Market Voice Weekly Call | ADC 2026 Target Review & Investment Insights into the Optical Communications Industry

Introduction of the guest lineup for this episode (the first episode):As the inaugural piece, we are honored to invite three heavyweight guests:Freya: Holds dual certifications as an FRM (Financial Risk Manager) and CFA (Chartered Financial Analyst), with years of experience in the pharmaceutical industry, focusing on innovative drug and AI healthcare target research.Tim: Formerly worked in the research department of a well-known top-tier brokerage firm, with extensive experience in sector research and institutional roadshows, excels at converting complex market information into clear investment logic.Joe: Executive Director of Institutional and Private Wealth at Futu Securities, with over 15 years of stock trading and research experience. He will serve as today'sProfessional host, leading the subsequent interactive Q&A session.

Time waits for no one. We should not only watch the bustling market but also understand the underlying dynamics. First, let's turn our attention to the biopharmaceutical field. Let's invite Freya to share insights on the track with the most commercial potential by 2026.

Core conclusion: In 2026, ADC will be the core investment focus for biopharmaceuticals, with an emphasis on technological breakthroughs like bispecific ADC and differentiated niche targets. Undervalued companies such as Fosun Henlius and Duality Biologics deserve attention. Optical communication benefits from AI computing power demands, upgrading to 1.6T, with Lumentum being the top choice in the first half of the year and Coherent as a long-term prospect; also keep an eye on upstream core materials and domestic leaders.

Freya:Analysis of the ADC track

Concept redefined: What are 'biological missiles'?ADC (Antibody-Drug Conjugate), fully known asantibody-drug conjugate, has gained significant attention in the capital markets and is hailed as 'biological missiles' or 'smart chemotherapy.' To help everyone understand its core logic, we can break it down into three key components:

Antibody (Antibody): Acts as the 'navigation system,' responsible for identifying antigens on the cell surface to achieve precise targeting.Payload: Drugs with toxicity, responsible for inflicting damage.Linker: Responsible for stably connecting the two components mentioned above. The core mechanism of this design is to leverage the transport capability of antibodies to precisely deliver highly potent toxins into tumor cells for release. It combines the powerful cytotoxicity of traditional chemotherapy with the precise targeting ability of antibody drugs, minimizing 'off-target toxicity' to normal cells.

Core Mechanism: From 'Precision Sniper' to 'Area Bombardment'The reason ADC drugs are considered a breakthrough lies in two main mechanisms of action:

Intracellular killing: Antibodies accurately identify and bind to cancer cell antigens, and after being internalized into the cells, release toxins to directly kill the cancer cells.Bystander Effect: This represents a revolutionary breakthrough in third-generation ADC drugs. Traditional limitation: Past targeted therapies could often only 'snipe' at cancer cells with high antigen expression. ADC breakthrough: By employing small-molecule toxins with high membrane permeability, ADC drugs can diffuse toxins to neighboring cells after killing the target cancer cells.low or non-expressingAntigen-positive cancer cells. This means the treatment logic has shifted from simply relying on antigen expression to a 'regional bombardment' of the tumor microenvironment, effectively breaking through the treatment bottleneck posed by the high heterogeneity of solid tumors.

Investment Logic: Why Focus on ADCs Now?Based on our Market Maturity Matrix analysis, the ADC sector currently exhibits a 'dual-high' characteristic:High maturity: Technological iteration has reached the third generation, with major pharmaceutical companies actively deploying resources, moving beyond early-stage concept speculation.High popularity: Currently in the midst of a commercialization boom year (Listing Boom).

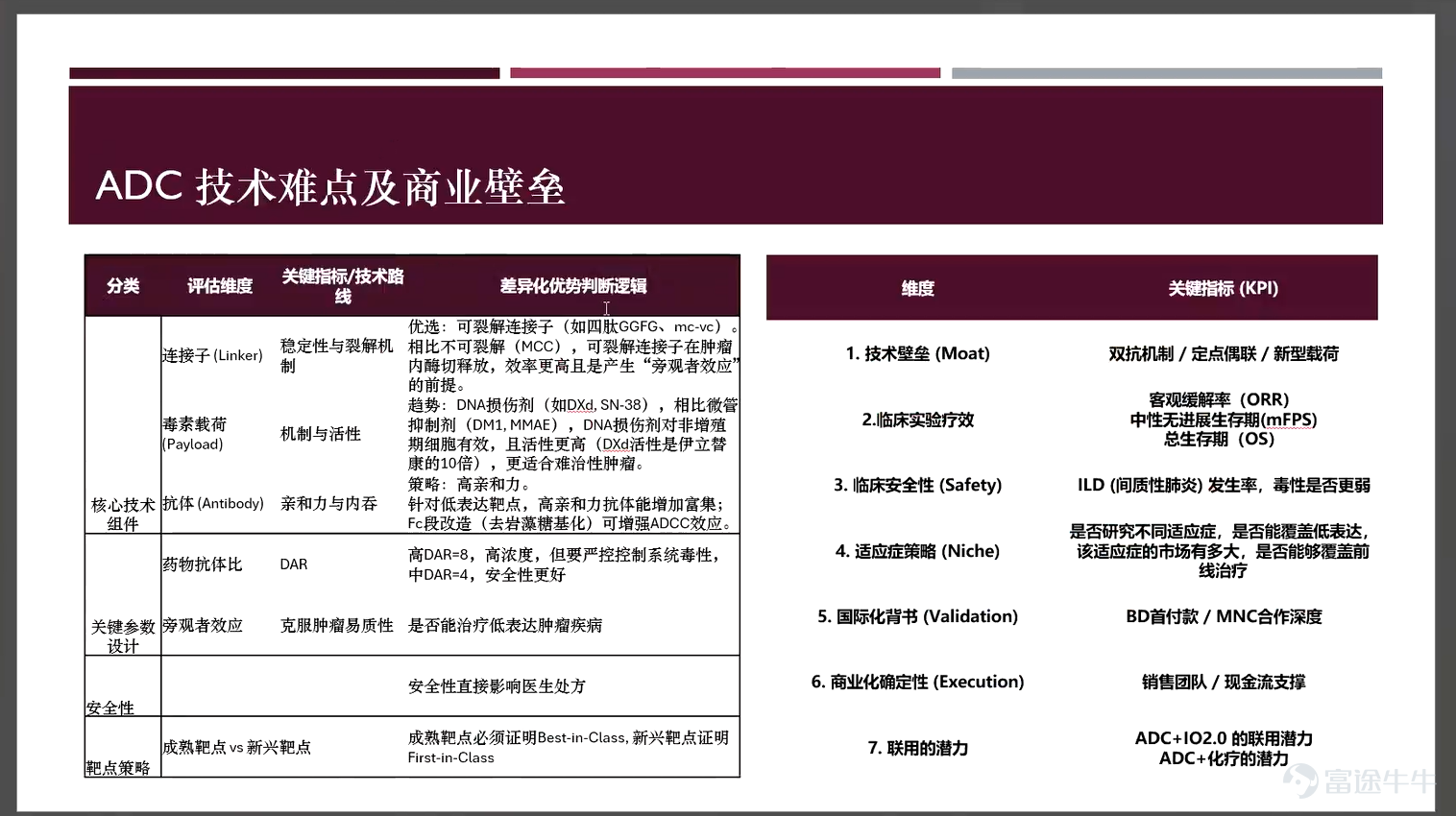

Therefore, whether considering technological certainty or market explosiveness, ADC represents a core investment theme in the biopharmaceutical field that cannot be overlooked by 2026.Technology Assessment: Four Core Pain Points and the Art of BalanceReferring to the PPT chart, by deconstructing the core components of ADCs, we can categorize their technical challenges and evaluation dimensions into four main areas. An excellent ADC drug must achieve breakthroughs or balance in the following aspects:

Improvements to core components (Core Components): Linker: The key lies in stability and the cleavage mechanism. The trend is toward usingcleavable linkers, which not only enable enzymatic release of toxins within tumors but also serve as a prerequisite for generating the 'bystander effect.' Payload: The current trend is shifting from microtubule inhibitors toDNA-damaging agents(such as DXd), because the latter are effective against non-proliferating cells, exhibit higher potency, and are better suited for treating refractory tumors.

Key parameter: Balancing the DAR value (Drug-Antibody Ratio): Definition: DAR refers to the drug-to-antibody ratio, indicating the number of toxin molecules conjugated to an antibody. The average DAR typically ranges between 3.5 and 4. Challenge: This is a 'double-edged sword.' Theoretically, the higher the DAR, the more payload it carries and the stronger the efficacy; however, it also increases toxicity and risks causing drug aggregation, affecting metabolism. Thus, the technical core lies inBalanced—maximizing the drug-loading capacity per antibody while ensuring safety (e.g., increasing DAR from 4 to 8 while controlling toxicity).

Mechanism design: Bystander effect: This is the key to determining whether ADC can treatlow-expression tumors(Low Expression). Drugs with a bystander effect can penetrate cell membranes after killing target cells, destroying nearby cancer cells that do not express antigens and overcoming tumor heterogeneity.

Target Strategy: For mature targets: it must prove to beBest-in-Class(the best in its class). For emerging targets: it must prove to beFirst-in-Class(the first of its kind).

