和譽-B(02256):年報釋放持續規模盈利信號,商業化元年開啓全新增長空間

轉自:智通財經

淨利潤同比大增近100%,連續第二年實現年度盈利,在創新研發和BD交易的加持下,2025年的和譽-B(02256)再次用亮眼的年度業績,驗證了持續規模盈利的預期,向市場進一步傳遞了積極的配置信號。$和譽-B (02256.HK)$

淨利潤同比大增近100%,連續第二年實現年度盈利,在創新研發和BD交易的加持下,2025年的和譽-B(02256)再次用亮眼的年度業績,驗證了持續規模盈利的預期,向市場進一步傳遞了積極的配置信號。

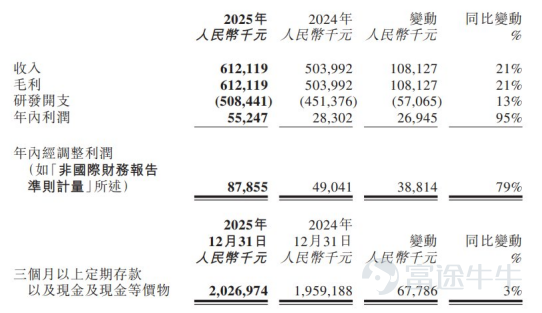

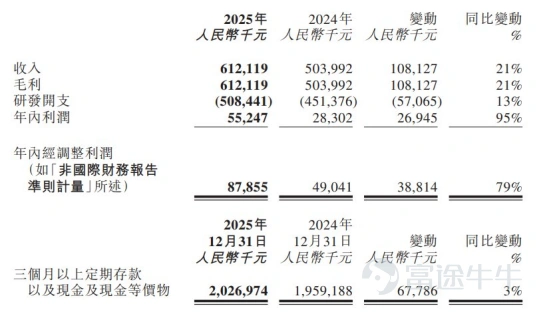

據智通財經APP了解,近日,和譽的2025年年度業績新鮮出爐。業績顯示,2025年,和譽實現年度綜合收入合計約7.22億元,同比增長19%;公司當期淨利潤達到5524.7萬元,同比大幅增長約95%;當期對應經調整淨利潤則達8785.5萬元,同比大幅增長約79%。這是繼2024年首次取得全年盈利之後,公司連續第二年實現全年盈利。

在實現持續性規模化的創新收益與盈利的同時,和譽的在手現金流也日益充沛,公司當期現金及銀行結餘資金達到20.27億元,爲公司中長期創新研發提供了可觀的資金保障。

而作爲港股18A中少數的持續通過股票回購「真金白銀」回饋投資者的創新藥企,和譽在2024年耗資6870萬港元累計回購2259.4萬股股份的基礎上,於2025年3月再次經公司董事會批准動用2億港元在市場上購回股份。截至2025年年末,公司累計購回1022.9萬股股份,佔年初已發行股份總數的1.51%,累計涉及資金8467萬港元。二級市場上,和譽2025年股價年度漲幅達到182.83%,正是市場信心與股東價值提升的真實寫照。

展望2026年,隨着核心品種貝捷邁®(鹽酸匹米替尼膠囊)的全球首個新藥上市申請在國內獲批,和譽迎來商業化元年的同時,也將步入“硬核創新-商業化變現-業績驗證”的全新價值循環模式中。

在貝捷邁®強勁商業化預期下,和譽後續大幅淨現金狀態同樣可期,從而推動公司創新研發踏上新臺階,爲未來公司估值持續上行突破奠定紮實的基礎。

「十億美元分子」商業化帶來高投資確定性

在當前環境下,一家創新藥企具備高投資確定性的重要標誌在於,將公司的現金循環支柱從融資現金流切換到經營性淨現金流。這便需要藥企擁有一款「現象級」現金牛產品作支撐。如今,貝捷邁®的正式獲批上市,爲和譽投資價值穩步增長提供了關鍵條件。

據智通財經APP了解,得益於貝捷邁®突出的「十億美元分子」潛力,和譽在2023年底就該藥與知名跨國藥企默克達成了一項「高首付、高里程碑、高分成」的BD交易,並在2024年初獲得7000萬美元首付款。隨着貝捷邁®研發與商業化進程的持續推進,2025年4月1日,默克再次宣佈行使全球商業化選擇權,支付8500萬美元鎖定匹米替尼全球權益。這也成爲和譽在2025年實現第二年年度盈利的直接驅動因素之一。

實際上,加上此次默克支付的行權付款,雙方的BD合作已爲和譽帶來逾1.5億美元現金。而根據此前協議,和譽後續還將獲得來自默克的研發里程碑付款及銷售里程碑付款,潛在付款總額可能高達6.06億美元,這還不包括兩位數的淨銷售分成。這些資金都將成爲公司後續的持續現金流,在2026年年度及後續爲和譽帶來明確的利潤兌現。

除了默克行權帶來的收益外,推動和譽後續投資確定性持續走高的更大動力,則來源於核心品種貝捷邁®的「十億美元分子」的全球商業化價值兌現。

去年12月22日,和譽公告宣佈,基於全球III期MANEUVER研究的積極數據,中國國家藥品監督管理局(NMPA)批准了貝捷邁®的全球首個新藥上市申請。而在今年1月13日,和譽再次宣佈貝捷邁®用於腱鞘鉅細胞瘤(TGCT)患者系統性治療的新藥申請(NDA)獲得了美國FDA正式受理,獲批上市在即。

