[Publishing orders] The market is ups and downs, did your options make or lose?

OptionsSir Breaks Down Hot Topics | PLTR Again Caught in Tug-of-War: Valuation Correction or Market Misjudgment?

$Palantir (PLTR.US)$ The stock price fell 7.3% on Thursday, marking the second consecutive day of sharp declines.The direct catalyst for this pullback is related to Michael Burry's latest negative comments.Burry recently stated on social media that Anthropic is 'eating Palantir’s lunch.' These remarks quickly gained traction (and were later deleted), causing PLTR to drop about 8% on April 9 and hit its lowest closing level in over a month.

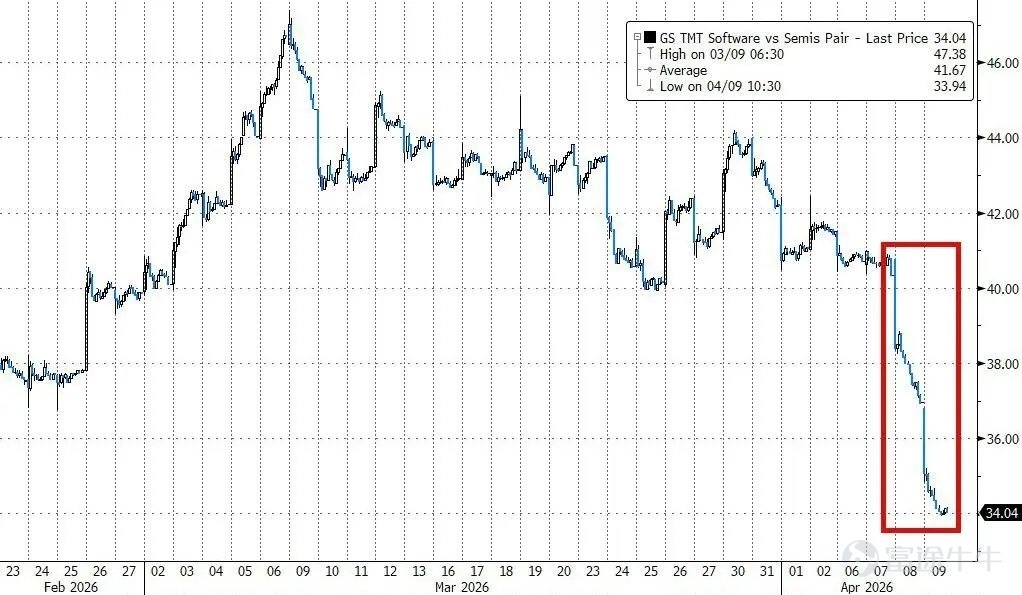

However, attributing this decline solely to bearish comments would be incomplete. The bigger picture is that the market is reassessing the valuation logic of the entire software sector amid rapid AI iteration. Concerns over the impact of Anthropic’s latest model update have caused the S&P 500 Software & Services Index to fall 25.5% year-to-date. On the trading front, the ratio of Goldman Sachs’ software-to-chip basket of stocks plummeted 15% over the past two days.After the US-Iran 'ceasefire,' the market quickly reverted to pre-war logic: chip stocks rebounded sharply while software stocks continued to plunge.

Why does Palantir always attract short sellers? A longer-term perspective makes it clearer.

Looking back, Palantir didn’t just start attracting short sellers recently.Almost since its initial public offering, it has been in a difficult position of having 'a story around fundamentals but also valuation controversies.'

The first typical shock occurred at the end of 2020. After the company’s direct listing, its stock price surged rapidly. Citron Research publicly shorted it, calling PLTR 'no longer a stock but a casino.' Subsequently, Palantir plummeted 17.6% intraday, with short interest rising to 8.2% of the float. Morgan Stanley simultaneously downgraded the stock to 'Reduce,' citing excessive deviation from its software peers in terms of valuation. The logic behind that round was straightforward: the stock had risen too fast in the short term, prompting bears to challenge the valuation and trading sentiment.

A few years later, a similar storyline hasn't disappeared, it has just shifted to a new backdrop. By 2024, the market's divergence over Palantir had further escalated. In January, Jefferies downgraded Palantir from 'Hold' to 'Underperform,' bluntly stating it was 'overhyped by AI.' In March, Monness downgraded it to 'Sell,' criticizing its valuation as 'outrageously high.' Then in May, although Palantir raised its full-year revenue guidance, it still failed to meet overly high market expectations, causing its stock price to plummet 15.1% in a single day, marking the largest one-day drop since 2022. The company’s data wasn’t bad; the issue was that the market had already set expectations too high.

Entering 2025, this debate hasn’t vanished, but rather been amplified by even higher stock prices. In November, after Burry disclosed his bearish bet on Palantir through regulatory filings, PLTR fell another 6%, while the market valuation at the time had reached nearly 250 times forward earnings.

Figure 1: Key negative milestones for PLTR and stock price reactions

What the shorts truly seized upon was not an issue with Palantir’s business but rather its valuation problem.

From this perspective, the shorts’ criticism of PLTR isn’t complicated and could even be said to have not fundamentally changed over the years:

First, the valuation is too high;

Second, the market leaves little room for error; any slight dip below the most optimistic expectations can easily trigger a selloff.

From 2024 to 2026, Palantir repeatedly traded at valuation multiples far above its peers. For assets like this, what the market is often most sensitive to is not 'poor performance' but 'performance that isn’t impressive enough.'

The post-earnings pullback in May 2025 best illustrates the issue. That quarter, the company reported revenue growth of 39% year-over-year to $883.9 million, with U.S. government revenue growing 45% year-over-year, and full-year revenue guidance was revised upward to between $3.89 billion and $3.9 billion. By standard growth stock metrics, this was not a poor earnings report. Yet the market still reacted with a decline of over 13%, because 'good' was no longer good enough—it had to be 'exceptional.'

For Palantir, this environment is particularly sensitive.Because what's easiest to magnify has never been 'the company is not good enough,' but rather 'the stock price is too expensive.'Once new competitive narratives emerge externally or new valuation pressures arise within the industry, Palantir often becomes the first target for selloffs. This is a recurring scenario that has played out repeatedly over the past few years.

What Anthropic is tapping into now is exactly the layer where enterprises are most willing to pay: general AI capabilities plus improved development efficiency.Anthropic has been advancing very rapidly on the enterprise side in recent months.If AI models themselves continue to improve, a portion of the 'intelligence layer' that Palantir has traditionally charged for will be compressed.。The essence of this round of declines in software stocks is that the market is beginning to worry: as Anthropic releases stronger new models, much of the value that traditional software companies have packaged through workflows, rule engines, knowledge retrieval, and decision support could be partially absorbed by stronger foundational models.

Anthropic is transitioning from being a 'model company' to becoming an 'enterprise product company,' which will directly encroach upon Palantir’s territory.This is because one of the most compelling aspects of Palantir has been that it doesn’t just sell models, but rather the entire capability of 'integrating AI into real business processes.' If Anthropic starts to fill this gap itself, the boundary between Anthropic and Palantir will become even more blurred.

Figure 2: PLTR Valuation Snapshot (Key points in time as reported by the media)

Why are the bulls always reluctant to concede easily? Because Palantir is not just about the story.

If we only look at valuation, Palantir naturally appears risky;but if we only consider valuation, it’s also easy to underestimate this company. The reason it repeatedly becomes the focus of both bulls and bears is not because it only has imagination, but because it has delivered a very strong growth performance over the past two years.Anthropic is indeed eroding part of Palantir's value proposition, but claiming that it has already 'eaten Palantir's lunch' is clearly premature.

The company's Q4 2025 earnings disclosed in February 2026 showed quarterly revenue growth of 70% year-over-year, reaching $1.41 billion; U.S. government revenue grew 66% year-over-year to $570 million; the company provided 2026 revenue guidance indicating a year-over-year increase of approximately 61%. Official materials also revealed that full-year 2025 revenue reached $4.475 billion, a 56% year-over-year increase; U.S. revenue grew 75% year-over-year to $3.32 billion; and U.S. commercial revenue for the full year increased 109% year-over-year to $1.47 billion.Whether looking at growth rates or scale, this is not a company 'propped up by sentiment.'

Figure 3: Core Growth Metrics Underpinning the Bullish Thesis

In government, defense, and high-compliance scenarios, Palantir’s moat doesn’t primarily stem from its models but from deployment, permissions, auditing, and certifications.The DISA authorization Palantir obtained in February and the official introduction of PFCS Forward both emphasized that its complete software stack can achieve 'authorize once, deploy everywhere' in IL5/IL6 environments. Such capabilities are certainly related to how advanced models are, but they won’t automatically disappear just because Anthropic’s models are stronger. For many government clients, what’s truly hard to acquire isn’t Claude itself, butthe systems engineering capability that allows Claude to operate safely, compliantly, and continuously in sensitive environments.。

Palantir’s official documentation shows that AIP supports models from providers such as xAI, OpenAI, Anthropic, Meta, and Google. This means that theoretically, Palantir is not in an 'either-or' relationship with Anthropic, but rather treats Anthropic as one of the model suppliers on its own platform.Under this logic, the stronger Anthropic becomes, the less it necessarily hurts Palantir; instead, it may enhance the overall attractiveness of Palantir's platform because clients can access stronger models within the Palantir framework.

This is also why the bearish argument against Palantir hasn't been decisive. It’s not the kind of speculative stock that collapses easily. The barriers provided by government clients, the expansion of domestic business in the US, and the implementation of AI platforms on the enterprise side are all very real factors.Even during the period when its valuation was most controversial, Palantir did not experience the kind of fundamental collapse often seen in 'highly valued growth stocks.'On the contrary, even as its performance continued to exceed expectations, the market still focused on questioning its valuation.

Another important detail is that as of March 13, 2026, the short position in PLTR was approximately 52.61 million shares, representing 2.41% of the free float. This indicates that Palantir is not currently a 'highly shorted stock' under prolonged pressure from significant short sellers. Instead, it resembles apopular growth stock that, due to its expensive valuation, is prone to rapid deleveraging at the slightest hint of trouble.a popular growth stock.

Is this a case of unjustified selling, or is it a return to high valuation norms?

In the short term, the focus is on the heavy pressure from negative catalysts affecting its valuation. However, in the medium term, the core issue remains: Can it continue to grow fast enough to justify its high valuation? It has not yet reached the point where it can simply be defined as a 'bursting bubble.'

Palantir is indeed expensive, and obviously so. But at the same time, Palantir is not a stock driven purely by sentiment without any materialization of results. Its problem does not lie in a lack of growth but rather in the market pricing, which demands that it consistently exceed expectations. As long as it can continue to prove itself in the coming quarters, this decline appears more like volatility in a high-valuation environment rather than a refutation of its long-term fundamentals.

From a technical perspective, examining the moving average system reveals that the current stock price (USD 130.6) has fallen below all commonly used moving averages, forming a bearish alignment pattern. On April 9, trading volume surged to 92.3614 million shares, the highest level in nearly a month, indicating heavy selling pressure and significant market divergence during the decline. Several medium- and short-term momentum and oscillation indicators are showing strong oversold signals. The lowest price on April 9, at USD 128.47, broke through the lower Bollinger Band significantly, suggesting the price is in an extreme volatility range.

In the options market, implied volatility for PLTR has risen sharply amid the stock price decline, reaching 70.25% on April 9, far above the historical volatility (HV). Its IV Rank percentile stands at 79%, meaning the current implied volatility is higher than 79% of levels over the past period, making option prices relatively 'expensive.' Put options remain actively traded but not imbalanced, with the Put/Call Ratio at 0.84, indicating no extreme consensus on bearish expectations in the overall market.

Overall, there is room for a technical rebound, but signs of a trend reversal have yet to emerge. Aggressive traders may consider opportunities in oversold rebounds but must set strict stop-losses. Conservative investors should wait for clearer bullish signals, such as a surge in volume breaking above key moving averages or sustained capital inflows, or further valuation adjustments before making decisions.

(1) If you still remain optimistic and plan to buy at a lower price after a pullback

In this scenario, if you continue to be optimistic about PLTR's performance, choosingCash-secured Putto opportunistically bottom-fish may be more appropriate.

The essence of this strategy is a 'cash-secured Short Put' approach. If by expiration the stock price is above the strike price, the put option will not be exercised, and you can pocket the entire premium. If the stock price falls below the strike price, you can purchase the corresponding number of shares at the pre-set price.

However, it’s important to note that selling puts requires sufficient margin. Carefully manage your position size; just because you can sell a certain number of puts doesn’t mean you’ll necessarily be able to take delivery of the same amount. Therefore, set the number of puts sold based on how much you can actually take delivery of, leaving enough buffer space. Otherwise, failure to do so could trigger account risk controls and result in forced liquidation before expiration, which would be counterproductive.

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

(2) If you already hold a long-term position but expect a short-term pullback

Buying Put options is a good approach, but at this time, due to the high volatility, the cost of buying Puts is also relatively high. YouBullish in the long term, aiming to profit when PLTR's share pricerises or moves sideways, while still wanting to hedge against the possibility of a sharp drop in the stock priceHedging protection. In this case, you can use the Long Collar strategy: while holding the underlying stock, use 'buying Puts' to hedge against the downside risk of the stock. Use the income from 'selling Calls' to offset part of the cost of buying Puts, thereby achieving the purpose of hedging risk at a lower cost.

The trade-off is giving up some upside potential, making it suitable for investors who are heavily invested in the stock, already have profits, or are deeply stuck but worried about earnings risks. The strike price of the Put should be chosen based on where you want to set your floor, while the strike price of the Call depends on where you're willing to cap your upside gains.

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

(3) If your final position leans more towards being bearish, and you believe PLTR needs more time to digest its high valuation

, you might consider using a Bear Put Spread strategy. The reason is that the current implied volatility (IV) is not low, so directly buying naked Puts could expose you to two risks: one, the stock price may not fall as quickly as you expect; and two, even if it does fall, volatility may not rise significantly further. Using a spread strategy essentially acknowledges that 'PLTR might not crash unilaterally but could instead decline in a staggered manner,' which makes the risk-reward ratio more appropriate for the current environment.

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

Finally, Option Sir brings a small perk for fellow investors, welcome to claim it.Options Beginner Pack

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Market conditions are complex and volatile,Options strategyOverwhelmed by choices? Futubull helps you build a portfolio in three steps.Options strategymaking investing simple and efficient from now on!

Option Risk Warning:An option is a contract that grants the holder the right, but not the obligation, to buy or sell an asset at a fixed price on a specific date or at any time before that date. The price of an option is influenced by various factors, including the current price of the underlying asset, the strike price, time to expiration, and implied volatility. Implied volatility reflects the market’s expectations for the level of volatility in the option over a future period. It is a data point derived inversely from the Black-Scholes option pricing model and is generally regarded as an indicator of market sentiment. When investors anticipate greater volatility, they may be more willing to pay a higher price for options to hedge risks, resulting in higher implied volatility. Traders and investors use implied volatility to assess the attractiveness of option prices, identify potential mispricings, and manage risk exposure.

Disclaimer:This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee for any securities, financial products, or tools. The risk of loss in trading options can be substantial. In some cases, losses may exceed the initial margin deposited. Even if you set contingent orders such as 'stop-loss' or 'limit' orders, these may not prevent losses. Market conditions may prevent these orders from being executed. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any shortfall in your account. Therefore, before trading, you should study and understand options and carefully consider whether such trading is suitable for you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures for exercising options and the rights and obligations upon exercise and expiration. Option trading involves extremely high risks and is not suitable for all investors. Investors should read carefully before engaging in any options trading strategy.Characteristics and Risks of Standardized Options。

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

39

58