Commercialization prospects: It’s not just about efficacy, but also about strategy.For investors, evaluating the commercial value of an ADC product should not only focus on clinical efficacy (ORR, OS) and safety (such as the incidence rate of interstitial pneumonia ILD), but must also consider it from a broader business strategy perspective:

Indication Strategy (Niche & Expansion): Breadth: Can the drug cover multiple indications? (One drug for multiple uses) Depth: Can it move forward from third-line treatment (later lines) tosecond-line or even first-line treatment? The market space for first-line treatment is much larger than that of later lines, but this requires extremely high safety and efficacy data support. Coverage: Does it have the ability to cover 'low-expression' populations? This directly determines the ceiling of the target patient group.

Market Size and Landscape: How large is the market size for this indication? Is the competitive landscape crowded? Is there international validation, such as whether there are significant upfront payments from large BD (licensing deals) with MNCs (multinational pharmaceutical companies), which often serve as the gold standard for technical strength.Dimension Reduction Impact: Why can ADC replace traditional therapies?

Referring to the comparison chart in the PPT, we need to look beyond the surface and understand the underlying principles. The core reason why ADC drugs can capture significant market share from chemotherapy and even some small molecule drugs lies in their 'combination punch' mechanism:

First, compared to traditional chemotherapy (Chemotherapy), this is a victory of precision.Traditional chemotherapy was like 'carpet bombing,' killing a thousand enemies at the cost of eight hundred of your own; whereas ADCs are more like 'biological missiles' with guidance systems. The direct benefit of such high targeting capability is a significant improvement in the safety of toxicity profiles—simply put, under the premise of achieving the same therapeutic effect, patients suffer less and toxicity becomes controllable.

Secondly, when compared to small molecule targeted drugs, ADCs excel in terms of potency and breadth.Small molecules typically work by blocking signals, while ADCs take a straightforward and aggressive approach by delivering high concentrations of toxins directly into the target. For instance, ADCs with a Drug-to-Antibody Ratio (DAR) of 8 are akin to soldiers carrying heavy weaponry, significantly enhancing single-agent activity. More crucially, when patients develop resistance to previous targeted therapies, such as TKIs, ADCs become a lifeline for late-stage patients. Moreover, thanks to the bystander effect generated by cleavable linkers and highly permeable payloads, ADCs can even address tumors with low expression levels—a feat many small molecule drugs reliant on high expression struggle to achieve.

Lastly, let’s examine its relationship with immunotherapy.The two mechanisms differ: immunotherapy mobilizes the body's immune system, while ADCs focus on precision elimination. Additionally, the production cost structure of ADCs is often more favorable than complex cell therapies. The future trend isn't about one replacing the other but rather powerful synergies—the 'ADC + Immunotherapy (IO)' combo strategy, which delivers a 1+1>2 effect, will be the mainstream going forward.

Value Anchors: How do we evaluate the BD potential of a Chinese Biotech company?

When discussing the BD value of a Chinese biotech company, investors aren’t just spectating—they’re scrutinizing three core dimensions under a microscope.

First, it’s about the scalability of the technology platform—whether you can apply lessons learned across multiple areas.What investors fear most is that you stumbled upon a successful molecule by luck. What we value is whether you have a replicable platform. A strong bonus point here is if you’ve had successful BD records in the past, especially multi-asset deals with multinational pharmaceutical companies (MNCs), which directly proves that your underlying technology platform has been validated by major players—not just sheer luck.Second, we return to the hard metrics of clinical data.OS (Overall Survival) and ORR (Objective Response Rate) are of course the key benchmarks, but current competitive differentiation is increasingly reflected in safety. For instance, everyone is working on HER2; if you can significantly reduce the incidence of interstitial lung disease (ILD), then you’ve hit a weak spot for AstraZeneca’s DS-8201, which translates into a massive competitive edge.Third, commercial execution and differentiated survival.In the domestic market, the focus is on whether a drug can get quick approval, enter the national insurance system, and scale up production. When choosing indications, it's crucial to avoid direct competition. AstraZeneca's Enhertu (DS-8201) already dominates the breast cancer space, so going head-to-head isn't just difficult—it’s unnecessary. The smart move is to pivot towards niche areas like urothelial cancer, gastric cancer, or endometrial cancer, where you can build your own stronghold.

Global perspective: The underlying logic behind MNCs' aggressive 'buying spree.' Zooming out globally, the ADC market is currently in a high-growth phase with about a 30% growth rate, and the $200 billion market is largely driven by blockbusters like Enhertu. Against this backdrop, why are overseas pharmaceutical giants (MNCs) on a buying spree? The motivations are quite pragmatic, boiling down to two main points:

Pipeline complementarity:It’s simple—I have a gap, you have a product, so I buy it to fill my target空白.This is a defensive play, also known as the “combination advantage.”The most typical example is Merck & Co’s acquisition of Kelun-Biotech’s TROP2 ADC. Why? Because their flagship Keytruda (K-drug) is struggling to compete against Enhertu in certain areas. Merck urgently needs to bring in ADCs to pair with its K-drug, not only boosting efficacy through “ADC + IO” combinations but also providing follow-up options for patients who develop resistance to Keytruda. In short, this is a necessary step to protect Keytruda’s market share.

