Trump to launch trade investigation, another tariff war on the way?

Risk appetite continues to dominate the market, with Bitcoin participation dropping to extremely low levels | Latest Bitcoin market analysis | Cryptocurrency | Virtual assets

This week’s global financial markets started with turmoil triggered by a geopolitical conflict originating from Greenland, beginning with a small-scale 'triple sell-off' in stocks, bonds, and currencies. This was followed by fluctuations due to U.S. employment data and third-quarter GDP figures, finally concluding with the suspension of tariff hikes on eight European countries and data that met or slightly exceeded expectations.

By Friday, the U.S. Dollar Index plummeted 1.91% for the week to 97.479, while the 10-year U.S. Treasury yield gave up most of its gains but remained at a high of 4.231%. The three major U.S. stock indexes recovered most of their early-week losses, closing slightly lower.

Amid wild speculation driven by both safe-haven and speculative capital, precious metals continued to surge, with gold and silver rising 8.3% and 14.8% respectively for the week.

Last week's attempt to rebound to new highs failed. $Bitcoin (BTC.CC)$ Bitcoin (BTC), hit hard again at the start of the week due to decreased risk appetite caused by geopolitical conflicts, plunging to as low as $87,000 before stabilizing in ultra-low volatility trading, ultimately closing at $86,561.94, down 7.55% for the week.

This week, Bitcoin (BTC) once again faced intertwined challenges: declining risk appetite triggered by geopolitical factors, liquidity shocks, and persistent outflows from long-term holders. Selling pressure intensified while buying power dwindled, deepening the bearish sentiment. Since the October peak, BTC has dropped approximately 31%. After emotional retreats and panic-driven selling, the market entered a state of apathy with thin trading. Both futures and lending markets remained subdued, consistent with the 'cold bear' patterns seen repeatedly over the past three years.

Key focus moving forward will be on the Fed's statements following the January interest rate meeting, whether the return of risk appetite can bring back buying power, and whether the selling by long-term holders can be curbed.

Next week, U.S. tech companies will release earnings reports in bulk. $Meta Platforms (META.US)$ Meta, $Microsoft (MSFT.US)$ Microsoft, $Apple (AAPL.US)$ Apple, $Tesla (TSLA.US)$ Companies like Tesla will face market scrutiny — whether the high spending on AI can deliver the expected financial returns.

Policy, macro-financial, and economic data

This week, the macro financial market was mainly influenced by the geopolitical crisis in Greenland. The employment and GDP data released by the US this week were largely in line with expectations, further reinforcing the expectation of a 'soft landing' characterized by 'growth not stalling but marginally cooling + inflation/cost pressures still present.' This also led the market to believe that the Fed will not cut interest rates in the next three FOMC meetings, with the earliest rate cut likely occurring in June.

The escalating 'Greenland' conflict this month dominated this week's financial market volatility.

At the beginning of the month, Trump publicly stated the need to 'own' Greenland rather than lease it, linking the narrative to national security issues such as 'defense/countering China and Russia,' setting the stage for subsequent escalations.

On January 19, in an effort to 'acquire' Greenland, President Trump proposed a timeline for imposing additional tariffs on goods from Denmark and several European countries — starting February 1, an additional 10% tariff would be imposed, increasing to 25% on June 1 if no 'Greenland agreement' is reached.

This news triggered an accelerated decline in Bitcoin, leading to a mini 'triple sell-off' crisis in stocks, bonds, and currency in the US at the beginning of the week.

On January 21, during the Davos meeting, Trump announced that he had reached a 'framework for future Greenland arrangements' with the NATO Secretary General, and accordingly withdrew tariff threats against several European countries. The market breathed a sigh of relief, and with slightly better-than-expected employment and GDP data, the three major indices gradually recovered their losses.

This conflict further exacerbated the global capital's trust crisis in the United States, sparking widespread discussions about selling off US assets, driving the US dollar index down 1.91% for the week.

Amid the sell-off of US assets, speculative funds rushed into the precious metals market, resulting in an 'apocalyptic rally,' with gold and silver surging 8.3% and 14.8%, respectively, in a single week.

Although the TACO incident occurred again and the tariff imposed on February 1 was canceled, the geopolitical crisis in Greenland has not been completely resolved. The statements from Denmark and Trump are inconsistent, indicating that further博弈 will continue. This conflict may intensify further, causing continued market震动 and further affecting global capital's allocation attitude towards US assets.

Cryptocurrency Market

As a leading indicator of global risk appetite and liquidity, Bitcoin’s decline was still notably larger than that of US stocks, and it failed to reclaim the important psychological level of $90,000 even after the US stock market recovered. This is because, as risk appetite continued to decline, funds are further撤离ing from long-duration assets, causing inflows through the newly turned positive Bitcoin ETF channel to reverse back to outflows, while减持 by long-term holders within the market also加剧ed once again.

The lack of buying power is the fundamental reason for Bitcoin's无力反弹 this week.

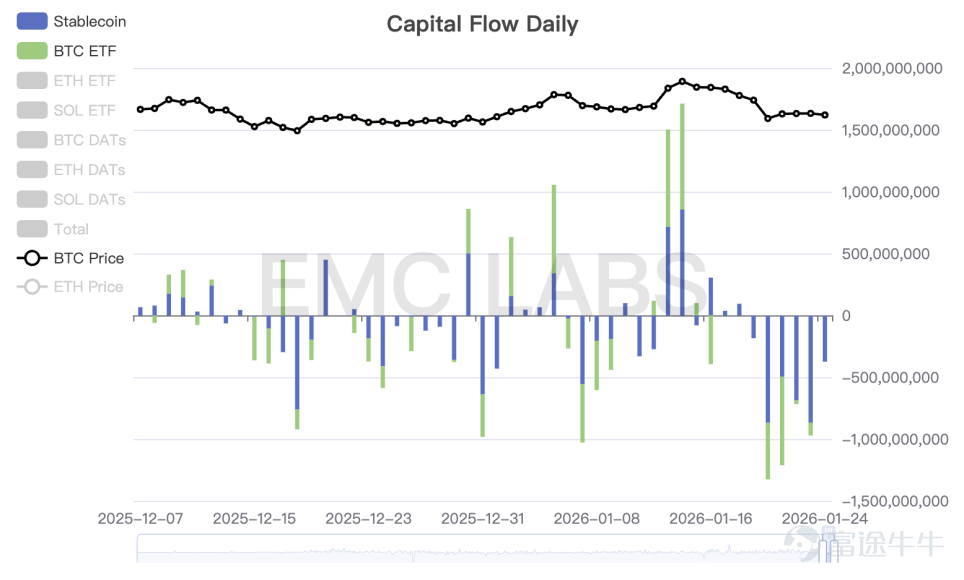

BTC Market Capital Flow Statistics (Daily)

The crypto market is again facing an outflow dilemma via both stablecoin and ETF channels, with total weekly outflows exceeding $4.7 billion, of which $3.4 billion came from the stablecoin channel and $1.3 billion from the ETF channel. This scale of outflow marks the largest weekly outflow since January 2023, surpassing last week's inflow of $3.1 billion.

In addition to the lack of buying power, amidst significant fund outflows, the减持 by long-term holders continues, further loosening筹码 and pushing prices down towards equilibrium.

BTC Long and Short Position Holding Change Statistics (Daily)

Although, as risk appetite changes, this week saw an increase in selling规模 among both short- and long-term holder groups, overall selling still did not exceed last week's levels, with the 7-day average sell volume also declining.

Statistics on Long and Short Selling and Exchange Reserves

However, there was a堆积 of exchange reserves at the beginning of the week, indicating a rapid loss of buying power. It should be noted that the current inventory on exchanges is still rising, which could cause Bitcoin prices to fall further.

Moreover, the progress of the 'Crypto Market Structure Act' has encountered obstacles. Traditional financial institutions and industry forces represented by Coinbase have fundamental conflicts regarding interest-bearing stablecoins, causing the voting progress to be delayed until February or March. This has also led to the exit of short-term speculative funds.

The above analysis is provided by EMC Labs.

———————————————————————

About EMC Labs

EMC Labs is a partner of Victory Securities, and together they have launched the only virtual asset fund approved by the Securities Regulatory Commission to accept stablecoin subscriptions—the Victory EMC BTC Cycle Fund. EMC Labs was co-founded by seasoned virtual asset investors and data scientists, with its core team hailing from JD.com, Bell Labs, and Marsbit. EMC Labs has invested substantial resources into building professional engines for analyzing on-chain BTC data and technical indicators.

Disclaimer

Investment involves risks, and investors are advised to exercise caution. The value of securities and investments may rise or fall, and returns are not guaranteed. Investors may not recover the original investment amount, and past performance is not necessarily indicative of future results. Securities trading services of Victory Securities are provided by Victory Securities Limited (hereinafter referred to as "Victory Securities"). This document has been prepared and authorized for release on this platform by Victory Securities Limited. The information contained herein is for reference purposes only, and Victory Securities Limited reserves the right to modify or terminate it at any time without prior notice. All information available on this platform may not be reproduced, linked, reposted, or otherwise used for commercial purposes by any media, website, or individual without the prior written authorization of Victory Securities. Authorized parties must acknowledge that the source of the material is Victory Securities when using this document and its contents, and they must commit to complying with relevant laws and all international practices regarding internet usage. They shall not use this document for any illegal purpose or in any unlawful manner; violators will bear all related legal and financial responsibilities. The data or information cited in this document may be obtained from third parties. Victory Securities does not guarantee the accuracy of such third-party data or information, nor does it assume any liability for the fairness, accuracy, timeliness, completeness, or correctness of any information, forecasts, and/or opinions contained in this document, or for the basis upon which such forecasts and/or opinions are made. Any forward-looking statements contained in this document should not be construed as a guarantee of future performance, and actual circumstances or developments may differ significantly from such statements. This document is not and should not be regarded as or constitute an offer, invitation, solicitation, recommendation to buy or sell any investment product or make any investment decision, nor should it be interpreted as professional advice. Persons reviewing this document or considering any investment decision should fully understand the associated risks and the relevant legal, tax, and accounting characteristics and consequences. They should determine whether the investment aligns with their personal investment objectives and whether they can bear the associated risks. If necessary, appropriate professional advice should be sought. In certain jurisdictions, the distribution and circulation of this document may be restricted by law or regulation. Persons obtaining this document are required to be aware of and comply with such restrictions.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment