Goldman Sachs In-Depth Analysis: Can the software industry’s moat withstand the AI wave?

Image Source: techorange

Last week, Pando provided an in-depth analysis of the impact of AI on the software sector and how to respond from an investment perspective. This week, Pando has selected the latest analysis from Goldman Sachs Research, guiding you through a systematic breakdown of the seven major 'bearish arguments' targeting software stocks. Through logical reasoning and risk scoring, investors can better assess which software stocks have had their foundations shaken and which ones are being unduly punished.

In the software sector pullback at the beginning of 2026, market focus has shifted from short-term demand fluctuations or interest rate impacts to deeper 'endgame valuation' issues—whether the moats of software are being eroded by AI and whether business models will be disrupted.

In this report, Goldman Sachs pointed out that the current core of market discussion is no longer about 'next quarter’s growth rate,' but rather 'will this company still exist ten years from now.' This anxiety mainly stems from the rapid evolution of AI technology, particularly the rise of Agentic AI, which is reshaping the value chain of enterprise software. Goldman Sachs systematically addresses the seven most controversial bearish views in the current market, providing risk scores from 1 to 5, while also screening for companies with 'architectural moats.'

Source: Goldman Sachs Global Investment Research

1. Will AI trigger a 'complete overhaul,' uprooting existing core systems? Risk Score: 1

Image Source: aishield

Bearish View:

New AI-native players will solve core enterprise data storage problems in entirely new ways, sparking a 'complete overhaul' movement that renders today's core system (System of Record, SoR) companies obsolete.

Goldman Sachs View:

The risk is extremely low. Generative AI is essentially an analysis and generation engine, not a trading engine. Existing core systems (such as ERP, CRM, and HR systems) serve as the foundational base for AI operations, providing structured data accumulation and historical context. AI models require massive amounts of high-quality, verified data for training and operation, and this data is precisely stored in existing Systems of Record (SoR). For instance, in financial planning and analysis, AI must extract accurate financial historical data from audited and reliable ledgers; sales analysis AI needs to correlate call content with customer data in CRM or ERP systems to generate meaningful insights. Data does not migrate easily but instead creates 'data gravity'—as data accumulates in existing systems, it attracts more applications and services, further enhancing the value of these systems.

You are trained on data up to October 2023.

Goldman Sachs believes that even in a reasonably bearish scenario, the value of application software in the technology stack may indeed compress to the value of SoR, but the value of SoR itself is not zero, which provides support for valuation.

AI tools will 'hollow out' application value, leaving existing software as mere infrastructure? Risk rating: 4

Bearish perspective:

New AI tools sit atop existing software stacks, capturing incremental value. While SoR remains necessary for data storage and compliance, they will increasingly act as infrastructure rather than primary value creators. Today's application software leaders have limited exposure to growth but are overly exposed to risks such as reduced seat counts or commoditization.

Goldman Sachs perspective:

The risk is higher, but not all companies will lose. Goldman Sachs believes that the risk posed by AI is more about 'value abstraction' rather than complete replacement. As Agentic systems mature, intelligence is being moved out of SoR into an orchestration layer capable of cross-system reasoning, API calls, and autonomous workflow execution. In this architecture, the role of SoR is to reliably store and expose data, while decision-making, prioritization, and workflow logic reside elsewhere. This weakens the traditional moat of SoR related to UI, workflow ownership, and user habits. However, the key lies in domain expertise and contextual understanding.

Goldman Sachs expects that some established companies will be able to prove to customers that their domain expertise can deliver better AI outcomes, provided they have cleared technical debt, maintained a dynamic tech stack, and innovated as fast followers. As Microsoft pointed out, customers staying within its ecosystem can benefit from lower latency, real-time data, and more contextual advantages.

You are trained on data up to October 2023.

HubSpot believes that AI performs poorly in business use cases due to a lack of context—models trained on the internet do not understand specific businesses. Datadog, on the other hand, demonstrated a small model trained on its internal data, which can provide higher accuracy than leading-edge models at a lower cost. Players who master 'context' can still control pricing power.

3. Will the moat of vertical software be 'crushed' by horizontal AI products? Risk score: 2

Bearish perspective:

The continuous improvement of general AI models is penetrating industries traditionally reliant on vertical software. For instance, Palantir has partnered with AIG to leverage Anthropic for insurance use cases, while Intuit launched GenOS to allow customers to create vertically-specific workflows within QuickBooks. If horizontal AI agents can integrate into existing data and systems to replace rule-based workflows, the pricing power and profit pool of vertical software will face erosion.

Goldman Sachs perspective:

Vertical software possesses four structural barriers that are difficult for horizontal AI products to penetrate in the short term.

First, the exclusivity of proprietary data: Take Guidewire as an example. Its customer base covers over 500 insurance companies, managing approximately $775 billion in property and casualty insurance premiums, accumulating massive historical data that AI newcomers cannot obtain from public sources for training.

Second, deep integration into business processes: Vertical software is often the core of daily operations, becoming a mission-critical system within the industry, understanding historical patterns and operational characteristics of businesses, making replacement costs extremely high.

Third, the irreplicability of brand reference value: In high-trust industries such as healthcare, public sectors, and financial institutions, brand reputation and successful case studies are key factors in customer procurement decisions, which new players cannot build in the short term.

Fourth, compliance thresholds in highly regulated industries: As Via Transportation mentioned, participating in public sector tenders requires overcoming numerous regulatory obstacles, resulting in an average sales cycle of about 10 months. Goldman Sachs particularly emphasized that for deeply embedded vertical suppliers, customers are willing to give them several years (or even longer) to innovate and catch up with AI-native solutions rather than easily 'jump ship.' During Guidewire’s cloud transformation process, its on-premises customer base avoided following the trend to switch, and this patience was a crucial reason for its success as a market leader.

Source: iauro

4. Will the decline in coding costs and 'ambient programming' disrupt the software industry? Risk score: 2

Bearish perspective:

AI-powered programming tools significantly boost development efficiency, lower software development costs, and reduce entry barriers, which will give rise to numerous new competitors, eroding the moats of existing software companies.

Goldman Sachs perspective:

Goldman Sachs acknowledges that coding costs are indeed declining and will inevitably bring new entrants, but its assessment of this risk is relatively relaxed, assigning it a low score of 2. The core logic lies in the fact that 'writing code' and 'running a company' are two very different things.

First, software engineering is far more than just writing code. Engineers spend a significant amount of time on non-coding tasks such as design, debugging, risk identification, and code review. Over the past two decades, from manually managing memory to abstracting frameworks, tools have continuously evolved, yet the value of engineers has never diminished. No matter how powerful 'ambient programming' becomes, it cannot replace other stages of the software development lifecycle.

Second, the moats of software companies go far beyond the code itself. There are over 15,000 SaaS companies in the US, but only a handful achieve scalable success. Success requires much more than just an interface: data accumulation, accuracy, security, maintenance, workflow orchestration, ecosystem building, third-party integration, and go-to-market strategies – these capabilities cannot be replicated by AI-generated code in the short term.

Third, generated code still requires 'human-AI collaboration.' Faros’ research on 10,000 developers shows that teams with high AI adoption rates increase task completion by 21%, merge requests by 98%, but code review times also increase by 91%. While AI accelerates code generation, it may shift bottlenecks to the review and maintenance stages. In enterprise environments, there is no 'one-click solution' to bypass the complex code lifecycle.

Image source: New Intelligence Source

5. The future of software is 'customization.' Will the self-build wave disrupt SaaS? Risk rating: 3

Bearish view:

The decline in coding costs will drive companies to build their own customized software, shifting value upstream to infrastructure, model layers, or customization platforms like Palantir, while traditional SaaS providers become marginalized.

Goldman Sachs view:

Goldman Sachs believes that the decline in coding costs will not fundamentally alter the 'build vs buy' equation, although a portion of the market will indeed shift toward customized software. The core logic lies in the fact that maintenance costs and responsibilities accumulate over time, and specialized suppliers consistently lead in performance-to-cost frontiers compared to internal technology. Historically, SaaS achieved economies of scale through centralized R&D, making procurement cheaper and more reliable than building internally. AI is indeed changing this landscape, with internal teams now able to deliver code faster, making customized applications more feasible, especially when tailored to a company's specific processes rather than relying on 'good enough' standardized workflows.

Palantir is a quintessential example of this model: by embedding forward-deployed engineers (FDEs) within clients, they transform fragmented data into customized applications, achieving approximately 85% gross margins and growth rates exceeding 100%. However, Goldman Sachs argues that we may currently be at a localized peak in companies' willingness to build in-house, as established SaaS players are catching up by adding AI functionalities. Security and governance protocols continue to evolve, and ServiceNow has started winning budgets that were previously allocated to in-house builds. Many enterprises still value standardized applications for their compliance, security, and reliability advantages, particularly in regulated or mission-critical fields.

Source: YouTube

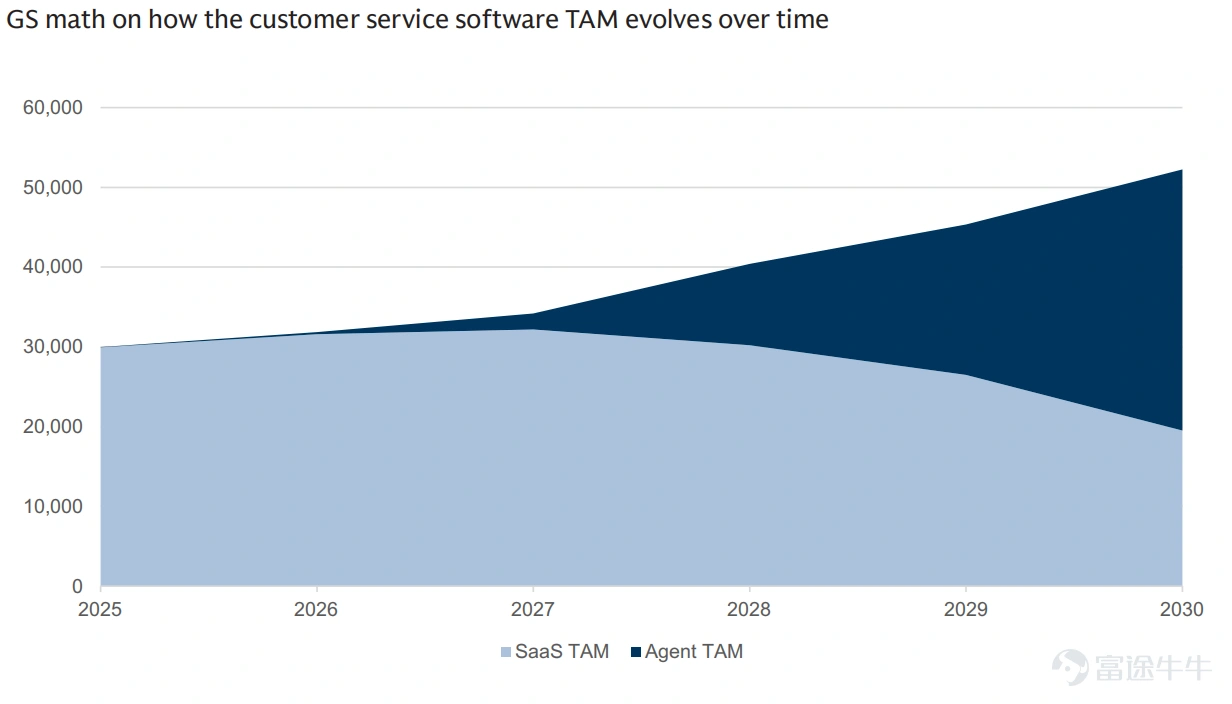

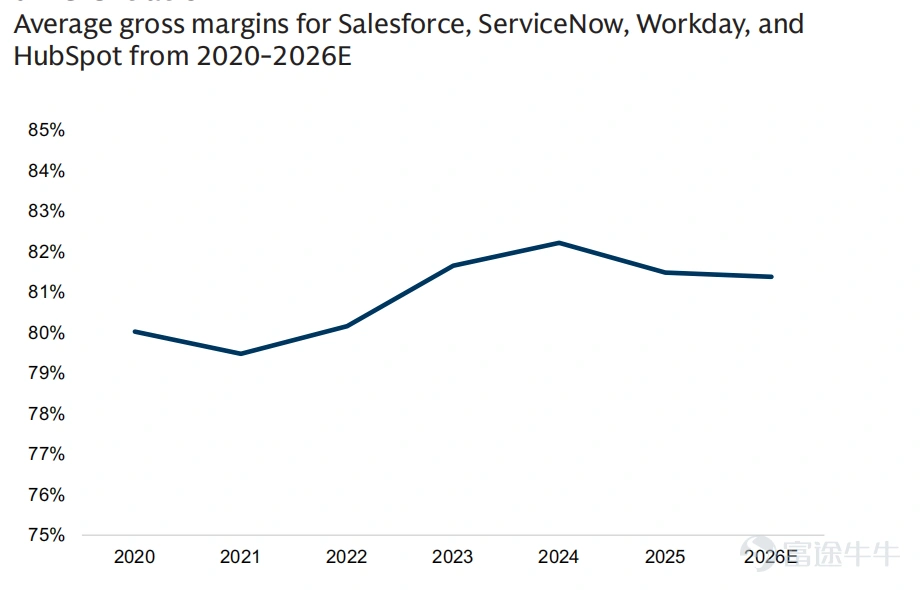

6. Is the era of high software gross margins coming to an end? Risk rating: 3

Bearish view:

The high gross margins of 70-90% in software are unlikely to be sustainable in an AI-dominated landscape. As competition intensifies, new entrants may deliver comparable or superior outcomes at lower cost structures. Meanwhile, the marginal production costs for existing vendors are rising from 10-20% (CPU hosting costs) to higher levels (GPU inference costs).

Source: Company data, Visible Alpha Consensus Data, Goldman Sachs Global Investment Research

Goldman Sachs' View:

Goldman Sachs expects moderate pressure on industry gross margins over the next 12-24 months as many companies prioritize customer adoption over monetization, choosing to absorb the costs of GPU inference and LLM API. However, for the industry as a whole, inference costs will decline over time relative to AI-related productivity value/volume. For any specific company, gross margin ultimately becomes a function of pricing power, which in turn depends on product differentiation. Established firms that can convert their domain expertise into higher-quality outcomes may hold an advantage.

Goldman Sachs points out that unlike the traditional SaaS model where the marginal cost of incremental usage is extremely low, AI capabilities translate directly into expenses, with token consumption, model complexity, and query frequency driving costs directly. This marks a structural shift from fixed-cost IP leverage to consumption-based economics. The positive aspect, however, is that inference costs should decline over time, and software may also capture share from service and labor pools; Intuit’s assisted tax solutions demonstrate how spending shifts from human tax professionals to software platforms. Ultimately, maintaining software gross margins depends on pricing power, which itself depends on product differentiation.

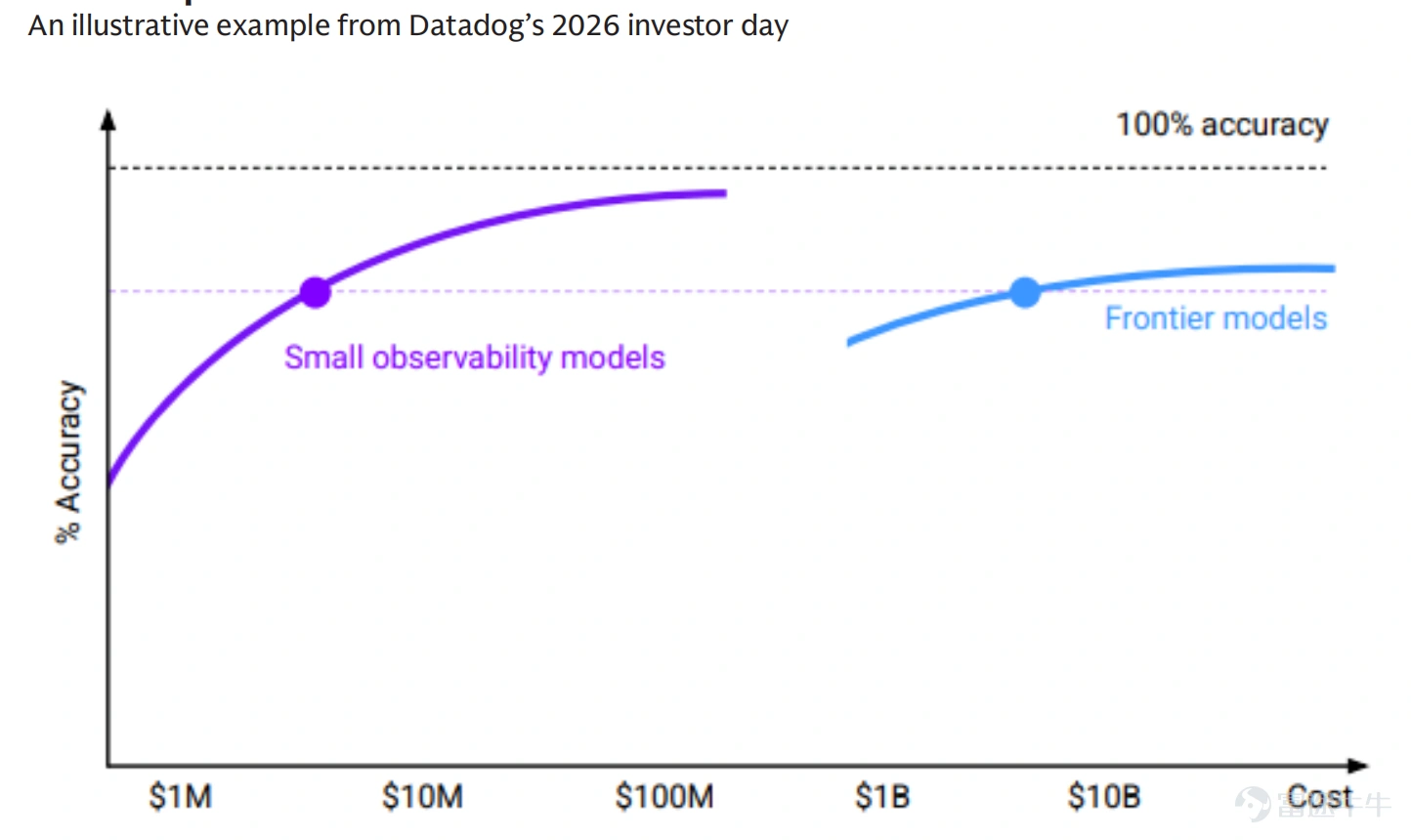

7. Technological changes are happening too fast, making the endgame unpredictable? Risk score: 5

Bearish Perspective:

The speed of technological iteration is astonishing, with major updates released this year by Anthropic, OpenAI, Google DeepMind, and Meta. The future shape of knowledge work, the structure of the software industry, and the terminal value of companies are filled with significant uncertainty, and uncertainty is a hallmark of low-valuation businesses.

Goldman Sachs' View:

Goldman Sachs frankly admits that this is the most challenging risk to plan for, hence assigning it the highest risk score of 5. Economies of scale remain in effect, and the technological frontier continues to advance, with GPT-5.2 and Claude Opus 4.6 achieving over 90% scores on the graduate-level reasoning test GPQA Diamond. At the same time, new application forms are also driving innovation: ChatGPT's breakthrough lies in 'packaging' rather than a model revolution; Claude Cowork allows non-technical users to participate in experiments through a GUI interface; OpenClaw may replicate ChatGPT’s development trajectory over the next three years. Microsoft MAI-DxO models have achieved an 85% pass rate in medical diagnostics (compared to single-digit rates for human experts), corresponding to a TAM of $500-2,000 billion; Google Deep Think has helped Duke University break through semiconductor manufacturing bottlenecks. These cases prove that uncertainty both suppresses valuation and breeds opportunities.

The biggest challenge comes from 'unknown unknowns.' In 1993, no one foresaw Web 2.0, and at the end of 2022, no one anticipated Claude Cowork. We are still living in the 'ChatGPT era,' but this could change in unpredictable ways. These 'unknown unknowns' make precise predictions about the future of AI impossible—not implying that negative outcomes are inevitable, but they do make them harder to rule out, which is the essence of uncertainty.

Summary:

Goldman Sachs believes that AI is not the terminator of software, but a touchstone and accelerator. The market is shifting from the 'straw man argument' (easily refutable viewpoints) to the 'iron man argument' (challenges that need to be taken seriously). The real winners will be companies that can deeply integrate data, context, product strength, and AI. Goldman Sachs particularly emphasizes that enterprises with an 'architectural moat' – meaning their competitive advantage extends beyond the application layer – are more likely to succeed in this new era. Investors should focus on software companies that can transform domain expertise into high-quality AI outcomes while maintaining technological innovation vitality.

Statement

This content is for reference only. It is neither an invitation nor an offer to buy or sell any securities or other financial instruments. Any information, including facts, opinions, or citations, may be condensed or summarized and is accurate as of the date of writing. Information may change without prior notice, and Pando Limited ('Pando') has no obligation to ensure you are notified of such updates. Investing in products mentioned in this content involves significant risk of loss and may not be suitable for all investors. Valuations may fluctuate, potentially resulting in substantial investment losses. Past performance is not indicative of future results. If an investment is denominated in a currency other than your base currency, exchange rate fluctuations may adversely affect value, price, or income. You should not engage in any investment unless you fully understand the nature of the transaction and the extent of potential losses. If you do not fully understand these risks, you must seek independent advice from your financial advisor. Under no circumstances should this content be interpreted as an express or implied commitment, guarantee, or suggestion by Pando or from Pando that you will profit or limit losses in any way. Investors should note that past performance is not indicative of future results.

Virtual assets are highly speculative and risky investments. Investors should exercise extreme caution when participating in these products. The legal status of virtual assets has not been clearly defined, which may affect the nature and enforceability of investors' rights in such virtual assets. Research reports on virtual assets have not been reviewed by regulatory authorities, and investors cannot benefit from the protection of an investor compensation fund. Virtual assets are not legal tender, and related transactions may be irreversible, meaning losses caused by fraudulent or unintended transactions may not be recoverable. The value of virtual assets stems from market participants' ongoing willingness to exchange them for fiat currency, implying that if the market for a particular virtual asset disappears, its value could be entirely and permanently lost. There is currently no guarantee that virtual assets will continue to be accepted as a means of payment in the future. The volatility and unpredictability of virtual asset prices relative to fiat currencies can lead to significant losses within a short period. Changes in legislation and regulation may also adversely affect the use, storage, transfer, trading, and valuation of virtual assets. Certain virtual asset transactions may only be considered complete once recorded and confirmed by a platform licensed by the Securities and Futures Commission, which may differ from the time the client initiated the transaction. The inherent nature of virtual assets makes them more vulnerable to fraud or cyberattacks. Technical malfunctions could also prevent clients of licensed platforms from executing virtual asset trades.

About Pando:

Pando is a licensed company providing virtual asset management services. As a participant in the digital asset management field, Pando has obtained Type 1, Type 4, and Type 9 licenses issued by the Hong Kong Securities and Futures Commission and is authorized to provide virtual asset-related services. Additionally, Pando has acquired public offering fund qualifications and has launched two actively managed ETF products and two passively managed virtual asset ETF products. Through strategic positioning, Pando has accumulated extensive experience in digital asset management and compliance, offering diversified investment solutions and attracting numerous investors.

Phone: +852 3891 3288

Address: Room 1408, Two Exchange Square, 8 Connaught Place, Central, Hong Kong

Email: media@pandofinance.com.hk

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1