貝捷邁®中美雙地上市,意味着這款「十億美元分子」即將踏出全球商業化的關鍵一步,也標誌着和譽迎來從開創性創新研究邁向首個產品全球商業化的關鍵里程碑。

從市場角度來看,匹米替尼主要用於治療不適合手術的TGCT。美國罕見疾病組織(National Organization for Rare Disorders)報告指出,TGCT發病率約43/100萬。目前市場上競品主要有第一三共的FIC產品Pexidartinib(培西達替尼),其作爲針對無法通過手術改善的重症TGCT的系統療法,2019年在美獲批上市,但該藥存在嚴重肝毒性並被FDA「黑框警告」。即便如此,培西達替尼的2023年營收依舊達到53億日元。

相較而言,匹米替尼已被持續驗證其針對腱鞘鉅細胞瘤在實現療效最佳的同時還能大幅改善安全性,因此在獲批上市後,隨着在多種適應症上治療空間不斷被挖掘,其全球商業化造血潛能有望加速兌現。

此前招商證券國際發表報告稱,和譽開發的匹米替尼是全球療效最優CSF-1R小分子。該行認爲默克對該分子寄予厚望,有望在全球做到接近15億美元高峰的銷售收入,進一步釋放自身「十億美元分子」潛力,成爲後續增厚和譽全球收入利潤的「重磅炸彈」,增高公司投資確定性。

加速差異化創新,FIC/BIC品種潛力凸顯

業績顯示,2025年,和譽確認研發投入達到5.08億元,同比增長13%。可見強勁收入增長與現金流儲備,爲公司帶來了創新研發端的強支撐。在強勁研發下,目前和譽正加速差異化創新,創新管線內多個FIC/BIC品種潛力凸顯。

近年來,和譽醫藥聚焦腫瘤精準治療與免疫治療,覆蓋EGFR、FGFR、CSF-1R,PMRT5等熱門靶點,已建立了22條具有全球競爭力的差異化創新研發管線,其中多款在研創新藥都具有「同類最優」或「全球首創」潛力。

例如,和譽管線內的第二款「十億美元分子」依帕戈替尼(ABSK011),目前已實現全球小分子管線進度領先,有望憑藉優異的有效性及安全性逆襲爲Global FIC/BIC藥物。

去年5月26日,和譽宣佈依帕戈替尼獲納入突破性治療品種,擬用於治療既往接受過免疫檢查點抑制劑(ICI)和多靶點酪氨酸激酶抑制劑(mTKI)治療失敗的FGF19過表達晚期肝細胞癌患者。這也是繼匹米替尼之後,和譽第二款獲納入突破性療法的重磅品種。而後同年12月,依帕戈替尼再獲美國FDA授予的FTD。

據GlobalData預測,到2029年,全球肝癌市場大約在53億美元左右,其中免疫療法約佔市場份額的72.2%,達到38億美元。參考此前已上市的小分子激酶抑制劑索拉非尼,其針對肝癌適應症的ORR不到20%,即便如此其在2021年全球銷售依然超過5億美元,側面反映出當前市場龐大的未滿足治療需求。

在此市場背景下,依帕戈替尼之所以有望成爲和譽第二款「十億美元分子」,其優勢在於成藥確定性高,作爲小分子相比其他FGFR4靶向藥具依從性和經濟性優勢,且在競爭格局中的領先地位。

繼去年6月完成依帕戈替尼用於治療既往曾接受全身治療且FGF19過表達的HCC患者的註冊性研究的首例患者給藥後,今年2月和譽還完成了全球多中心I期研究擴展階段首例美國患者給藥。目前依帕戈替尼已實現研發層面的「彎道超車」,有望成爲首個治療FGF19過表達HCC患者的突破性藥物,並存在潛在的重磅BD價值。

除了上述兩款具備「十億美元分子」潛力的核心品種外,和譽創新管線內還有多個具備潛在FIC/BIC產品。

智通財經APP觀察到,去年12月以來,公司多個管線內創新品種陸續刷新了研發里程碑。和譽相繼披露了其口服小分子PD-L1抑制劑ABSK043、口服小分子KRAS G12D抑制劑ABSK141和FGFR2/3抑制劑ABSK061的最新研發進展。

而在2025年年內,和譽早期候選藥物也繼續保持了強勁的推進勢頭。期內,公司獲得了6項新藥IND批准,其中ABSK141(KRAS G12D抑制劑)還同時獲得了美國FDA及中國NMPA的批准;此外,公司三項臨床前候選藥物ABSK211(Pan-KRAS)、ABSK191(CDK4/2抑制劑)及ABSK192(可入腦CDK4抑制劑)也已進入IND準備階段;雙抗ADC項目P020則推進至先導化合物優化階段;而在自體免疫及心血管代謝領域,公司還佈局了P151、P022及P023項目,早研管線擴展到非腫瘤領域,進一步豐富了自身創新研發管線。可見持續的研發端利好,正在爲和譽後續的內在價值加速釋放,積蓄強勁勢能。

小結

不難看到,在覈心品種商業化及充沛現金流支撐下,和譽正憑藉不斷完善的一體化創新閉環,在全球化研發、海外註冊以及國際商業化等多領域體系化競爭中向Biopharma方向加速躍遷。

基於對和譽未來增長的樂觀判斷,包括中金公司、申萬宏源和中泰證券等多家機構更新了對公司的研報,重申「買入」或「跑贏行業」評級。

其中,中金公司維持對公司「跑贏行業」評級並表示,2026年建議關注:匹米替尼美國上市進展、依帕戈替尼2L註冊臨床進展和1L臨床計劃、ABSK061、ABSK043的潛在數據讀出機會、早期分子包括ABSK131、ABSK141的開發進展等。根據DCF模型,該行維持跑贏行業評級和目標價20港元,較當前股價有近60%的上望空間。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論

發表評論