Focus on the Super Macro Week! Japan raises interest rates by 25 basis points

Why the sharp decline after the FOMC? The whole world misinterpreted the Fed's easing!

At the December FOMC meeting, Powell announced that the Federal Reserve would initiate reserve management purchases on December 12, also known asRMP (Reserve Management Purchase). Many people associate this with QE. However,the mechanism of RMP is entirely different from QE-style easing. Today’s in-depth professional article will help everyone fully understand what this FOMC’s RMP really is. Why does itIt is not.“ease”。

First,? RMP serves as a supplement to ON RRP.To understand RMP, one must first grasp the mechanism of ON RRP.

What is ON RRP

The Federal Reserve previously offered banks a “reserve deposit” service, allowing banks to earn interest by depositing excess funds with the Fed, representing a risk-free return option for banks. However, non-bank institutions such as money market funds and brokerages are not eligible for this benefit. When there is an abundance of liquidity in the market, their idle funds have nowhere to go, which can lead to disorderly declines in market interest rates. To address this, in 2013 the Fed introduced ON RRP, effectively creating a 'deposit channel' specifically for these non-bank institutions (Non-bank institutions lend their idle cash to the Federal Reserve in exchange for Treasury bonds as collateral; the next day, the Fed repays the principal with interest, and the institution returns the bonds. This process can be understood as the Fed engaging in reverse repo operations to withdraw liquidity from the market.)。ON RRP and reserve deposits together form the Federal Reserve’s reserve framework system, establishing a floor for interest rates. When market interest rates drop too low, the Fed uses these two tools to influence both the non-banking and banking sectors to stabilize the lower bound of interest rates. This represents one of the Fed’s methods for managing liquidity.

The purpose of ON RRP

Its core function is to maintain a floor for interest rates. With this 'piggy bank,' non-banking institutions are unlikely to lend money at rates below the ON RRP rate — after all, it is more profitable to earn risk-free interest by depositing funds with the Federal Reserve. In this way, ON RRPSupports the lower bound of short-term market interest rates, preventing disorderly declines in rates,Assisting the Federal Reserve in maintaining the stability of its monetary policy.

The ON RRP will be depleted.

