Behind Oracle's global layoff of 30,000 people, is it an AI bubble or AI replacement?

Li Ping/Author Lishi Business Review/Produced by

1

30,000 people globally fired via 'email dismissal'

Not long ago, the US tech giant Oracle launched a surprise large-scale layoff worldwide, with an estimated total of 20,000 to 30,000 employees affected, accounting for nearly 18% of Oracle's global workforce of 162,000. This has become one of the largest layoffs in the global tech industry since the beginning of 2026.

According to feedback from multiple Oracle employees on social media platforms, they were suddenly cut off from access to the company’s internal systems at around 3 a.m. that day and received termination notices via email. It is reported that this round of layoffs impacted several core departments, including Oracle Health, sales, and cloud services, covering major markets such as the US, India, and Europe. Among them, 12,000 employees in the Indian market alone were laid off, making it the hardest-hit area in this round of cuts.

For a long time, Oracle Corporation has been widely regarded as a Silicon Valley 'retirement factory' due to its stable work environment, slow pace, no overtime culture, and good benefits. However, this global mass layoff completely shattered that impression. Reportedly, Oracle's official explanation for the layoffs was extremely brief, stating only in the notice: 'After careful consideration of current business needs, we have decided to eliminate your position as part of a broader organizational restructuring. Therefore, today will be your last working day.'

At the same time the layoff emails were sent out en masse, the affected employees’ corporate email accounts, internal system access, and building entry permissions were immediately terminated without any prior communication, one-on-one discussions, or a transition period for handing over responsibilities. In terms of severance packages, Oracle offered four weeks of basic salary, plus an additional week’s pay for each year of service, capped at a maximum of 26 weeks.

As of now, Oracle has not made any public comments on this layoff event nor disclosed the exact number of layoffs. However, public opinion generally believes that since Oracle is heavily investing in AI data center construction, the main reason behind this round of layoffs is cost-cutting and efficiency enhancement, aiming to free up cash flow for its AI business by strictly controlling operational costs.

Additionally, as large language models (LLMs) increasingly demonstrate remarkable capabilities in understanding scientific literature and generating high-quality code, the latest advanced models such as Claude Opus 4.5 and GPT-5.2-Codex are now able to generate higher-quality code. Many software companies have started using these large models to produce program frameworks and simple logic, thereby reducing the number of mid-to-low-level programmer employees.

According to public reports, on February 27th Beijing time, fintech company Block suddenly announced it would lay off about half of its workforce. Regarding this, Jack Dorsey, co-founder and CEO of Block, stated that as 'smart tools' bring efficiency improvements, most companies will be forced to make similar structural adjustments within the next year; he simply chose 'to take this step in our own way, honestly, rather than eventually being forced into a passive response.'

Some analysts also believe that in order to concentrate resources on training smarter AI, Oracle did not hesitate to lay off standardized engineers, who have been highly sought after over the past decade, which can be seen as an indirect form of 'robot replacement.' In other words, the first wave of the AI revolution did not attack traditional fields but instead targeted IT industries characterized by asset-light businesses, even including those who once personally helped build this edifice.

2

Revenue growth and cost pressures

Based on the company's latest financial report data, Oracle is far from the stage of 'cutting off limbs to survive.' On the contrary, due to the rapid growth of businesses like cloud infrastructure, Oracle’s third-quarter financial results were quite impressive, with a substantial backlog of orders, and the fiscal year 2027 guidance exceeded market expectations.

According to Oracle's earnings report released on March 11, in the third quarter of fiscal year 2026 (ended February 28, 2026), Oracle achieved total revenue of $17.19 billion, a year-on-year increase of 22%, surpassing market expectations of $16.91 billion; net profit was $3.721 billion, a year-on-year increase of 26.5%. This marks the first time in fifteen years that Oracle has achieved both revenue and adjusted earnings growth of over 20% in a single quarter.

As the world’s largest enterprise software company, Oracle’s traditional strengths lie primarily in areas such as databases, tools, and application software. In recent years, Oracle has continued to invest heavily in AI infrastructure, accelerating its transformation into a cloud services giant to compete with industry leaders like Amazon AWS, Microsoft Azure, and Google Cloud GCP.

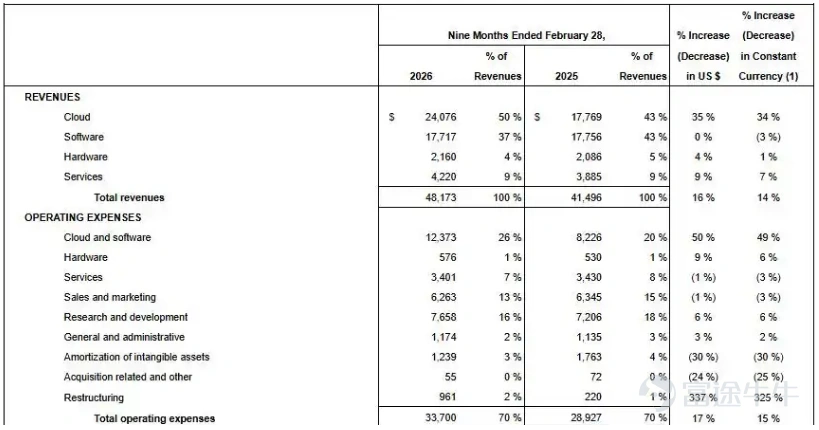

In terms of revenue composition, Oracle's main business is divided into four major segments: cloud business (Cloud), software business (Software), hardware business (Hardware), and services business (Services). The cloud business includes IaaS (Infrastructure as a Service) and SaaS (Software as a Service), which represent Oracle's fastest-growing business segment at present.

It is reported that IaaS is mainly provided through Oracle Cloud Infrastructure (OCI), including the company’s signature database cloud services and computing power rental business, while SaaS is mainly delivered through Oracle Cloud Applications (OCA), covering SaaS-based enterprise resource planning (ERP), customer relationship management (CRM), and other general management tools as well as some specialized tools for vertical industries.

In the third quarter of fiscal year 2026, Oracle's cloud business generated sales revenue of $8.9 billion, a year-on-year increase of 44%, accounting for 52% of total revenue. Among this, cloud infrastructure (IaaS) generated sales revenue of $4.9 billion, a year-on-year increase of 84%, becoming the key driver of rapid growth in cloud business revenue; SaaS business generated sales revenue of $4 billion, a year-on-year increase of 13%.

Aside from the cloud business, Oracle's other three business segments also achieved positive growth. Software revenue reached $6.119 billion, a year-on-year increase of 3%, accounting for 36% of total revenue; hardware revenue reached $714 million, a year-on-year increase of 2%; service revenue generated sales revenue of $1.443 billion, a year-on-year increase of 12%.

Oracle’s software (Software) business refers to traditional software operations where customers deploy and manage the software themselves. It mainly consists of software license sales and software support services, and was once the segment with the largest share of the company's revenue, at one point exceeding 60%.

Since fiscal year 2025, cloud business has gradually replaced traditional software business as Oracle’s largest source of revenue. Based on the latest financial data, cloud business now accounts for more than 50% of Oracle's revenue., marking Oracle’s successful transformation into a technology company centered around cloud services.

Notably, judging by Remaining Performance Obligations (RPO), Oracle’s future performance remains promising. According to the earnings report, in the third quarter of fiscal year 2026, Oracle signed new contracts worth over $29 billion, bringing the company’s Remaining Performance Obligations (RPO) to $553 billion, a year-on-year increase of 325%.

Moreover, in terms of future earnings guidance, Oracle expects its total revenue for the fourth quarter of fiscal year 2026 to increase by 19%-21% year-over-year in dollar terms, with cloud service revenue growing by 46%-50% year-over-year in dollar terms. Meanwhile, Oracle has maintained its guidance for total revenue of $670 billion and full-year capital expenditure of $500 billion for fiscal year 2026 unchanged, while raising its total revenue guidance for fiscal year 2027 to $900 billion, surpassing the market consensus range of $866-$867 billion.

