Behind the 'highlight' performance of Jinge New Materials: Unavoidable triple challenges of pricing, procurement, and production capacity | Understanding IPO

Source: Times Business Research Institute Authors: Special Research Fellows Zeng Ruizhi and Zheng Lin

Image source: Tuchong Creative

Source: Times Business Research Institute

Authors: Special Research Fellows Zeng Ruizhi and Zheng Lin

Editor | Zheng Lin

On April 10, the Beijing Stock Exchange's official website showed that the IPO review process of Guangdong Jinge New Materials Co., Ltd. (hereinafter referred to as 'Jinge New Materials') had entered the submission-for-registration stage, sparking considerable discussion in the market.

This company, which specializes in functional powder materials, appears to have solid performance and high gross margins. However, a closer look at the two rounds of inquiry letters from regulators reveals some rather sharp questions. We'll dissect these inquiry disclosures to discuss the real situation of this company.

The Times Business Research Institute found that despite Jinge New Materials’ revenue and net profit growth year-on-year in 2025, the company’s operational challenges are far from over. Although the company has passed the Beijing Stock Exchange Listing Committee review, it faced key inquiries about the sustainability of its earnings growth and the reasonableness of raw material procurement prices. The company later stated that these issues had been somewhat mitigated through cost control and supplier adjustments, but concerns such as weak pricing power and related-party transactions may continue to attract scrutiny from IPO regulators. Whether it can transition from scale growth to high-quality growth remains to be seen.

On April 13 and 14, regarding product pricing power and the ability to absorb new production capacity from fundraising, the Times Business Research Institute sent emails and made calls to Jinge New Materials for clarification, but had not received a response by the time of publication.

Impressive financials, but pricing power may be somewhat 'illusory'

Jinge New Materials' revenue fluctuations in recent years are quite intriguing. According to iFinD data, the company's revenue was 416 million yuan in 2022, dropped to 385 million yuan in 2023, and rebounded to 467 million yuan in 2024. The non-recurring net profit followed a similar trajectory, dropping from 44.14 million yuan to 40.94 million yuan, before recovering to 46.93 million yuan. This 'V-shaped' reversal was explained by the company as being due to intensified competition in downstream industries, with cost pressures being passed on to upstream suppliers.

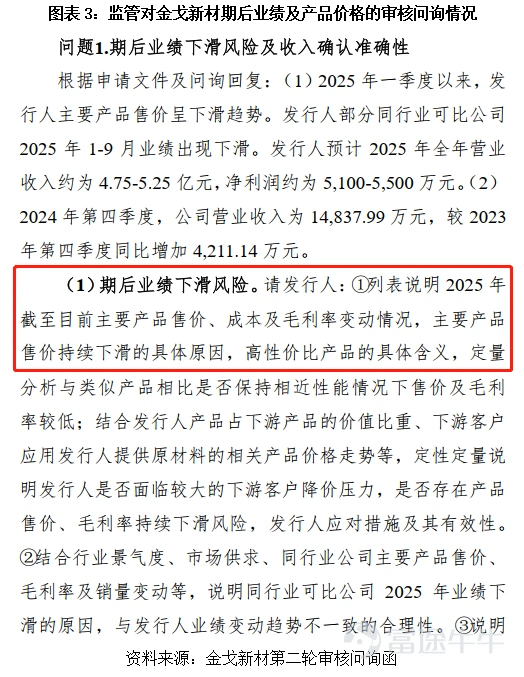

However, the issue is that the reply to the first round of the Beijing Stock Exchange’s review inquiry revealed that the selling price of Jinge New Materials' products had declined during the reporting period. The first round of inquiries directly highlighted that the gross margin of key products fell in 2024, and by January to April 2025, the gross margin had dropped to 19.40%. In the second round of inquiries, regulators explicitly asked about 'the changes in selling prices, costs, and gross margins of key products up to 2025, as well as the specific reasons for the continued decline in selling prices.'

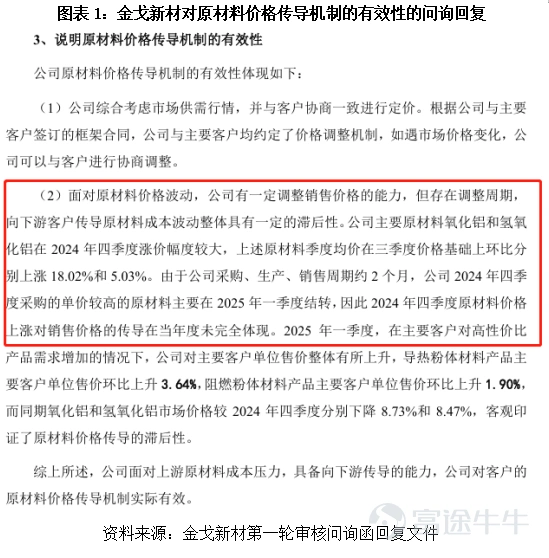

According to the responses to the two rounds of inquiries, as shown in Chart 1, Jinge New Materials has a noticeable lag in price transmission. In the fourth quarter of 2024, prices of key raw materials like alumina and aluminum hydroxide rose by 18.02% and 5.03% quarter-on-quarter, respectively. However, due to a 2-3 month lag in price transmission and increasing demand from downstream customers for cost-effective products, major clients significantly pressured the company to lower prices.

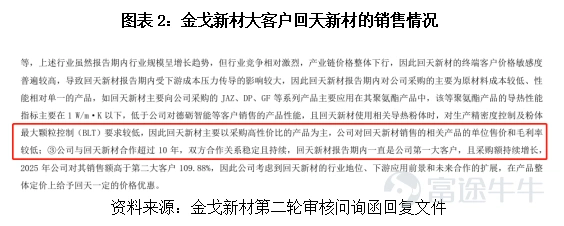

As shown in Chart 2, taking the largest client, Huitian New Materials (referring to Hubei Huitian New Materials Co., Ltd. and its consolidated companies), as an example, over 95% of the products Jinge New Materials sells to them are high-cost-performance products. Due to large purchase volumes, Jinge New Materials offered price discounts, resulting in significantly lower gross margins compared to other clients. This situation prevented Jinge New Materials from fully and promptly passing on cost increases to clients.

What does this indicate? It suggests that within the supply chain, Jinge New Materials may not possess significant pricing power. More crucially, the inquiry letter also questioned the price transmission mechanism—raw material prices increased in 2024, yet product selling prices decreased. So who is bearing the cost pressure? The answer is self-evident.

To be honest, this situation of being squeezed by both upstream and downstream is not just an issue for Jing Ge New Materials. The financial performance of its peer company, Wan Sheng Shares (603010.SH), for January to September 2025, has also declined, indicating that the entire industry is under pressure.

However, during the second round of review inquiries, Jing Ge New Materials projected that its full-year results for 2025 would still show year-over-year growth, and indeed they did. According to iFinD data from Tonghua Shun, the company's revenue in 2025 reached 534 million yuan, a year-over-year increase of 14.15%.

The regulatory inquiry actually serves as a reminder: short-term fluctuations in performance can be understood, but the justification for countercyclical growth must be sufficiently solid.

Gross margin higher than peers, but procurement prices are somewhat 'unclear'

From 2022 to 2025, Jing Ge New Materials' gross margin has consistently been higher than that of its comparable peer, Wan Sheng Shares, which could be seen as a positive. However, regulators repeatedly questioned the reasonableness of raw material procurement in two rounds of inquiries, which raises some concerns.

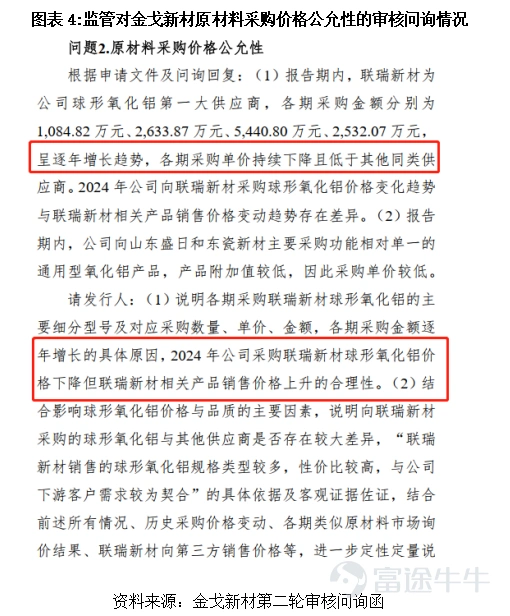

Let’s first discuss spherical alumina, a core raw material for Jing Ge New Materials. The second round of inquiry revealed that the procurement price from Lian Rui New Materials (688300.SH) had been declining annually and was lower than prices from other suppliers. In the first round of inquiry, it was pointed out that there were significant differences between the sales prices of Lian Rui New Materials and Ya'an Baitu Hi-Tech Materials Co., Ltd. (hereinafter referred to as 'Baitu Shares') and the procurement prices of Jing Ge New Materials. Jing Ge explained that the lower prices were due to reaching strategic partner procurement volumes, with purchases mainly focused on cost-effective micron-level products; whereas Lian Rui's disclosed average selling prices included higher-end sub-micron level products, making the pricing discrepancy reasonable.

While this may not necessarily be problematic, the second round of inquiry probed further: in 2024, while Jing Ge New Materials’ procurement prices decreased, Lian Rui New Materials’ own product sales prices increased. The response to the second round of inquiry showed that the procurement price of Jing Ge New Materials' core raw material, spherical alumina, remained consistently lower than other suppliers and continued to decline year over year. The company attributed this solely to “product mix differences + strategic procurement volume,” sidestepping the direct contradiction between its own falling procurement prices in 2024 and the rising sales prices of similar products from supplier Lian Rui New Materials, casting doubt on the authenticity of its high gross margin.

Next, let’s talk about Guangzhou Shengteng Trading Co., Ltd. (hereinafter referred to as 'Shengteng Trading'), a related party. This company exclusively sold to Jing Ge New Materials, ceased transactions in 2023, and was directly dissolved in 2024.

In the first round of inquiry letters, the establishment background, historical evolution, and the destination of profits of Shengteng Trading were all subject to regulatory questioning. However, Jing Ge New Materials explained in its response to the first round of inquiries that Shengteng Trading was established as a trading company to protect the confidentiality of key raw material suppliers and product models. Its exclusive sales to the company were deemed commercially reasonable. After terminating related-party transactions in 2023, Jing Ge New Materials protected trade secrets by enhancing internal coding management and access controls, establishing partnerships with alternative suppliers such as Guangzhou Shi Sheng Chemicals and Guangdong Fangding New Materials, ensuring stable supply of relevant raw materials. Shengteng Trading was dissolved in 2024, and its profit margins were in line with those of other industry trading companies, with no evidence of profit shifting or external cost padding.

Frankly speaking, trading companies that appear to be 'specifically serving the issuer' have always been a sensitive point in IPO reviews. A hasty dissolution only invites more speculation, and the follow-up questions in the second round of inquiries precisely reflect regulators’ concerns about related-party transactions.

The first round of inquiries revealed that, as shown in Chart 4, the prices at which Jinge New Materials purchased general-purpose alumina from Shandong Shengri (referring to Shandong Shengri Aopeng Environmental Protection Technology Co., Ltd. and its consolidated companies) and Dongci New Materials were lower, with the reason being 'lower product added value.' However, after 2024, purchases from Dongci New Materials will cease. In the second round of inquiry responses, Jinge New Materials stated that their self-produced semi-finished products (models CF59, CF51) are similar in performance but lower in cost, leading to an active termination of cooperation. Both parties confirmed there is no dispute. Despite claims of no disputes, the change in procurement patterns further raises questions about supply chain authenticity.

When piecing together all these details, it raises doubts about the quality of the 'high gross margin'—is it real capability or reliance on some less transparent procurement arrangements?

Can the market absorb a planned production expansion of 60% through this fundraising?

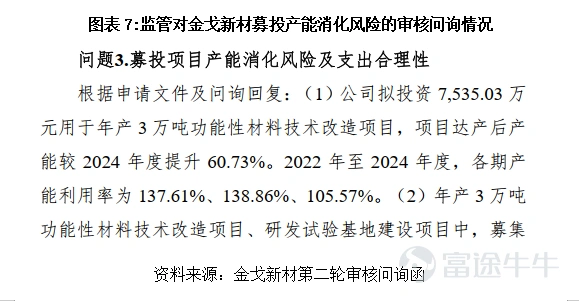

One of the core projects in Jinge New Material’s IPO fundraising is the technological renovation project for producing 30,000 tons of functional materials annually, which will increase capacity by 60.73% upon completion. The first round of inquiry documents showed that Jinge New Materials’ total capacity in 2024 was 49,400 tons, meaning the new capacity is substantial.

Notably, Jinge New Materials has been operating above capacity during the reporting period, with capacity utilization rates reaching 137.61%, 138.86%, and 105.57% for 2022, 2023, and 2024 respectively. This indicates that growth achieved through 'overload' operations in the past may face uncertainty transitioning smoothly to the absorption of new capacity.

However, we can identify some potential positive news in the second round of inquiry responses. Data cited by Jinge New Materials from research firms like LeadLeo shows that China’s thermally conductive powder market size for new energy vehicles is projected to grow at a compound annual growth rate (CAGR) of 15.00% from 2025 to 2029, while the consumer electronics sector is expected to grow by 7.40%, and the photovoltaic energy storage sector by 8.4%.

Additionally, according to iFinD data, major clients of Jinge New Materials, such as Huitian New Materials, Debang Technology (referring to Yantai Debang Technology Co., Ltd. and its consolidated companies), and Guibao Technology (300019.SZ), all reported year-over-year earnings growth in 2025. Moreover, the second round of inquiry responses indicate that these clients have clear expansion plans, with projected capacity absorption rates for Jinge New Materials at 84.71%, 80.90%, 87.37%, 94.36%, and 101.91% from 2026 to 2030; the forecasted absorption rate for the additional capacity (30,000 tons/year) from the fundraising project could reach 93.75% by 2030. The risk of idle capacity is low, as Jinge New Materials has maintained a production-sales ratio above 95% during the reporting period, with 95.04% recorded in 2025, indicating that the products are well-suited for the market and downstream demand is not shrinking, providing a solid basis for capacity digestion.

To summarize, the first round of inquiry letters required Jinge New Materials to quantitatively analyze capacity absorption risks by considering market space, competitive landscape, downstream demand, and current orders. The second round of inquiries further demanded a 'quantitative explanation of how the new 30,000-ton functional material technology upgrade project would handle capacity absorption after completion.' Essentially, regulators want to know how Jinge New Materials plans to sell the increased 60% capacity.

According to the first round of inquiry documents, certification from the Powder Technology Branch of the China Electronic Materials Industry Association shows that the high-performance thermally conductive fillers produced and sold by Jinge New Materials for electronic appliances perform at a leading level, with market share ranking among the top domestically.

In conclusion, Jinge New Materials may indeed have its own accumulation in the field of functional materials and ranks high in market share. However, after carefully reviewing the content of the two rounds of inquiry letters, several key issues warrant questioning: How strong is their pricing power? Are procurement prices entirely fair? Is there sufficient market demand to absorb the additional capacity?

These issues are not unique to Jinge New Materials; many companies undergoing IPO reviews face repeated questioning during the audit stage. However, the difference lies in whether a company can provide solid answers or remains relatively vague. Based on the information disclosed in the inquiry letter, Jinge New Materials still needs to provide clearer responses.

Jinge New Materials is still in the process of its IPO review, and we will have to wait and see how it ultimately turns out. Regardless, the questions raised and the corresponding responses themselves already provide valuable clues for understanding the true nature of a company.

Disclaimer: This report is intended solely for clients of the Times Business Research Institute. The company does not regard any recipient of this report as a client simply by virtue of receiving it. This report is prepared based on information that the company believes to be reliable and publicly available, but the company makes no guarantees regarding the accuracy or completeness of such information. The opinions, assessments, and forecasts contained in this report reflect only the views and judgments as of the date of publication. The company does not guarantee that the information contained in this report remains up-to-date. The company may modify the information contained in this report without prior notice, and investors should independently monitor any updates or changes. The company strives to present objective and impartial content in this report; however, the views, conclusions, and recommendations contained herein are for reference only and do not constitute an offer or solicitation to buy or sell any securities. Such views and recommendations do not take into account the specific investment objectives, financial situation, or particular needs of individual investors and at no time constitute personalized investment advice. Investors should fully consider their own circumstances and comprehensively understand and utilize the content of this report and should not regard this report as the sole factor in making investment decisions. Neither the company nor the author assumes any legal responsibility for any consequences arising from reliance on or use of this report. Within the scope of their knowledge, neither the company nor the author has any legally prohibited interest in the securities or investment targets referenced in this report. To the extent permitted by law, the company and its affiliated entities may hold positions in the securities issued by companies mentioned in this report and engage in trading, or they may provide or seek to provide related services such as investment banking, financial advisory, or financial products. The copyright of this report belongs exclusively to the company. Without the written permission of the company, no institution or individual may infringe upon the company's copyright by reproducing, copying, publishing, quoting, or redistributing this report in any form. If the company grants permission for citation or publication, the report must be used within the allowed scope, with proper attribution to 'Times Business Research Institute,' and no alterations, omissions, or modifications may be made that distort the original intent. The company reserves the right to pursue relevant responsibilities. All trademarks, service marks, and logos used in this report are the property of the company.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment