A key period of negotiations, will military conflict erupt again between the US and Iran?

The extension of the ceasefire failed to narrow differences, as the deadlock in US-Iran negotiations tests market expectations

Middle East Conflict Update: US-Iran talks stall as Iran refuses to come to the negotiating table; ceasefire extension deepens divisions

With the ceasefire deadline looming, global attention is on whether the US and Iran can engage in a second round of negotiations, but there have been notable developments. Trump initially stated that he would not extend the ceasefire if it expired, but later announced a unilateral extension of the ceasefire after receiving messages from mediators and citing internal disagreements within Iran. The blockade of Iranian ports will continue until Iran presents a concrete and unified solution.

On the other hand, according to Iran’s semi-official Tasnim News Agency, Iran has refused to attend the second round of talks originally scheduled for the evening of April 22 in Islamabad, Pakistan, accusing the US of lacking sincerity and deeming further negotiations meaningless. As a result, the US delegation led by Vice President Vance canceled its trip to Pakistan.

Short-term Outlook: Ongoing blockade of the strait leaves localized risks still present

The current situation, against the backdrop of an extended ceasefire but ongoing blockade of the strait, shows significant back-and-forth in the US-Iran negotiation process; this tumultuous process still falls within the scope of the negotiation model we previously anticipated. In the short term, regardless of the reasons for extending the ceasefire, it at least provides some breathing space; in the market, the Asian opening (on 4/22) rebounded after a brief dip this morning, showing that investors are gradually becoming desensitized to the lack of progress in negotiations and remain in a wait-and-see phase overall.

It is necessary to closely observe whether there will be further contact or indirect negotiations between the two sides during the extended ceasefire period. However, given the continued hardline stance maintained by both parties, the timeline for achieving partial, temporary interest exchanges is being prolonged as they wait to return to the negotiating table. Once the mutual trust mechanism undergoes significant changes, localized risks will increase.

Long-term outlook: Negotiations continue to drag on, prolonged timelines may weigh on long-term economic recovery momentum

Although the extension of the ceasefire has injected some buffer space into the current situation, which is relatively positive development, the foundation of mutual trust between the two sides remains fragile, and core differences have not been truly resolved. Both parties tend to pursue maximum results in their key interests and are unwilling to accept obvious compromises, a dynamic that can easily deepen divisions, meaning long-term peace will require more time and multiple rounds of negotiations to gradually achieve.

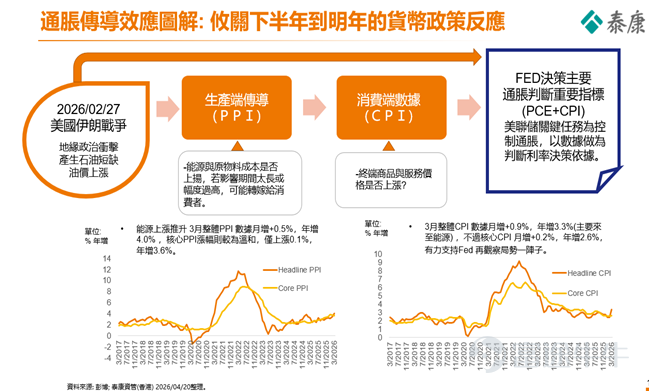

More importantly, once hostilities are brought under phased control, market focus will gradually shift from 'negotiation progress' to the actual impact of post-war economic data. As March economic data has gradually been released, whether oil prices can stabilize and fall, whether the transmission from the production side (PPI) to the consumer side (CPI) is controllable, and the extent of lag in transmitted data will directly affect the Federal Reserve’s subsequent monetary policy path. If negotiations and blockades persist for too long, it will disrupt post-war reconstruction and regional stability restoration, adding mid-to-long term uncertainty.

Additionally, from the perspective of the critical timeline, the US is facing pressure from the War Powers Resolution (WPR).

According to legal requirements, military actions without congressional approval cannot exceed 60 days but can be extended to 90 days (including withdrawal periods). Based on this calculation, the end of April to May will be an important time node for whether US troops will withdraw. However, considering Trump’s past governing style, White House staff will likely seek other legal tools or pragmatic interpretations to bypass restrictions and maintain a military presence.

Investment Perspective: Leverage the advantage of short-term bonds, focus on the long term, and stabilize your portfolio.

In response to the rapidly changing situation in the Middle East, investors should maintain a long-term strategic asset allocation mindset while moderately capitalizing on opportunities brought by short-term market fluctuations. They should avoid excessively chasing or betting on the outcome of a single event, prioritizing stable positioning. Previous analysis has pointed out that the recent pressure on the bond market is mainly due to rising oil prices pushing up inflation expectations. However, as the market quickly adjusts, we observe that the 1-year forward OIS rate one year from now (1Y1Y OIS) has risen further, approaching the upper limit of the federal funds rate benchmark. This provides technical support for front-end bonds and shows that market concerns about US interest rate hikes have eased somewhat.

In contrast, the European and UK central banks have shifted to a more hawkish tone on rate hikes in March, while the Federal Reserve, burdened with the dual mandate of employment and inflation control, has adopted a more cautious approach to policy adjustments, offering greater flexibility to respond to economic data gradually rather than rushing to tighten. Notably, yesterday (April 21), the Senate Banking Committee held the confirmation hearing for Kevin Warsh, the next Federal Reserve Chair nominee. Warsh reiterated at the hearing that controlling inflation remains the Fed's top priority, while emphasizing the maintenance of the Fed’s policy independence. His overall stance leaned towards steady neutrality. Historically, during the early days of a new Fed Chair taking office, average U.S. Treasury yields have tended to rise. Therefore, how smoothly the new Chair’s policy direction and market communication proceed will be one of the key variables for the market.

In summary, given the uncertainties surrounding Middle Eastern geopolitical risks and potential shifts in Federal Reserve personnel policies, we recommend that investors continue to position short-term bonds as a core hedge: effectively managing interest rate volatility and geopolitical risks on the one hand, while maintaining relatively stable returns as a buffer and foundational element for overall asset allocation and long-term planning.

Source: Taikang Asset Management (Hong Kong), compiled on 2026/04/20.

$Taikang Kaitai Monthly Stable Income Fund MDis (HK0000965985.MF)$$Taikang Kaitai Monthly Stable Income Fund (HK0000965977.MF)$$Taikang Kaitai Hong Kong Dollar Money Market Fund (HK0000772993.MF)$$Taikang Kaitai Hong Kong Dollar Money Market Fund (HK0000772993.MF)$$Taikang Kaitai Monthly Stable Income Fund (HK0000965993.MF)$$Taikang Kaitai Overseas Short Tenor Bond Fund (HK0000369188.MF)$$Taikang Kaitai Overseas Short Tenor Bond Fund (HK0000369196.MF)$$Taikang Kaitai US Dollar Money Market Fund (HK0000857273.MF)$$Taikang Kaitai Overseas Short Tenor Bond Fund (HK0000369196.MF)$

Disclaimer

Unless otherwise stated, all information contained in this document is current as of the publication date.

The above content is for reference purposes only and is intended for general review by clients of Taikang Asset Management (Hong Kong) Limited ('Taikang Hong Kong'). It does not consider any specific investment objectives, financial situation, or particular needs of any specific recipient and should not be considered as advice or an offer or solicitation to buy any investment products.

Any research or analysis used in the preparation of this document was acquired by Taikang Hong Kong for its own use and purposes, and is sourced from what is considered reliable as of the date of this document. However, no representation or warranty is made regarding the accuracy or completeness of information originating from third parties.

Any forecasts or other forward-looking statements regarding future events or performance may not be indicative and could differ from actual events or results. Any opinions, estimates, or predictions may be changed at any time without prior notice. Taikang Hong Kong shall not be liable for any losses arising from the use of this document.

The views, recommendations, advice, and opinions expressed in this document do not necessarily reflect the position of Taikang Hong Kong and may be changed without notice. Taikang Hong Kong also has no obligation to provide any updates regarding such information or opinions.

This document may not be reproduced, distributed, or transmitted to anyone without the prior written approval of Taikang Hong Kong. This document and the information contained herein may not be distributed or published in any jurisdiction where such distribution or publication is prohibited. If you are not the intended recipient of this document, please refrain from reading it further and destroy it immediately.

Investment involves risks. Past performance is not indicative of future results.

This document is issued by Taikang Hong Kong and has not been reviewed by the Securities and Futures Commission. You should consult your investment advisor before making any investment decision.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment