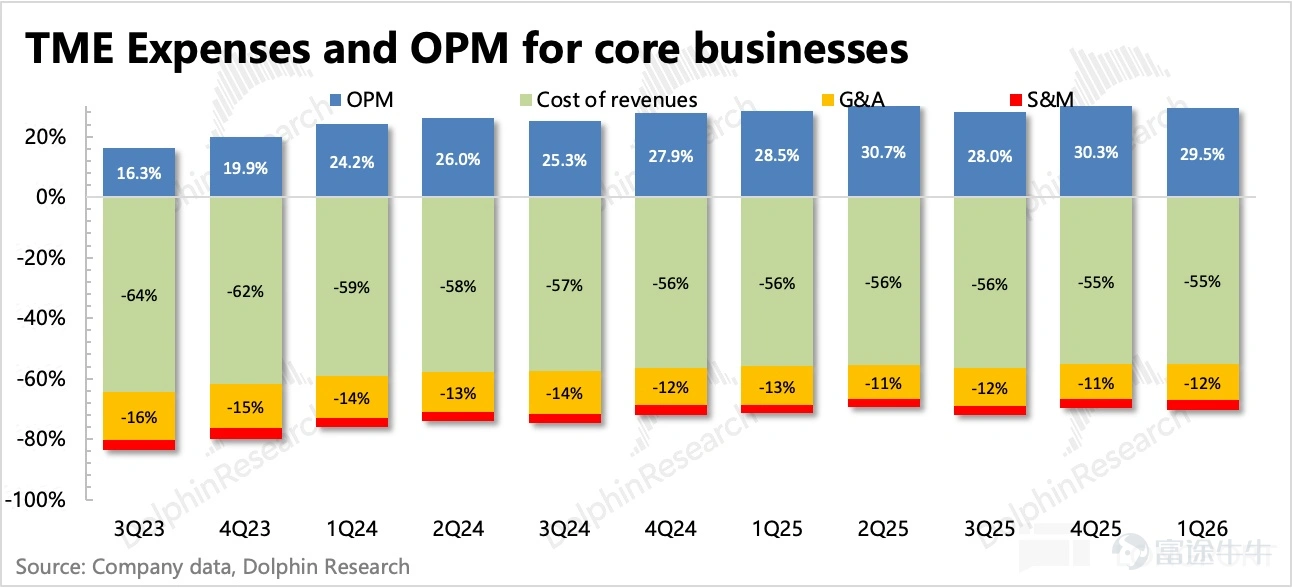

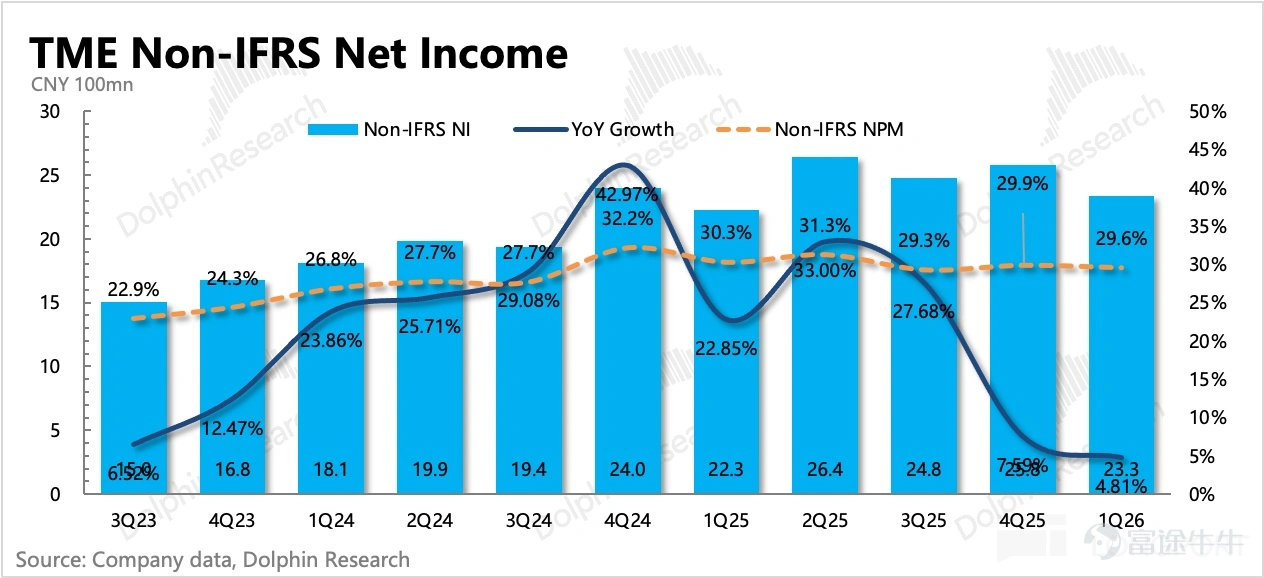

5. Investment in expansion while continuing to improve internal efficiency:Gross margin for the first quarter was 44.9%, up 30 basis points from the previous quarter, driven by an increase in the revenue share of non-subscription businesses (such as high-margin advertising) and optimization in copyright cost scale. On the operating expenses side, sales expenses maintained strong growth, reflecting the company’s ongoing efforts to actively expand its business and acquire customers. However, administrative expenses remained flat year-on-year and declined sequentially, which may indicate workforce optimization.

6. Anticipated shareholder returns:As of the end of the first quarter, Tencent Music had short-term net cash of RMB 25 billion (cash + short-term investments - short-term interest-bearing debt), equivalent to USD 3.6 billion. The company maintains a strong cash position with good cash flow from its business model, and the two-year USD 1 billion repurchase program announced in March last year has barely been utilized.

If the repurchase proceeds normally and is fully utilized before its expiration in March 2027, combined with the dividend payout of USD 370 million, the current market cap of USD 14 billion implies total shareholder returns nearing 10%, which is considered quite substantial.

7. Key Financial Data Overview

Dolphin's Perspective

