業績全面超預期!台積電後市你點睇?

富途研究 | 台積電業績點評:毛利率大超預期,AI需求旺盛

10月17日週四,全球芯片代工巨頭台積電公佈2024年第三季度業績。三季度業績表現強勁,銷售額、淨利潤、毛利率均超預期。尤其是毛利率重新回到58%附近,遠高於市場預期(54.8%)。而下季度指引中收入和毛利率也都大幅超出市場預期,顯示出AI需求仍然旺盛。

一、AI需求仍然旺盛,智能手機需求正在恢復

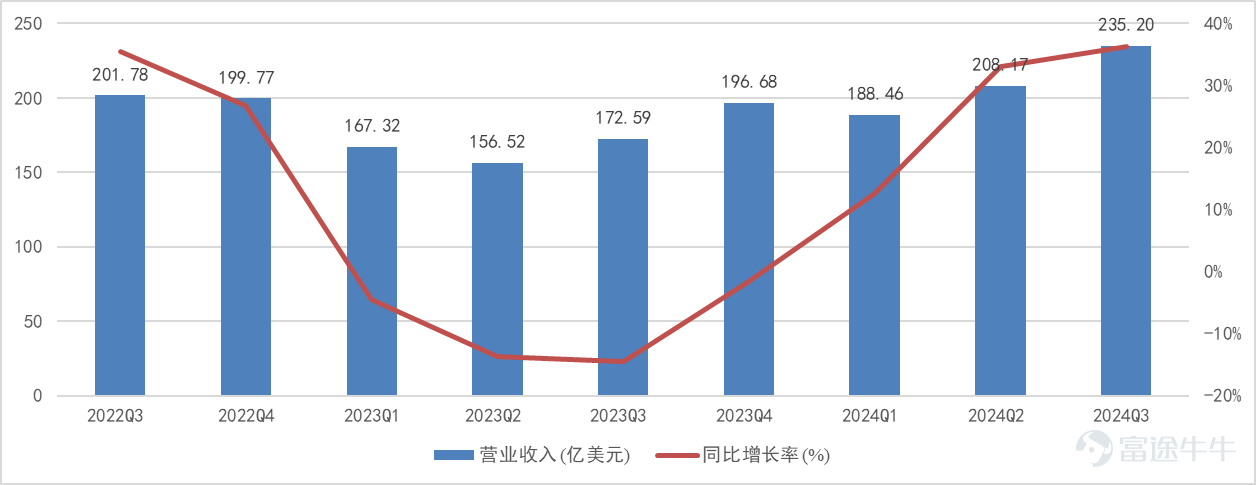

Q3淨營收爲7596.9億元臺幣,即235億美元,同比增長39%,超出預估的7510.6億元臺幣;但收入端的超預期其實已經滯後,因台積電每月度銷售額的公佈,市場對這一數字早已心中有數。更值得關注的是收入端的拆分,即收入的需求動力以及均價的提升。

圖:台積電營業收入情況

資料來源:公司公告,富途證券整理

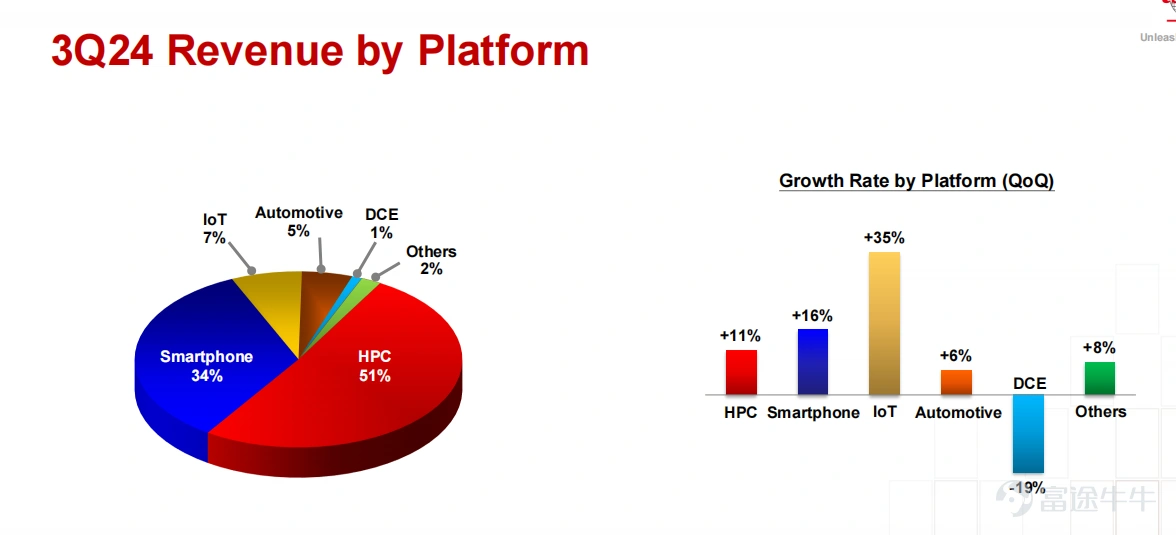

從收入端的拆分來看,高性能計算平台佔比爲51%,智能手機收入佔比爲34%。與上季度相比,AI需求仍然非常旺盛,季度環比增長11%;而智能手機的季度環比增長達到了16%(上季度爲-1%),佔比有1%的提升,表明智能手機需求正在逐季恢復。

圖:台積電分平台銷售額情況

資料來源:公司公告,富途證券整理

鑑於 Apple Intelligence 在其主要 iPhone產品中分階段推出,買家仍保持謹慎,蘋果公司的iPhone 16 發佈會並未引發近期 AI 智能手機的上升週期。不過全球智能手機銷售的疲軟逐漸減弱,Canalys報告第三季全球智能手機出貨量按年增長5%,連續四個季度實現增長。

圖:智能手機出貨量統計數據

資料來源:Canalys,富途證券整理

公司指引2024年第四季度收入261-269億美元,超出市場預期249億美元。在高性能計算領域,英偉達的Blackwell將開始量產,隨着市場預期 Blackwell 芯片將開始批量出貨,預計會提高臺積電前瞻性指引的清晰度。而AMD也發佈了3nm的新產品,從而推動台積電下季度的高性能計算收入繼續提升。

在AI需求仍然旺盛的基礎上,過去季度有所拖累的智能手機需求已經度過低谷期,開始產生正向效果。這使得台積電的四季度收入前景仍然積極。

二、先進製程帶動毛利率遠超預期

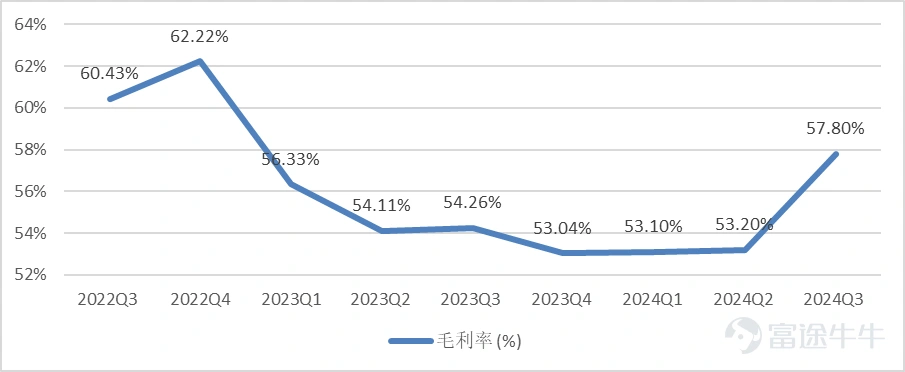

三季度毛利率重新回到 58%附近,遠高於市場預期(54.8%),環比上季度提升了4.6%。這主要得益於公司 3nm 產量繼續增加,帶動公司產品均價和毛利率的提升,以及產能利用率提高。

圖:季度毛利率情況

資料來源:公司公告,富途證券整理

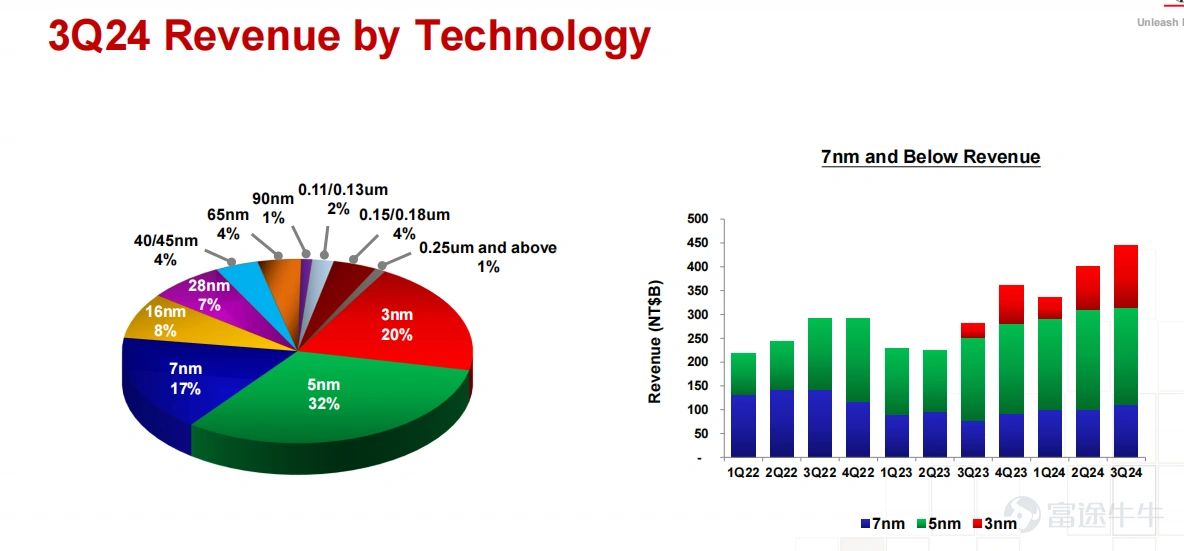

高單價的先進製程(定義爲7納米及更先進的技術)佔比持續提高,三季度先進製程佔晶圓總收入的69%,較上季度67%的佔比繼續上升,其中3納米出貨量佔晶圓總收入的20%,佔比提升了5%,尤其顯著。iPhone16全系列都將採用3nm節點,英偉達的數據中心GPU主要使用7nm和5nm製程,並正在逐步進化到3nm製程,這意味着先進製程的收入佔比仍將繼續提高。

圖:季度分技術收入情況

資料來源:公司公告,富途證券整理

公司下季度指引中毛利率也大幅超出市場預期,公司預計2024年第四季度毛利率57-59%(市場預期 54.7%),主要由於Q4較高的產能利用率抵消了N3爬坡、N5到N3的轉換成本以及臺灣上漲的電價帶來的不利影響。

而對於更長期的25年的毛利率判斷則偏複雜一些,有多重積極和不利因素互相交織。整體來說,我們依然對2025年毛利率持樂觀態度,鑑於海外工廠的收入貢獻規模較小,2025年不太可能對臺積電構成太大拖累,具體因素如下。

積極因素包括:

1)前沿技術(N3、N5和CoWoS封裝)的平均售價(ASP)提高。據 TrendForce 報道,TSM計劃將其 3nm 芯片的價格提高 5% 以上,而先進封裝價格預計明年將上漲10%至20%。鑑於3nm佔其2024 財年第三季度收入的 20%,隨着3nm的量產繼續帶動公司產品均價的提升,對公司毛利率有正向作用。

2)工藝良率和產能利用率的提升。

3)隨着半導體庫存調整結束,N7及成熟節點的利用率有望回升。

潛在的不利因素有:

1)海外工廠明年開始產能爬坡,對毛利率有負面影響,在未來三年每年都有2~3個點的毛利率的稀釋。

2)成本通脹,特別是臺灣地區電力關稅的持續上漲。更高的電費以及通脹成本會至少稀釋台積電的毛利率1%。

3)鑑於對N3的極高需求,可能會進一步將N5產能轉換爲N3。

三、台積電基本實現了事實壟斷

當前台積電基本實現了事實壟斷,英特爾和三星面臨的挑戰增強了台積電作爲首選AI代工廠的地位。在代工領域,台積電在競爭中佔據主導地位,並在與供應商和客戶的談判中佔據了有利地位——畢竟,想要最好芯片的芯片公司幾乎沒有機會避開臺積電。

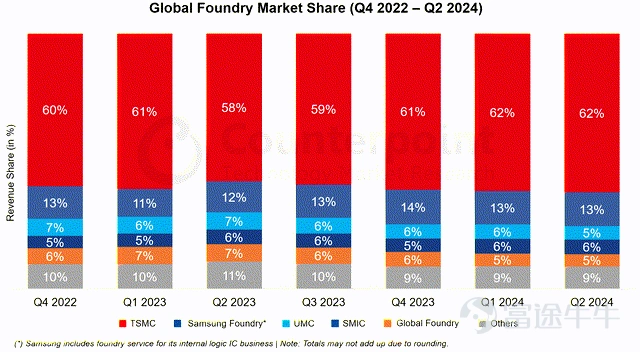

根據Counterpoint Research 的數據,台積電第二季度在全球代工市場的份額爲 62%。長期來看,隨着芯片製程進入「5納米」乃至「3納米」時代之後,由於三星已經失去市場份額,而英特爾良率不達預期。毋庸置疑,台積電很可能繼續保持明顯的市場領先地位。

當前台積電面臨的問題仍然是先進製程產能不足,在「賣方市場」格局下,台積電有可能將當前的高利潤率維持較長一段時間。

圖:全球代工市場份額情況

資料來源:Counterpoint Research ,富途證券整理

總結

本次台積電的業績表現非常不錯,不僅指引了強勁的AI需求前景且智能手機的需求也在回暖,且毛利率的回升遠超預期。作爲一家制造業企業,台積電三季度的淨利潤率高達42.8%,以強有力的事實壟斷地位確立了高利潤。

基於此背景,我們認爲25年將繼續保持較高的收入增長,毛利率仍有提高空間,預計24/25/26年營收將同比增長30%、25%和20%,分別對應營收896.8、1121.0和1345.2億美元,對應淨利潤362、493和578億美元。當前估值1.07萬億美元,對應25年淨利潤的22倍。

與美股上市半導體同業比較的角度來看,台積電的估值仍然相對便宜。但考慮到地緣政治風險的潛在不利影響,尤其是當前美國大選正進行中,風險因素的增多料在近期對臺積電的估值和投資情緒有一定折價。若估值回落至25年20倍以下的交易區間,則安全邊際更強,因此,善於交易的股東而言,可積極把握高拋低吸的機會。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論

發表評論

13

21