Options Square: Storage stocks keep surging! Is UBS Group offering a double-up price?

Can NVIDIA reignite the AI narrative as pessimistic valuations collide with loosening H200 restrictions?

The easing of H200 exports to China has brought a whiff of certainty to the market.

On December 24th, $NVIDIA (NVDA.US)$ the stock price rose slightly by 3%, marking the fourth consecutive trading day of increases.The driving factor was the clarification of NVIDIA's supply plans for the H200 chip to China. According to Reuters, NVIDIA plans to commence H200 deliveries by mid-February 2026, with an estimated initial shipment of 5,000 to 10,000 modules (equivalent to approximately 40,000 to 80,000 chips).

As early as December 9, Trump explicitly stated on social media: Provided that 'national security remains secure,' the U.S. would allow NVIDIA to export the H200 to designated countries, including China. He specifically mentioned that 25% of the sales revenue from related transactions must be remitted to the U.S. government, calling this move a way to 'support American jobs, manufacturing, and taxpayers.'

At first glance, this appears to be a technological compromise; upon closer inspection, it is a strategic retreat.

The H200, released in November 2023, utilizes Taiwan Semiconductor's 4N process and remains a top-tier AI chip in 2024. During the Biden administration, it was included on the list of banned exports to China. Now, times have changed—by the end of 2025, the B200 based on the Blackwell architecture will become the new industry benchmark, and the H200’s technological halo has faded.

The U.S. decision to approve the H200 at this juncture also reflects an acknowledgment: this chip no longer represents 'cutting-edge computing power.'Rather than rigidly adhering to an ambiguous performance threshold, it has been transformed into a quantifiable 'revenue channel'—a 25% revenue share (10 percentage points higher than the 15% levy for H20 export licenses), which generates tax-like income while deftly avoiding discussions about more advanced architectures like Blackwell or Rubin.

For NVIDIA, CEO Jensen Huang has repeatedly acknowledged that their market share in mainland China has dropped to zero. It is worth noting that even H20, compared to domestic alternatives, no longer holds a competitive advantage in computational power. Industry estimates generally suggest that H200 delivers about eight times the computational capability of H20, making it not only more powerful but also closer to global mainstream standards, thus naturally more appealing to customers.

A rough estimate suggests that if the Chinese market recovers to contribute 10%-15% of NVIDIA's annual data center revenue (projected at $160-$200 billion) over the next few years, it would translate to additional annual sales of $16-$30 billion. Of course, this is merely a scenario analysis, not official company guidance.

A more realistic support comes from the suppressed demand. In early 2025, several major Chinese companies had placed a total of $16 billion in H20 orders with Nvidia, which ultimately could not be fulfilled due to regulations. Now that the H200 has been unblocked, the capital expenditures and demand that have been accumulated by domestic companies are expected to be released. Recently, Alibaba has also been reported to be evaluating the procurement of 40,000 to 50,000 AMD MI308 accelerators. This indicates that even if the H200 is approved, Chinese customers are actively building a multi-source supply system and will not put all their eggs in one basket.

For NVIDIA, this may not necessarily be a high-profit business.——25% of the revenue is paid to the U.S. government. NVIDIA's current non-GAAP gross margin is around 75%. If this expense is fully accounted for in the cost of sales, it will reduce the unit gross margin of the H200 business in China by about 25 percentage points. Bernstein estimates that the overall gross margin may be under pressure by about 1 percentage point. However, compared to being "completely absent," this is already a pragmatic choice.

However, the situation is far from settled, and regulation remains the biggest risk.Reuters pointed out that, as of now, China has not approved any H200 orders. In July of this year, the National Internet Information Office had a discussion with Nvidia regarding potential security vulnerabilities of the H20 chip—regulatory concerns about imported AI chips have not diminished.

Valuation has dropped to a low point, but the story is not over yet.