The Q4 performance and guidance last year completely shattered Tencent Music’s previously advantageous investment thesis: transitioning from 'streaming price hikes' to 'lowering prices to attract users,' essentially reflecting weakened competitive moats. Additionally, the uncertain timing of regulatory approval for acquisition cases has impacted expectations for buybacks to support the stock, causing valuations to drop sharply from the historical 20x P/E to the current 10x P/E—according to company guidance, this year’s revenue will reach RMB 36 billion, adjusted profit will be RMB 10.4 billion, growing 8% year-on-year, corresponding to yesterday’s closing market cap of USD 14.4 billion at 9.6x.

Although the valuation appears lower compared to both its historical average and peers in the internet industry, until a turning point of stabilized competition emerges, the market will lack sufficient confidence in future growth. This impacts expectations on whether Tencent Music can sustain long-term growth at a CAGR above 10%, which would drive the P/E ratio to recover from 10x to 15x or even higher levels.

Based on current user data, that turning point has yet to arrive.In Q1, Soda Music’s DAU continued to grow beyond 50 million, surpassing Kugou and QQ Music. Its growth rate also does not appear to have slowed significantly. Meanwhile, Kugou Music is clearly losing users, Q&M Dental continues to weaken, and QQ Music remains barely stable.

Therefore, simply reviewing the financials makes it difficult for investors to give a positive response.However, the pre-market news about Himalaya's approval completion is the real 'confidence' catalyst.On one hand, it can boost market expectations regarding the sustainability of the user ecosystem and the restoration of competitiveness (although the effect may be limited). On the other hand, it addresses the relatively crucial issue of stock repurchases at this moment.

Tencent Music is not short on cash—it not only has substantial reserves but also operates a cash-cow business model. Previously, due to an acquisition involving a TME share swap, management was unable to use buybacks to support or compensate when the stock price was under pressure. Now that the approval process has been successfully completed, the two-year $1 billion buyback program initiated last year can be resumed.

In an optimistic scenario, the company could continue to complete the $1 billion buyback by the previously stated deadline—March 2027 (currently less than $100 million has been used). Dolphin Investment believes that given the significant recent stock price correction, the company might adhere to the original pace or even exceed the planned buyback to restore market confidence.If calculated this way, the shareholder return rate from buybacks and dividends would be close to 10%, which could already be somewhat attractive to certain investors.The continued recovery in weak sentiment could help further valuation repair. However, caution is warranted when the P/E ratio approaches 15x, or exceeds 20 billion. At this point, the shareholder return rate would decline to around 6%, reducing its attractiveness, and investors will likely demand stronger evidence of competitive inflection points and earnings delivery.

The following detailed analysis

1. Weak Growth Expected in Subscription Revenue

Subscription revenue growth in the first quarter was less than 7%. The company no longer discloses detailed 'volume and price' breakdowns, but Dolphin Investment estimates that net subscription users grew by approximately 1 million, with average monthly spending per user at 11.7 RMB. This reflects changes in the company’s strategy, including promotional campaigns at the start of the year and lowering membership thresholds to grow user scale.

After completing the merger with Himalaya, there is expected to be a short-term opportunity. According to QuestMobile, the core user overlap between the two platforms is only 15%. However, as music is a universal need, if sold in bundled packages (e.g., existing memberships paired with a 1-2 RMB premium), converting users to paying customers wouldn’t be difficult.

However, attempting to leverage their 'leading position' to extract more premium won't work in the current consumer environment, and regulators have explicitly prohibited it—service prices cannot be raised, service quality cannot be lowered, the proportion of free content cannot be reduced, exclusive licensing agreements with copyright holders are banned, and music platforms cannot be bundled with car manufacturers for sales.

Although the acquisition value has been weakened, for Tencent Music at this stage, having something is better than nothing. In addition to the integration of long-form audio users, organic growth may mainly rely on the penetration of the Super VIP (SVIP) membership (continuously adding more fan benefits).

II. Other Music Services: Growth Remains Relatively Strong

In the first quarter, other music services grew by 28% year-over-year, slightly below expectations, with a slowdown quarter-over-quarter. This is likely due to the off-season for concerts. However, several large K-Pop group concerts and NCT-WISH's Hong Kong concert were still held during this period.

Other revenue includes advertising, digital album sales, copyright sublicensing, value-added services, and more. These are all IP derivative businesses centered around monetizing fan value. While the audience size is much smaller than that of essential music consumers, the per-person value is very high, and core users in China show purchasing power comparable to those in Europe and the US.

III. Social Entertainment: Unstable Bottom, Further Deterioration

In the first quarter, social entertainment revenue declined by 11%, worsening further. In addition to live streaming being continuously affected, combined with Q&M Dental data, it’s likely that the karaoke business has been significantly impacted by competition from traditional players and AI technologies.

IV. Profit: External Investment and Internal Reflection Simultaneously

The gross margin in the first quarter was 44.9%, up 30 basis points quarter-over-quarter, benefiting from an increase in the revenue share of non-subscription businesses (such as advertising, which has high gross margins) and optimization in copyright cost scale.

However, although sales expenses remain relatively small in scale, they continued to grow rapidly by 36%, reflecting the company’s ongoing efforts to promote business expansion and customer acquisition. Administrative expenses remained flat year-over-year but decreased quarter-over-quarter, possibly reflecting workforce optimization.

Ultimately, the operating profit from the core business reached 2.3 billion yuan, growing by 11% year-over-year, outpacing the total revenue growth rate of 7%. The profit margin increased by 1 percentage point year-over-year to reach 29.5%.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

1