Next-generation trends: Given that the field is already a red ocean, where are the opportunities for differentiation? The current level of competition in ADCs is intense, but we can still identify several highly attractive areas for differentiation:One is the exploration of new targets.HER2 and TROP2 have long been fiercely competitive, but now the opportunity lies in emerging targets like B7-H3. Whoever takes the lead will seize the chance.The second is bispecific ADC (Bispecific ADC).This is a direction where Chinese pharmaceutical companies have made significant progress. By leveraging dual-target synergy to enhance specificity, it theoretically overcomes drug resistance further. For instance, Baili Tianhe has performed well in this area.The third is dual-payload ADC (Dual-Payload ADC).This involves an antibody carrying two different toxins, which poses significant technical challenges and remains in its early stages (e.g., Kanghong Pharmaceutical is working on it), but it represents a promising long-term investment.Finally, there is the evolution of combination therapy (Combo).The industry is highly optimistic about the combination of 'PD-1/VEGF bispecific + ADC,' considered highly explosive. Additionally, even traditional-sounding combinations like 'ADC + chemotherapy' have shown significant advantages in real-world data—old trees can bloom anew.

In-depth analysis of core targets (HER2 & TROP2)

HER2: The battle of kings in a red ocean and the breakout of Chinese pharmaceutical companiesHER2 is not just a target; it is currently the most mature and heavily contested 'main battlefield' in the ADC field, spanning from breast cancer to gastric cancer and urothelial cancer, covering nearly all major solid tumors.

First, we must pay tribute to the 'global benchmark' that redefined the rules – Enhertu (DS-8201). This is a blockbuster creation jointly developed by AstraZeneca and Daiichi Sankyo. Its status now goes beyond being just a 'good drug' to becoming a mainstay replacing chemotherapy. The numbers don't lie: by 2025, its global sales are expected to reach $5 billion, with an intimidating growth rate of around 30%. Why is it so powerful? The core lies in its high drug-to-antibody ratio (DAR) of 8, combined with a potent 'bystander effect,' allowing it not only to eliminate tumors with high expression but also tackle the tough cases of low HER2 expression.

So, under the shadow of this giant, how can Chinese companies break through by 2026? The answer is: differentiation.

DualityBio's strategy is to 'avoid strength and strike at weakness.'Their DB-1303 (in collaboration with BioNTech) cleverly avoids the meat grinder of breast cancer and instead focuses onendometrial cancer.。The biggest highlight lies in safety:This is a huge competitive advantage. No severe interstitial lung disease (ILD) has been observed with DB-1303, which happens to be the most feared shortcoming of DS-8201 among doctors.The efficacy is also impressive:In patients with advanced endometrial cancer, the ORR reached 58.8%, and the DCR exceeded 94%, marking clear Best-in-Class potential. Currently, it holds a solid position in the first tier of global R&D and has great potential to fill the treatment gap for late-stage resistant patients.

Baili Tianheng’s approach is 'two-pronged.' The highlight is their bispecific antibody-drug conjugate (ADC):This is the BL-B01D1 (EGFR/HER3 dual-target, already licensed to Bristol-Myers Squibb) that everyone is watching. They are moving very fast, having launched phase three clinical trials for five indications, covering non-small cell lung cancer, small cell lung cancer, and various types of breast cancer. At this year's (2026) ASCO or ESMO conference, everyone is waiting to see their key data unveiled.Monoclonal antibodies are also making progress:In addition to bispecific antibodies, their HER2 monoclonal antibody ADC (BL-M07D1) is advancing in global registration clinical trials, providing double insurance for global market entry.

RemeGen, on the other hand, is taking a steady and methodical approach as a 'commercialization veteran.'Their RC48 (Vedotin) is following a step-by-step strategy.Domestically:Gastric cancer has long been covered by national health insurance; last year (May 2025), the indication for HER2-positive breast cancer with liver metastasis was also approved.The combination therapy is even more promising:RC48 combined with PD-1 for treating urothelial carcinoma shows efficacy superior to chemotherapy, and it is expected to secure more first-line indications this year (2026).Internationally:The current partner is Pfizer, which acquired Seagen. With the progress of overseas clinical trials, sales revenue is expected to be recorded this year.

TROP2: The next 'pan-cancer' goldmine after HER2. If HER2 represents the present, then TROP2 represents the future. It is highly expressed in lung cancer and breast cancer and is considered the next breakout target.

The global benchmark still comes from the 'AstraZeneca + Daiichi Sankyo' combination: Dato-DXd.This drug is regarded as the next-generation nuclear weapon following Enhertu, with a key focus on breast cancer and non-small cell lung cancer (NSCLC).

However, in the TROP2 space, Chinese companies are launching a fierce counterattack: Kelun-Biotech is an absolute 'seed player.'Their SKB264 (Lukansatuzumab) is China's first domestically developed TROP2 ADC to receive marketing approval.Promoter of globalization:After acquiring it, Merck & Co has gone all out. As of early this year (2026), they have already launched 14 global Phase III clinical trials, showcasing the execution capability of a large pharmaceutical company.The most noteworthy winning moves:In first-line treatment for non-small cell lung cancer, they adopted a triple strategy of 'PD-1 + VEGF + ADC.' The preliminary data so far has been stunning, with efficacy even surpassing the competing product Dato-DXd, which could potentially redefine the entire standard for first-line treatment.Hengrui Pharma is seeking out 'niche markets'.Their SHR-A1921 did not compete in the crowded field of breast cancer but instead focused onOvarian cancerandsmall cell lung cancer (SCLC)。Key data highlights:especially for refractory small cell lung cancer, achieving an ORR of 33.3% and a median PFS of nearly 4 months. For patients who have no treatment options after recurrence, this is a real lifeline. The Next Frontier: Bispecific ADC

Bispecific ADC: The technological dividend of entering the '3.0 era'. If HER2 and TROP2 represent the peak of single-agent therapies, then bispecific ADCs are the art of cooperative warfare. This is seen as the '3.0 era' of ADCs, with a simple core logic: two targets bind more firmly, endocytosis efficiency is higher, and most importantly—it can handle those cunning drug-resistant tumors.

Baili Tianheng: The frontrunner holding the 'trump card'The reason Baili Tianheng is favored by the capital market lies in its BL-B01D1, a dual-target combination of EGFR and HER3.Its clinical value is extremely precise:primarily aimed at solving the drug resistance problem in non-small cell lung cancer (NSCLC). Particularly for patients who developed resistance after using third-generation EGFR TKIs (such as Osimertinib), where previously there was no hope, BL-B01D1 now achieves deep remission.The surprises are not limited to lung cancer:Its performance in nasopharyngeal cancer has been stunning, marking it as the world's first bispecific antibody-drug conjugate (ADC) to enter Phase III trials. If it can successfully expand into major indications like breast cancer and gastric cancer in the future, its potential will be extremely high.Commercialization timeline:It is expected to make its debut in China between 2026 and 2027. Overseas, its progress is driven by a significant business development (BD) collaboration with Bristol-Myers Squibb (BMS). The upcoming readout of overseas data will directly determine its position in the global value chain.

Alphamab Oncology: Ingenious mechanism innovationAlphamab’s JSKN-016 takes a different approach: HER3 × TROP2.The mechanism here is highly ingenious:It leverages the exceptionally high endocytic property of HER3 to 'drag' TROP2 into the cell. Why is this design necessary? To address the safety concerns of traditional TROP2 ADCs. Through this synergy, the aim is to reduce toxicity and thereby broaden the therapeutic window. Currently focused on lung cancer and breast cancer, though still in Phase II, this mechanism innovation is worth tracking over the long term.

2026 BD Outlook: Seeking undervalued 'Alpha.' This section is the key takeaway from the conference. Note that while companies like Kelun-Biotech and Baili Tianheng are promising, expectations have already been largely priced in. If we want to seek excess returns in 2026, we must look toward targets with significant BD potential that are still undervalued by the market.

Hong Kong stocks/Potential Hong Kong stocks: Who is brewing an 'expectation gap'?

A. Henlius: More than just biosimilarsThe impression of Henlius may still linger on Hanquyou for many, but their ADC portfolio is highly differentiated, with the core rationale being to address the challenge of 'IO resistance' after immunotherapy.Two key assets: HLX42 (EGFR ADC):It targets lung cancer resistant to third-generation TKIs and has 'pan-cancer' potential.HLX43 (PD-L1 ADC):This mechanism is very appealing. It focuses on tumors with high PD-L1 expression, aiming to solve the dilemma after resistance to PD-1/PD-L1 immunotherapy. This is akin to throwing a bomb into the enemy when they think the immune defense has been breached.BD Opportunity:The early PoC (Proof of Concept) data looks quite promising, with ORR and DCR both encouraging. For MNCs (like Merck & Co.) urgently seeking new solutions in the 'post-IO era,' this represents an extremely attractive License-out opportunity.

B. DualityBio: More than just speedDualityBio is now among the global frontrunners in terms of speed, with deep ties to BioNTech.DB-1303 (HER2 ADC):It is one of the fastest progressing third-generation HER2 ADCs globally. The key focus is on its performance in endometrial cancer, with excellent ORR and DCR data, and no severe ILD, giving it 'best-in-class' (BIC) potential.DB-1311 (B7-H3 ADC):This was developed using the DITAC platform, targeting small cell lung cancer and prostate cancer, and could very well be the next hot asset for BD.Investment Logic:With the pivotal registration clinical data readout expected in 2026, coupled with potential IPO or deeper M&A rumors, I believe its value has yet to be fully realized.

Global perspective: Who is the “check-writer” backer? Overseas major pharmaceutical companies (MNCs) currently have a very clear BD strategy—either 'filling gaps' or 'defensive counterattacks'.Merck & Co:They are under the most pressure. With Keytruda facing a patent cliff, they urgently need new growth drivers. Therefore, they are fully committed to building an 'IO + ADC' ecosystem, and introducing Hengrui's TROP2 ADC is aimed at creating barriers to maintain dominance.AstraZeneca:As the 'kingmaker' in the ADC space, having DS-8201 and Dato-DXd is not enough. To prevent being disrupted, AstraZeneca is actively moving into bispecific ADCs and dual-payload ADCs, aiming to continue leading in the 'post-Enhertu era'.Pfizer:After acquiring Seagen, they are in the process of integration, but the revenue gap left by the decline in their COVID-19 business is too large and urgently needs to be filled. They prefer assets with better safety profiles or those that can address specific drug resistance issues, such as Rongchang Bio's RC88.BioNTech:They are in a transitional phase, aiming to transform from an mRNA platform company into a full-industry-chain giant in cancer treatment through their collaboration with DualityBio. Their strategy is to seek ADCs that can create synergies with their own immunotherapy pipeline.

Summary: The final summary of the 2026 investment focus is that the single-target competition in the ADC market has already become saturated, leaving little room for outsized profits. Investment and business development will shift significantly: look for technological breakthroughs, such as whether bispecific ADC (e.g., Baili Tianheng, Alphamab Oncology) can fully address drug resistance. Examine niche differentiation, such as Duality Biologics' positioning in endometrial cancer and Fosun Henlius’ unique stance in PD-L1 ADC. Evaluate commercial execution: focus on companies backed by multinational corporations but whose valuations have not soared, with Fosun Henlius and Duality Biologics being key names to watch.

Tim Yang: Analysis of the Optical Communications Industry and Investment Strategies

Key Insights and Investment Recommendations

Market Sentiment: Against the backdrop of expanding AI computing power demand, the optical module industry's sentiment will continue to rise through 2025.

Key Focus Stocks (US Market): It is recommended to focus onLumentum (LITE)andCoherent (COHR). The optical communications industry chain can be divided into three main segments: upstream core components, midstream packaging and manufacturing, and downstream application scenarios.

A. Upstream: Core Components (High Entry Barrier)

Main products:

Optical Chips/Electronic Chips: The jewel in the crown of the industry chain.Optical devices: Including lasers and detectors.Optical fiber and cables: Used for data transmission.

Representative manufacturers:Optical/electrical chips and devices:Lumentum(The recording was misidentified as RAMTRON.)Coherent(Gao Yi),Mitsubishi Electric(Mitsubishi Electric),Sumitomo Electric(Sumitomo Electric).DSP chips(Core electronic chip):Broadcom(Broadcom),Marvell(Marvell Electronics).Optical fiber and cables:Corning(Corning, US stock),Changfei Fiber Optics(YOFC),Hengtong Optoelectronics。

Current Status: High-end core components (especially high-speed optical and electronic chips) are still predominantly controlled by foreign manufacturers (such as Broadcom, Lumentum), but domestic substitution is accelerating.

B. Midstream: Optical Engines and Optical Modules (Module & Packaging)

Key segments: Integrating upstream lasers and detectors intooptical engines, then further packaging them intoOptical module。

Representative manufacturers ('The Big Three of A-Share Optical Communication'):InnoLight Technology: The global leader in optical modules.Eoptolink Technology: A globally leading optical module manufacturer.Tianfu Communications: Specializing in optical engine and precision component packaging.

Overseas manufacturers:Coherent、Lumentum。

C. Downstream: Application market customer base: Traditional telecom operators (Telecom) and cloud vendors (Datacom/Cloud).Driving Force: Current growth is mainly driven by the data communication market (cloud vendors) building AI computing clusters.

Market share and competitive landscape (2026 outlook)

Forecast for 2026800G optical module: Market demand and share were estimated (assuming global demand is approximately 50 million units):InnoLight Technology: Expected to capture about30%of the market share, maintaining its leading position.Eoptolink Technology&Coherent (COHR): Expected to each account formore than 20%of the market share.Lumentum (LITE): Estimated to account for approximately5%approximately.1.6T outlook: In the higher-end 1.6T product line,Zhongji Xuchuangmarket share may be even higher, with a clear first-mover advantage.

Industry development trendsSpeed upgrades: Driven by the expansion of AI infrastructure, optical module rates are in a rapid upgrade cycle.Product iteration: Starting from 2025, mainstream demand will shift from800G to 1.6T upgrades。Increase in value: The unit price (ASP) and profit margin of 1.6T products are significantly higher than those of 800G, which will drive earnings growth for related companies.

Key focus on target analysis (Hong Kong/US/Japan stocks) Hong Kong/A-share targets (high volatility)

A. Cambridge Technology (CIG)

Market position: In 2025,800Gthe global market share of optical modules will be approximately4%-5%. Key major client:Cisco, forming a deep partnership.

2026 forecast:1.6T Optical Module: Expected shipment volume is approximately800,000 units。Key catalysts: The R&D progress and mass production capability of Cisco switches; whether it can secureMetaorders.Key milestones:End of April 2026, observe whether bulk supply to Cisco is possible.

Competitive landscape: Industry leaderZhongji Xuchuangis aggressively expanding its 1.6T capacity, which may affect the delivery of its 800G products, thereby creating opportunities for second-tier manufacturers like Cambridge Technology (Second Source).Meta order: Currently, 800G and 1.6T products have been sampled, but the factory audit has been postponed toJanuary 2026later.

B. Changfei Optical Fiber (YOFC)

Market position: The global leader in optical fiber and cable, with market share remaining first since 2016.

Price Trend: Starting from May 2024, China'sG652Dbare fiber prices continue to rise.

Demand Analysis:Domestic: Overall weak demand in telecom, but tenders by China Mobile/China Unicom may ease contraction.Overseas: Rising demand helps absorb domestic overcapacity.Computing power network: Strong demand for high-end optical fibers (such as ultra-low loss fibers) targeting computing power networks, offering long-term upside potential.

Stock price characteristics: Highly tied to sentiment in the optical communication sector, with significant volatility and less stability compared to industry leaders.

Key US stock: Lumentum (LITE)

A. Laser business (core growth driver)

EML laser (200G):Demand: The explosive growth of 1.6T optical modules drives demand for supporting200G EMLChips have become the core bottleneck.with production capacity: Planning to increase the production capacity share of 200G lasers to10%. The chip shortage is expected to last at least4 quarters。Strategy: PrioritizingGooglecustomers who have signed long-term agreements (LTA), such as hyperscale clients; in 2026, planning to continuePrice hike。

CW lasers (continuous wave, used for silicon photonics/CPO):Mass production: Expected to enter full-scale mass production around mid-2026100mWhigh-power CW lasers, mainly for internal 1.6T module use.NVIDIA collaboration:Ultra-high power CW lasers: Expected to deliver samples in Q1 2025, ramp up production in Q3, and show significant growth by Q4.Exclusive supply: Currently two models from NVIDIACPO silicon photonic switches(Rubin architecture) with external light sourcessole supplier。Market potential: Based on conservative shipment projections for NVIDIA switches in 202615,000 unitsEstimate: single unit configuration18 unitsExternal light source → Total270,000 units. Unit price approximately$100→ Contributing revenue of approximately27 million US dollars(currently a small proportion, but with huge potential).

B. System Business (System) OCS (Optical Circuit Switch):Growth expectations: Rapid growth expected in 2026-2027, driven byGooglethe commercial deployment of OCS.Revenue guidance: Planned completion by 2025150 million US dollarsOrders; starting from Q4 2025, production capacity will increase to100 million US dollars per quarter。Optical modules (Datacom Modules):Current Status: Previously, due to the factory relocation from Dongguan to Thailand, production expansion fell short of expectations, with shipments in 2025 reaching only700,000 to 800,000 units。Target for 2026: Shipment volume will increase to2 to 2.5 million units。Customer: Main client is Google. By 2026, there is potential for shipping 800G products (Oracle orders expected to materialize in Q1 2025).MicrosoftandOracleShipment of 800G products (Oracle order expected to land in Q1 2025).Cloud Light (Yun Hui Technology): Initial integration after the acquisition has been delayed, with future revenue expected to steadily reach250 million USD per quarter。

Key US stock: Coherent (COHR)

A. Business Overview Lasers: Including EML and CW, it is a direct competitor of Lumentum, with most production capacity used internally.material: Optical chip materials (InP, etc.), thermal management materials.Networking: Acquired in 2018Finisar, providing optical module and OCS products.

B. Aggressive capacity expansion: Plans to double internalInP (Indium Phosphide)laser chip production capacity within the next year.Wafer transition: The Texas (Sherman) and Sweden (Järfälla) plants are transitioning to6-inch wafers, significantly boosting production capacity.Customer visibility: Revenue expectations from key customers have extended toThe year 2028。

C. Optical module business progress is ahead of schedule: Shipment pace is faster than Lumentum's.1.6T modules: Coherent can contribute to quarter-on-quarter revenue growth next quarter (Lumentum will not see contributions until mid-2026).Supply chain:Gross margin: As the share of 1.6T increases, gross margin gradually moves closer to40%.

D. OCS switch market opportunity: MaintainUSD 2 billionAssessment of market opportunities.Shipment volume: Currently, approximately2,000 unitsin bulk orders have been received. If production capacity ramps up smoothly in August (reaching 500-600 units/month), the annual capacity is expected to reach4,000-4,500 units。Customer distribution:Google (3,000 units)、Oracle (1,000 units); Amazon, Microsoft, and Nvidia are currently testing samples.

Upstream material indicators:

Sumitomo Electric (5802.JP)Core Position:Indium Phosphide (InP)A core supplier of substrate materials.Market share: Approximately50%。LogicHigh-end laser chips (EML) are highly reliant on InP substrates, and Sumitomo Electric directly benefits from the expansion of the optical communication industry.

Comparative analysis of upstream material suppliers, foundries, and leading companies: Upstream material suppliers:

A. Sumitomo Electric (5802.JP) Industry Position:Indium Phosphide (InP)A core supplier of substrate materials.Customer:LumentumandCoherentAre its top two customers.EML chip: Holds approximately10%of the global market share in the EML chip sector, while also engaging in high-end optical fiber and preform businesses.Capital structure:Revenue: Automotive wiring harness components account for50%or more; information and communication business accounts for about5%。Profit margin: The operating profit margin in the communications segment is significantly higher (approximately12%), while other segments are below 10%.Logic: Growth in demand for optical modules and lasers (EML/silicon photonics solutions) has a significant impact on Sumitomo Electric's profit, with high certainty for InP demand.Risk points:Export Controls: Involves China's export controls on rare metals such as gallium and germanium. As China is a major supplier, there may be short-term pressure.

B. AXT Inc. (AXTI) Positioning: A US-listed company, the overseas manufacturer's 'second source,' also producesIndium Phosphide (InP)substrate.Customer: Core clients include China's optoelectronic chip manufacturers (such as Yuanjie Technology, Changguang Huaxin, etc.).Recent risks:Earnings revision: Downgraded Q4 2025 earnings forecast.Reason: Lower-than-expected number of export licenses issued by China led to shipping delays.Comparison conclusion: Sumitomo Electric (the leader) is more stable; AXT has greater elasticity but faces risks from fluctuations in export licensing (based on historical situations, such issues typically recover later). Foundry business

A. Fabrinet (FN) Business: Contract manufacturing for optical module assembly (primary foundry for Lumentum).Current Status: Strong performance in earnings and stock price by 2025, driven by surging demand for optical modules.Long-term perspective:Not optimistic enough。Low barriers to entry: Unlike TSMC’s GPU foundry business, which has high barriers to entry.Market share: Approximately15%。Competition: Major players such as InnoLight and Coherent have their own internal production lines (In-house). Stock prices are highly sensitive to demand fluctuations.

B. Tower Semiconductor (TSEM) Business:Silicon Photonics Chip (SiPh)Contract manufacturing.Advantage:High barriers to entry: Technological threshold is higher than optical module assembly.Gross margin: Approximately twice that of Fabrinet.Outlook: Launched an exponential capacity expansion plan. With the silicon photonics ramp-up cycle expected over the next two years, order and performance visibility remains strong.Valuation: Though relatively expensive, it shows a strong upward trend after the pullback.

Key Leader Comparison: Lumentum vs. Coherent

A. Valuation and Market Sentiment (2027E):Lumentum: Forward P/E ratio approximately36 times。Coherent: Forward P/E ratio approximately29x: Note, it is slightly above the historical average of the past two years +1 standard deviation, partially reflecting tight supply expectations.Strategy: The short-term risk-reward is moderate; it is recommended to accumulate on dips.CatalystExpectedNVIDIA GTC Conference in Marchwill bring a new wave of sector catalysts.

B. Market Supply, Demand, and Price Outlook for 2026:800G: Doubling growth to approximately45 million units。1.6T: Significantly raising expectations to20 to 30 million units。Price (ASP):Current Status: Price for 1.6T is approximately$1000 - $1200。decline: The annual price reduction used to be around 15%, but given the current supply shortage (especially for NVIDIA's best-selling products),RubinandGB200the price decline by 2026 is expected to narrow, potentiallynot exceeding 10%。

C. Comparison of investment rationale

Summary Recommendation:First half of the year: PrioritizeLumentum, leveraging its monopolistic position in optical chips/lasers to capture offensive gains.

Long-term: FollowCoherentValue its economies of scale and diversified business, which provide defensive advantages and a better risk-return profile.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

10