瀚亞's View: The Investment Value of Japan Amid a Strengthening Yen and Rising Yields (Part 1) 🏯

As Japanese Prime Minister Sanae Takaichi called for an early election, yields on Japanese government bonds surged, and the yen significantly rebounded against the US dollar since last Friday, the Japanese market quickly became a focal point for global investors. Below, we will explain why we remain optimistic about Japanese equities, particularly value stocks, even as we expect the yen to further strengthen and long-term bond yields to continue rising.

As of writing, the TOPIX (Tokyo Stock Price Index) fell by 2.0%, narrowing its year-to-date return to 4.3% in yen terms but still maintaining 6.0% in dollar terms. This still far outpaces the roughly 1% increase in the US stock market this year. Today’s decline almost entirely reflects the 2.8% appreciation of the yen against the dollar since last Friday. This rebound occurred after both the Bank of Japan (BoJ) and the Federal Reserve (Fed) issued official warnings about the weak yen and conducted price reviews last Friday.

We agree that a stronger yen will reduce earnings forecasts for Japanese companies, but the impact is insufficient to cause underperformance in well-structured portfolios with currency-neutral allocations. For the overall market, our rough estimate suggests that a 10% drop in USD/JPY would lead to about a 5% downward adjustment in earnings expectations for Japanese equities. However, caution must be exercised when applying such estimates, as we cannot be certain of the actual exchange rate levels used in earnings forecasts prior to the yen's movement.

We tend to believe that just before the Bank of Japan and the Federal Reserve conducted their interest rate review last week, the market generally expected the USD/JPY exchange rate to be around 155–157. This again implies (also a very rough estimate) that if the yen rebounds to 145 against the dollar and remains at that level, earnings forecasts could be revised down by approximately 3.5%–4.5% compared to expectations from a week ago. However, we believe that from a full-year perspective, this impact is likely overestimated.

One reason is that Japan's economic outlook has improved over the past two quarters, leading us to expect nominal GDP growth of around 4% this year.

• Japan’s PMI and Tankan surveys indicate real economic growth of approximately 1%;

• Core machinery orders have risen to their highest level in about five years, showing good momentum for capital expenditure growth;

• Robust economic growth in the US and Europe suggests exports are likely to rebound, and the worst impact of US tariffs has already passed;

• Fiscal policy may provide mild stimulus in the coming year.

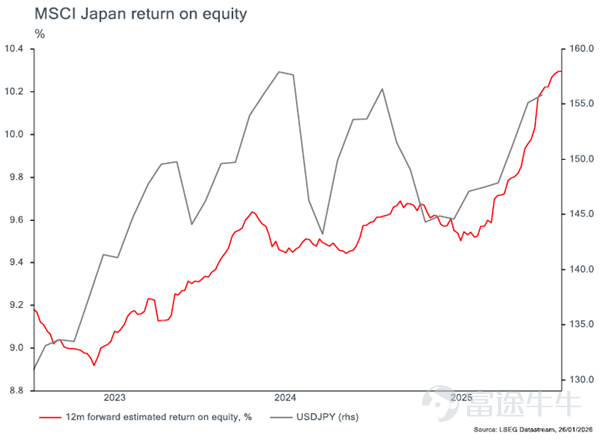

Another key reason is that the chart below shows a rise in return on equity (RoE). We believe this is a direct result of ongoing corporate governance reforms. Notably, the rise in RoE has not been driven solely by the weak yen. The RoE of the MSCI Japan Index has increased from 9.5% in mid-2024, when the dollar-yen rate rose slightly above 161, to 10.3% currently, with the dollar-yen rate now below that previous high.

An important consequence of the rising return on equity is that earnings growth in the Japanese stock market has significantly outpaced GDP growth (see chart below).

Against this backdrop, "value" as an investment style has particularly stood out. Bloomberg estimates that over the past three years, value-based investment strategies have delivered active returns of 61% in yen terms, far exceeding the second-best investment style, "high dividend yield," at 38%. Since Sanae Takagi was elected last October, value investing has generated an active return of 5.6%. (To be continued)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

1