港股節後行情如何看?

智通特供|南向1.41萬億「壓艙」 韓國散戶「點火」——港股迎來定價權分層時代

2025年至2026年初,港股市場迎來兩股特徵迥異、但方向共振的增量資金——內地南向資金以1.41萬億港元的年度淨買入刷新歷史紀錄,成爲港股定價權的核心構建者;韓國散戶資金則以「東學螞蟻」式的集中押注、高槓杆交易及對前沿科技的極致追逐,在港股邊緣地帶掀起結構性浪潮。二者一者長線配置、價值爲錨,一者高頻交易、產業敘事驅動,共同勾勒出港股市場資金來源多元化、定價邏輯分層化的全新圖譜。

規模與結構:絕對主力與邊際鯰魚

南向資金與韓國股民在港股市場的資金體量存在顯著的層級差異,但其功能定位與市場影響力各具不可替代性。

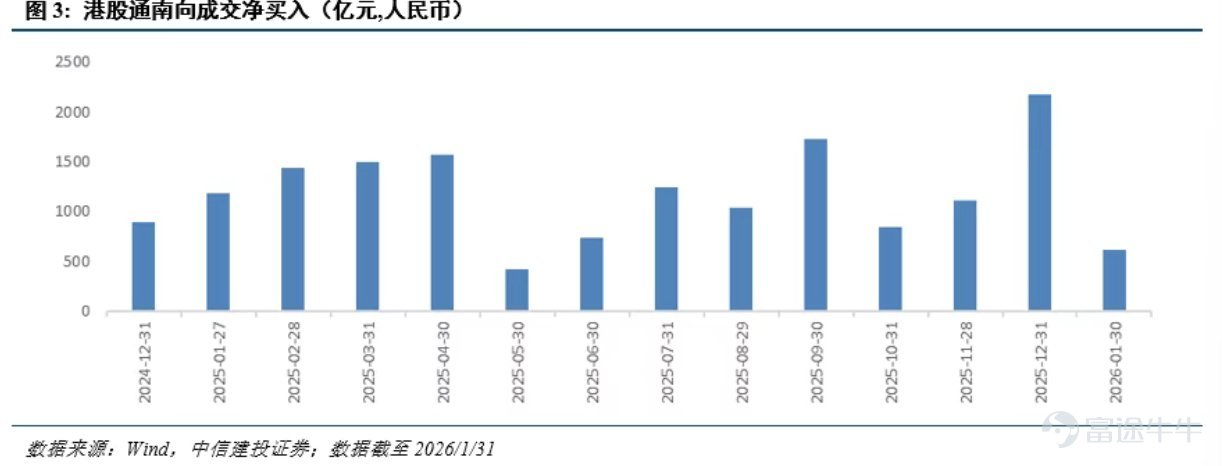

南向資金已確立爲港股市場的核心增量來源與估值體系重塑者。截至2025年末,南向資金累計淨流入達5.11萬億港元,2025年當年淨買入1.41萬億港元,規模接近2022至2024年三年總和。持倉市值突破6.3萬億港元,佔港股總市值比重升至12.7%。這一量級表明:南向資金已跨越「邊際補充」階段,進化爲港股市場的「內生定價變量」。

韓國股民在港股市場的資金體量相對有限。然而,其交易行爲具有高度集中性、槓桿化特徵顯著、決策形成呈現強社群同步效應,使其在特定標的——尤其是新經濟IPO、半導體產業鏈、人工智能主題龍頭——上能夠形成短期定價衝擊與流動性溢價塑造能力。2026年開年,韓國散戶單月淨買入MiniMax-WP逾2000萬美元,該股IPO錄得1837倍超額認購,韓國資金是上市初段估值溢價的重要催化力量。

行業偏好:價值錨定與成長銳度的分層配置

兩股資金在行業覆蓋維度呈現顯著的配置層級分化與有限的賽道共振,其背後映射的是資金屬性、收益目標與決策久期的根本性差異。

金融業與高股息公用事業是南向資金的「獨立配置域」。建設銀行(00939)、工商銀行(01398)、中國平安(02318)、中國移動(00941)、中國神華(01088)等標的獲南向資金百億級系統性增持,核心驅動因子爲高股息率、低估值分位、人民幣資產屬性及永續經營假設。韓國股民在該板塊近乎零持倉。

南向資金重倉阿里巴巴-W(09988)(1913億港元市值增量)、美團-W(03690)、騰訊控股(00700),配置邏輯由2024年的「估值修復」升級爲2025年的「價值重估」,持倉行爲呈現跨週期、低換手、左側累積的配置盤特徵。

韓國股民2025年重倉小米集團(01810)(8775萬美元淨買入),2026年開年迅速切換至MiniMax-WP(2067萬美元),其資金流向呈現高彈性、高換手、強敘事驅動的交易盤特徵。二者共享對中國科技龍頭的系統性看好,但在標的篩選與持倉久期上呈現顯著分形。

2025年,南向資金淨買入中芯國際(00981)5.08億股,持股市值增加360億港元,充當板塊定價的絕對主力;韓國股民同期淨買入3311萬美元,形成配置盤壓艙、交易盤助攻的雙層定價結構,共同推升板塊估值中樞。

2026年開年,韓國資金迅速向瀾起科技(06809)、英諾賽科(02577)及中國半導體ETF遷移,呈現產業細分賽道輪動與工具化配置;南向資金則延續對中芯國際的穩定增持,配置剛性與持倉慣性特徵顯著。二者在半導體賽道由策略共振轉入策略分化,反映交易盤與配置盤在產業週期不同階段的決策分野。

地平線機器人-W(09660)以214億港元市值增量進入南向2025年前20榜單,表明南向資金對智能駕駛算力層已開啓左側佈局,但整體仍處認知導入期。 MiniMax-WP的IPO狂熱則主要由韓國散戶驅動——單月淨買入超2000萬美元,1837倍超額認購,其決策路徑呈現強社群共識、弱機構依賴的典型特徵。韓國資金在該賽道表現出明確的風險溢價定價意願,對南向資金具備產業敘事驗證與估值錨參照的雙重指示意義。

百濟神州(06160)、藥明合聯(02268)、歌禮制藥(01672)在韓國股民持倉中呈現年度級賽道輪動,其進出時點與全球流動性預期、美股生物醫藥指數高度相關,屬全球貝塔驅動下的交易盤行爲。

比亞迪股份(01211) $比亞迪股份 (01211.HK)$ 、理想汽車(02015) $理想汽車-W (02015.HK)$ 等整車標的則獲南向資金持續性底倉配置,決策錨點在於滲透率曲線、產能週期及全球化驗證,呈現產業阿爾法追蹤型配置盤特徵。交易盤與配置盤的久期錯配,在此類高估值彈性、高研發投入的成長賽道中體現最爲充分——韓國資金博弈邊際變化,南向資金押注產業終局。

機構化配置盤範式VS全球交易盤的極端樣本

南向資金與韓國股民的交易行爲,呈現出機構化與散戶化、價值錨定與敘事驅動、長週期與高頻輪動的根本分野。

南向資金決策錨點包含股息率、ROE穩定性、自由現金流生成能力、估值分位。交易易特徵呈現連續增持、逆勢買入、持倉穩定。以建設銀行爲例,2025年在股價震盪區間持續淨買入73.89億股,持股市值增加558億港元。「越跌越買」並非情緒宣泄,而是股息率隨股價下跌提升、安全邊際持續強化的配置盤行爲。

通過持續、可預測、規模化的資金流入,南向資金正逐步將港股金融、通信運營商的估值體系向A股收斂。在建設銀行、中國移動等標的上,持股比例已超20%。

韓國股民的決策錨點具體爲產業敘事強度、社交媒體熱度、社群共識濃度。其定價邏輯並非「公司值多少錢」,而是“下一個進入者願以多高價格接棒。交易特徵呈現高槓杆爲默認設置。韓國活躍股票帳戶數達6200萬個,爲總人口的1.2倍;海外股票融資餘額峰值突破18萬億韓元(約126億美元)。

值得關注的是,韓國交易所數據顯示,本土個人投資者的股票持倉平均持有周期不足3個月,部分熱門美股及港股標的的換手率,甚至超過部分加密貨幣。這與南向資金動輒以「年」爲單位的持倉週期形成鮮明對比。高頻交易帶來的不僅是高額佣金(2025年12家主要券商海外股票交易佣金達1.95萬億韓元),更是極致的情緒敏感度。

智通財經APP認爲,韓國股民的「賭性」標籤,實則是制度環境與產業結構共同塑造的理性適應行爲。韓國雖擁有全球半導體制造巨頭,但在互聯網平台、雲計算、AI大模型等軟科技領域缺乏代表性企業,形成補償性交易衝動——重倉阿里是押注「韓國沒有的亞馬遜」,搶籌MiniMax是尋找「韓國沒有的OpenAI」。

對於港股市場而言,韓國股民的湧入既是流動性的增量來源,也是投資者結構多元化的重要一步。他們不會像南向資金那樣以年爲單位配置國有大行吃股息,也不會像國際長線基金那樣苛求ESG數據。這種資金,在某些時刻會加劇波動,但在另一些時刻——如MiniMax-WP的IPO——能直接改寫上市初期的定價生態。

綜上,南向資金以萬億級體量重塑港股估值底座,韓國散戶則以極致交易爲邊緣地帶注入流動性溢價。兩種資金、兩套邏輯,共同催生港股市場「定價分層、敘事並行」的新常態——既需要配置盤的定力,也需要交易盤的銳度。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論

發表評論

1

1