[Delin Institute for New Economics] The Origin and Practice of Modern Monetary Theory (1)

The Delin Institute for New Economics published the research report “The Origin and Practice of Modern Monetary Theory”, which analyzes in detail the origin of modern monetary theory in Japan and its growth in the US, and its impact on the future global economy. According to the report, we will face a world where inflation continues, and the gap between the rich and the poor will become a persistent problem that is difficult for society to cure. After the US enters the third phase of monetary theory, the dollar's dominance will be in jeopardy.

Due to its length, we have divided the research report into 5 chapters. Please read the first chapter in this series: Modern Monetary Theory and Japan's Experience.

![[Delin Institute for New Economics] The Origin and Practice of Modern Monetary Theory (1)](https://nnqimage.futunn.com/sns_client_feed/40000168/20240408/1712556752134-4a9c7bec1d.jpeg/big?area=1&is_public=true)

CHAPTER I

Modern Monetary Theory and Japan's Experience

The world economy is being Japanized, characterized by low interest rates, low inflation, low growth, high welfare, high currency, and high debt. It all started when Japan's housing bubble burst in 1990.

Bubble Burst - Falling into the Altar

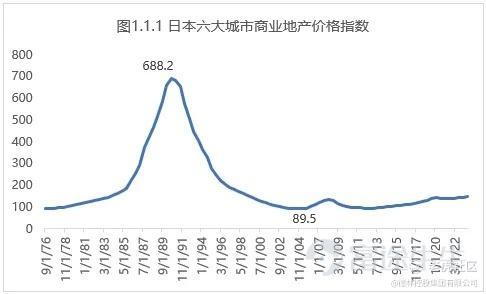

Japan's housing bubble peaked in 1990 (Figure 1.1.1), then began to decline, reaching its lowest point in 2004, with a cumulative decline of 87%.

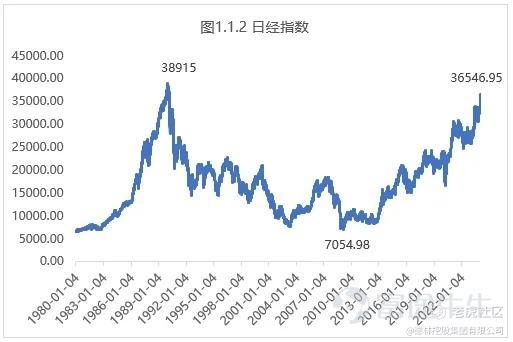

The Nikkei 225 Index peaked at 38,915 points on December 29, 1989, and then began 20 consecutive years of decline. The Nikkei 225 index did not return to its 1989 high until February 2024 (Figure 1.1.2).

Beginning in the 90s, the Japanese economy entered an era of low growth. Japan's nominal GDP growth rate in the 1990s was 2.2%, -0.6% in the 2000s, and 0.8% in the 2010s. Domestic consumption in Japan continues to be sluggish, corporate productivity growth is stagnating, and technological progress is slowing down. The economics community began discussing Japan's “lost decade,” “lost 20 years,” and “lost 30 years.”

The income level of residents in Japan was also locked at the level of the 1990s (Figure 1.1.3), and there was no breakthrough for more than 30 years since then. Corresponding to this is the simultaneous stagnation of final consumption expenditure of Japanese residents (Figure 1.1.4).

If commercial real estate falls 87%, stocks fall for 20 years, residents' income stagnates for a long time, domestic demand stops growing, and there is a risk of deflation in prices, the economic situation is conceivable. This is how the lost ten, twenty, and thirty years came about.

The Japanese government will definitely not sit idly by and ignore it; it will definitely use various methods to restore economic vitality. From a macroeconomic perspective, the solutions proposed by Japan can be divided into two categories. One is monetary policy and the other is fiscal policy.

Monetary policy — not helping

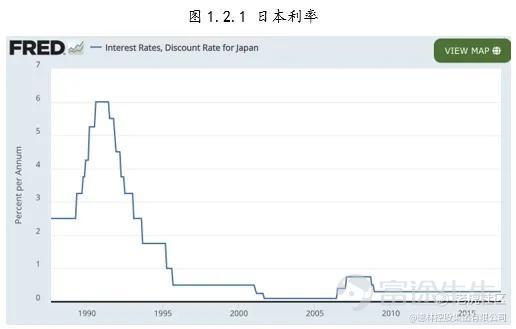

On July 1, 1991, the Bank of Japan cut interest rates for the first time, from 6% to 5.5%, beginning a shift in Japan's monetary policy from tight to loose (Figure 1.2.1). Interest rates continued to be lowered in 1992. By February 1993, they had already dropped to 2.5%, reaching the level of the bubble period, and still not doing anything good. The amount of loans from Japanese financial institutions is still declining. The M2 growth rate even fell negative in the fourth quarter of 1992 (Figure 1.2.2).

Japan's experience shows that central bank intervention in monetary policy is effective during periods of austerity, because the central bank can either raise interest rates or directly recover the base currency. However, when the central bank wanted to expand its currency, it had no tools at its disposal, because the government could not force ordinary people and businesses to borrow money. Europe and America later faced the same problem; they were only able to rely on fiscal policies to stimulate the economy.

Fiscal Policy - Maintaining the Economy

In 1995, the Japanese government introduced an economic stimulus package of 115.7 billion US dollars. Due to reduced taxes and increased spending, the Japanese government deficit rose sharply, and government debt as a share of GDP began to grow rapidly (Figure 1.3.1). The Japanese government deficit reached 65% of GDP in 1996, an increase of 10 percentage points over 1994. The economy improved slightly. In 1997, the Japanese government tried to restructure its finances, including raising the consumption tax, removing tax incentives, and cutting government spending. As a result, the economy deteriorated again, and had to stop austerity and continue to stimulate the economy.

On April 20, 1998, the Japanese government once again announced the largest stimulus plan in history, totaling 128.1 billion US dollars. The government began cutting taxes and building a large number of public works at the same time, including national highways, fishing ports, bridges, leveling arable land, etc., but there is still no inflation in the Japanese economy. Since then, Japan's government debt as a share of GDP has risen wildly.

In March 2001, the Bank of Japan first introduced quantitative easing. The central bank purchased large quantities of Japanese long-term treasury bonds to provide liquidity to the market. This movement continued until 2006, when government debt reached 129% of GDP (Figure 1.3.1). This move greatly eased the fiscal pressure on the Japanese government; this was the monetization of the fiscal deficit, which was later hotly debated.

Driven by the fiscal deficit monetization policy, the decline in the leverage ratio of Japanese companies was offset by an increase in the leverage ratio of government departments (Figure 1.3.2), and Japan maintained a stable economy and manageable inflation. This also gave birth to two economic theories: balance sheet recession theory and modern monetary theory (discussed in detail in section 2). They all found evidence from Japan's experience, and provided theoretical support for the Federal Reserve's monetary release in 2008. However, we believe that both theories overlook some important factors. We'll discuss this in more detail in later sections.

Abenomics — a huge success?

In December 2012, Abe became Japan's prime minister again. In order to continue to stimulate the economy, he proposed the “Three Arrows” reform plan. The first arrow targets monetary policy, requiring the central bank to drastically relax the currency until it reaches the 2% inflation target and appoints a new central bank governor Haruhiko Kuroda to implement his ideas; the second arrow targets fiscal policy and announced a $226.76 billion stimulus plan in January 2013 to continue expanding public investment; and the third arrow targets structural reforms, including encouraging innovation and enhancing the competitiveness of Japanese companies through introducing competition. The first two arrows have been implemented, and the third one has come to an end because it is much more difficult to adjust benefits than printing money.

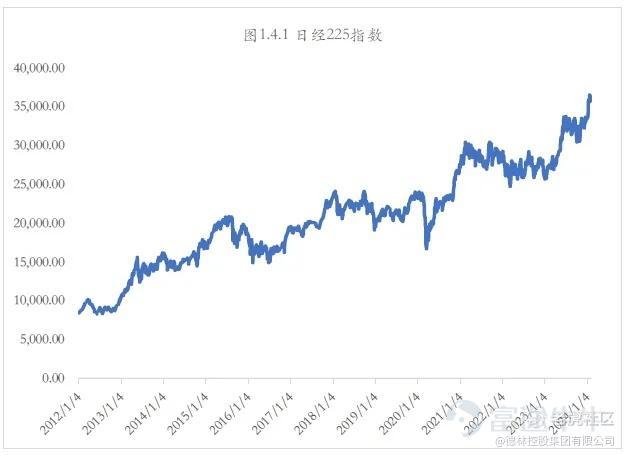

On February 16, 2016, the Bank of Japan began implementing negative interest rates, and introduced a fiscal stimulus plan of 28 trillion yen in the same year. Abenomics was a huge success! The Nikkei 225 Index rose from 10,000 points when Abe came to power to 36,000 points in February 2024 (Figure 1.4.1), with an average annual increase of 12.5%.

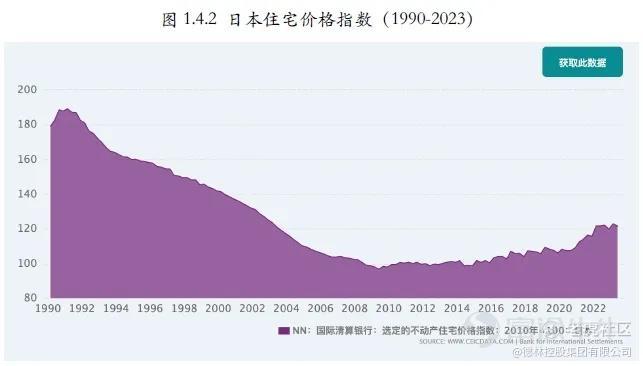

Housing prices in Japan also began to rise in 2013, and the national actual residential property price index rose from 100 to 123, ending the continuous decline since 1990 (Figure 1.4.2).

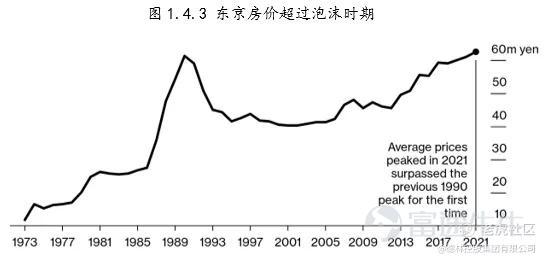

The image above uses the average housing price in Japan, which is very confusing. In fact, due to the influence of Abenomics, housing prices in the Tokyo area in 2021 have already surpassed the high in 1990. According to data released by the Japan Real Estate Economic Institute (Real Estate Economic Institute) on January 25, 2022, the average price of new apartments in the Japanese capital and surrounding areas reached 62.6 million yen each in 2021 (Figure 1.4.3), surpassing the historical high of 61.2 million yen set during the peak of Japan's economic bubble in 1990.

Since the implementation of Abenomics in 2013, government bonds held by the Bank of Japan have increased fivefold. The Bank of Japan held 113 trillion yen in government bonds in January 2013, and 593 trillion yen in January 2024 (Figure 1.4.4). The share of government bonds held by the Bank of Japan rose from 11.4% to 54%. Although the Bank of Japan has yet to buy bonds directly from the Ministry of Finance, it has become the largest creditor of the Japanese government, and there is only a thin layer of cover between directly purchasing Ministry of Finance bonds.

After the implementation of Abenomics, the property market rose and the stock market rose, just like singing and dancing leveled off. Moreover, with such crazy money printing, Japan's inflation rate has always been around 0, and Japan seems to have found a way to develop its economy. However, all of this is based on the Japanese government's massive increase in base currency (Figure 1.4.5). When Abenomics began to be implemented at the end of 2012, Japan's basic money supply was 132 trillion yen. At the end of 2023, Japan's basic money supply rose to 665 trillion yen, an average annual increase of 15.8%. This is the basis for rising property prices and stock prices in Japan.

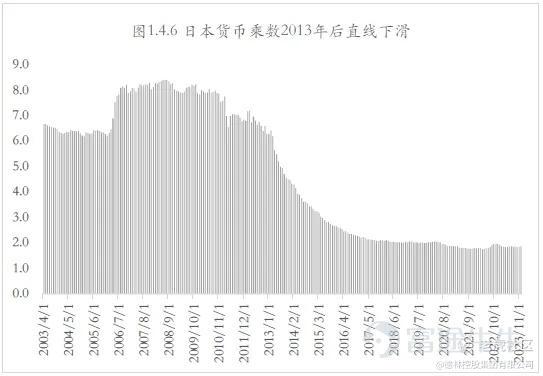

Meanwhile, Japan's currency multiplier declined sharply after 2013 and fell to around 2 in 2016 (Figure 1.4.6). This is a typical zombie economy. In other words, after leaving the central bank, the money is borrowed once by the enterprise and deposited into a deposit account. Money has not reached ordinary people at all, nor has it entered the economic cycle; it basically flows directly into the stock market or property market.

In 2016, the Washington Post published an article “The World Economy Is Being Japanized”. The article indicates that the world economy is shifting to the Japanese model, which is characterized by low interest rates, low inflation, low growth and high welfare, high currency, and high debt. With the gradual Japanization of financial policies in European and American countries, studying Japan once again became explicit, and two major theories were born. One is Gu Chaoming's balance sheet decline theory, and the other is the modern monetary theory represented by Randall Ray. They can all find evidence of Japan's economic performance over the past 30 years.

The lost 30 years gave birth to two major theories

(1) Balance sheet decline theory

The balance sheet recession theory answers two questions: first, it explains why monetary easing was not effective for Japan's economy after the crisis; second, it explains why the government should actively spend through fiscal policies to offset the economic contraction caused by corporate and household repayments.

Japan's housing bubble burst in 1990, and the fall in asset prices in Japan was equivalent to three times the 1989 GDP. Almost all households and businesses participated in this game.

If you were one of them and faced falling prices for the commercial real estate you bought, what would you do? If you are a business with poor cash flow, and asset prices plummet, you may have to directly declare bankruptcy. But because large Japanese companies and banks are inextricably linked, they can help you maintain harmony on the surface.

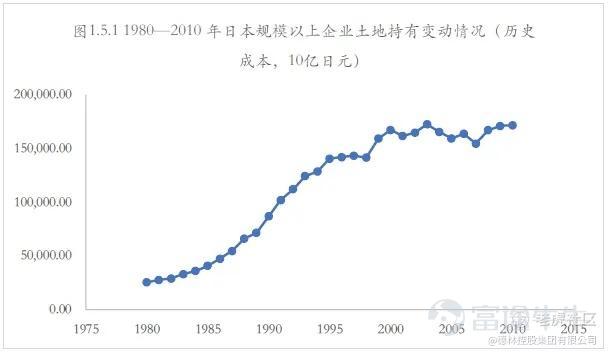

As shown in Figure 1.5.1, it is clear that real estate prices in Japan crashed in 1990, and land should have depreciated drastically. However, according to the accounting standards of Japanese companies, land values are recorded according to historical costs. Judging from public information, the company's assets are still healthy, but both the operator and the bank know what happened; they are probably already insolvent.

However, Japanese companies were still very competitive at the time. The automobiles and electronic products they produce have a large global market and can continue to bring positive cash flow. Under such circumstances, it is a rational choice for Japanese companies to stop borrowing and try to make money to repay bank debts. So, no matter how low bank interest rates fall, they won't borrow money anymore. Businesses and households throughout the 90s worked hard to produce and concentrate on paying off debts.

Ku Chaoming believes that this is the reason why Japan's monetary policy is not working. He summed up this phenomenon as: the goal of an enterprise starts fromThe biggest profitTransform intoDebt minimization. In fact, it's about quickly saving companies from the quagmire of insolvent debt through healthy cash flow.

How serious were the bad debts of Japanese companies at the time? In July 1995, the Japanese government published the “White Paper on the Japanese Economy”, which estimates that Japan's non-performing debt balance was 12.5 trillion yen. In fact, non-performing debt at that time was probably 100 trillion yen, accounting for 20% of GDP. The reason is that the Bank of Hyogo of Japan went out of business in August 1995, and it was announced before it went bankruptNon-performing loans are 60.9 billion yenThe government's statistics of 12.5 trillion non-performing loans are based on this kind of data published by banks. As a result, after clearing the Bank of Hyogo, it was discovered that his bad debt was 790 billion yen.Add the non-performing debts of affiliated companies totaling 1,500 billion yen. Other financial institutions are in a similar situation, and their operating conditions are very opaque.

In 1998, Japan established a special Financial Services Office to deal with non-performing debts. The amount of bad debt self-inspected by banks still accounted for 17% of Japan's GDP back then. After that, Japan began to focus on using fiscal policies to stimulate the economy and maintain the apparent harmony of the Japanese banking industry. This is the big background for the birth of the balance sheet recession theory.

Businesses and households are saving money to pay off debts. No one is spending, and the economy will definitely shrink or even collapse, so the government must borrow money to spend.

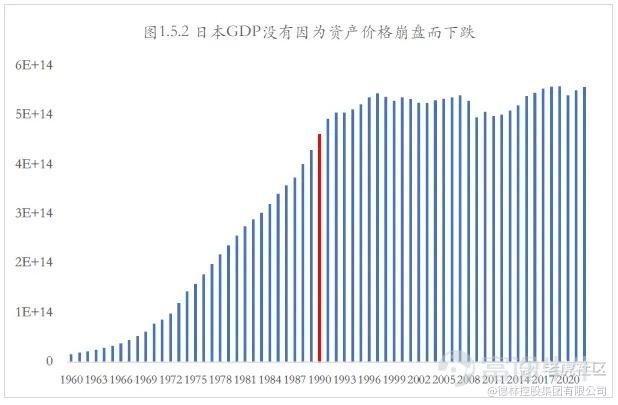

The balance sheet recession theory explains why the government must stimulate the economy through fiscal policies. Ku Chaoming believes that it is precisely because the Japanese government borrowed money to spend to offset the impact of corporate and household deposit repayment, that Japan did not experience an economic collapse when asset prices fell sharply, and GDP remained above the bubble level (Figure 1.5.2).

Ku Chaoming also said, “This is a credit to Japan's fiscal policy. Because as long as GDP remains at the bubble level, residents and businesses will have money to pay off their debts.

On the other hand, the balance sheet recession theory also explains why it took Japan 20 years to get out of trouble. Because every time Japan provides fiscal stimulus, the economy improves. Once the economy improves, the Japanese government will begin discussions on reducing stimulus, but once the stimulus is cut and taxes are raised, the economy immediately begins to decline, so it is necessary to start stimulating again. This iterative process has extended the balance sheet repair time.

Ku Chaoming believes that if the Japanese government recognizes the balance sheet recession theory from the beginning, it can shorten the economic recovery process from 20 to 10 years.

(2) Modern monetary theory

Taking the balance sheet recession theory one step further is modern monetary theory.

The policy suggestion brought about by the balance sheet recession theory is that businesses and households are saving money to pay off debts, and the government should borrow money to spend; otherwise, the economy will collapse and fall into an even greater disaster. The money spent by the government can be raised through fiscal deficits (Gu Chaoming believes that even in the era of credit money, central banks must still operate according to the logic of the gold standard, and the central bank must implement a responsible monetary policy).

Modern monetary theory describes from an accounting perspective how governments finance and spend through fiscal deficits, and why such deficit consumption is reasonable. More frankly, modern monetary theory has torn the shield between central banks and the Ministry of Finance, providing a rational explanation for the actions of the Japanese government.

Modern monetary theory has the following core arguments:

First, the government does not collect taxes before spending money; instead, it spends money first and then returns the currency by collecting taxes.

Second, as a monopoly currency issuer, the sovereign currency government will not default on bonds denominated in local currency (the financial crises in Southeast Asia and South America all defaulted on US dollar bonds). Government spending is limited only by resources (inflation); it is not constrained by finances.

Third, the government's fiscal deficit is equal to the net financial assets of the non-government sector, so increasing the fiscal deficit rate can reduce the non-government sector's debt ratio.

Fourth, Japan's experience shows that fiscal deficits do not necessarily lead to inflation. Japan has been in deficit since 1993, and there is no inflationary pressure.

Based on the above four points, supporters of modern monetary theory believe that government budgets should be functional and pursue full employment, sustainable growth, environmental sustainability, etc.

This deduction was welcomed by some politicians because the theory not only satisfies voters' needs, but also doesn't have to worry about where the money comes from. Former US presidential candidate Bernie Sanders appointed Stephanie Kelton, a supporter of modern monetary theory, as her economic advisor. Stephanie Kelton also served as chief economist on the US Senate Budget Committee. This move has taken modern monetary theory from the margins to the “temple.”

The problem is,Can printing money really solve all economic problems?

We'll continue the discussion in the next section!

Disclaimers

This article is for reference only. Investors should only rely on the information contained in the company announcement to make investment decisions.

No one may reprint without the authorization of this public account.

The content covered by Futu is for reference only. The copyright belongs to Delin Holdings and related content providers. For the disclaimer, see Delin Holdings official website:https://www.dl-holdings.com/

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.

Read more

Comment

Sign in to view/post comments

DL HOLDINGS GP

The official account of Delin Holdings Group Limited

Delin Holdings is a financial services group headquartered in Hong Kong. It holds SFC license No. 1/4/6/9 and provides global family wealth management and investment banking services to ultra-high net worth families.

27K

Followers

19K

Visitors

Follow

Market Insights

HK Tech and Internet Stocks HK Tech and Internet Stocks

Stocks of companies primarily involved in technology and internet sectors in the HK stock market. Stocks of companies primarily involved in technology and internet sectors in the HK stock market.

View More

Nancy Pelosi Portfolio Nancy Pelosi Portfolio

Former U.S. House Speaker Pelosi, renowned as the "Stock Market Queen" in politics, concentrates her investment portfolio on tech giants in AI and semiconductors. Her core strategy involves purchasing call options for leveraged trading to maximize potential returns. Former U.S. House Speaker Pelosi, renowned as the "Stock Market Queen" in politics, concentrates her investment portfolio on tech giants in AI and semiconductors. Her core strategy involves purchasing call options for leveraged trading to maximize potential returns.

Hot Topics Hot Topics

Tariff game between the US and Europe shakes the market! Will TACO happen again?

Amidst the global market turbulence triggered by the US-Europe dispute over Greenland, a single post by Trump instantly reversed market tren

Futubull Options Sir

Jan 19 17:47

Options Weekly 0119 | Greenland tariff standoff, gold and silver surge again, shocking reversal in Fed chair nominee! Watch Intel, Netflix earnings reports

年頭旺到年尾

Jan 25 15:05

2026 Futu Creators Conference