15:9, the Senate Banking Committee passed the CLARITY Act!

Circle: Despite the terrible market conditions, the leading stablecoin stock continues to expand

(This article was authored by Dolphin Research, and published by Titanium Media with authorization)

By Dolphin Research

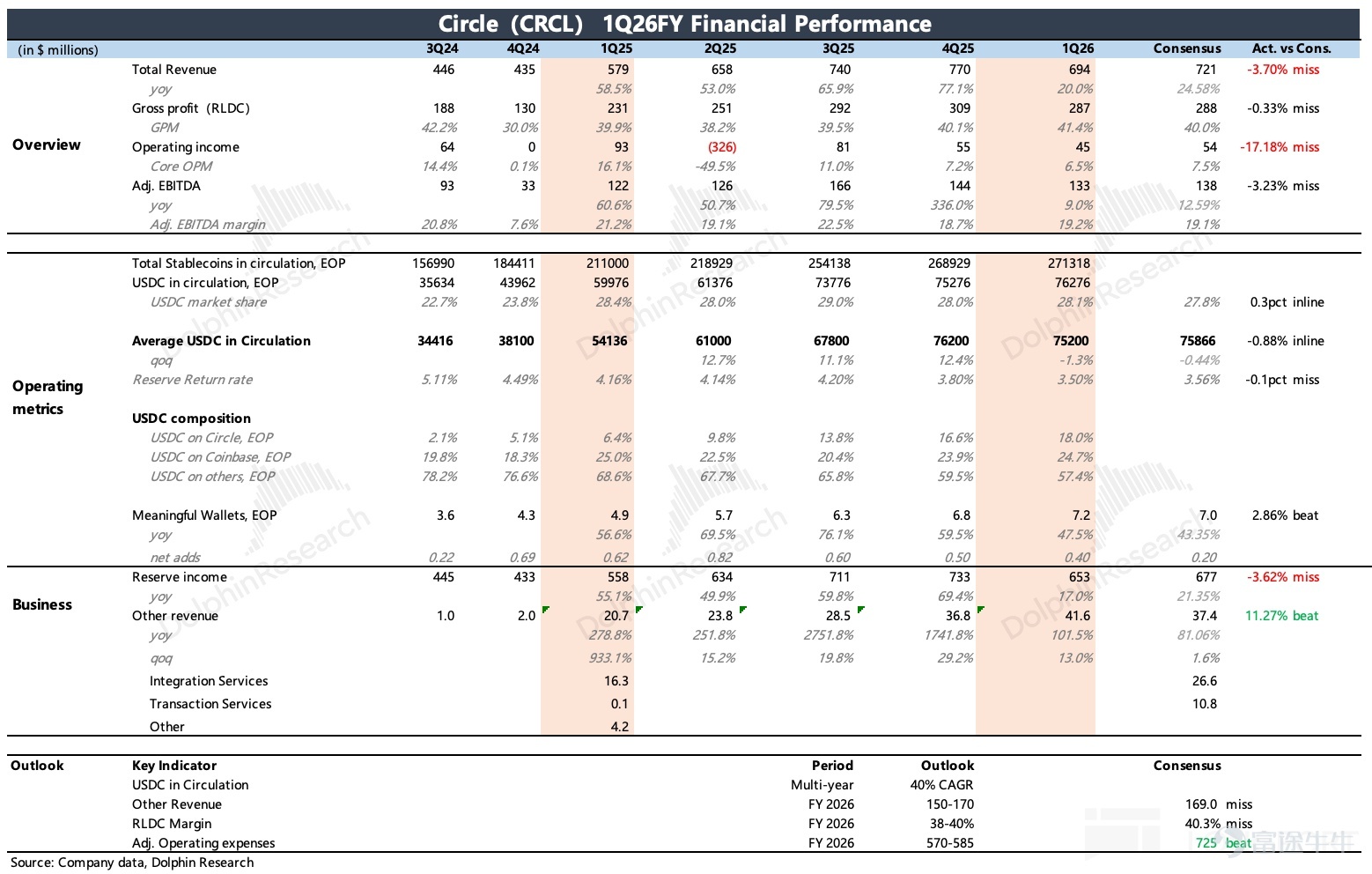

On the pre-market of May 11 in the Eastern Time Zone, Circle (CRCL.US), the leading stablecoin stock, released its Q1 2026 earnings.

It should be noted that due to the public knowledge of USDC’s scale and reserve asset interest rates, the interest income accounting for 95% can be largely determined. Therefore, most of the time, fluctuations in Circle's share price follow changes in the market value of USDC, which essentially reflects expectations of interest rate cuts and changes in crypto asset policies.

The key insights from the earnings report lie in other non-interest income, internal operational efficiency, and guidance indicating medium- to long-term strategic goals.

Overall, the highlight of Q1 remains the capital market's focus on 'other revenue' in the financial report, reflecting the steady expansion trend of the USDC ecosystem beyond cryptocurrency use cases. However, the necessary rigid investments required for ecosystem expansion will also bring significant volatility and pressure on Circle’s short-term profitability.

Specifically:

1. Ecosystem Layout: Still the same script, with crypto investments under pressure and new scenarios continuing to be developed

(1) The average USDC circulation in the first quarter was 75.2 billion. After hitting a low in February, it slowly climbed to nearly 77 billion by the end of the quarter despite an unfavorable geopolitical environment, marking a 2% increase quarter-over-quarter, similar to the previous quarter. During this period, 73 billion new coins were minted, down quarter-over-quarter due to the bleak performance of crypto assets in Q1. However, excluding this impact, the minting scale remains at a high level, reflecting the expansion of demand scenarios outside of crypto asset investment.

Meanwhile, redemptions reached 72 billion, with a faster year-over-year growth rate, indicating that some users are cashing out profits or shifting to other interest-bearing products amid the pressured crypto asset market.

The proportion of USDT's scale compared to USDC decreased in January but quickly recovered over the following two months. Therefore, from a competitive standpoint, the threat from USDT remains significant. Following the Drift hacker incident in April, Circle faced negative public sentiment while Tether actively provided substantial support to Drift, causing Circle to lose clients.

Currently, the stablecoin market is still in the early stages of overall expansion, so competition will not yet become a major factor affecting USDC's growth.

(2) Distribution within the USDC ecosystem: Circle’s share increased further to 18%, with an average daily retention rate of 17.2%. Over the past year, it has risen steadily from 6% and now stands at its current level. Meanwhile, the percentage of reserve interest income shared externally slightly decreased by 1%, with room for further optimization to enhance profitability. Coinbase accounts for nearly 25%, showing a continued trend of active retention compared to the last quarter.

(3) By the end of the first quarter, the number of digital wallets (on-chain wallets holding more than 10 USD in crypto) reached 7.2 million, with a net increase of 400,000 during the quarter, surpassing market expectations and reflecting the growth of platform-direct user base.

(4) In terms of ecosystem expansion news, the first quarter mainly involved collaborations with Cash App, Polymarket, and Kyriba (platforms supporting native USDC transactions), along with advancing the scale of Arc public chain and CPN transactions.

Overall USDC on-chain transactions in the first quarter amounted to 21.5 trillion USD, a year-on-year increase of 263%. The annualized transaction volume of CPN as of March was 8.3 billion USD, and in April, a new product called Managed Payments was launched, allowing financial institutions to enable stablecoin payments without managing digital assets.

2. Revenue has bright spots but is less impressive than last quarter: Non-interest income exceeded expectations, but growth slowed quarter-on-quarter.

The aforementioned B-end focused ecosystem expansion also brings additional revenue to Circle beyond reserve interest income – recorded under 'other income'. Therefore, in addition to helping expand the USDC market, it represents a second growth curve for Circle to counteract the pressure of declining reserve interest income in a rate-cutting cycle.

