買力逐步迴歸,《結構法案》再生波折,BTC中期突破再次失利|比特幣行情分析|加密貨幣|BTC

得益於美國CPI數據推動的市場風險偏好提升,和美國《市場結構法案》(Clarity Act)預期推動,BTC在本週再次衝擊2月以來形成壓制的94500美元壓力位,最高升至97963.62美元,之後隨《結構法案》再生波折、格陵蘭島地緣政治衝突加劇,再度出現回撤,失守94500美元。

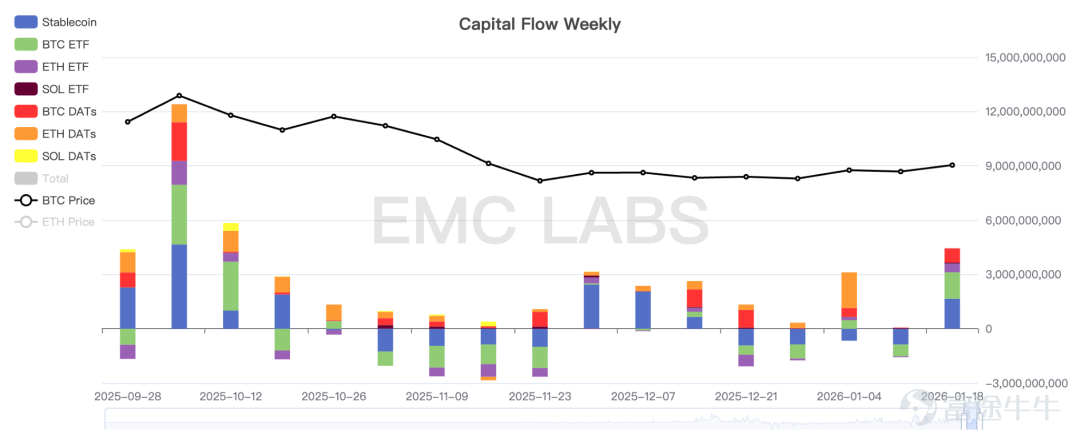

資金層面,加密市場迎來11月調整以來最大流入規模周,全周超過43億美元通過穩定幣、BTC ETF及DAT公司流入市場。且伴隨風險偏好回升,ETH上漲強度亦小幅領先BTC。

隨着下週PCE數據發佈,本週影響BTC價格中期走勢的兩大因素——通脹預期和《市場結構法案》進展,下週將繼續作爲核心影響因子發揮效應。

政策、宏觀金融及經濟數據

1月13日,美國發布數據顯示,12月未季調CPI年率爲2.7%,符合預期,亦與前值持平。12月未季調核心CPI年率爲2.6%,與前值持平,低於預期值2.7%。CPI數值小幅低於市場預期,雖不足以推動降息預期,但可以消解市場對於中長期降息的疑慮。

同日公佈的美國10月新屋銷售總數年化則達到73.7萬戶,高於預期的72萬戶,顯示降息後房屋市場購買力正在復甦。

次日公佈的11月零售銷售月率公佈值爲0.6%,高於預期值0.4%,亦高於前值-0.1%,顯示消費市場景氣度明顯處於復甦狀態,並未冷卻。

15日,美國發布1月10日當週初請失業金人數爲19.8萬人,低於預期的21.5萬人,亦低於前值20.7萬人。顯示就業市場依然承壓,這有利於美聯儲在2026年繼續推動利息下行。

以上經濟數據並未打破之前的市場預期及定價——後疫情時代,美國經濟正在實現“軟着陸”甚或“不着陸”,就業市場正在趨冷,不達預期,但並非“失速/惡化”,更像“低裁員、低招聘”的持平狀態,可以進一步觀察,不必通過降息來刺激就業,因爲消費市場依然在復甦。

這均暗示降息概率仍未有根本性改變,市場將目光投向下週發佈的亦是美聯儲最爲關注的的PCE數據。

隨着降息交易回吐,及 Fed獨立性與主席人事噪聲,進一步擡升了長期不確定性補償,美國國債收益率在週四週五大幅反彈,10年期美債收益率升至4.223%的高位,進一步壓制了高久期資產,使得納指及BTC持續調整。

除宏觀經濟及就業數值之外,近期對加密市場形成較強影響的因素還包括《市場結構法案》(CLARITY Act)。該法案原計畫在1月15日進行委員會審議,但在 Coinbase臨時撤回支持後被推遲;委員會主席稱這是“短暫停頓”,法案並未終止,正進入條款再談判階段。

《市場結構法案》旨在界定數字資產在法律上何時屬於證券/商品/其他類別,明確SEC與CFTC的管轄邊界,給現貨市場監管、投資者保護、合規路徑提供更清晰框架。這一方案的完成,有助於產業的健康有序發展,有助於助力美國成爲加密產業發展高地,因此獲得產業的高度矚目,並有可能引發加密資產尤其是智能合約平臺資產(如ETH)的廣泛配置。

15日,Coinbase CEO因不滿穩定幣利潤分配的限制,撤回對法案的支持,當天BTC達到高點97176.42後開始持續下跌,並最終在週日再度失守90日均線,中期轉爲弱勢。

作爲中期利好,《市場結構法案》將來未來一段時間內繼續爲市場提供情緒動力。

加密市場

加密市場內部,經過2個多月的劇烈調整,正在迎來複蘇期。

首先宏觀流動性,持續好轉,資金緊張情況已大爲改善。在加密市場內部體現爲,資金正在由流出轉爲流入。

加密市場資金進出統計 (周)

本週加密市場整體流入43.44億美元,其中對於短期定價非常關鍵的BTC ETF通道,流入14.63億美元。此外,以Strategy爲代表的DAT公司在調整期間,斥巨資購入,亦爲市場發揮託底作用。

本週中心化交易所流出規模超過2.4萬枚。以鏈上視角來看,巨鯨和鯊魚羣體繼續作爲主要的掃貨買家爲市場提供買力。

市場最大利空,亦是決定市場調整究竟是“深熊”還是“冷熊”定性的重要因素的長手羣體減持,在周初暫停後在後半周重啓拋售,但整體拋售規模呈縮小勢。

後市BTC價格,能否有效越過95000美元,甚至更重要的98000美元,仍需長手羣體拋售規模的減少甚至轉爲重新積累。

此外,市場偏好和《市場結構法案》進展引發的投機衝動也是市場中短期動力來源。

以上分析由EMC Labs提供

———————————————————————

關於EMC Labs

EMC Labs為勝利證券之合作夥伴,雙方聯手推出目前唯一一支獲證監會批准可接受穩定幣認購的虛擬資產基金—Victory EMC BTC Cycle Fund。EMC Labs由資深虛擬資產投資人與資料科學家聯合創立,核心團隊來自京東金融、貝爾實驗室、火星財經(Marsbit)等公司。EMC Labs投入大量資源建立專業引擎對BTC鏈上資料和技術指標進行分析。

EMC Labs為勝利證券之合作夥伴,雙方聯手推出目前唯一一支獲證監會批准可接受穩定幣認購的虛擬資產基金—Victory EMC BTC Cycle Fund。EMC Labs由資深虛擬資產投資人與資料科學家聯合創立,核心團隊來自京東金融、貝爾實驗室、火星財經(Marsbit)等公司。EMC Labs投入大量資源建立專業引擎對BTC鏈上資料和技術指標進行分析。

聲明

投資涉及風險,敬請投資者註意。 證券及投資的價值可升亦可跌,並不能保證。 投資人可能無法取回原本投資金額,過往的表現不一定可以預測日後的表現。 勝利證券之證券交易服務由勝利證券有限公司(以下簡稱「勝利證券」)提供。 本文件由勝利證券有限公司編製及授權發佈於本平台,所載資料勝利證券有限公司僅供參考之用途,勝利證券有限公司保留隨時更改或終止而毋須另行或事先通知。 本平台所提供的所有訊息,任何媒體、網站或個人未經勝利證券之事先書面授權不得轉載、連結、轉貼或以其他方式複製發表貯本文件及任何內容或作任何商業用途。 已獲授權者,在使用本文件及任何內容時必須註明稿件來源於勝利證券,並承諾遵守相關法例及一切使用互聯網的國際慣例,不作任何非法目的或以任何非法方式使用本文件,違者 將承擔所有相關法律及經濟責任。 本文件所引用之數據或數據可能得自第三方,並非對第三方所提供數據或資料之準確性負責,且勝利證券不會就本文件所載任何資料、預測及/或意見的公平性、 準確性、時限性、完整性或正確性,以及任何該等預測及/或意見所依據的基準作出任何明文或暗示的保證、陳述、擔保或承諾而負責或承擔法律責任。 本文件中如有類似前瞻性陳述之內容,此等內容或陳述不得視為對任何將來表現之保證,且應注意實際情況或發展可能與該等陳述有重大落差。 本文件並非及不應被視為或構成對任何人士投資證券的提呈發售、邀約、招攬、邀請、建議買賣任何投資產品或投資決策之依據,亦不應被詮釋為專業意見。 閱覽本文件的人士或在作出任何投資決策前,應完全了解其風險以及有關法律、賦稅及會計的特點及後果,並根據個人的情況決定投資是否切合個人的投資目標,以及能否承擔有關風險 ,必要時應尋求適當的專業意見。 在若干國家,傳閱及分派本文件的方式可能受法律或規例所限制,取得本文件的人士須知悉及遵守該等限制。

投資涉及風險,敬請投資者註意。 證券及投資的價值可升亦可跌,並不能保證。 投資人可能無法取回原本投資金額,過往的表現不一定可以預測日後的表現。 勝利證券之證券交易服務由勝利證券有限公司(以下簡稱「勝利證券」)提供。 本文件由勝利證券有限公司編製及授權發佈於本平台,所載資料勝利證券有限公司僅供參考之用途,勝利證券有限公司保留隨時更改或終止而毋須另行或事先通知。 本平台所提供的所有訊息,任何媒體、網站或個人未經勝利證券之事先書面授權不得轉載、連結、轉貼或以其他方式複製發表貯本文件及任何內容或作任何商業用途。 已獲授權者,在使用本文件及任何內容時必須註明稿件來源於勝利證券,並承諾遵守相關法例及一切使用互聯網的國際慣例,不作任何非法目的或以任何非法方式使用本文件,違者 將承擔所有相關法律及經濟責任。 本文件所引用之數據或數據可能得自第三方,並非對第三方所提供數據或資料之準確性負責,且勝利證券不會就本文件所載任何資料、預測及/或意見的公平性、 準確性、時限性、完整性或正確性,以及任何該等預測及/或意見所依據的基準作出任何明文或暗示的保證、陳述、擔保或承諾而負責或承擔法律責任。 本文件中如有類似前瞻性陳述之內容,此等內容或陳述不得視為對任何將來表現之保證,且應注意實際情況或發展可能與該等陳述有重大落差。 本文件並非及不應被視為或構成對任何人士投資證券的提呈發售、邀約、招攬、邀請、建議買賣任何投資產品或投資決策之依據,亦不應被詮釋為專業意見。 閱覽本文件的人士或在作出任何投資決策前,應完全了解其風險以及有關法律、賦稅及會計的特點及後果,並根據個人的情況決定投資是否切合個人的投資目標,以及能否承擔有關風險 ,必要時應尋求適當的專業意見。 在若干國家,傳閱及分派本文件的方式可能受法律或規例所限制,取得本文件的人士須知悉及遵守該等限制。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論

發表評論