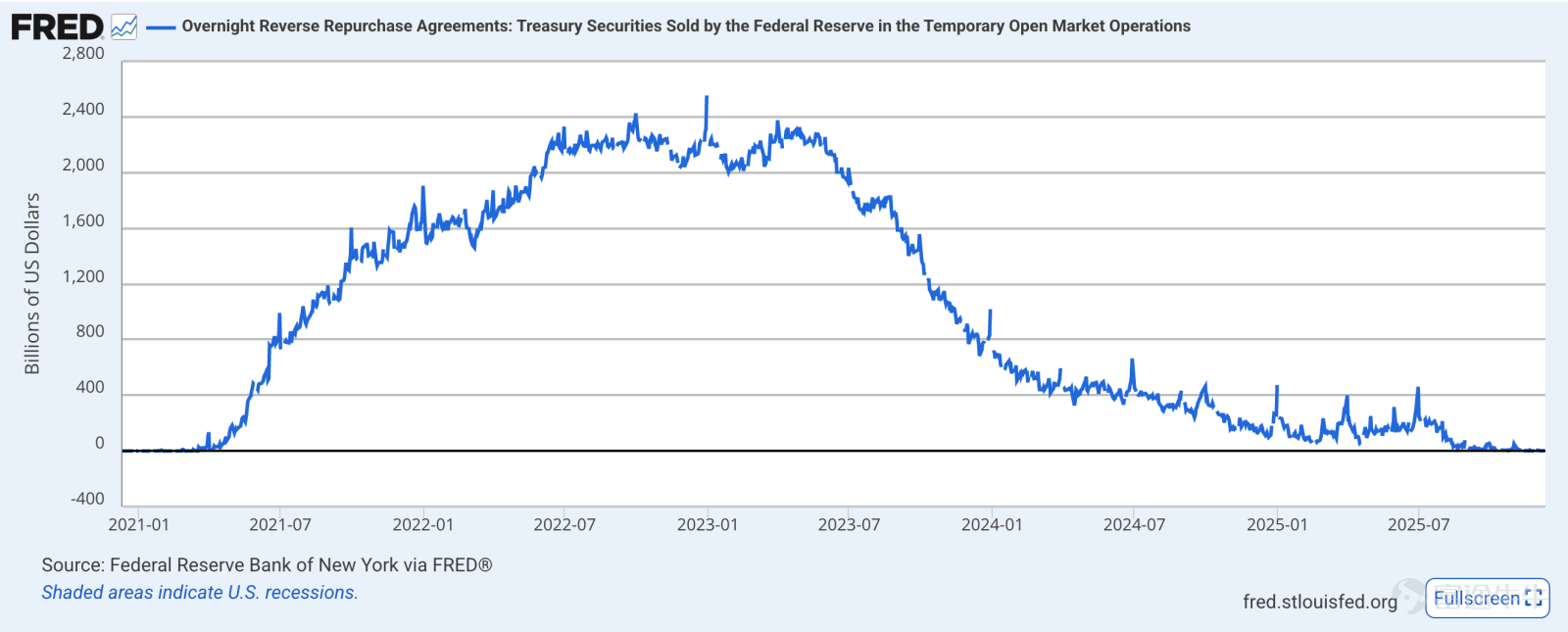

The amount of money in the ON RRP depends on whether non-bank institutions are willing to deposit funds into it. In recent years, due to a series of market factors, non-banks have stopped depositing money into this account. For instance,the Federal Reserve's balance sheet reduction and fiscal bond issuance have reduced overall market liquidity.with scarcity driving up value, market interest rates have become higher than the ON RRP rate, thus discouraging non-banks from 'depositing' money in the ON RRP. As a result,the scale of the ON RRP has been shrinking and is now nearly exhausted.(As shown in the chart, the ON RRP has been rapidly depleted since 2023.)。

RMP compensates for the ON RRP.

As the ON RRP nears depletion, the Federal Reserve needs to have sufficient tools to maintain stability in the lower bound of interest rates. (Recall that the ON RRP mechanism was designed to prevent disorderly declines in rates below the floor).This time, the tool chosen by the Federal Reserve is the RMP, which aims to offset the depletion of the ON RRP.

Purpose of this RMP

This FOMC meeting is aboutthe initiation of a monthly 40 billion RMP, along with reinvestment of 20 billion MBS into short-term government bonds each month.Therefore, the purchase volume of short-term government bonds in the coming months could reach 60 billion US dollars per month. This approach serves two purposes:first, to prevent the depletion of liquidity, and second, to conduct liquidity management solely at the short-term end.。

Regarding the MBS portion,

previously, when the MBS held by the Federal Reserve matured, real estate companies would repay the principal and interest to the Fed. If the Federal Reserve took no further action upon receiving this money, it would disappear (on the balance sheet, the MBS under the asset section of the Federal Reserve decreases, as does the reserve in the banking system on the liability side. The MBS on the Federal Reserve's balance sheet corresponds to reserves.) Thus, over time, the money corresponding to MBS would naturally 'extinguish.' However, the Federal Reserve is now using these funds to purchase short-term government bonds, effectively reinjecting the money back into the banking system (short-term government bonds under the asset section of the Federal Reserve increase, as do reserves on the liability side).Liquidity represents the liability side of the Federal Reserve.Therefore, this operation did not bring incremental funds to the market but rather aimed to prevent the existing scale of liquidity from shrinking further.

2 Liquidity Management

The Federal Reserve's announcement this time is to purchase only short-term Treasury bonds and avoid long-term bonds. This is the core distinction from QE.QE involves indiscriminate large-scale asset purchases. However, this time, the Federal Reserve explicitly emphasized that it will only buy short-term bonds, essentially signaling to the market that thisis merely a short-term liquidity management measure(Supplementing the depletion of ON RRP). This recalls Alan Greenspan’s statement that 'market expectations of short-term interest rates form the core of the yield curve.' As mentioned earlier, ON RRP is nearly depleted, but it remains within the non-banking system.What the Federal Reserve truly fears is that the banking system, observing the depletion of ON RRP, may begin to hoard liquidity out of concern for a potential cash shortage. Under such circumstances, banks could proactively reduce lending, leading to a credit crunch. The introduction of RMP by the Fed is essentially intended to reassure banks, assuring them not to worry about liquidity and avoid panic-driven money hoarding.

In summary, this RMP aims to prevent liquidity contraction and does not inject additional funds into the market; it is not quantitative easing (QE) or monetary expansion.In one sentence: This is not stepping on the gas pedal but merely preventing the brakes from being applied.As for the future, if U.S. fiscal spending continues to exceed sustainable levels, the Federal Reserve may be forced to expand the scale of the RMP and extend its duration. Only then would the RMP evolve into QE.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (30)

to post a comment

172

310