Other revenue in the first quarter reached 42 million US dollars. Although it still accounts for a small proportion (6%), it maintained double growth despite a rising base. However, from a trend perspective, the quarter-on-quarter growth rate of 13% slowed down compared to 29% in the previous quarter, making it less impressive than the last quarter.

3. Gross margin: Increased retained share to ease revenue-sharing pressures

The market previously worried that as Circle expands its ecosystem, it would need to share reserve interest income with partners, and that Coinbase's earnings report revealed an increase in the proportion of USDC, thereby raising Circle's channel distribution costs and creating gross margin pressure.

In reality, Circle continued to ease cost growth pressures by increasing its self-held share of USDC. The cost paid to Coinbase accounted for a decreasing proportion of the overall revenue-sharing costs (dropping from 97% to 75%). It is important to note that Coinbase had the strongest bargaining power in its cooperation with Circle, resulting in the highest revenue-sharing ratio of 50%.

In addition, most of the other revenue from software, payment, and other infrastructure services falls under high-margin businesses. This quarter saw faster growth in other businesses, with an increased contribution to revenue. Ultimately, the gross margin was 41.4%, improving by 130 basis points quarter-on-quarter.

4. Under rigid investment cycles, profit pressures persist:Operating profit declined significantly year-over-year, mainly due to the sensitivity of profit fluctuations when interest income, which constitutes a large proportion, is impacted under rigid investment cycles.

However, in the Q1 earnings report, management maintained its guidance for the full-year adjusted operating expenses range for FY 2026 (570-585 million US dollars), which is better than the market’s higher investment expectations (725 million US dollars).

5. Future Growth: Guidance remains unchanged, with a note of caution amid short-term volatility

(1) Regarding the outlook for multi-year scale growth of USDC, Q1 management maintained the expectation of a multi-year CAGR growth rate of 40%. However, as in the previous quarter, Dolphin君 believes caution should be exercised and immediate pricing avoided: due to significant market changes, this qualitative guidance does not necessarily represent short-term achievement based on last year's situation.

(2) Other revenue targets remain at 150-170 million US dollars, with a year-on-year growth rate of 46%. If we directly annualize Q1, it amounts to 167 million US dollars, just within the target range. However, Dolphin君 believes that with the effective progress of the CLARITY Act, there is a good chance this guidance could be exceeded.

6. Overview of Key Financial Metrics

Dolphin's Perspective

Q1 performance was akin to a "strengthened" version of last Q4 – sentiment in cryptocurrency trading further cooled, but Circle did not stop expanding into other scenarios, leading to even greater short-term profit pressure.

Although Coinbase and Circle operate in different parts of the industry chain, the impact during poor cryptocurrency market conditions varies (Circle's impact is relatively smaller). Additionally, there are issues of profit sharing between them, but in the short term, both follow a similar trading rhythm in terms of direction.

Therefore, in the previous quarter, under the dual pressures of weak cryptocurrency assets and unclear policy timelines, we focused on a price that emphasized safety. Currently, Circle has largely completed a reasonable recovery process. Future upside will depend on the expansion progress of stablecoins and USDC. In the short term, the effective progress of the CLARITY Act could provide some positive sentiment if there are no more systemic macro risks, thereby supporting the current valuation.

Below is the detailed analysis.

Circle is the issuer of the stablecoin USDC, and its main revenue comes from: (1) interest on reserve assets, which is tied to the scale of USDC in circulation and government bond rates; (2) other revenues, including Web3 software services for clients (SaaS subscriptions), CPN payments (fees based on payment amount/number of transactions), and service fees or gas fees collected through the Arc public blockchain (charged per transaction).

To mitigate the impact of interest rate cuts, Circle is actively expanding its other revenue streams. In 2025, it will mainly focus on promoting CPN payments and Arc public blockchain businesses. Currently, the proportion of other revenues has gradually approached 5%, and further growth is expected to accelerate in the future.

In terms of expenditures, Circle’s internal operational costs are primarily employee compensation, while external costs mainly consist of channel commissions and transaction fees, accounting for 60% of revenue (the majority going to Coinbase). After adding back depreciation and share-based compensation, the EBITDA profit margin is around 20%, lower than most fintech platforms. Therefore, alongside ecosystem expansion, expectations of rising commission costs have also raised concerns among some investors regarding Circle's short-term profitability.

From a medium- to long-term perspective, the importance of ecosystem expansion outweighs other factors. Currently, USDC ranks second in market share within the stablecoin space. Compared to USDT, its primary advantage lies in compliance. Once the CLARITY Act is implemented, USDC is expected to continue showcasing its “relative” advantage, attracting more institutional capital allocations.

In Q1, USDC's average circulation was $75.2 billion, a decrease quarter-over-quarter, but rebounded to $77 billion by the end of the quarter, up 2% compared to the previous quarter. During this period, $73 billion worth of coins were minted, with $72 billion redeemed, resulting in a significant slowdown in net issuance compared to Q3. According to Coinmarketcap, USDC’s circulating balance rapidly declined in January amid a panic sell-off in crypto assets, only beginning to recover in early February.

1. USDC External Market Share

Within the overall stablecoin market, USDC maintained a steady 28% market share quarter-over-quarter. However, compared to its closest competitor, USDT, USDC has not demonstrated a sustained competitive edge.

2. Internal Channel Competition within USDC

The proportion of USDC held internally by Circle continues to increase, reaching 18%.

According to Coinbase's Q1 earnings report, its share of USDC circulation has increased to 25% quarter-over-quarter, showing a continued trend of active retention compared to the previous quarter.

Another core indicator reflecting ecosystem growth - the number of effective digital walletsBy the end of Q1, the number of digital wallets MeWs (on-chain wallets holding more than $10 worth of cryptocurrency) reached 7.2 million, with a net increase of 400,000 from the previous quarter, likely due to the pressure on the crypto market continuing to slow down.

As 95% of Circle’s revenue comes from interest income on reserve assets, which is essentially public data, the main area for potential surprises lies in other income, which again exceeded expectations this quarter.

Specifically, other income mainly includes token issuance income, trading, custody, Web3 API suite, tokenized fund USYC, and fees from CPN launched in April last year (fixed access fee + settlement/audit fee per transaction, Arc chain gas fee, etc.).

Other income in Q1 was $42 million, up 13% quarter-over-quarter, but the growth slowed compared to the impressive results of the previous quarter. Meanwhile, the company maintained its guidance for full-year other income at $150-170 million, which doesn’t seem too optimistic based on the current quarter-on-quarter trend. Dolphin believes that if USDC expands normally, there may still be room for further beats.

The majority of revenue is affected by the pace of USDC expansion and the current interest rate environment. In Q1, the average scale of USDC grew by 70% year-over-year, while interest rates dropped to 3.5%, down 64 basis points year-over-year. As a result, the growth rate of reserve interest income slowed sharply to 17%.

However, expectations for further interest rate cuts have essentially fallen to zero. If the scale grows as expected in the next three quarters (QoQ above 5%) under stable interest rates, there is still hope to maintain 5-10% growth despite the pressure from lower year-over-year rates.

Gross margin in Q1 increased by 130 basis points to 41.4%. Circle continues to alleviate channel revenue-sharing pressures by increasing its self-held USDC share. Additionally, high-margin businesses like software and payment infrastructure services contributed to faster-growing other revenues, raising their income contribution ratio this quarter.

Although revenue growth slowed under pressure in Q1, all expense items remained strong, leading to an adjusted EBITDA of $133 million and a profit margin of 19.2%, up 50 basis points quarter-over-quarter.

The company’s guidance indicates that its full-year costs and operating expenses (excluding SBC and depreciation and amortization) for 2026 will remain unchanged at 570-585 million, representing a year-over-year increase of 10%, which is below market expectations.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1