The S&P 500 has risen for seven consecutive weeks—should you chase the rally or take profits?

Global Weekly Review | US job market shows resilience, China’s foreign trade achieves 'stable volume and quality improvement', consumption sees rational recovery

On the macroeconomic front

United States: The labor market remains resilient, manufacturing expansion faces obstacles, and the Federal Reserve maintains a wait-and-see policy.

Last week, the US core macro showed characteristics of both employment resilience and manufacturing divergence, with the Federal Reserve's wait-and-see stance unchanged.In terms of employment, 115,000 new non-farm jobs were added in April, surpassing market expectations, with the unemployment rate remaining at a low 4.3%.The labor market shows ample resilience, but the labor participation rate is declining, and there are structural differences in employment. The proportion of permanent unemployment has decreased, and while year-on-year wage growth has moderately rebounded, subsequent increases are limited, and real household purchasing power may be eroded by inflation.In terms of manufacturing, the ISM Manufacturing PMI for April remained at an expansion level of 52.7, unchanged from the previous month, but the input price index hit a four-year high.The employment index contracted for the 15th consecutive month, combined with supply chain disruptions caused by Middle East conflicts, manufacturers face dual pressures of high costs and shrinking workforce, resulting in weaker-than-expected expansion. Regarding Federal Reserve policy, influenced by uncertainties in the Middle East situation, inflationary pressures, and the state of the labor market, the thresholds for both interest rate cuts and hikes within the year have increased.It is expected that a wait-and-see approach will be maintained in the short term, and attention should be paid to policy statements after Wash's succession.。

China: Foreign trade achieved 'stable volume and quality improvement', consumption rationally recovered, and overall economic resilience was highlighted.

The core macro focus in China is on foreign trade and consumption performance, showing a strong growth in foreign trade and a rational recovery in consumption.In terms of foreign trade, the total value of goods trade imports and exports in the first four months increased by 14.9% year-on-year, with April's imports and exports increasing by 14.2% year-on-year.Import growth continued to outpace exports, leading to an expansion of the trade surplus; various trade methods worked together effectively, with bonded logistics and processing trade showing significant growth. The pattern of diversified trading partners continued to improve, with machinery and electronic products leading in exports.Private, foreign-invested, and state-owned enterprises all achieved relatively fast growth in imports and exports.Demonstrating the resilience of the supply chain and the success of high-quality development.In terms of consumption, the number of domestic tourists during the May Day holiday increased by 3.6% year-on-year.Total tourism spending grew by 2.9% year-on-year, but per capita spending was slightly lower than the same period last year, reflecting more cautious and rational consumer behavior. Combined with March’s weaker-than-expected growth in total retail sales of consumer goods, the recovery in consumption still needs sustained efforts.

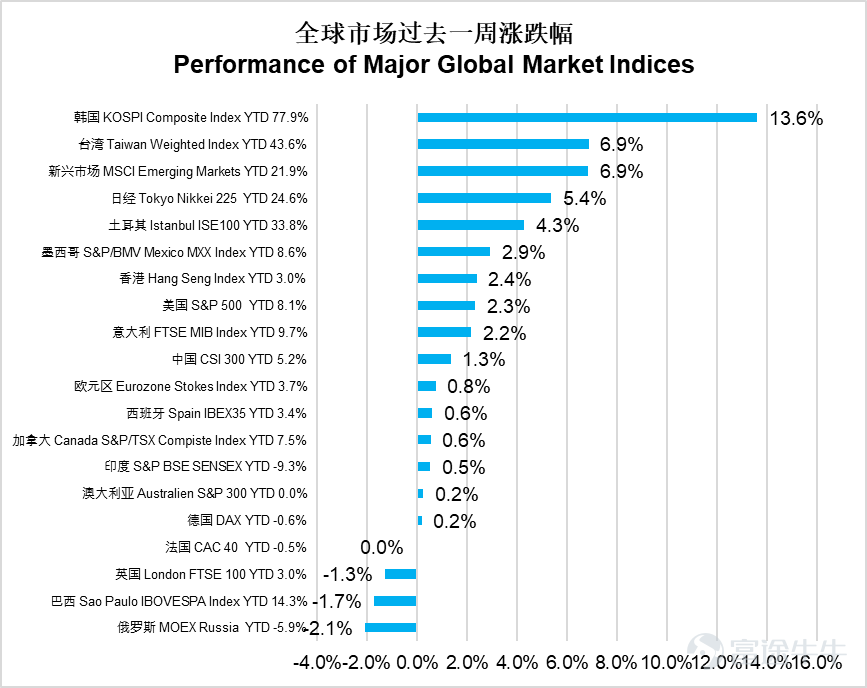

In the equity market,

global markets generally rose last week, with South Korea’s KOSPI surging 13.6%, leading global markets.Taiwan’s weighted index and the MSCI Emerging Markets both rose by 6.9%, while Japan’s Nikkei 225 increased by 5.4%. Emerging markets as a whole surged by 6.9%, the Hang Seng Index rose by 2.4%, and the CSI 300 climbed by 1.3%.Russia's MOEX fell by 2.1%, Brazil's IBOVESPA dropped by 1.7%, and the UK's FTSE 100 declined by 1.3%,becoming one of the few markets that ended lower. The US S&P 500 rose by 2.3%. Overall, emerging markets in Asia performed particularly well.