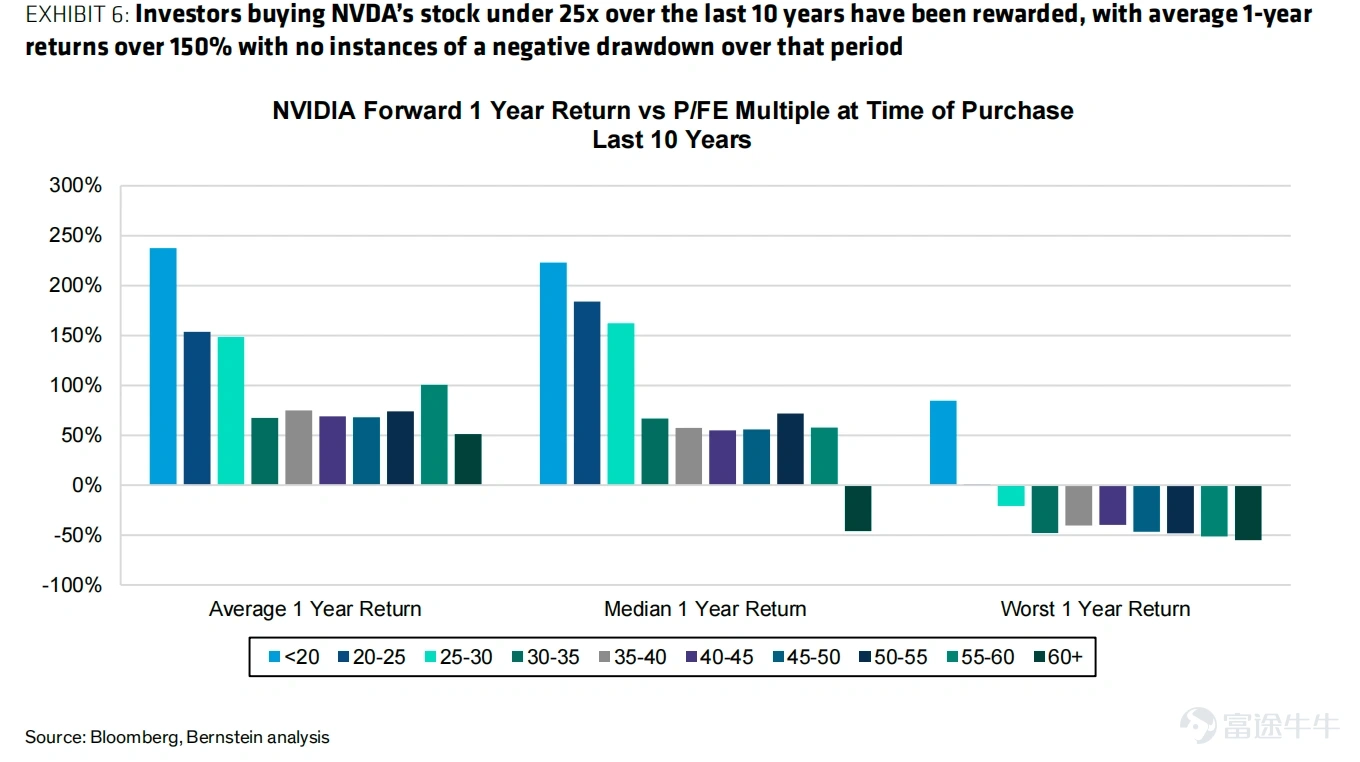

Despite a cumulative increase of about 30% this year, NVIDIA has been in a consolidation phase since peaking in July, significantly underperforming the semiconductor sector.According to Berstein's calculations, the current forward P/E ratio for the fiscal year 2027 is about 24 times.Within the relative valuation range of the past 10 years.1st percentile of its relative valuation range over the past decade. This implies that, over the past ten years, there were only 13 days when its stock was cheaper than it is now.In other words,The market pricing for it has approached a pessimistic level.

Historical experience may provide some comfort: over the past decade, whenever Nvidia's forward price-to-earnings ratio fell below 25, the average return in the following year exceeded 150%, and there has never been a negative return.Of course, history does not simply repeat itself, but it reminds us: when valuations are compressed to this extent, it often means sentiment has been 'washed out enough.'

Fundamentally, demand remains strong, but the market is scrutinizing the sustainability of capital expenditures.The latest earnings report shows that data center revenue for Q3 of fiscal year 2026 reached $51.2 billion, a year-over-year increase of 66%; guidance for Q4 is $65 billion (±2%). On one hand, there is tangible shipment volume, while on the other hand, there is market anxiety over the sustainability of AI-related capital expenditures. Investors are indeed concerned: will cloud vendors cut CapEx? Will customers shift to self-developed ASICs? — The juxtaposition of these factors highlights the mismatch between short-term sentiment and long-term trends. However, at present, corporate willingness to invest in AI remains firm, and GPUs’ dominance in training and inference workloads even shows signs of stabilization.

