鳴鳴很忙上市後首份年報,市場該怎麼看?

過去一年,港股新消費板塊熱度很高,市場對新消費公司的要求也明顯提高了。投資者不再只看收入增速,更關注增長背後的質量:增長能不能持續,利潤率能不能提升,商業模式能不能穿越週期。

前天,鳴鳴很忙披露了上市以來的首份年報。相比單純看收入和門店數,我認爲這份業績更值得關注的,是公司在持續擴張過程中,門店運營效率和盈利能力已經展現出同步提升。

畢竟,對一家仍在快速擴張的零售公司來說,只有把店開得更好,後續的擴張才能走得更穩、更遠。

一、開好店,才能開更多店

如果只看最表層的數據,這份年報本身已經足夠亮眼。

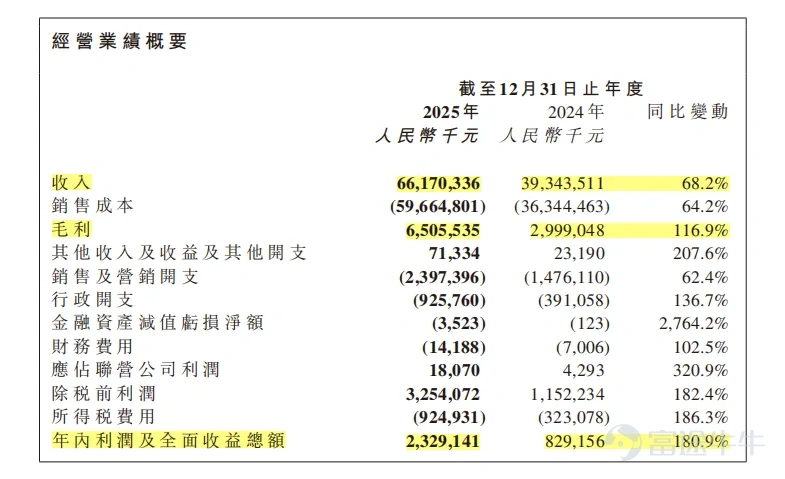

2025年,鳴鳴很忙門店 GMV 爲 935.69 億元,同比增長 68.5%;收入爲 661.70 億元,同比增長 68.2%。截至 2025 年末,門店總數達到 21,948 家,較 2024 年末的 14,394 家增加了 7,554 家。

這份業績最重要的信號是,鳴鳴很忙已經開始展現出更強的經營槓桿。對一家擁有兩萬多家門店的公司來說,當利潤率改善時,對應的規模效應就會非常可觀。

「根據管理層的表態,2025年門店盈利性達到歷史最好水平,而今年的同店表現或將優於2025年。」

在這次業績前,市場一直擔心,隨着門店規模擴大,門店的收入和盈利能力會受到攤薄,這也是不少連鎖消費公司擴張過程中常見的擔憂,但目前我在鳴鳴很忙上還沒看到。

對一家門店規模已經超過兩萬家的量販零食企業來說,這一點尤其難得。

除了收入和門店數,利潤率同樣取得了積極變化。

2025年,鳴鳴很忙的毛利率提升至9.8%,較2024年的7.6%提升了2.2%。

雖然從表面上看,毛利率的提升幅度似乎不算特別大,但這對於當前公司的門店規模來說,這個經營槓桿是非常明顯的。

比如,我們從去年的利潤水平來看。

2025年,公司年內利潤達到23.29億元,同比增長180.9%;經調整淨利潤爲26.92億元,較2024年的9.13億元大幅增長。

這背後的原因主要有兩點:一是公司通過直接向廠商採購,減少中間環節,隨着採購規模提升,對上游的議價能力進一步增強;二是供應鏈、倉儲、物流和數字化體系的協同效率持續提升。與此同時,產品結構的優化也可能對毛利率改善起到了積極作用。

利潤增速顯著快於收入增長,這說明鳴鳴很忙已經不只是單靠擴店帶來的收入增長,而是在規模擴張的同時,存量門店的盈利水平也在提升。

更重要的是,這種增長並不是建立在激進的財務槓桿之上,反而體現出財務結構在持續改善,開始進入更健康的正循環。

從財務上看,到 2025 年末,公司現金及現金等價物爲 37.37 億元,連同受限制現金合計 37.44 億元,同比增長約 90%;資產負債率從 43.7% 降至 35.8%;截至年末沒有計息銀行借款。

如果進一步看資產負債表裏的細項,這種改善其實更清楚。首先,預付款項、按金及其他應收款項從 2024 年末的 23.41 億元降至 2025 年末的 19.36 億元,同比下降 17.3%,公司在年報中明確解釋,主要是因爲向供應商支付的採購預付款減少,背後反映的是其對預付款項管理更積極。

同時,貿易應付款項及應付票據也從 14.95 億元降至 11.77 億元,同比下降 21.3%。年報將其歸因爲公司加強了對應付賬款及應付票據的管理措施。換句話說,公司並沒有通過拉長賬期來支撐擴張,反而是在擴張過程中同步優化了對上游結算節奏的管理。

根據管理層的表態,即使今年規模持續擴張,絕對額有增加,但整體費用率基本保持不變,後續仍有優化的空間。

對於一家仍在快速擴張的零售公司來說,收入利潤高增長,資產負債表還在改善,後續還有改善空間,這在同類的零售企業中並不多見。

二、兩萬家門店的效率外溢

在鳴鳴很忙上市前,很多投資者都好奇,這樣的低價模式是如何成立的,以及公司又是如何在低價之下實現盈利的。

量販零食這個行業,表面上看是在賣便宜零食,甚至有的產品價格便宜的讓消費者不敢相信,但本質上拼的並不是「便宜」,而是背後的供應鏈效率。

鳴鳴很忙通過直接向廠商採購,減少了中間環節。依靠大規模採購形成更強的議價能力,再通過數字化、倉配和加盟管理,把這些能力最終傳導到門店和消費者端。

截至 2025 年末,公司已與超過 2,500 家廠商建立合作關係,擁有 56 個倉庫,總面積約 123.2 萬平方米;門店通常位於距最近倉庫 300 公里範圍內,一般可實現 24 小時內配送;數字化團隊共有 432 人,系統覆蓋門店管理、供應鏈、庫存控制和加盟體系等關鍵環節。

這些數字單看可能不如收入和利潤那麼直觀,但這些背後看不見的投入,決定了鳴鳴很忙爲什麼能夠做到「高質價比」,這也是鳴鳴很忙能夠持續提供高質價比商品的基礎。

因爲所謂質價比,絕不是單純把價格壓低,而是通過直採、倉配、補貨和管理效率,把原本損耗在鏈條裏的成本節省下來,再把省下來的錢還給消費者。

而我們從消費者的角度就看到「產品便宜、選擇更多、上新更快」,但背後真正起作用的是供應鏈的持續優化,以及組織能力的累積。

這其實也是量販零食行業的特點。

規模越大,議價能力越強;議價能力越強,質價比越好;質價比越好,消費者需求越強;消費者需求越強,門店網絡和規模效應就會進一步放大。這個過程本質上是一個效率外溢、需求放大、利潤釋放相互促進的良性循環。

三、未來鳴鳴很忙該如何定位?

結合上述幾個角度來看,我認爲接下來應該轉變下對鳴鳴很忙的理解。

從投資者的角度上看,市場未來對鳴鳴很忙的理解,可能不應再只停留在「量販零食門店還能開多少家」這一層面,而要更多把它看作一張已經具備全國化覆蓋能力的高效率零售網絡。

市場未來看鳴鳴很忙這樣的量販零食企業,可能會依據開好店才能多開店的理念,逐步從「門店擴張邏輯」轉向「擴張發展與注重運營質量效率並重」。

而從消費者的角度看,鳴鳴很忙所提供的,不只是零食本身,而是一種高頻、低門檻、貼近社區生活的消費供給,滿足的是日常化、輕決策的小額消費需求:離家近、價格友好、選擇豐富、上新夠快。

也正因爲如此,鳴鳴很忙的門店網絡才能深入縣城、鄉鎮和社區街邊,逐步形成一種貼近大衆生活場景的零售觸達能力,這是跨越週期的「普惠零售」,在任何時代都需要。

從這個意義上說,它對消費者而言,越來越像一個社區型消費入口,而不只是一個單純賣零食的品牌。

從門店分佈來看,截至 2025 年末,公司門店達到 21,948 家,覆蓋全國 30 個省份和所有城市等級,其中約 60% 位於縣城及鄉鎮,覆蓋 1,401 個縣,對全國縣城覆蓋率約 75%。

未來一二線城市的門店數量仍有擴張空間。隨着消費者對高質價比零食渠道的認知逐步加深,這類門店也有機會形成更強的消費粘性。

多家券商今年 3 月發佈的深度報告也都還在強調,全國理論開店空間仍然不小,有研究按湖南成熟市場爲錨測算,全國理論開店空間約 10 萬家;也有賣方認爲,2024 年中國量販零食飲料零售市場規模約 1297 億元,到 2029 年有望達到 6137 億元,仍處於高成長賽道。

結語

在首份年報披露後,市場對鳴鳴很忙的業績表現以及今年繼續擴張的指引整體反應較爲積極,股價也已有所上漲。

雖然近期市場因地緣衝突的擾動,大市的表現偏弱,但在後續市場的風險偏好回升後,相信市場能逐漸發生公司的基本面已經出現了較大的改善,市場對增長的疑慮被打消,當新消費的行情再來時,相信公司會有較好的表現。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論

發表評論