The US information technology sector surged by 7.0%, making it the best-performing sector, followed by communication services which rose by 1.9%, and consumer discretionary gaining 1.8%.Materials increased by 0.6%, industrials grew by 0.2%, and real estate edged up by 0.1%. However, the energy sector plummeted by 5.4%, utilities fell by 4.0%, financials dropped by 1.4%, healthcare declined by 1.2%, and consumer staples slightly decreased by 0.2%.The market exhibited an extreme divergence pattern with information technology leading gains and energy and utilities suffering significant losses.

Hong Kong-listed conglomerates soared by 9.5%, showing the strongest performance, while the real estate and construction sector and materials industry both rose by 7.5%,non-essential consumption increased by 6.2%. The Hang Seng Tech Index climbed by 4.8%, industrials gained 4.2%, and the information technology sector rose by 3.4%. Telecommunications advanced by 1.7%, utilities increased by 1.0%, financials grew by 0.8%, healthcare improved by 0.4%, and essential consumption edged up by 0.3%.However, the energy sector plunged by 8.8%, becoming the only sector that fell. The market showed a pattern where conglomerates and real estate led the gains while energy was the sole decliner.

In terms of the bond market,

Global bond markets rebounded somewhat over the past week, with the global composite index rising by 0.36%, and the US composite index increasing by 0.26%,US investment-grade corporate bonds climbed by 0.38%, and high-yield corporate bonds rose by 0.05%. The emerging markets USD bond composite index increased by 0.41%, and the Chinese offshore USD credit bond index advanced by 0.22%.

In terms of interest rates, the yield curve for US Treasuries has flattened further compared to last week.The 2-year US Treasury yield rose by 1 basis point to 3.88%, while the 10-year US Treasury yield fell by 2 basis points to 4.35%.

Market Outlook

– The US-Iran ceasefire negotiations have achieved phased progress, with both the S&P 500 and Nasdaq reaching new all-time highs.

The biggest variable in the market this week is the phased progress in the US-Iran ceasefire negotiations. Despite continued military friction between the two sides in the Strait of Hormuz,the emergence of a framework for a 14-point Memorandum of Understanding (MoU), Iran's substantive arrangement of designating two shipping lanes, and both sides expressing willingness to negotiate,marks the transition from 'military confrontation' to 'conditional engagement.' As a result, Brent crude oil fell from $114 to near $101 this week, retreating more than $25 from its historical peak of $126 reached on April 30. The decline in oil prices significantly boosted market risk appetite. $S&P 500 Index (.SPX.US)$and $Nasdaq (NDAQ.US)$Both indices hit new record highs, achieving a sixth consecutive weekly gain.

However, it is important to note that current asset prices have already priced in a certain degree of the 'ceasefire realization' scenario to some extent. The US-Iran MoU has yet to be formally signed, and the three core issues—nuclear concerns, sanctions relief, and strait security—remain unresolved, leaving the upcoming 30-day negotiation period full of uncertainty. This week’s exchange of fire when a US destroyer crossed the strait indicates that any military friction before a formal agreement could trigger an impulsive rebound in oil prices.Investors should remain cautious about the potential pullback risks after the 'negotiation benefits are fully priced in.'

Moreover, the Q1 earnings reports of US stocks continue to exceed expectations. About 84% of the companies in the S&P 500 index that have disclosed results reported earnings above expectations, with overall profit growth reaching 27.1%, the highest since Q4 2021.The technology sector has been particularly impressive, with the semiconductor and memory sectors experiencing significant gains driven by catalysts such as the Apple-Intel collaboration news and ongoing validation of AI computing power demand.The market is transitioning from 'telling Capex stories' to a phase where 'cloud revenue, ASIC orders, and advanced manufacturing' are being simultaneously validated. However, it's worth noting that current valuations of US stocks are at relatively high historical levels.The rise at the index level has mainly been driven by AI-related sectors, and the risk of sector rotation cannot be ignored.

In terms of interest rate policy, stronger-than-expected non-farm payroll data has further dispelled market expectations for rate cuts this year, with half of analysts predicting that the Fed will not cut rates in 2023.If oil prices rise again due to repeated tensions in the Strait, the risk of inflation will further strengthen the expectation of 'higher for longer,' at which point high-valuation tech stocks will face headwinds from rising rates.

Key economic data and events this week

China will release April CPI and PPI data on Monday;

The US will release April CPI data on Tuesday;

The US will release April PPI data on Wednesday;

The US will release April retail sales data on Thursday.

Disclaimer: The issuer of this report is E Fund Asset Management (Hong Kong) Co., Ltd. This report does not constitute an invitation or recommendation to invest in fund units. Fund unit subscriptions can only be made using application forms accompanied by the fund prospectus. Investment involves risks; fund prices may rise or fall, and past performance is not indicative of future results. Before investing, investors should carefully read the fund prospectus (including the 'Risk Factors' section) to understand the investment risks related to the fund. This report may only be distributed in certain jurisdictions. In any jurisdiction where distributing such information or making any invitation or recommendation is prohibited, or where distributing this report or making an invitation or recommendation to any person would be illegal, this report does not constitute such distribution or invitation or recommendation. This document has been exempted from prior review and approval by the Hong Kong Securities and Futures Commission, and has not been reviewed by the SFC. SFC approval does not imply promotion or endorsement of the plan, nor does it guarantee its commercial merits or performance, nor does it indicate suitability for all investors, or endorsement of suitability for any particular investor or category of investors. All rights reserved © 2026. E Fund Asset Management (Hong Kong) Co., Ltd.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1