In the coming months, catalysts are densely lined up: CES in January 2026 (Jensen Huang may deliver a keynote speech; CES typically has a minor impact on stock prices) and the GTC Conference in March (historically the most information-rich event).

Additionally, OpenAI plans to complete its latest round of financing as early as the end of Q1 next year.If it can raise the target amount, OpenAI’s valuation could soar to $8.3 trillion, indirectly benefiting NVIDIA.— Stronger capital strength means faster deployment of computing power, and NVIDIA remains the most direct beneficiary in hardware.

Options strategy

*The following content is for investor education purposes only and does not represent any investment advice.*

NVIDIA’s short-term technical indicators showbullish recovery signals(MACD golden cross, breakout above the upper Bollinger Band), but caution is warranted due to RSI overbought conditions; the medium-term trend depends on whether it can hold above the key resistance level near $185. Current IV stands at 35.93%, which is historically low. On December 23, call option trading volume reached 2.0057 million contracts, while put option trading volume was 922,300 contracts, with a call/put ratio of 0.46, indicating bullish market sentiment. A large block trade of call options was executed on the same day (strike price $50, expiring January 2026).

(1) If investors are optimistic about NVIDIA in the long term,

the recent correction has alleviated excessive valuation pressure,with IV (Implied Volatility) at a relatively low historical level, the premium cost required for option buyers is lower. It is possible to moderately extend the duration of the options or consider a LEAPs Call strategy as a substitute for direct stock investment in long-term positioning.

Strategy Logic: Buy deep in-the-money + medium- to long-term (e.g., 9 months to 2 years) call optionsTypically, when we buy options, we purchase “near-term” ones, betting on short-term surges; whereas buying LEAPs Calls involves purchasing “long-term” options, betting on prolonged trends. When you buy deep in-the-money options, their Delta approaches 1.0. This means that for every $1 increase in the stock price, the price of your option will also rise by nearly $1. By paying only a “premium” (usually 20%-30% of the stock price), you can achieve nearly synchronized gains with 100 shares of the underlying stock. The maximum loss is capped; if you directly buy the stock and its price halves, you lose 50%; but if you buy LEAPs Calls, your maximum loss is only the initial premium paid.

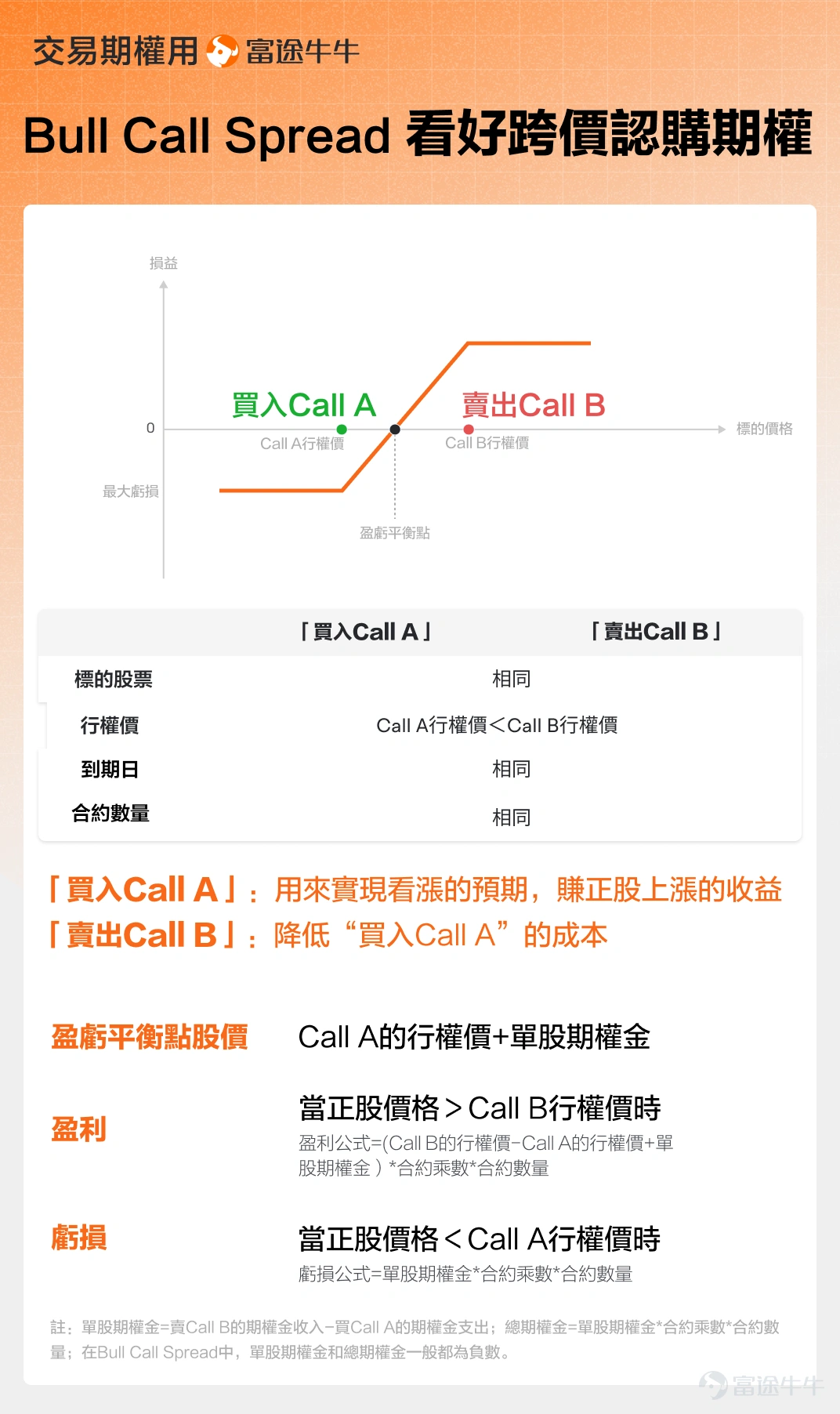

(2) For investors who expect moderate stock price increases but wish to limit risks,

a Bull Call Spread can be adopted.A Bull Call Spread involves selling a Call with a higher strike price on top of buying a Call, thereby reducing the cost of purchase but also capping the potential for higher returns. The biggest risk of this strategy is losing all the premium expenditure incurred at the time of establishing the position. In terms of expiration date selection, for investors with lower risk tolerance, choosing a longer timeframe might be slightly more expensive, but the erosion of the option's time value will also occur more slowly.

The unpredictable nature of geopolitical factors. Even though the H200 may seem “outdated,” competition between China and the US in the AI chip sector could escalate at any time. Additionally, the long-term trend of customers developing their own chips and fluctuations in short-term order rhythms are all potential disruptive factors.

However, for now, what the market may need is not perfection, but a bit of certainty. If the H200 can achieve stable delivery through a model of “25% revenue sharing + designated customers,” it may signify the formation of a new equilibrium: no longer a blanket ban, but a predictable, tradable, and priceable regulatory framework.

Being able to secure a share is better than standing on the sidelines and watching.

Finally, here’s a small perk for fellow investors. Welcome to claim it!Options Beginner's Package

This event is exclusively available to HK invited users. Click to learn more.Detailed event rules>>

Market conditions are complex and volatile,Options StrategyToo many options and not sure how to choose? Futubull helps you build in three easy steps,Options Strategymaking investing simple and efficient from now on!

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee regarding securities, financial products, or tools. The risk of loss in trading options can be substantial. In certain circumstances, the losses you incur may exceed the initial margin deposited. Even if you have set contingency orders, such as “stop-loss” or “limit” orders, these may not necessarily prevent losses. Market conditions may render such orders unexecutable. You may be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified timeframe, your open positions may be liquidated. However, you will still be responsible for any shortfall in your account resulting from such liquidation. Therefore, before engaging in options trading, you should thoroughly study and understand options and carefully consider whether such trading is suitable for you based on your financial situation and investment objectives. If you trade options, you should familiarize yourself with the procedures for exercising options and the rights and obligations upon exercise or expiration of options.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (8)

to post a comment

123

44