AI Power Crunch Breakthrough: Who Can Replace Heavy Gas Turbines?

(This article was authored by Dolphin Research, and published by Titanium Media with authorization)

By Dolphin Research

The U.S. power shortage is not a short-term supply and demand imbalance, but rather a structural contradiction formed by the explosive growth of AI computing power and long-term lagging energy and grid infrastructure. On the power generation side, heavy-duty gas turbines have become the theoretical 'optimal solution' for AIDC data centers due to their cost-effectiveness and power supply stability. However, the production capacities of the world’s 'big three' gas turbine manufacturers are already fully booked until 2028.

This research piece by Dolphin Intelligence will focus on:

1) The gas turbine industry chain: Where are the high-value segments?

2) The bottleneck of heavy-duty gas turbines restricting computing power: How are industry giants breaking through?

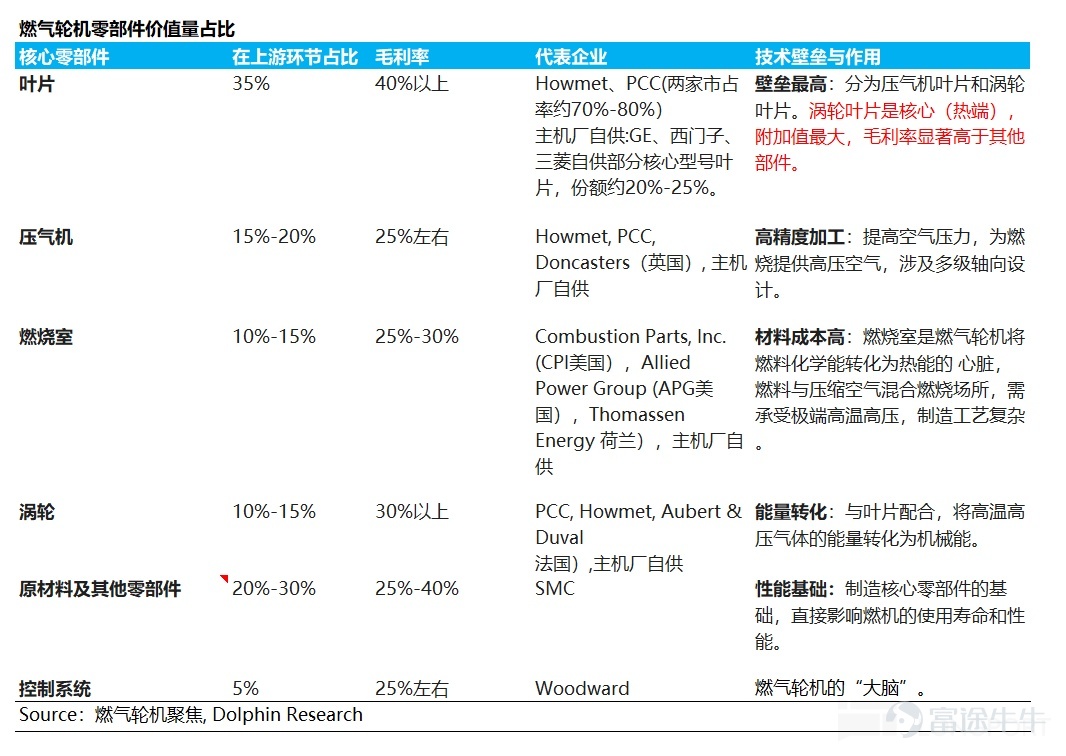

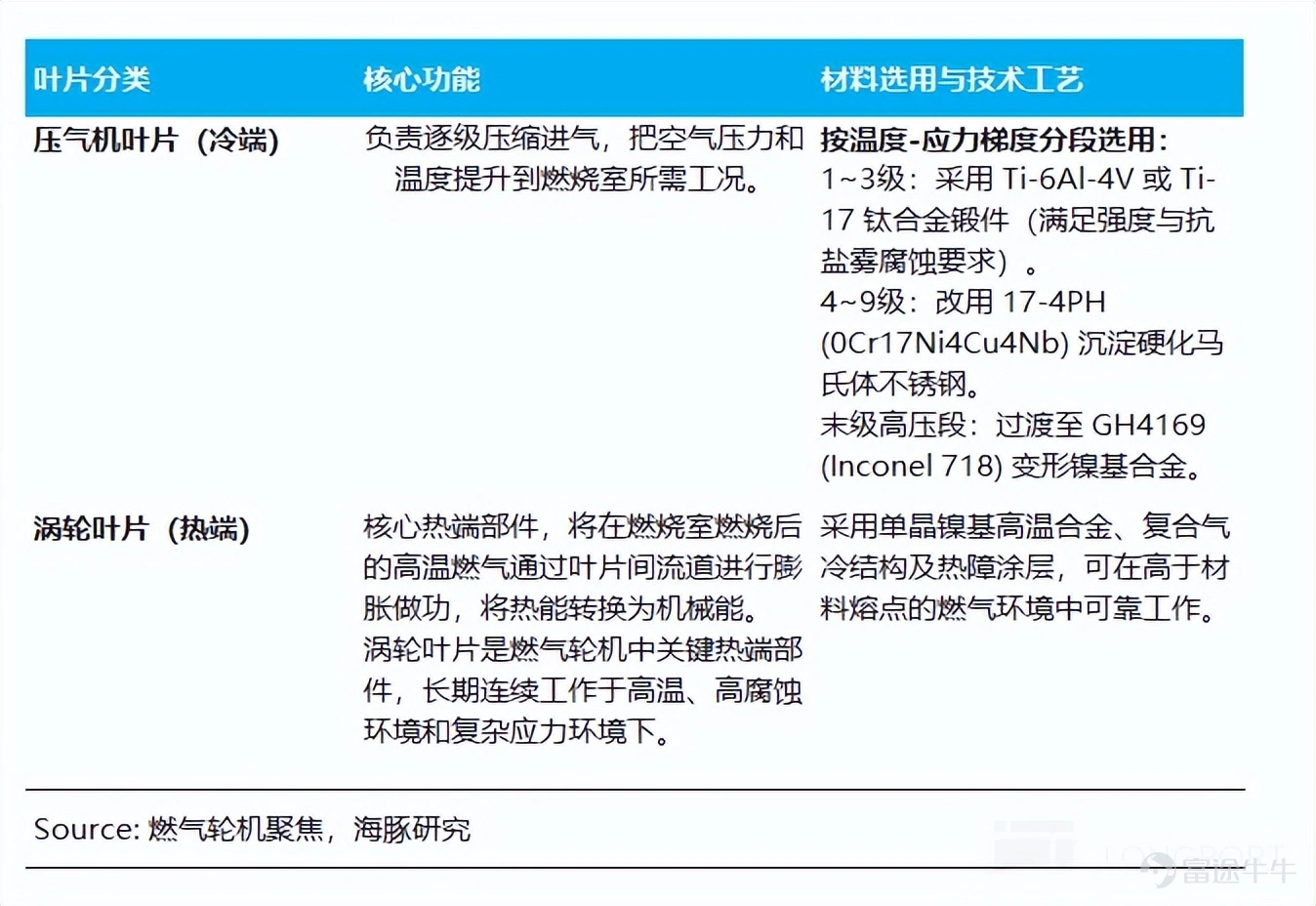

1) Turbine blades: The 'heart' of the gas turbine

Looking at the entire gas turbine industry chain, turbine blades are indisputably the 'heart' and 'bottleneck.' As the component with the highest technical barriers, largest value, and tightest supply in the whole machine, their performance directly determines the efficiency and power output of the gas turbine, while their scarce production capacity directly caps the delivery limits of downstream units.

As Elon Musk recently pointed out: 'Due to the unbearable 12-18 month grid connection delays in the US, xAI turned to purchasing natural gas turbines, only to find that orders were already backlogged until 2030. The real limiting factor is the vanes and blades inside the turbines because casting these blades is an extremely specialized and professional process.'

In the overall cost structure of a gas turbine, the value of blades (especially turbine blades) accounts for as much as approximately 35%, significantly higher than other components such as compressors, combustion chambers, and control systems. It is also the segment in the entire industry chain with both high added value and high gross margins (turbine blade gross margins have consistently remained above 40%).

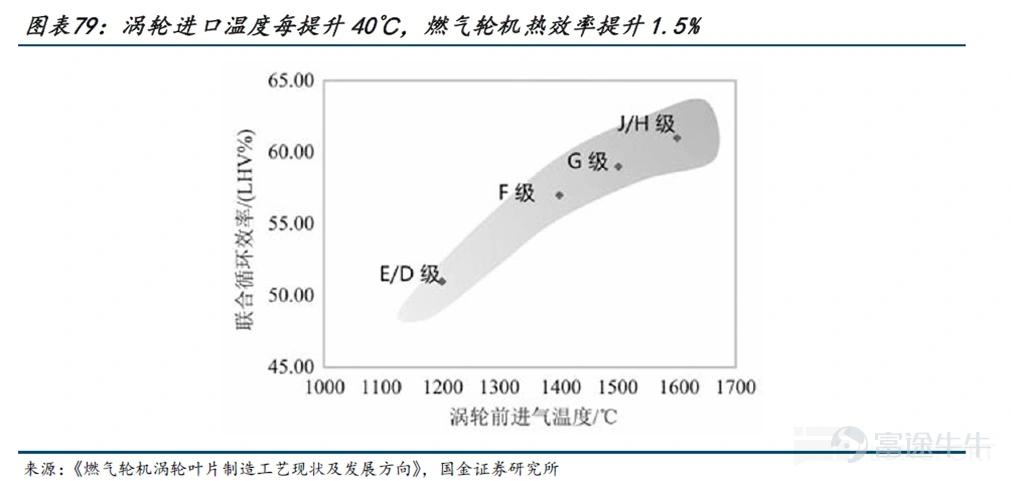

Turbine Inlet Temperature (TIT) is the core parameter for measuring intergenerational gas turbine performance. Theoretically, for every 40°C increase in TIT, the thermal efficiency of the gas turbine improves by about 1.5%, and output power increases by approximately 10%. The temperature resistance limit of turbine blades directly sets the physical ceiling for TIT and is key to achieving breakthroughs in gas turbine performance.

2) Hot-end turbine blades have extremely high barriers to entry:

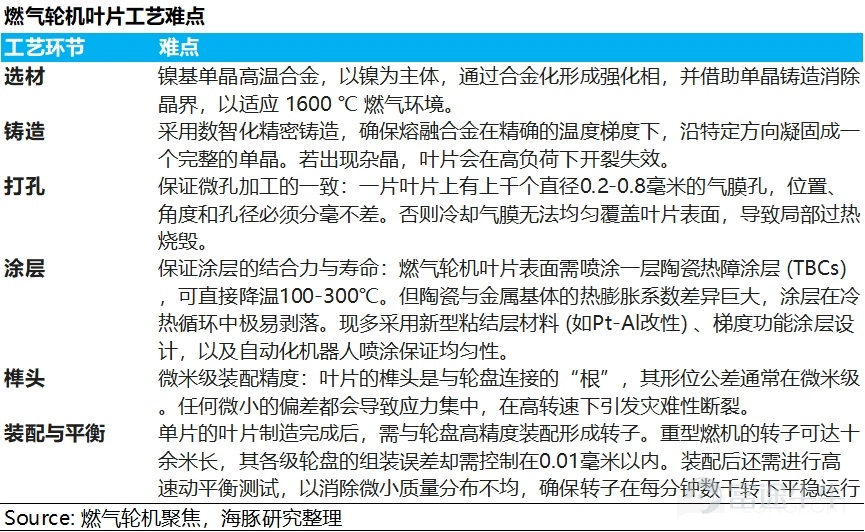

Gas turbine blades are divided into cold-end (compressor blades) and hot-end (turbine blades).The most critical turbine bladesare responsible for converting the expansion work of high-temperature gas after combustion into mechanical energy. They must operate stably for tens of thousands of hours in extreme conditions: over 1,400°C (close to or even exceeding the melting point of nickel-based alloys), bearing centrifugal forces tens of thousands of times their own weight, and under highly corrosive environments.This creates an extremely high barrier to entry:

① Material breakthroughs at their limits:Single-crystal superalloys must be used, with precise additions of expensive rare elements such as rhenium and hafnium to enhance high-temperature resistance and creep performance. Currently, only a handful of companies globally possess core technologies for single-crystal high-temperature components and have effective production capacity.

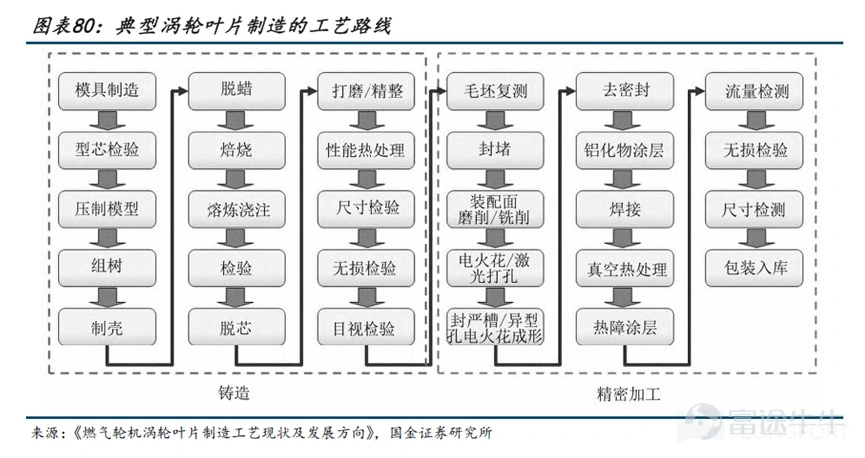

② Pinnacle challenges in manufacturing processes:The manufacturing process involves more than ten extremely difficult steps, including vacuum melting, single-crystal directional solidification, precision forming of complex hollow cooling channels, laser processing of film cooling holes, and thermal barrier coating (TBC) spraying. Tolerances and consistency requirements reach micron levels, making yield control a significant challenge.

In addition, to withstand extreme centrifugal forces, the blades must feature advanced aerodynamic designs. The wax mold manufacturing and assembly stages still heavily rely on skilled senior technicians.

3) Long cycles of trial and error and certification:From the development of base materials to passing tens of thousands of hours of rigorous grid testing by major manufacturers, the certification cycle often takes years, with extremely high trial-and-error costs.

3) Extremely high technological, capital, and time barriers have led to a highly concentrated global market for high-end turbine blades, with rigid supply constraints.

Currently, there are very few core players in the global turbine blade market, which has long been dominated by two American giants: PCC (Precision Castparts Corp) and Howmet Aerospace. Together, they account for approximately 70%-80% of the global high-end turbine blade market (especially single-crystal/directionally solidified blades), serving as the absolute main suppliers to gas turbine manufacturers such as GE Vernova, Siemens, and Mitsubishi Heavy Industries.

Facing the current gas turbine market driven by demand from AI and data centers, these two leading blade manufacturers show insufficient willingness and actual capacity to expand production. This 'supply rigidity' is primarily constrained by the following three structural factors:

1) The 'structural encroachment' of aviation engine demand on gas turbine production capacity

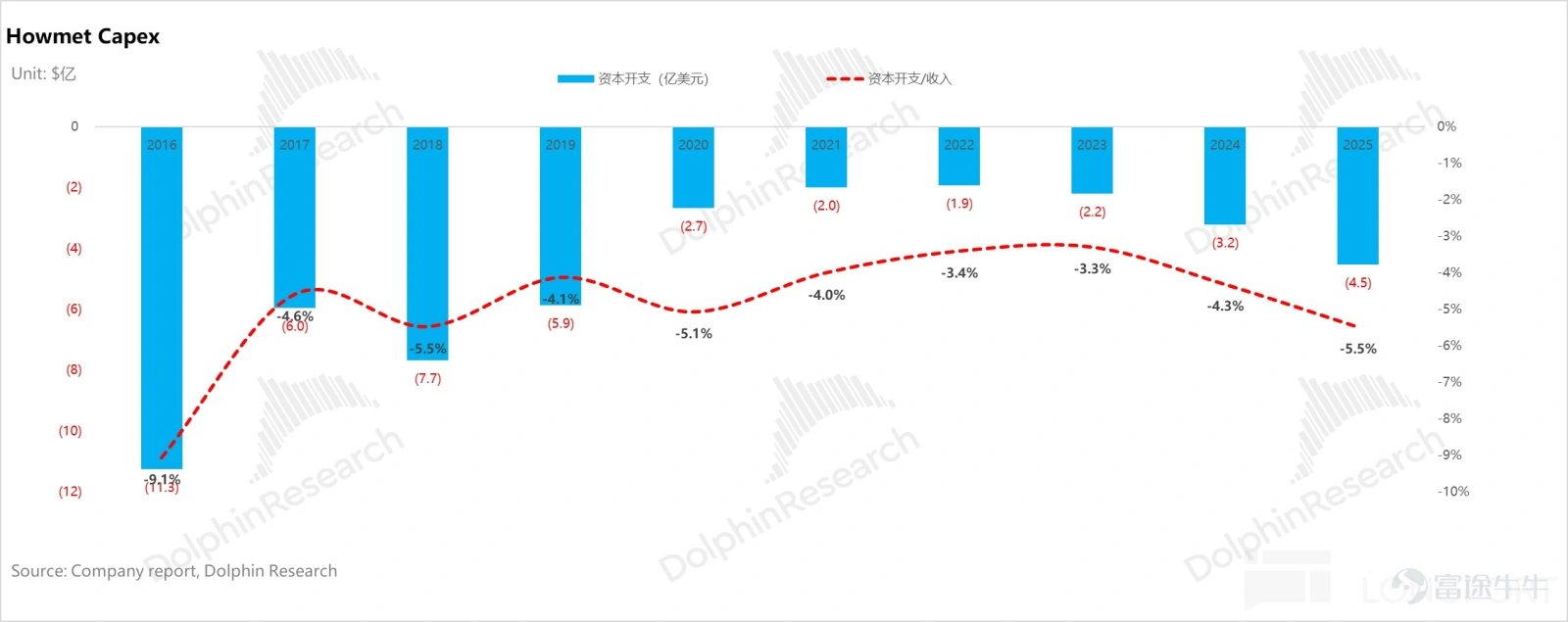

In response to aggressive expansion plans by downstream gas turbine manufacturers, upstream blade giants (PCC, HWM) remain highly conservative in capital expenditures (for instance, HWM's capital expenditure as a percentage of total revenue has consistently hovered around 5%).

This is not short-sightedness but a rational decision under their asset-heavy business model: idle core equipment (such as single-crystal furnaces), priced at millions of dollars per unit and with limited use, would incur substantial depreciation losses. To mitigate the risk of the 'bullwhip effect' caused by demand fluctuations, they prefer to sacrifice some growth rather than aggressively expand production.

Given the nearly fixed total production capacity pool, high-value orders will inevitably crowd out low-value orders. Aviation engine blades are comprehensively 'encroaching' on the production capacity for gas turbine blades, due to fundamental differences in their comparative advantages:

Certainty of the business model:Aero-engine blades are often tied to long-term agreements of 10 to 15 years (such as for Airbus, Boeing, and military aircraft), providing factories with a stable source of revenue that can weather business cycles. In contrast, long-term agreements for gas turbine blades typically do not exceed seven years and are more susceptible to energy policies and project investment cycles, resulting in higher volatility risks.

Aero-engine blades benefit from greater economies of scale and higher yields.The smaller size of aero-engine blades means a single model corresponds to thousands of aircraft globally, with batch production orders reaching hundreds of thousands of units, enabling significant cost amortization of high R&D and mold expenses.

Additionally, the smaller blades heat more uniformly during casting, leading to a significantly lower defect rate compared to larger gas turbine blades. Meanwhile, heavy-duty gas turbine blades are massive, and even minor flaws in the furnace can result in total scrapping, creating extremely high sunk costs.

Therefore, for PCC and HWM, allocating production capacity to aero-engine blades, which feature 'long-term agreements, large volumes, and high profitability,' is a safer and more profitable business decision than producing gas turbine blades, which involve 'short-term contracts, small volumes, and higher scrap rates.'

In 2025, HWM's engine business segment generated $4.32 billion in revenue, reflecting a robust year-over-year growth of 15.6% (an increase of $585 million). Commercial and defense aero-engines accounted for 45% of the core growth, while the gas turbine sector contributed 32% of the growth, though primarily driven by price increases rather than substantial sales expansion, indirectly confirming the severe constraints on gas turbine production capacity.

During the same period, PCC’s revenue in 2025 increased by only 4.6% year-over-year, with overall revenue growth showing signs of deceleration.

Against the backdrop of a strong post-pandemic recovery in global commercial aviation and a significant rise in procurement budgets for military aviation equipment in Europe and the US, the high demand for aero-engines is expected to persist over the long term, making it unlikely to reverse the situation where gas turbine blade production takes a backseat in the short term.

Core equipment limitations lead to an extremely lengthy production expansion cycle.

The current bottleneck in blade production is not basic metal raw materials but the extreme shortage of advanced machine tools and specialized casting equipment.

The supply chain for core casting equipment used in high-end blades is extremely long. Taking directional/single-crystal vacuum induction melting furnaces as an example, the entire capacity ramp-up cycle lasts over 3.5 years, from placing custom orders with leading equipment manufacturers like Germany's ALD (with a delivery time of approximately 1.5 years), to cross-border shipping, production line installation and debugging, process parameter testing, and finally passing stringent original equipment manufacturer certifications to achieve mass production of qualified products.

Deep integration leads to decision-making delays

Gas turbine hot-end blades are highly customized components, with their aerodynamic design and material formulations deeply tied to specific models of original equipment manufacturers. The front-end development incurs extremely high sunk costs (with manufacturers needing to pay tens of millions in mold fees and provide long-term technical guidance).

Therefore, blade manufacturers' capacity expansion decisions heavily depend on clear demand guidance and long-term contract commitments provided by OEMs two to three years in advance. Before the surge in demand in 2024, global supply and demand were balanced, and blade factories did not receive 'recommendations' for large-scale capacity expansion, resulting in significant lags in capacity planning relative to current demand.

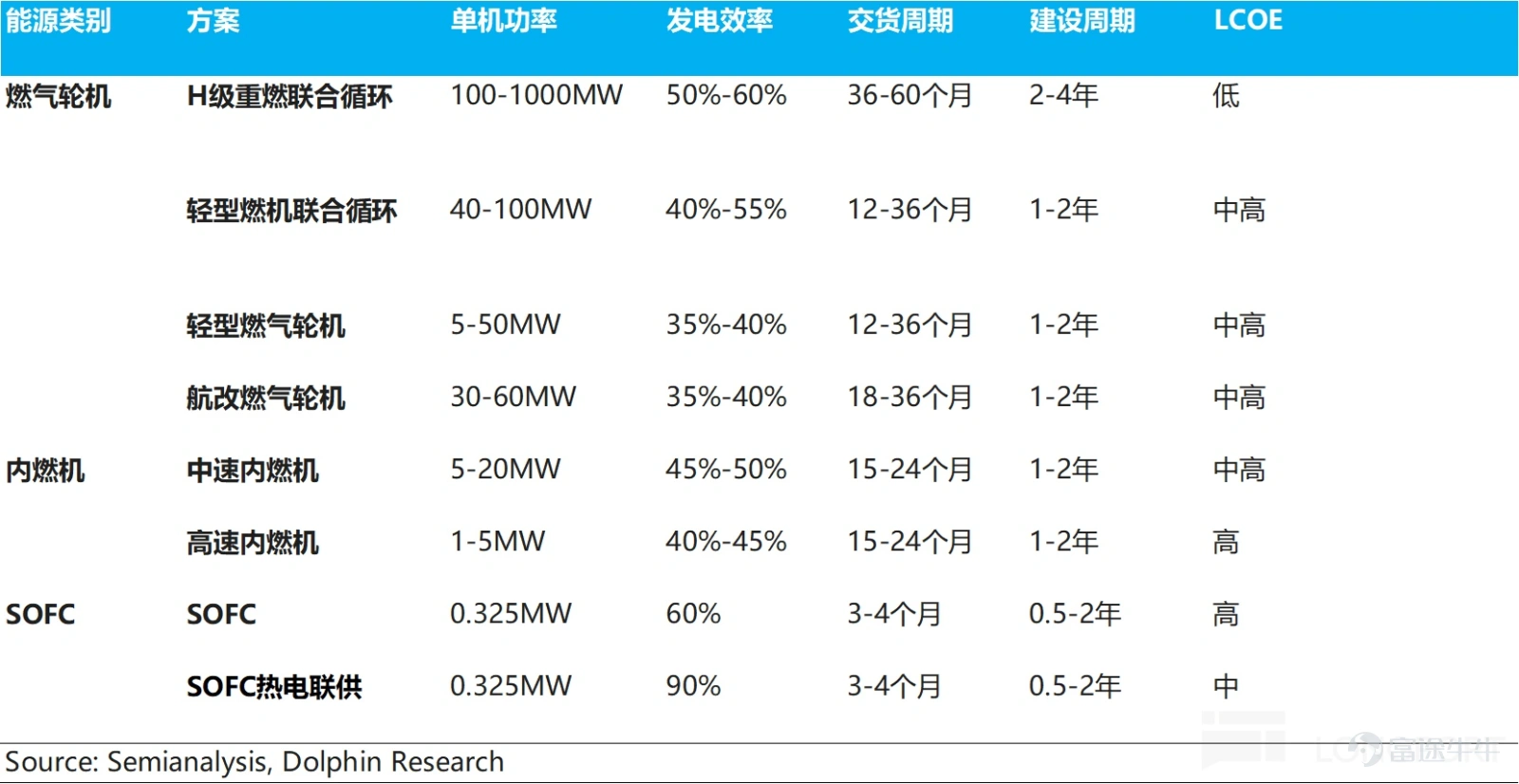

From the above, it is evident that the actual pace of expansion in the heavy-duty gas turbine industry is severely constrained by upstream core component capacity bottlenecks, particularly in turbine blades. Long-standing mismatches between leading manufacturers' orders and capacity present clear growth opportunities for alternative technologies with shorter delivery cycles, such as aeroderivative engines, light-duty gas turbines, gas internal combustion engines, and solid oxide fuel cells (SOFCs).

Amid saturated heavy-duty gas turbine orders and constrained capacity, there has been substantial spillover of urgent electricity needs for artificial intelligence data centers (AIDC), creating a clear substitution gradient:

In terms of delivery and construction timelines: Heavy-duty combined cycle gas turbines (CCGT) (3-5 years) > Aeroderivative engines (1.5-3 years) ≈ Light-duty gas turbines (1-3 years) > Gas internal combustion engines (1-2 years) > SOFC (90-120 days).

Cost per kilowatt-hour: SOFC > Internal combustion engines > Aeroderivative/light-duty gas turbines > Heavy-duty CCGT;

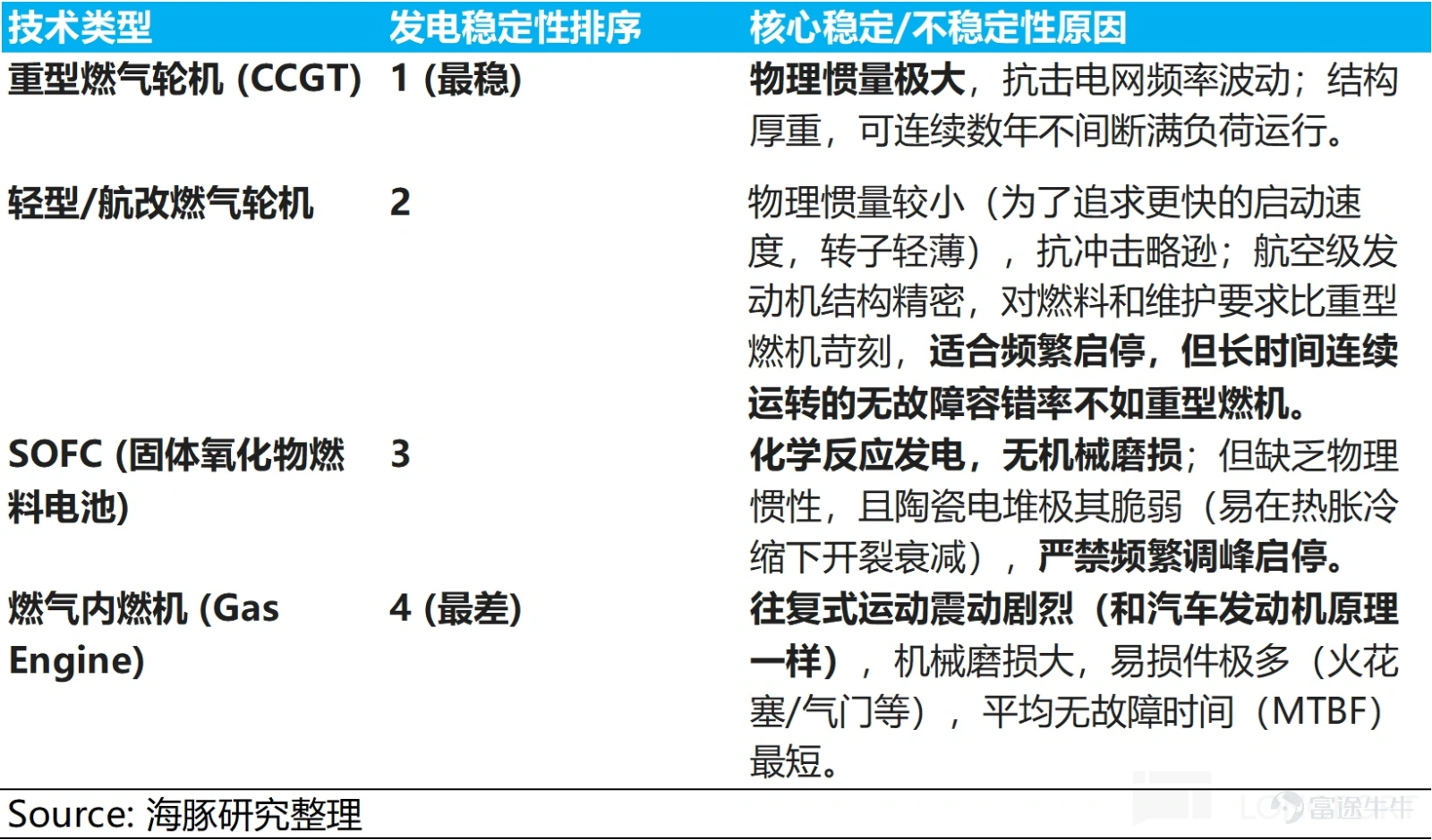

Power generation stability: Although all routes can provide highly reliable baseload power, the ranking in terms of stability is as follows: Heavy-duty gas turbines > Light-duty gas turbines/aeroderivative turbines > SOFC > Gas internal combustion engines.

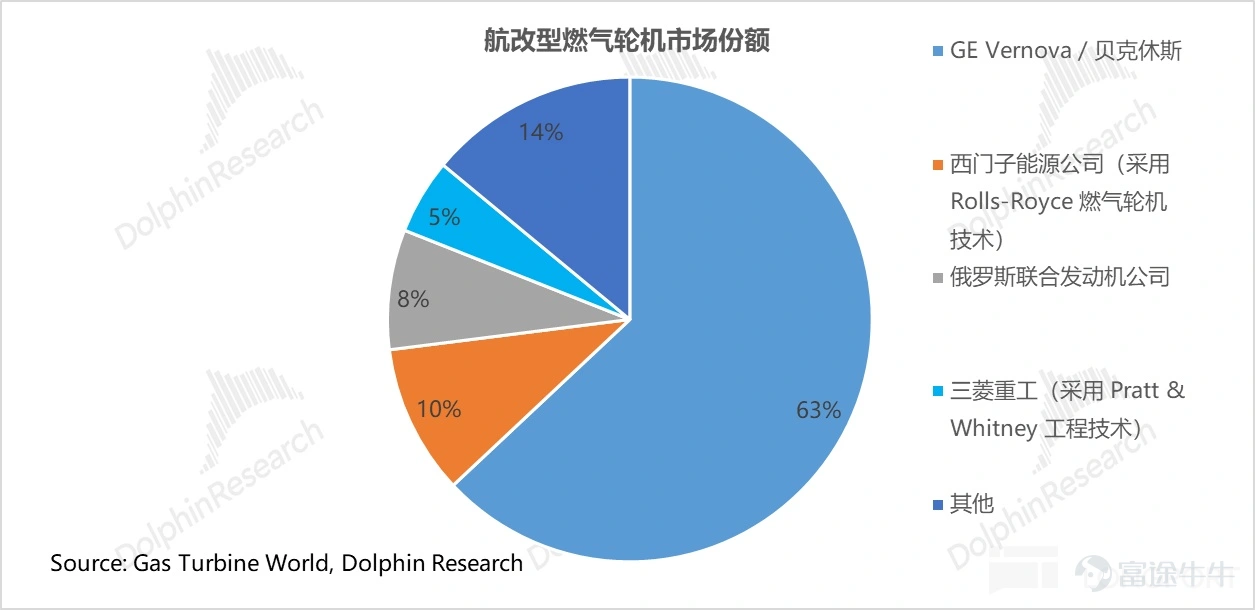

1) Aero-derivative gas turbine market (single unit power 30-60MW): Dominated by a duopoly

In the past five years, GE Vernova and Baker Hughes $Baker Hughes(BKR.US) have held an absolute leading position in the aero-derivative gas turbine market, with a combined market share of up to 63%. Other major players include: Siemens Energy (10%), United Engine Corporation of Russia (8%), and Mitsubishi Heavy Industries (5%).

Aero-derivative gas turbine technology originates from aircraft engines. GE Vernova and Baker Hughes (whose aero-derivative technology stems from the original GE Aviation division) have established a near-monopolistic advantage based on their deep expertise in aircraft engines (such as GE's LM series and Baker Hughes' LM/LMS series), highlighting extremely high technical homogeneity and patent barriers.

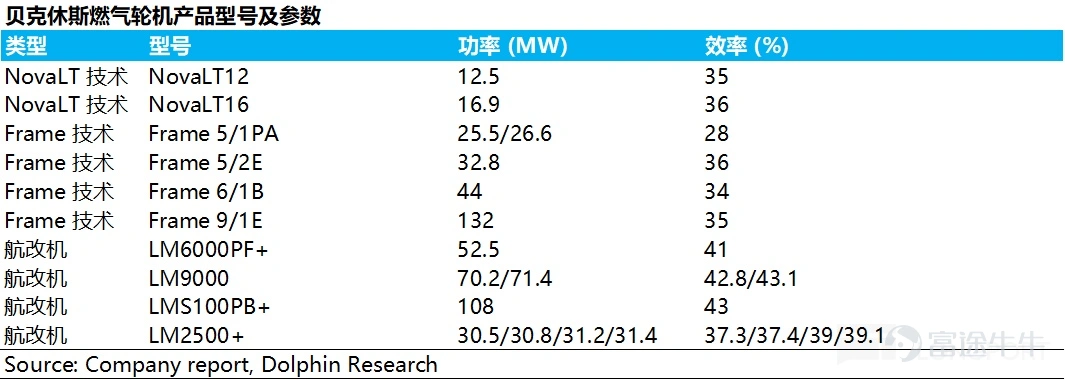

Baker Hughes' product line covers 12.5MW to 132MW, combining the high efficiency of aero-derivative turbines with the maturity of the Frame series industrial gas turbines, and is widely used in oil and gas field power generation, regional energy supply, and power peak shaving.

2) Light gas turbine market (single unit power 5-50MW): One superpower, many strong players

In 2024,Solar Turbines (a subsidiary of Caterpillar) dominates the light gas turbine market, with a market share as high as 48%Its absolute leading position stems from decades of deep cultivation in the oil and gas sector. Lightweight gas turbines are core equipment for industrial drives such as oil and gas fields and pipeline boosting.

Sola has built strong customer loyalty through its extremely high reliability, a global service network, and synergy with Caterpillar's distribution channels. Other key players include Siemens Energy (25%) and MAN Energy Solutions (10%).

3) Gas internal combustion engines: The core承接of AIDC power demand overflow

① Working principle of gas internal combustion engines

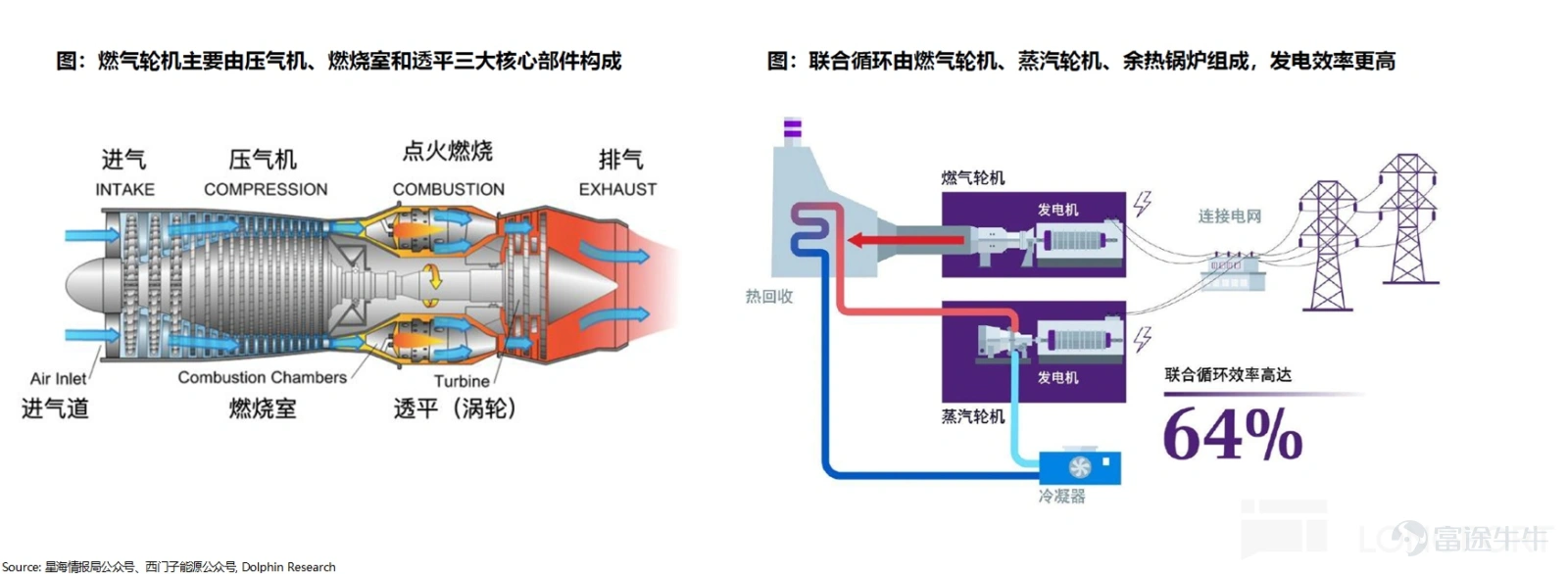

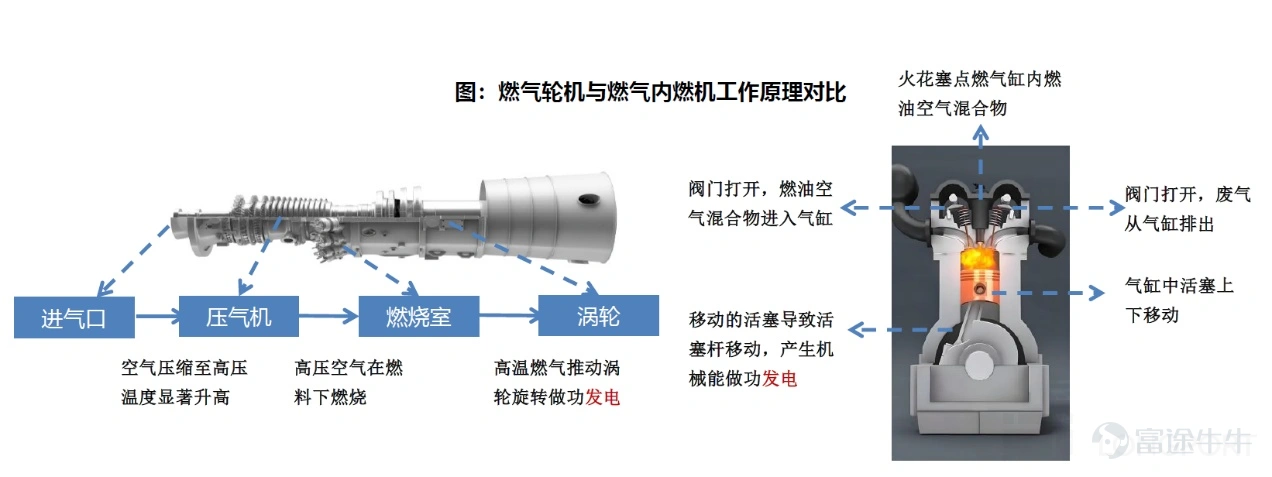

There is a fundamental difference in working principles between gas turbines and gas internal combustion engines (reciprocating engines): the former operates on the Brayton cycle, generating electricity by driving turbines with gas; the latter operates on the Otto cycle, generating electricity through piston reciprocation (structurally similar to a reinforced version of a large automotive engine).

In the current global wave of power infrastructure construction driven by AIDC, the strategic role of gas internal combustion engines (particularly medium-speed engines) has undergone a fundamental shift. Due to the severe shortage of heavy-duty gas turbine production capacity (with some leading manufacturers’ schedules extending to 2029) and the rapidly growing power demands of AIDC, gas internal combustion engines have quickly transitioned from their traditional roles as backup power or combined heat and power solutions to become core primary and peak-shaving power options for AIDC, thanks to their modular rapid deployment (fast delivery times), second-level load-following capabilities, and mature global supply chains.

② High-speed engines focus on backup, while medium-speed engines target baseload

Gas internal combustion engines used in AIDC are mainly divided into two technical categories, with technical parameters directly determining their respective commercial applications:

High-speed engines (≥1000 rpm): Flexible disaster recovery power and emerging primary power solution

These are characterized by smaller single-unit power output (1-5MW), second-level rapid start-stop capabilities, lower initial investment (Capex), and quick deployment, but their power generation efficiency (about 45-48%) is lower than that of gas turbines.

Historically, the core applications of high-speed machines have been data center backup power (the most widely used application), grid peak shaving, and industrial self-generation/combined heat and power (CHP). Today, thanks to their short construction cycle, investment-friendly nature, and flexible start-stop capabilities, they are rapidly transitioning from a "backup" role to become the primary power source for the high-growth market of data centers, particularly suitable for edge computing nodes and small to medium-sized distributed data centers. For large AIDCs, parallel operation of multiple units is required, demanding higher system integration and control.

Medium-speed machines (250-1000 rpm): A highly economical choice for base load and main power supply

Their characteristics include larger single-unit power output (6-20MW) and minute-level startup capability, with the core advantages being "extremely high power generation efficiency (48%-50%)" and good partial load performance.

Under long-term continuous operation, their levelized cost of electricity (LCOE) holds an advantage over high-speed machines, making them the preferred solution for main power supply in medium-sized AIDCs (50-400MW). They can also serve as the main power supply for phased construction of large AIDCs.

Historically, medium-speed machines were mainly applied in traditional fields such as marine propulsion (core application), peaking power plants, distributed grids, and industrial combined heat and power, offering limited profit margins. Today, leveraging the power shortage in North American AIDCs, they are successfully entering the high-barrier, high-value-added emerging market of overseas data centers.

Market Competition Landscape: Clear barriers in niche tracks, presenting an oligopolistic structure

In fields like data center backup power and gas power generation, market concentration is extremely high, with core shares controlled by a few global industrial giants:

High-speed machines: Dual-line oligopoly in diesel and gas

In the high-speed machine sector, both the diesel generator and gas generator markets exhibit a highly concentrated oligopolistic structure.

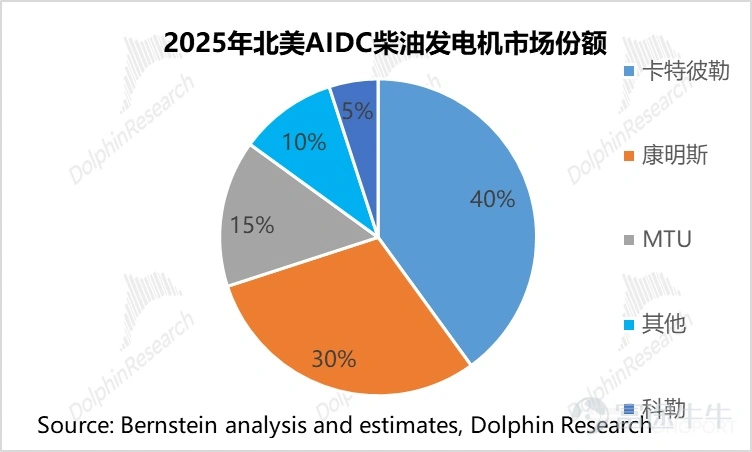

Diesel generator market (mainstay of backup power):The market is dominated by three global giants: Caterpillar (CAT), Cummins (CMI.US) (CMI), and MTU, collectively occupying the vast majority of the market share and forming the foundation of backup power solutions for data centers.

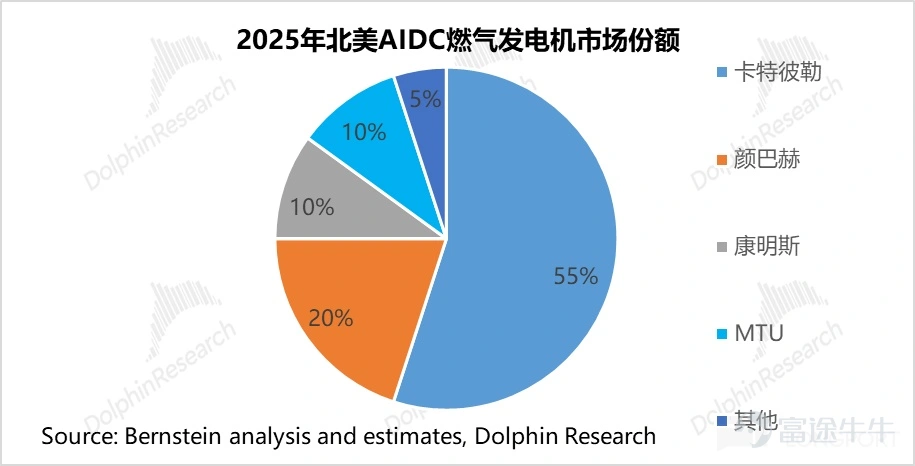

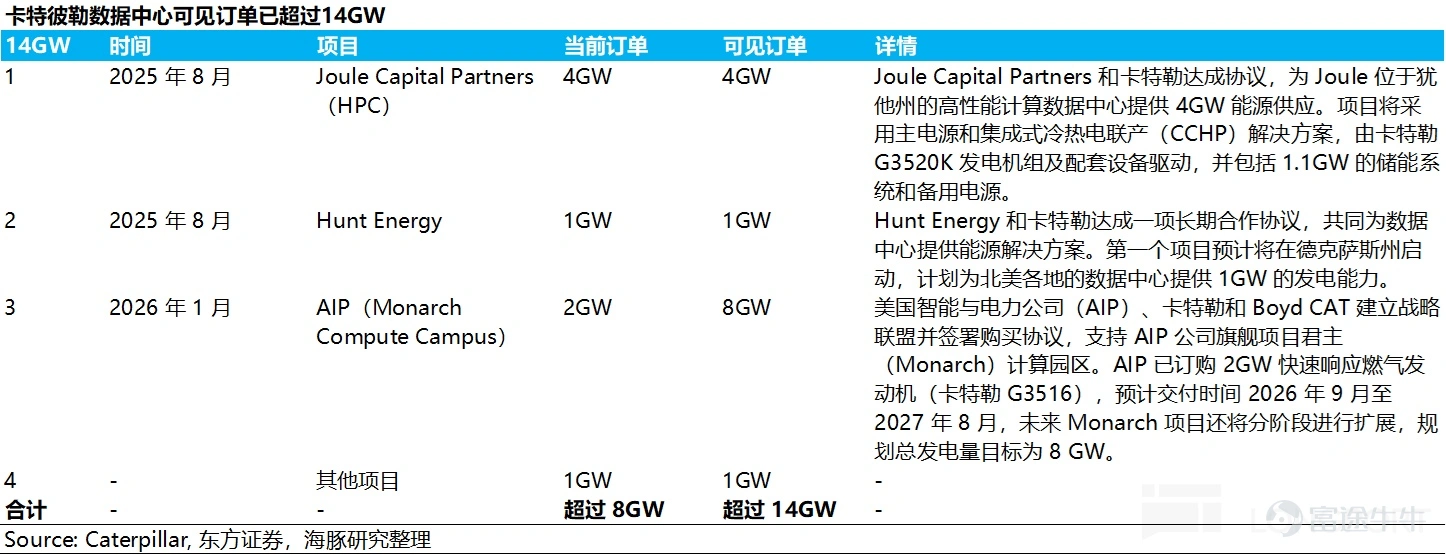

High-speed gas engine market (primary power/peak shaving):In the high-speed gas generator sector, Caterpillar holds an absolute global leading position (with a market share of approximately 55%), followed by INNIO (under Jenbacher). In the rapidly growing North American AIDC market, Caterpillar’s leadership stands out prominently, with its current backlog of data center gas power generation projects exceeding 8GW. Long-term order potential is substantial (partner plans total over 14GW).

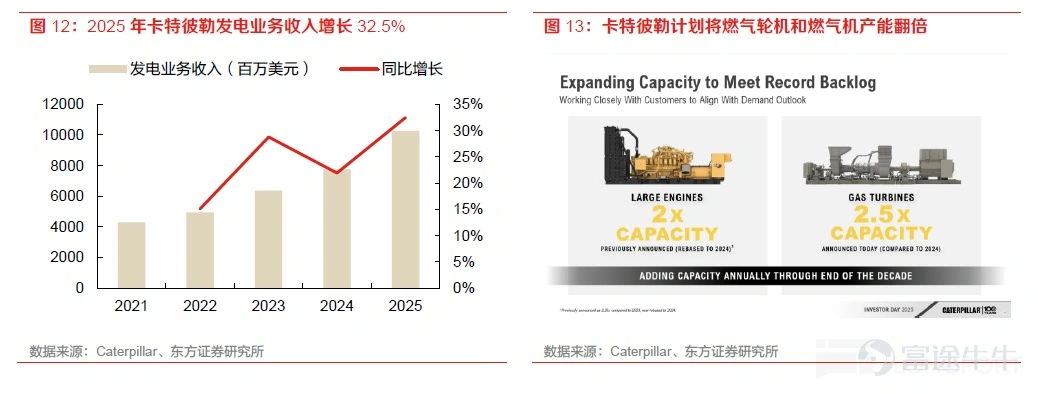

Caterpillar's power generation business showed strong performance in 2025, with revenue increasing by 32.5% year-on-year. The company has set a clear expansion strategy: aiming to more than double power generation revenue by 2030 compared to 2024 levels. To support this goal, the company is making large-scale capacity investments, planning to increase gas turbine production capacity to 2.5 times that of 2024 and gas generator capacity to twice the current level, corresponding to an annual power equipment supply capacity of approximately 50GW.

Medium-speed gas engine market: Leading companies positioning themselves in the emerging primary power blue ocean

Medium-speed engines have traditionally been used in ships and power stations, with a relatively dispersed traditional market share. Currently, due to their high power generation efficiency (48%-50%) and better cost per kilowatt-hour, they are becoming a key solution to fill the gas turbine capacity gap and serve medium-sized AIDC baseload needs, successfully entering the high-value-added track of primary power for data centers.

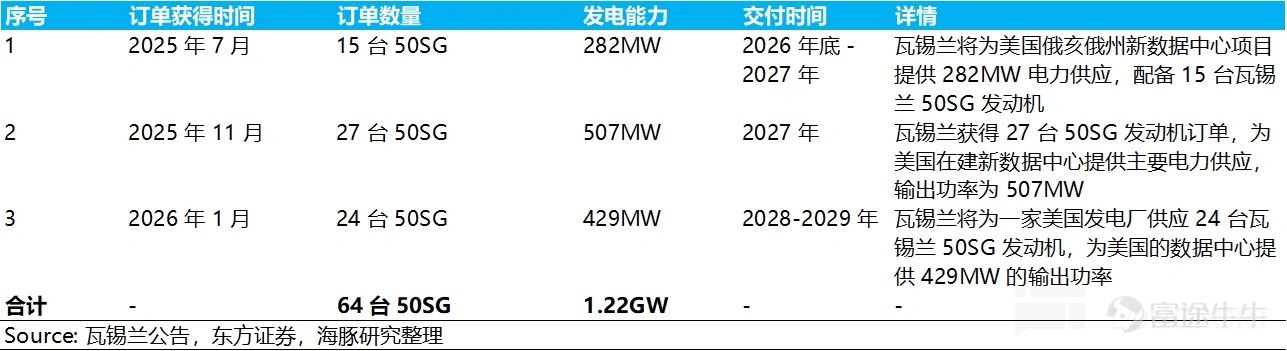

In this emerging market, Wärtsilä has secured GW-level orders thanks to its first-mover advantage; meanwhile, giants such as Caterpillar and Cummins are also leveraging their full product line capabilities and customer relationships to enter strongly, with the competitive landscape taking initial shape.

4) SOFC: The 'fast charging station for electricity' in the AIDC era, offering both delivery speed and long-term economic benefits

In the selection of power supply systems for North American data centers, the industry is undergoing a step-by-step evolution from 'seeking operational nuclear power → building new heavy-duty gas turbines → aeroderivative gas turbines/internal combustion engines → deploying new SOFCs.' The core driver behind thishas shifted from a mere demand for clean energy to an urgent need for 'extremely short delivery cycles (Time-to-Power)'。

Traditional nuclear power plants face regulatory headwinds due to grid expansion constraints (e.g., FERC rejecting relevant agreements), significantly increasing uncertainty for project implementation. Although 'gas-fired power' is an ideal off-grid power supply option, both heavy-duty and small gas turbines face delivery cycles of up to 2-3 years. In contrast, SOFCs perfectly align with the current supply and demand characteristics of AIDC (AI data centers), with their core advantages reflected in the following three aspects:

① Extremely short delivery cycle, matching AIDC construction timelines

Among on-site power generation solutions, SOFC deployment speed offers an overwhelming advantage. Compared to heavy-duty gas turbines with delivery cycles exceeding three years, SOFCs use a modular design, enabling 'plug-and-play' functionality.

According to data from Bloom Energy (BE.US), the delivery cycle for its 50MW systems is within 90 days, and for 100MW systems, within 120 days. For example, in its project supplying Oracle data centers, it successfully achieved power delivery within 90 days.

This 'month-based' delivery speed perfectly addresses the pain point where data center construction is fast but traditional grid connection is slow.

② Economic feasibility approaches that of gas-fired power; subsidies enhance competitiveness, with clear cost reduction pathways at scale

For natural gas-fueled SOFCs, their levelized cost of electricity (LCOE) has become highly competitive in the market after receiving subsidies.

a. ITC subsidies directly reduce initial investment

The U.S. Inflation Reduction Act (IRA) and subsequent legislation have included SOFCs under the Investment Tax Credit (ITC). The standard subsidy amount covers 30% of the initial investment (Capex); if additional requirements such as energy community or domestic production are met, subsidies can reach up to 50% of Capex. This reduces the per-unit cost of SOFCs from approximately $5/W to $2.5-$3.5/W after subsidies, significantly narrowing the investment gap with small gas turbines.

b. Low redundancy configuration and high efficiency optimize lifecycle costs

Despite the high initial investment, SOFC effectively compensates for this disadvantage in the following two ways:

Low redundancy requirements: To achieve 99.9% power supply reliability, meeting a 100MW power demand requires only 109MW of SOFC systems, compared to 130MW for gas turbines. The lower redundancy requirement reduces the total installed capacity, partially offsetting its higher unit cost.

High efficiency and low operating costs: SOFC has extremely high power generation efficiency (55%-65%) and supports high utilization hours. Its per-kilowatt-hour fuel cost is significantly lower than that of gas turbines, thereby reducing lifecycle operating costs.

Under assumptions close to commercial operations (e.g., natural gas price at 4 USD/MMBtu, equipment utilization rate of 86%, and initial investment at 3.5 USD/W after receiving a 30% ITC subsidy), the LCOE for SOFC is estimated to be approximately 90 USD/MWh, which is already on par with gas turbine-aero derivative projects, providing crucial economic support for its commercial application.

Fuel flexibility and a clear long-term cost reduction path

Dual-fuel compatibility: Additionally, although the LCOE for using green hydrogen as fuel currently exceeds 150 USD/MWh, which does not yet meet commercial standards, SOFCs have 'dual-fuel' compatibility. In the future, when green hydrogen becomes economically viable, it can seamlessly switch to hydrogen fuel, aligning perfectly with tech giants' ESG emission reduction narratives.

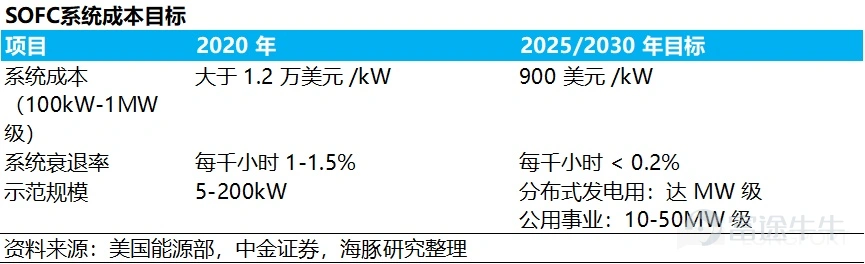

Significant cost reduction potential remains: Based on the scaling effects of electrochemical technology, SOFCs have enormous cost reduction potential. The US Department of Energy's Solid State Energy Conversion Alliance (SECA) has set long-term targets for SOFC costs, aiming to reduce SOFC system costs to below 900 USD/kW by 2025/2030. As production capacity expands and processes improve, their economic advantages are expected to further increase.

c. High efficiency and low emissions, aligning with tech giants' ESG goals

SOFC pure power generation efficiency reaches 55%-65%. If waste heat is utilized for combined cooling, heating, and power, the overall efficiency can exceed 90%. Even when burning natural gas now, carbon emissions are more than 30% lower than traditional units, with virtually no exhaust pollution. Plus, they occupy less space and operate quietly, making them an ideal power source for next-generation green data centers.

Technical principles and competitive landscape: Seeking the optimal balance between 'long life and low cost'

① Principle Essence: 'Direct Power Generation' Beyond the Carnot Cycle

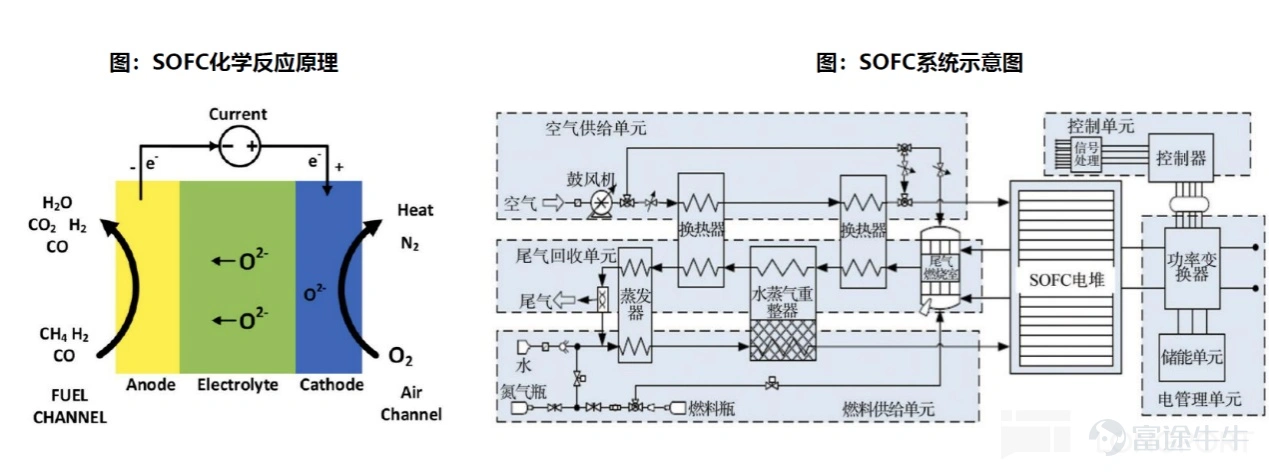

SOFC is essentially a power generation device that bypasses the Carnot cycle, directly converting chemical energy into electricity. In high-temperature environments ranging from 650°C to 950°C, oxygen ions pass through the solid electrolyte and undergo electrochemical reactions with fuels (such as natural gas or hydrogen) at the anode to generate electrical power.

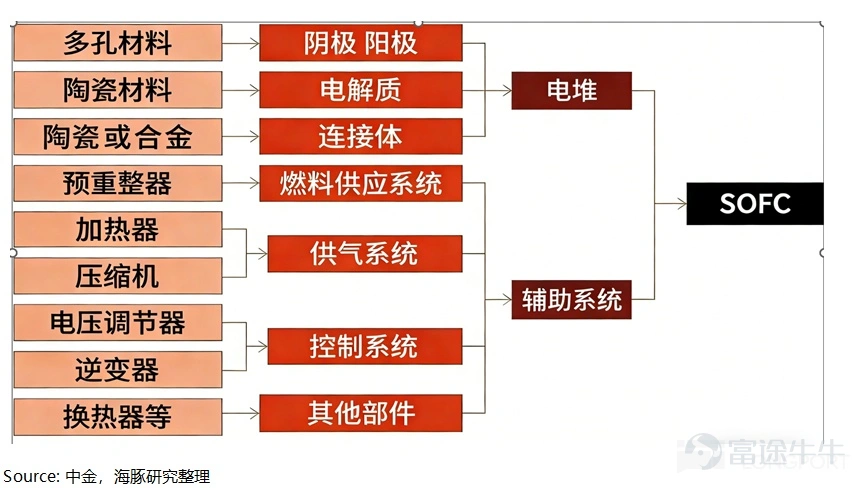

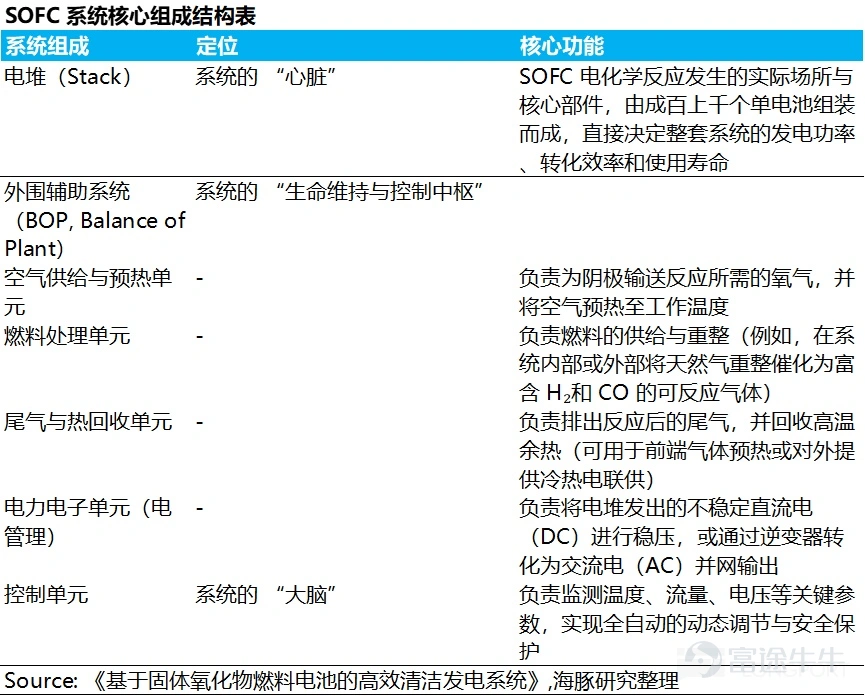

② System Architecture: Stack + Balance of Plant (BOP)

A complete SOFC power generation system consists of two major parts working together: the 'core reaction zone' and the 'peripheral support zone'.

Stack: The 'heart' of the system

The stack is where the electrochemical reactions of the SOFC take place, serving as the core component. It is assembled from hundreds or thousands of single cells, directly determining the system's power output, conversion efficiency, and service life.

Balance of Plant (BOP): Surrounding the stack, the BOP includes air supply preheating units, fuel supply (reforming) units, exhaust recovery units, power management units, and control units.

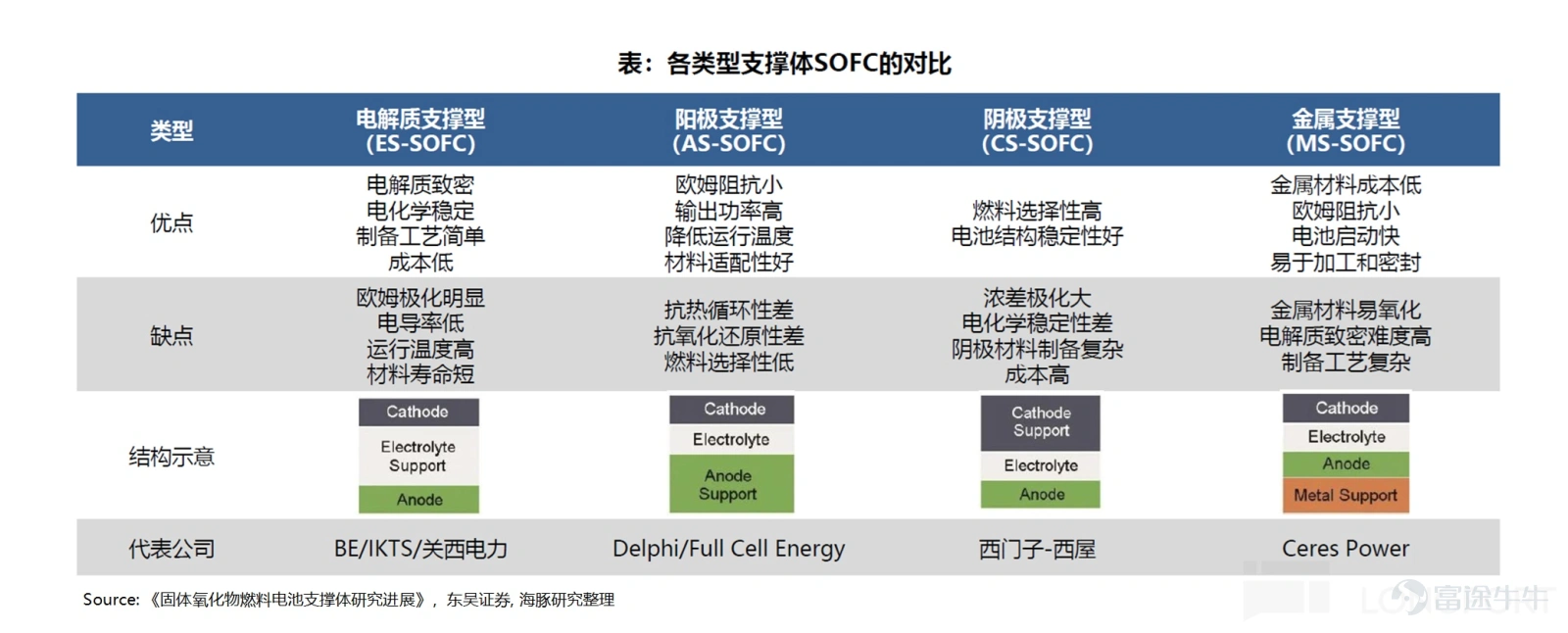

Based on structural support, SOFCs are mainly divided into three categories: electrolyte-supported, electrode-supported (primarily anode-supported), and metal-supported types. The evolution of different technical routes fundamentally seeks the optimal balance between 'mechanical strength, operating temperature, and internal resistance'.

① Electrolyte-Supported Cell (ESC): Stable at high temperatures, with mature technology (First Generation)

This technology originated the earliest, using a thicker electrolyte layer to provide mechanical support, with relatively thin electrodes. Although its start-up time is the 'slowest' among several technologies, its advantages lie in good mechanical performance, high structural stability, and a relatively simple preparation process for single cells. These extremely mature and robust characteristics make it highly suitable for 'baseload power generation,' where systems run continuously without shutting down for years.

Its disadvantage lies in the fact that a thicker electrolyte significantly increases ohmic impedance. To ensure ionic conductivity, its operating temperature must be extremely high (usually between 850°C and 1000°C), which imposes stringent requirements on the high-temperature resistance of surrounding BOP auxiliary materials.

Representative company: Bloom Energy.

② Electrode-supported type (ASC/CSC): Lowering temperature and reducing resistance, prioritizing performance (Second-generation mainstream)

To overcome the high-temperature limitations of the first-generation technology, this approach involves making the core electrolyte 'thinner' and using thicker porous anode material as the framework. This improvement successfully reduced the operating temperature to 600°C-800°C, not only significantly increasing the power generation density but also allowing the system to adopt cheaper metal interconnect materials.

Its disadvantage lies in the fact that an overly thick anode can easily lead to mass transfer limitations (poor gas diffusion); additionally, under frequent start-stop cycles or redox atmospheres, the anode material is prone to volumetric expansion, potentially causing stack rupture.

Representative companies: Delphi, FuelCell Energy (anode-supported); Siemens-Westinghouse (cathode-supported tubular type).

③ Metal-supported type (MSC): Resistant to thermal shock, cutting-edge disruption (Third-generation frontier)

Recognized as the most advanced technology, MSC completely abandons the all-ceramic skeleton, instead adopting extremely inexpensive and robust 'stainless steel (porous metal)' as the support, further reducing the operating temperature to 500°C-600°C.

Its core advantage lies in significantly enhancing the mechanical strength and thermal shock resistance of the system, enabling extremely fast start-stop speeds, while the base materials and manufacturing costs are very low.

Although MSC is regarded as the ultimate frontier route, it is currently in a commercialization bottleneck period marked by challenges in "large-scale production" and "long-term life validation." Metals are prone to oxidation during long-term operation at high temperatures, and the difference in thermal expansion coefficients between metals and ceramics can lead to coating peeling due to repeated thermal expansion and contraction. Companies in the industry are now working hard to solve these long-term degradation issues.

Representative company: Ceres PowerCeres Power Holdings plc (CWR.UK) (SteelCell technology), Weichai Power

The market structure shows a situation of 'one superpower and multiple strong players':

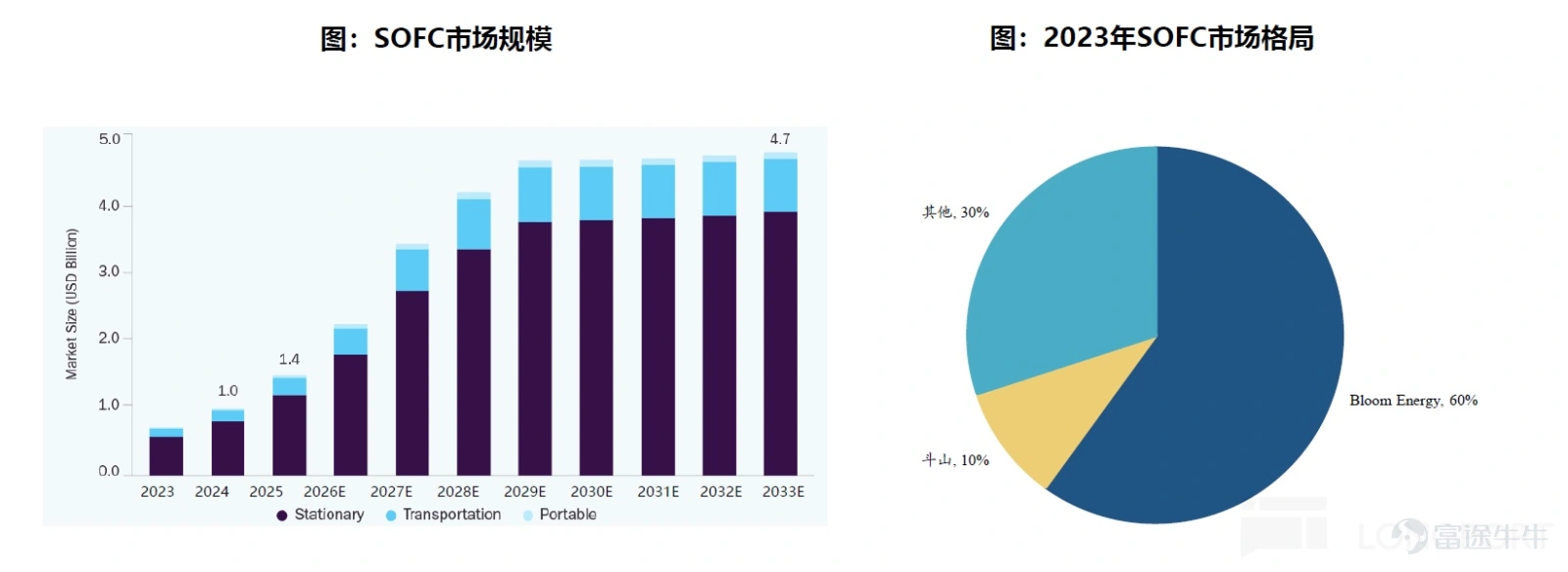

Though the base remains small, it is on the verge of an explosive growth phase:Currently, the global SOFC market size is relatively small overall. According to ID TechEx, the global SOFC market size in 2024 is only 1 billion US dollars. However, with the surge in emerging high-energy-consuming scenarios such as AIDC, this sector is entering a period of rapid growth.

In the field of mass production and system integration for industrial and commercial SOFC (Solid Oxide Fuel Cells), the market exhibits a structure of 'one superpower and multiple strong players,' dominated by Bloom Energy (BE). Meanwhile, several manufacturers are accelerating their catch-up through technology licensing and collaboration models.

Absolute leader: Bloom Energy (BE)

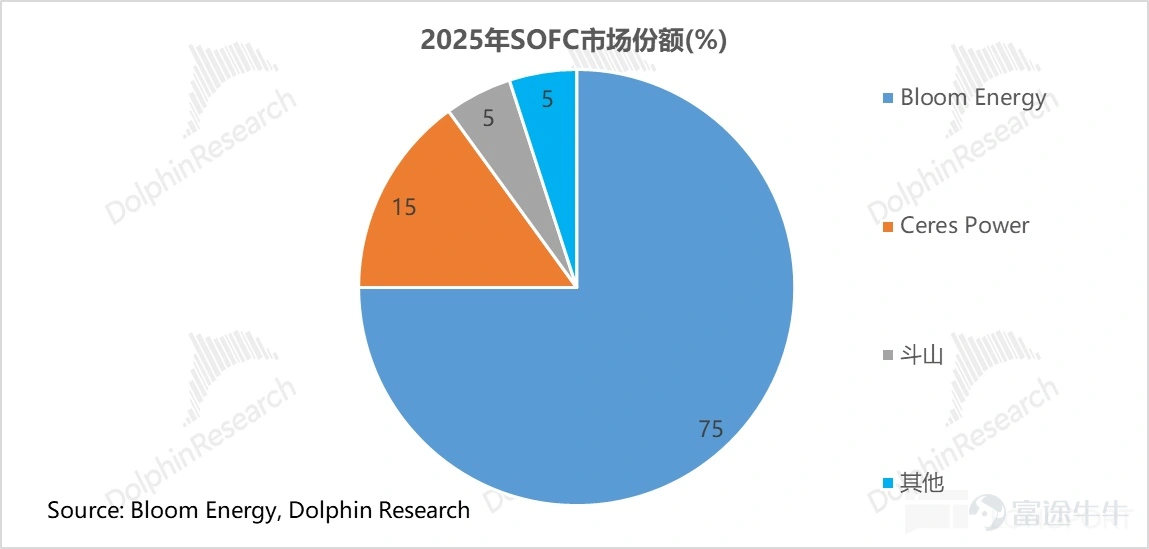

Bloom Energy is the absolute leader in the global commercial implementation of SOFC. Its market share is as high as 60%-80%, occupying a monopolistic position.

Its core advantages stem from mature and stable technology and system integration barriers, established mass production capabilities, faster delivery speeds compared to peers (typical projects can be deployed within 90-120 days), and a comprehensive and solid customer ecosystem built through first-mover advantages.

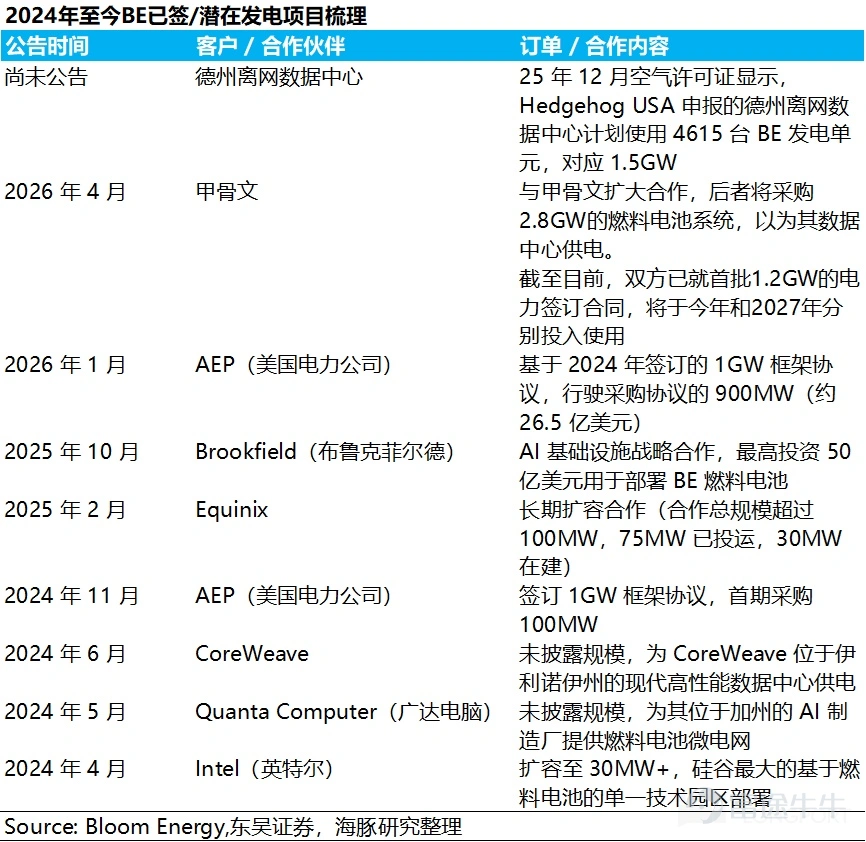

Its customers have fully penetrated the AI ecosystem, covering hyperscale enterprises (such as Oracle, AWS), power/gas suppliers (such as American Electric Power, with cumulative orders of approximately 1GW signed), emerging cloud providers (such as CoreWeave), and infrastructure investors (such as Brookfield, with a $5 billion strategic partnership reached).

In terms of capacity, the company's current production capacity is approximately 1GW, with plans to double it to 2GW by the end of 2026.

Active catch-up players: Capacity expansion under technology licensing and cooperation models

Outside of Bloom Energy, UK-based Ceres Power, with its third-generation 'metal-supported (MSC)' technology, is building a vast global manufacturing network through a 'light-asset IP licensing' model, becoming the strongest complementary force to constrain BE. Ceres itself does not build large-scale complete equipment factories but licenses its SteelCell core technology to global manufacturing giants. Its main ecosystem partners include:

Doosan: The fastest in mass production progress, with an annualized production capacity of 50MW already established, and mass production officially commencing in July 2025. The first sales are expected to be completed by the end of the year.

Delta: Has announced plans to invest in building a production base, accelerating system integration layout, with production capacity expected to commence operations by the end of 2026.

Weichai Power: As a strategic shareholder of Ceres (holding approximately 20%), it has obtained a core stack manufacturing license and is steadily advancing the construction of domestic production bases, making it the leading enterprise with the fastest SOFC industrialization process in the country.

Other regional giants: Including large equipment and component companies such as Denso and Thermax, which have been authorized and are working collaboratively to accelerate the commercialization of SOFCs across various regions globally.

Bloom Energy (BE): Triple leap in cost, orders, and role

① Cost Reduction: Technology iteration and scale effects drive full-scale production increase

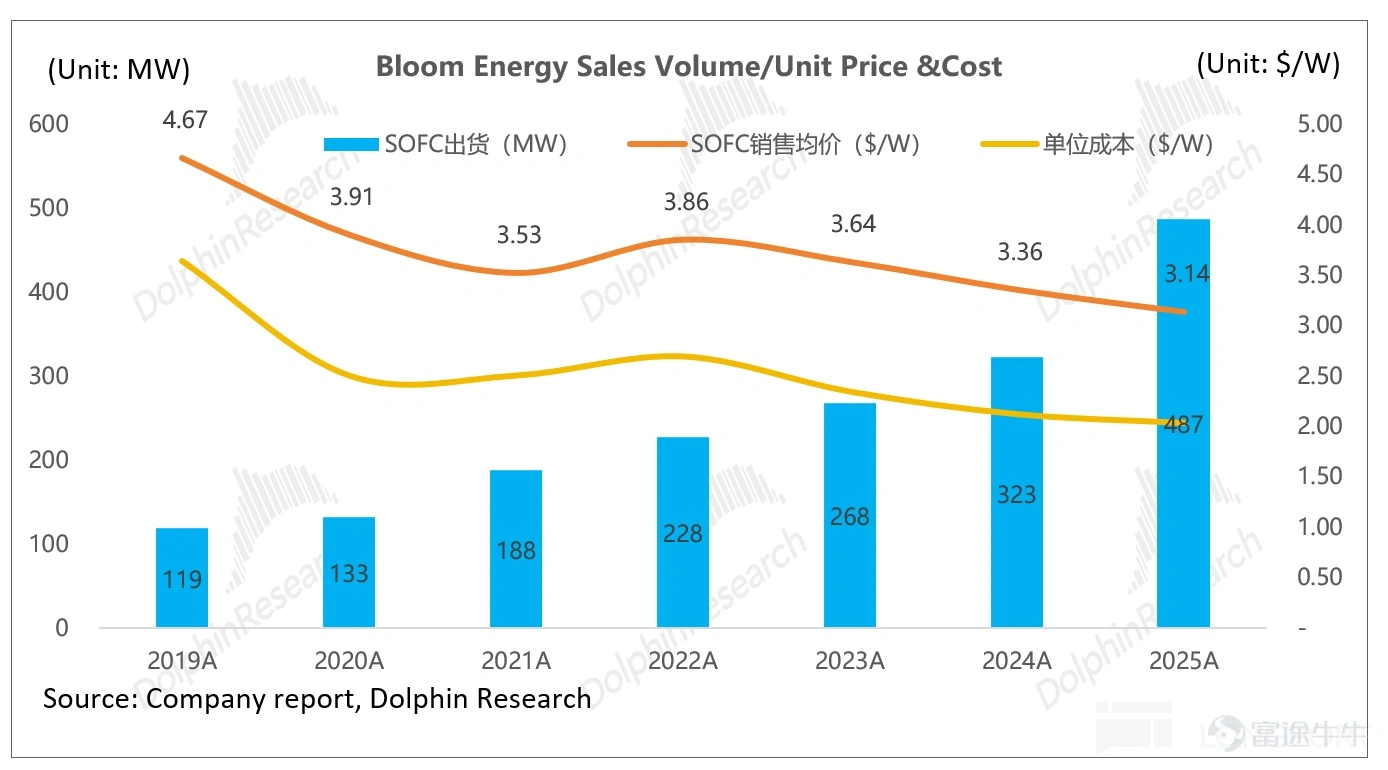

Bloom Energy has achieved a steady decline in hardware costs through continuous technological advancement and large-scale capacity expansion. The per-unit cost of its SOFC systems has dropped significantly from approximately $4.67/W in 2019 to about $3.14/W by 2025, with an average annual reduction of 6%. This cost-reduction capability is also the reason Bloom Energy has been able to break through the limitations of high electricity price regions and achieve scaled expansion into low electricity price states across the US.

② Surge in Orders: Backlog of $20 billion hits record high, strong visibility for the next 1-2 years

By the end of 2025, Bloom Energy's total backlog reached a record high of approximately $20 billion. Among this:

Product orders: Approximately $6 billion (a year-on-year surge of 140%), corresponding to about 2GW of potential SOFC deployment capacity;

Service orders: Approximately $14 billion (a year-on-year increase of 46%), indicating the high-margin cash flow value of long-term operations and maintenance under the PPA (Power Purchase Agreement) model.

These substantial backlogs have fully covered the company’s planned capacity for 2026 and partially locked in until 2027, providing extremely high visibility for earnings release over the next two years. Based on this, management provided strong guidance of 'over 50% revenue growth and Non-GAAP gross margin above 32% for 2026.'

③ Structural Optimization and Role Transformation: From 'Policy-Supported Energy' to 'Baseline Power Source in the AIDC Era'

The year 2024 marks a turning point for Bloom Energy’s role. Before 2024 (during the demonstration and validation phase), orders were mostly small to medium-sized (such as the SK Group project in South Korea), primarily driven by corporate or local government demands for clean energy.

However, with the outbreak of the North American AIDC power crisis, Bloom Energy's role has shifted from a traditional 'off-grid alternative power source' to a 'high-potential mainstay' resolving grid bottlenecks and providing 24/7 uninterrupted power supply for computing. This transformation is also evidenced by the optimization of the order structure:

Regional expansion (breaking away from electricity price dependency):In 2024, over 80% of orders will still come from high electricity price states in the US (the core logic being arbitrage on electricity price differences); however, by 2026, over 80% of the order backlog has shifted to low electricity price states.

This not only indicates that data center site selection is being forced to shift towards regions where base load power can be quickly accessed, but also confirms that BE's LCOE (Levelized Cost of Energy) now has cross-regional competitiveness, achieving a role transformation from 'electricity price arbitrage' to 'addressing computational power shortages'.

Client upgrade and high stickiness:The pool of high-priority order clients has significantly diversified, covering six hyperscale tech giants and emerging cloud vendors (compared to only one a year ago), while also forming deep ties with utility giants (American Electric Power), infrastructure capital (Brookfield), data centers (Equinix), and cloud giants (Oracle). Meanwhile, two-thirds of orders in the industrial and commercial sectors are from repeat purchases by existing clients, endorsing the absolute reliability of its technology under extreme loads.

According to the latest environmental approval documents, the planned off-grid data center cluster in Texas is expected to deploy approximately 1.5GW of BE equipment. With an extreme delivery capability of 90-120 days for plug-and-play, BE is aggressively entering the core supply chains of top cloud vendors like Meta and Google, leaving future mega-orders with considerable breakout potential.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

2