Due to the quarterly financial results, remaining performance obligations, and earnings guidance all exceeding market expectations, Oracle's stock price surged over 9% on the day following the earnings release, but then fell into a downtrend. As of the close on April 7, Oracle’s latest market value was approximately $506.9 billion, having shrunk by nearly $500 billion from its historical high.

So why is Oracle, with $550 billion in orders, not favored by investors?

3

Concerns over circular financing

In September 2015, Oracle released its first-quarter financial report for fiscal year 2026, showing that as of August 2025, the company’s remaining performance obligations surged 359% to $455 billion, far exceeding the market consensus of $178 billion. Based on this calculation, Oracle’s order backlog already extends a decade into the future.

Spurred by this news, Oracle's share price once soared over 40% during intraday trading, with its market cap briefly approaching the $1 trillion mark. The company's founder, Larry Ellison, also briefly surpassed Elon Musk to become the world's richest person.

However, investors soon realized that almost all of Oracle's explosive growth in orders came from just one company: OpenAI. It was reported that OpenAI signed a five-year computing power procurement agreement with Oracle worth $300 billion, accounting for 94.6% of the new RPO (Remaining Performance Obligations) of $317 billion reported in Oracle’s Q1 2026 earnings.

It should be noted that for the computing power purchaser OpenAI, the $300 billion five-year mega-order requires an annual expenditure of $60 billion. However, OpenAI’s annualized revenue is only $10 billion, with losses amounting to $5 billion. Clearly, OpenAI’s current revenue-generating ability is far from sufficient to cover the annual $60 billion expenditure brought by the agreement.

For Oracle, concentrating future revenue too heavily on this yet unprofitable star startup seems unwise. According to the agreement, Oracle must provide OpenAI with up to 4.5 gigawatts of power capacity, equivalent to the total output of two Hoover Dams, or enough to meet the annual electricity needs of about 4 million American households.

Additionally, Oracle will need to borrow heavily to procure AI chips, with the hidden risks being self-evident. Analysts believe Oracle may need to borrow $100 billion to complete the AI infrastructure investment required for the $300 billion order. Clearly, if OpenAI’s operations or external financing progress falls short of expectations, the risks involved are obvious.

As a result, the focus of the secondary market began to shift from the previous massive orders to OpenAI's actual fulfillment capabilities, as well as the capital expenditure pressures and cash flow performance faced by Oracle. Against this backdrop, Oracle's stock price started to reverse from gains to losses.

The subsequently released Q2 earnings report (corresponding to September to November 2025) showed that as of the end of November 2025, Oracle’s backlog orders had reached $523 billion, an increase of $68 billion year-on-year. However, in terms of operating cash flow, Oracle’s free cash flow for the quarter was negative $10 billion, with capital expenditures (CapEx) reaching $12 billion, significantly exceeding market expectations of $3.7 billion.

It is not difficult to see that, based on the metric of free cash flow, Oracle has fallen into a state of 'expenditures exceeding income,' indicating that the concerns previously held by the secondary market are becoming a reality. Therefore, following the release of the Q2 earnings report, Oracle’s stock price plummeted by 11%, with intraday losses exceeding 15% at one point.

Based on the latest Q3 earnings data, Oracle’s free cash flow for the quarter was negative $11 billion, worsening from the negative $10 billion in the second fiscal quarter. The company’s capital expenditures for the quarter were as high as $18.6 billion, far surpassing analyst expectations of $14 billion. Clearly, this indicates that the concerns previously held by the secondary market still persist, which is one of the main reasons Oracle’s stock price resumed its downward trend after the release of the Q3 earnings report. Behind investors rushing to exit, the secondary market’s concern over an 'AI bubble' has become the biggest bearish factor weighing on Oracle’s stock price.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment